0% found this document useful (0 votes)

2K views11 pagesComprehensive Project

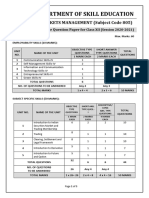

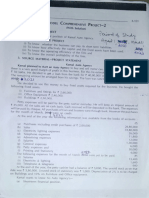

The document provides details of a case study for Arvind Auto Agency, including:

1) The objectives of analyzing the agency's financial position are to assess short-term solvency, operational efficiency, and overall profitability.

2) Facts about the agency's founding, including a loan taken and assets purchased.

3) Transactions during the year, including purchases, sales, and expenses.

4) Steps that will be taken to analyze the agency's performance through preparing financial statements and using ratio analysis.

Uploaded by

AKSH NAGARCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

2K views11 pagesComprehensive Project

The document provides details of a case study for Arvind Auto Agency, including:

1) The objectives of analyzing the agency's financial position are to assess short-term solvency, operational efficiency, and overall profitability.

2) Facts about the agency's founding, including a loan taken and assets purchased.

3) Transactions during the year, including purchases, sales, and expenses.

4) Steps that will be taken to analyze the agency's performance through preparing financial statements and using ratio analysis.

Uploaded by

AKSH NAGARCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as PDF, TXT or read online on Scribd

/ 11