0% found this document useful (0 votes)

192 views2 pagesConsignment Sales Notes

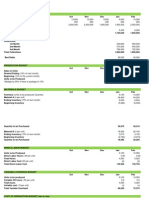

The document discusses consignment sales between a principal and an agent. Under consignment sales, the principal transfers merchandise to the agent without transferring ownership, and the agent sells the goods on behalf of the principal for a commission. The agent does not recognize the consigned inventory but instead records a memo entry. Revenue is recognized by the principal only after the agent notifies the principal of a sale and remits the sales cash. Expenses paid by each party relating to the consigned goods are capitalized to the inventory balance. The principal and agent use accounting entries to track inventory, sales, commissions, and payments between them for the consigned goods.

Uploaded by

Sittiehaina GalmanCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as DOCX, PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

192 views2 pagesConsignment Sales Notes

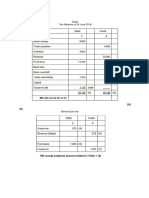

The document discusses consignment sales between a principal and an agent. Under consignment sales, the principal transfers merchandise to the agent without transferring ownership, and the agent sells the goods on behalf of the principal for a commission. The agent does not recognize the consigned inventory but instead records a memo entry. Revenue is recognized by the principal only after the agent notifies the principal of a sale and remits the sales cash. Expenses paid by each party relating to the consigned goods are capitalized to the inventory balance. The principal and agent use accounting entries to track inventory, sales, commissions, and payments between them for the consigned goods.

Uploaded by

Sittiehaina GalmanCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as DOCX, PDF, TXT or read online on Scribd

/ 2