0% found this document useful (0 votes)

7 views5 pagesAccounts Ch-4 Notes

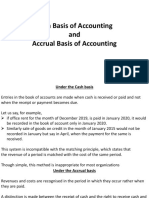

The document explains the Cash Basis and Accrual Basis of Accounting, highlighting their definitions, advantages, and disadvantages. Cash Basis records transactions only when cash is received or paid, while Accrual Basis records transactions when they are earned or incurred, regardless of cash flow. It also compares both methods, noting that Accrual Basis provides a more accurate financial picture and is required by law for companies.

Uploaded by

Ashish DokaniaCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

7 views5 pagesAccounts Ch-4 Notes

The document explains the Cash Basis and Accrual Basis of Accounting, highlighting their definitions, advantages, and disadvantages. Cash Basis records transactions only when cash is received or paid, while Accrual Basis records transactions when they are earned or incurred, regardless of cash flow. It also compares both methods, noting that Accrual Basis provides a more accurate financial picture and is required by law for companies.

Uploaded by

Ashish DokaniaCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as PDF, TXT or read online on Scribd

/ 5