0% found this document useful (0 votes)

73 views2 pagesHindustan Zinc Sales & Profit Analysis

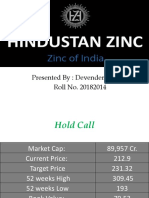

Hindustan Zinc Limited is the world's second largest zinc producer and one of the leading global producers of lead and silver. Its revenues in FY2020 were ₹18,561 crore. While sales increased from 2016 to 2018, there was a decline in sales in 2019 and 2020 due to lower metal premium prices and the impact of the COVID-19 pandemic. Similarly, net profits rose from 2016 to 2018 but then decreased in 2019 and 2020 as sales declined and expenses such as depreciation and employee benefits increased. Overall the company's performance has been good but has been adversely impacted by global economic conditions.

Uploaded by

Jay SharmaCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as DOCX, PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

73 views2 pagesHindustan Zinc Sales & Profit Analysis

Hindustan Zinc Limited is the world's second largest zinc producer and one of the leading global producers of lead and silver. Its revenues in FY2020 were ₹18,561 crore. While sales increased from 2016 to 2018, there was a decline in sales in 2019 and 2020 due to lower metal premium prices and the impact of the COVID-19 pandemic. Similarly, net profits rose from 2016 to 2018 but then decreased in 2019 and 2020 as sales declined and expenses such as depreciation and employee benefits increased. Overall the company's performance has been good but has been adversely impacted by global economic conditions.

Uploaded by

Jay SharmaCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as DOCX, PDF, TXT or read online on Scribd

/ 2