0% found this document useful (0 votes)

58 views6 pagesClass Example Solution

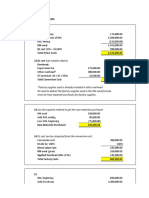

The document discusses the calculation and allocation of manufacturing overhead costs. It provides budgeted and actual overhead amounts, direct labor costs, and inventory balances. It then shows three approaches to allocating under-absorbed overhead: [1] prorating it to work in process, finished goods and cost of goods sold accounts based on their ending balances, [2] prorating it based on the overhead already included in the ending inventory accounts, and [3] an immediate write-off to cost of goods sold.

Uploaded by

PASCHAL IBELECopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as XLSX, PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

58 views6 pagesClass Example Solution

The document discusses the calculation and allocation of manufacturing overhead costs. It provides budgeted and actual overhead amounts, direct labor costs, and inventory balances. It then shows three approaches to allocating under-absorbed overhead: [1] prorating it to work in process, finished goods and cost of goods sold accounts based on their ending balances, [2] prorating it based on the overhead already included in the ending inventory accounts, and [3] an immediate write-off to cost of goods sold.

Uploaded by

PASCHAL IBELECopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as XLSX, PDF, TXT or read online on Scribd

/ 6