67% found this document useful (3 votes)

1K views4 pagesISA 560: Handling Subsequent Events

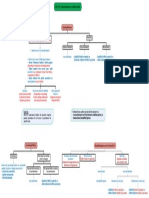

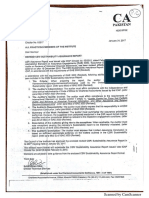

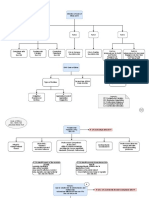

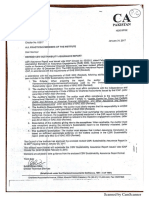

The document summarizes the auditor's responsibilities with respect to subsequent events according to ISA 560. It outlines the timeline of events from the end of the reporting period through the issuance of the financial statements and auditor's report. It discusses the auditor's procedures if subsequent events are identified before or after the date of the auditor's report and the impact on the financial statements and auditor's report. The document also provides examples of how the auditor's report would be modified depending on whether the financial statements are amended or not.

Uploaded by

saqlain khanCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as PDF, TXT or read online on Scribd

67% found this document useful (3 votes)

1K views4 pagesISA 560: Handling Subsequent Events

The document summarizes the auditor's responsibilities with respect to subsequent events according to ISA 560. It outlines the timeline of events from the end of the reporting period through the issuance of the financial statements and auditor's report. It discusses the auditor's procedures if subsequent events are identified before or after the date of the auditor's report and the impact on the financial statements and auditor's report. The document also provides examples of how the auditor's report would be modified depending on whether the financial statements are amended or not.

Uploaded by

saqlain khanCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as PDF, TXT or read online on Scribd

/ 4