Downloaded 390 times

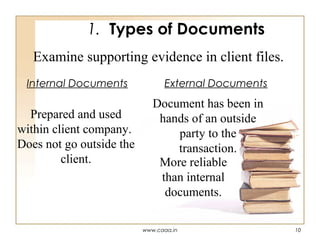

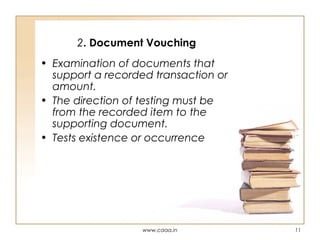

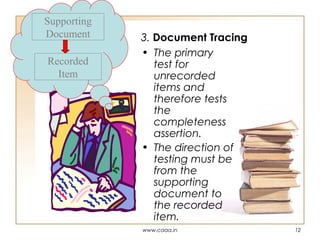

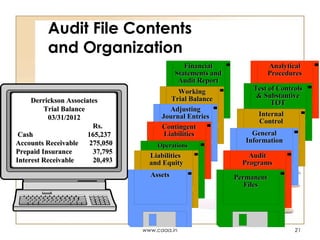

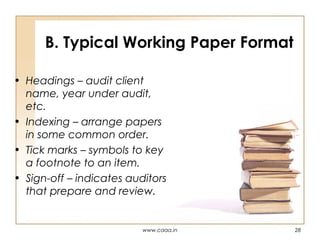

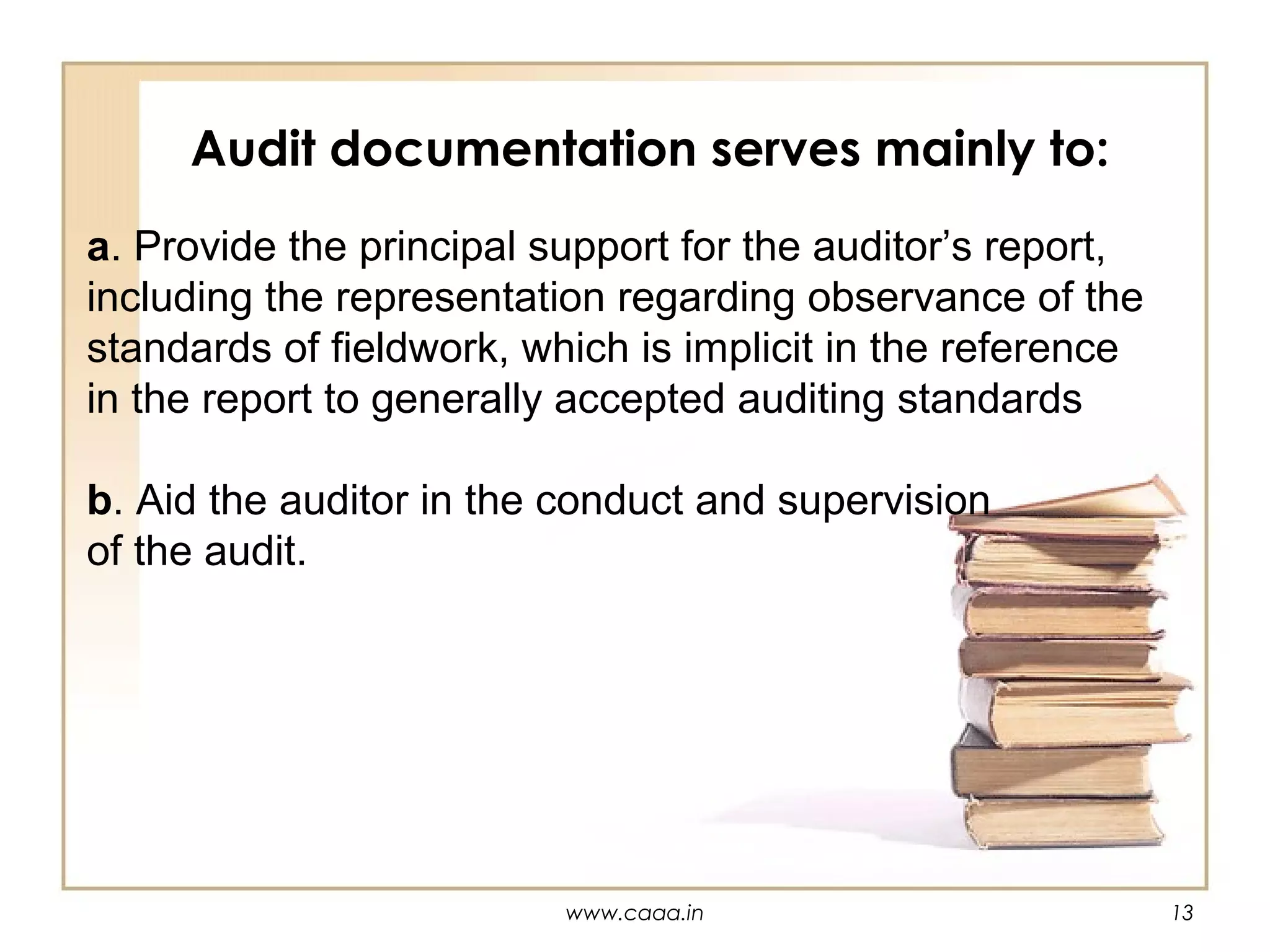

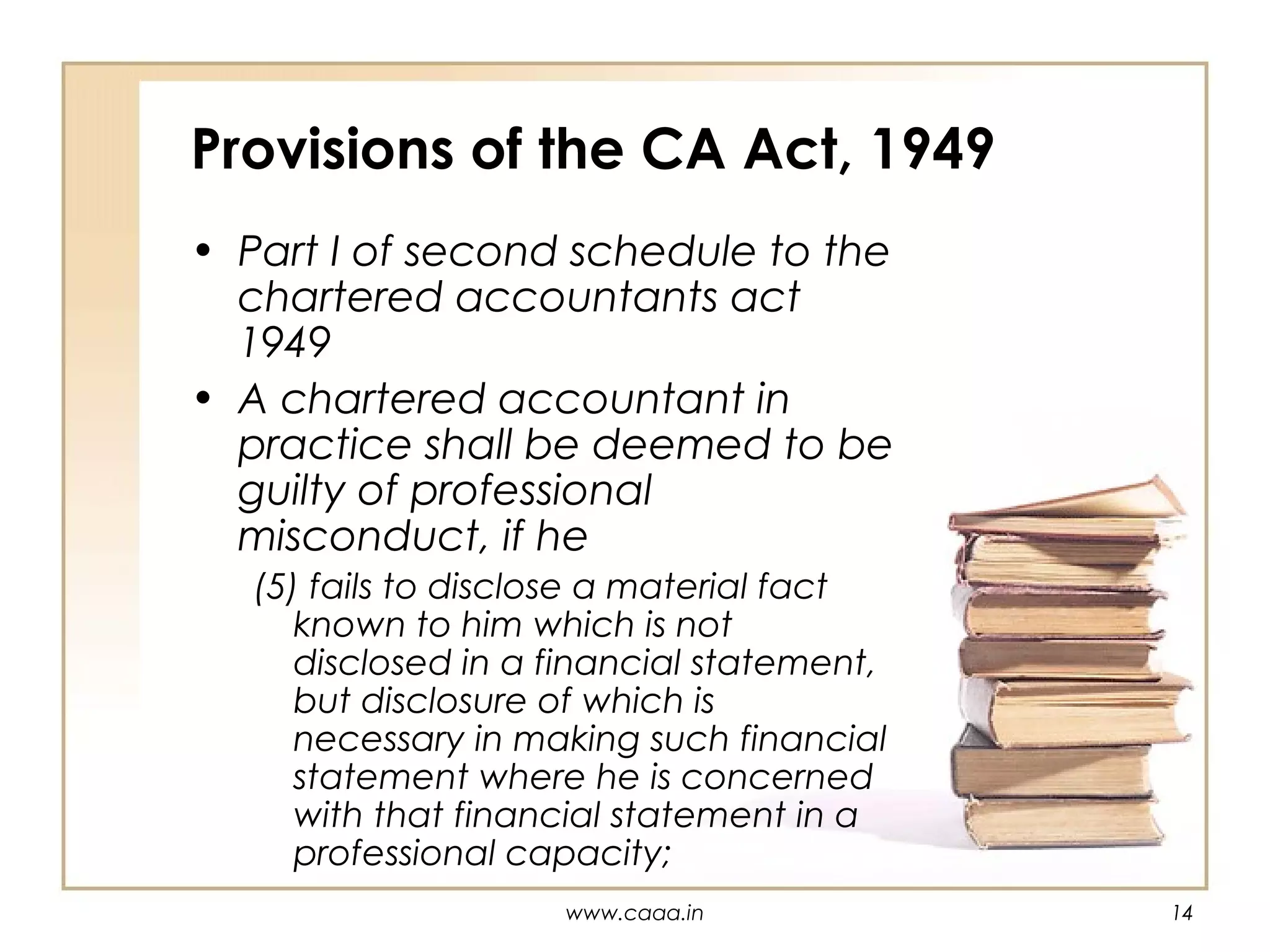

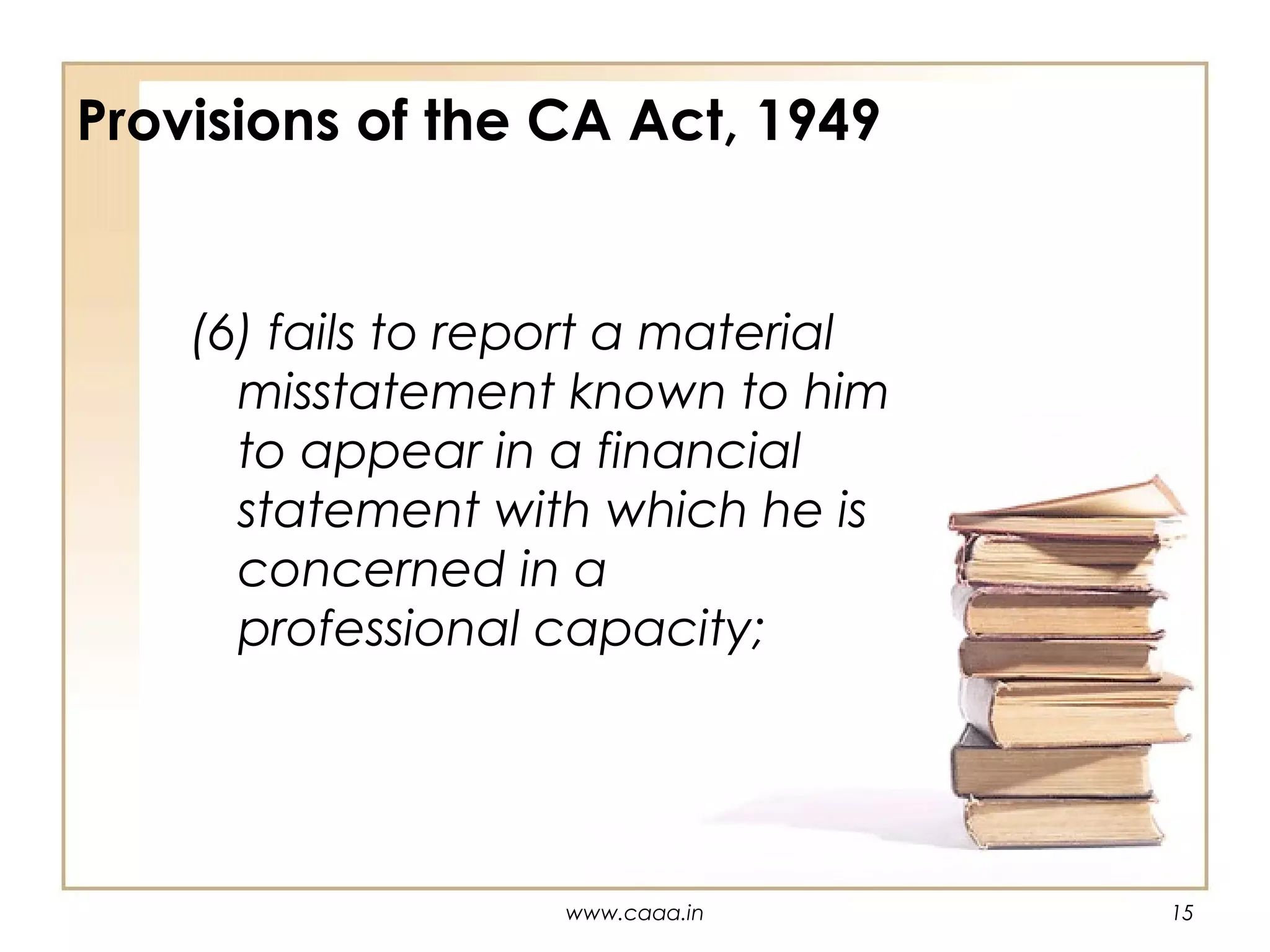

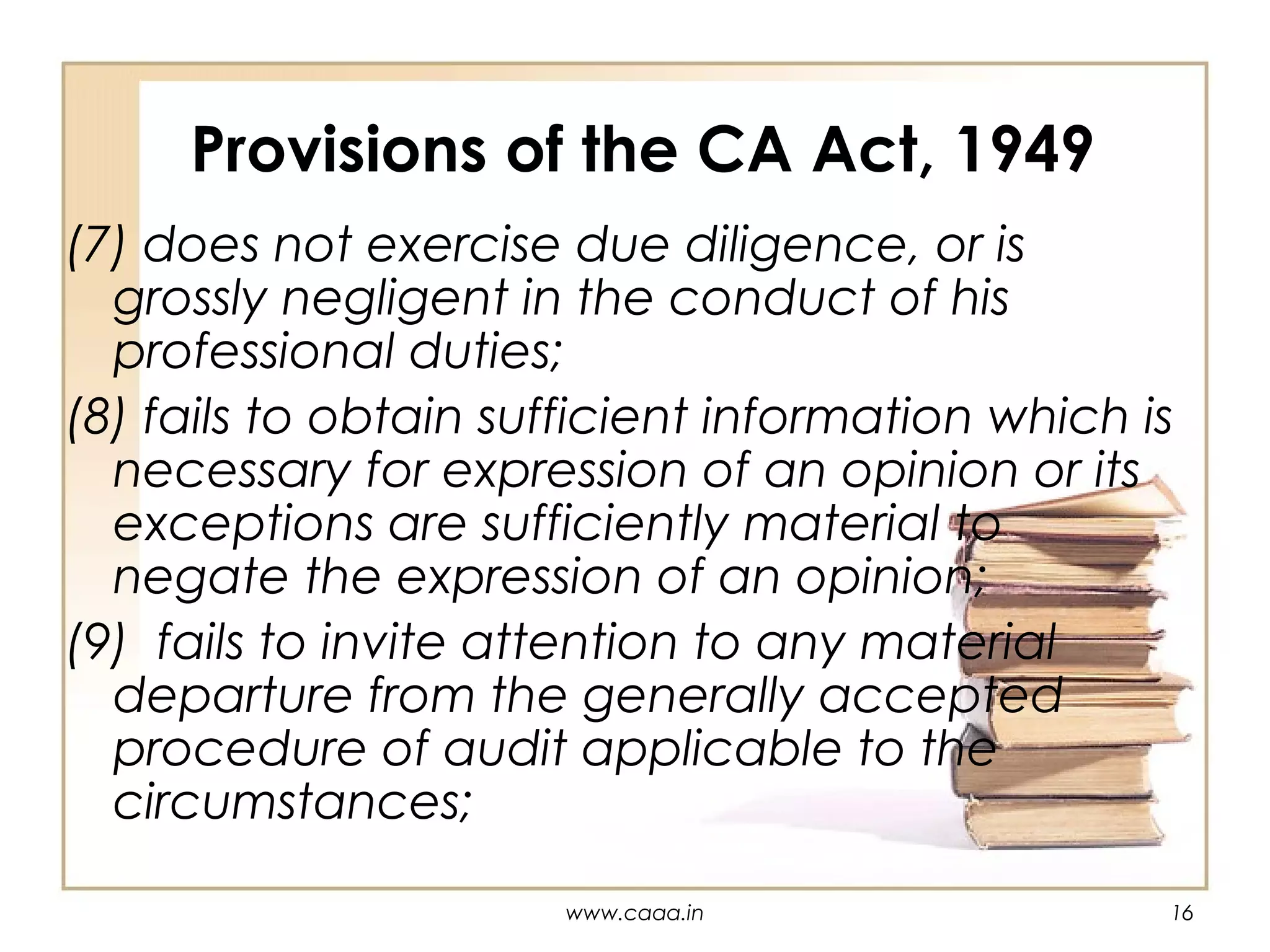

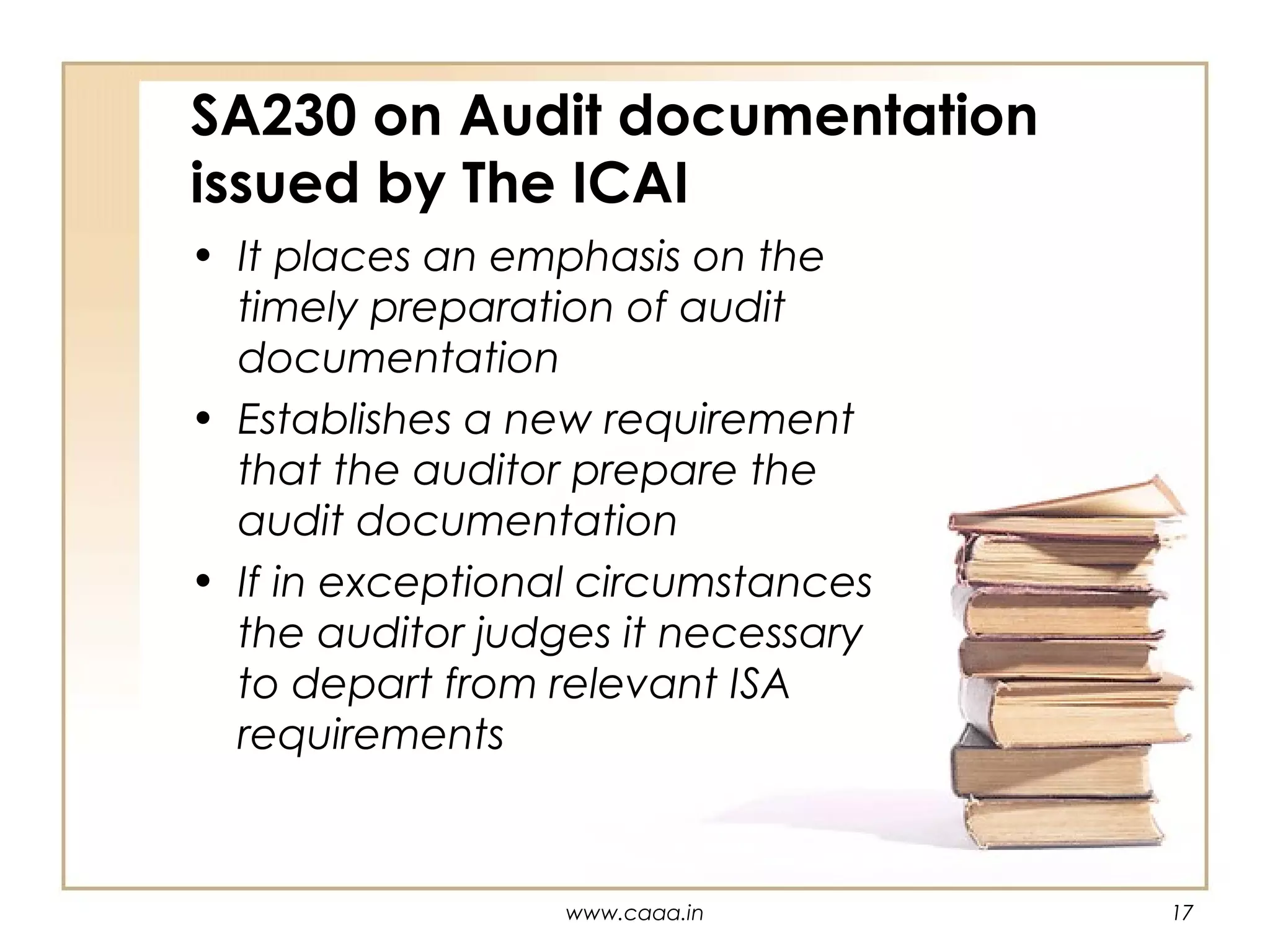

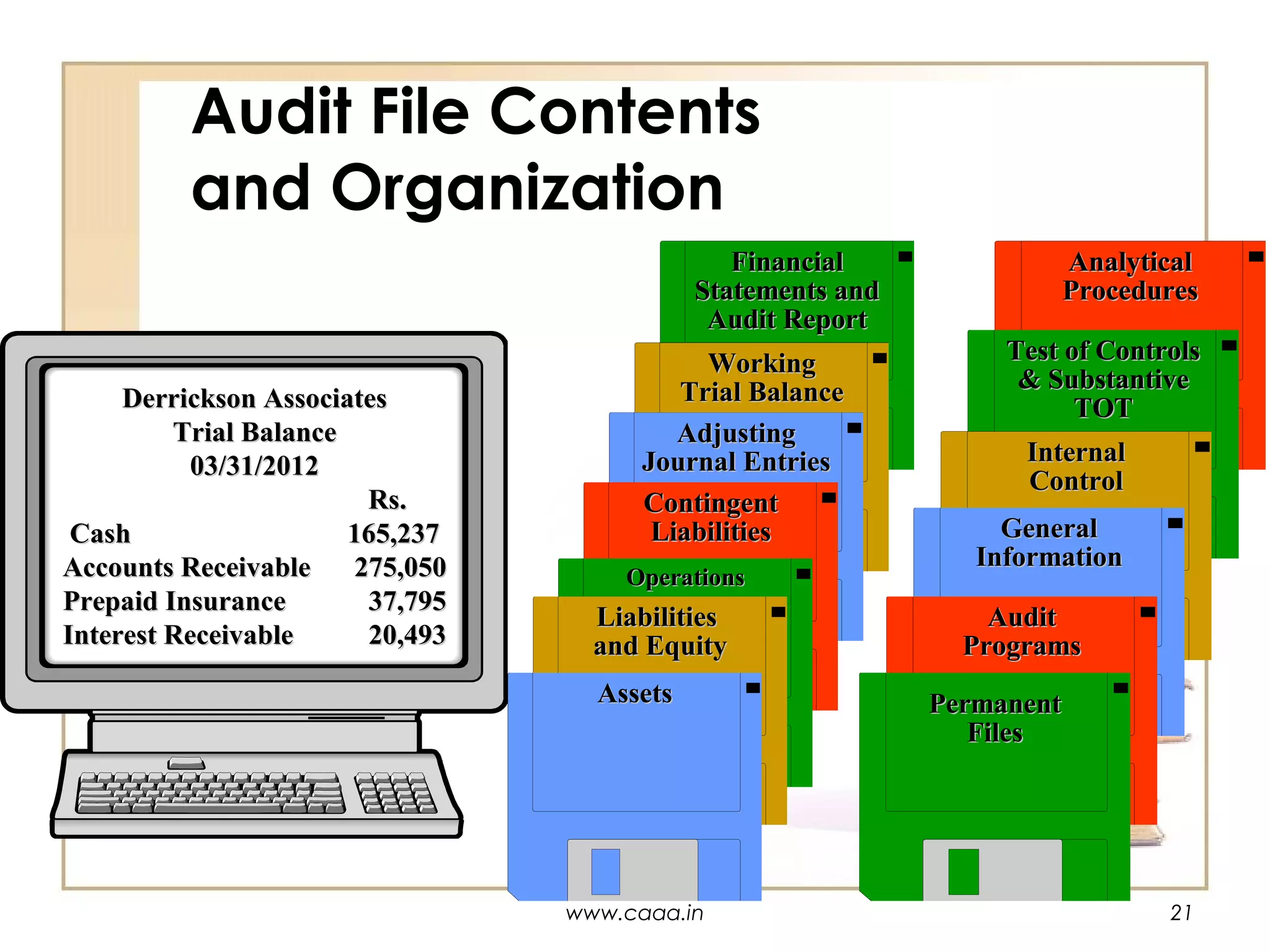

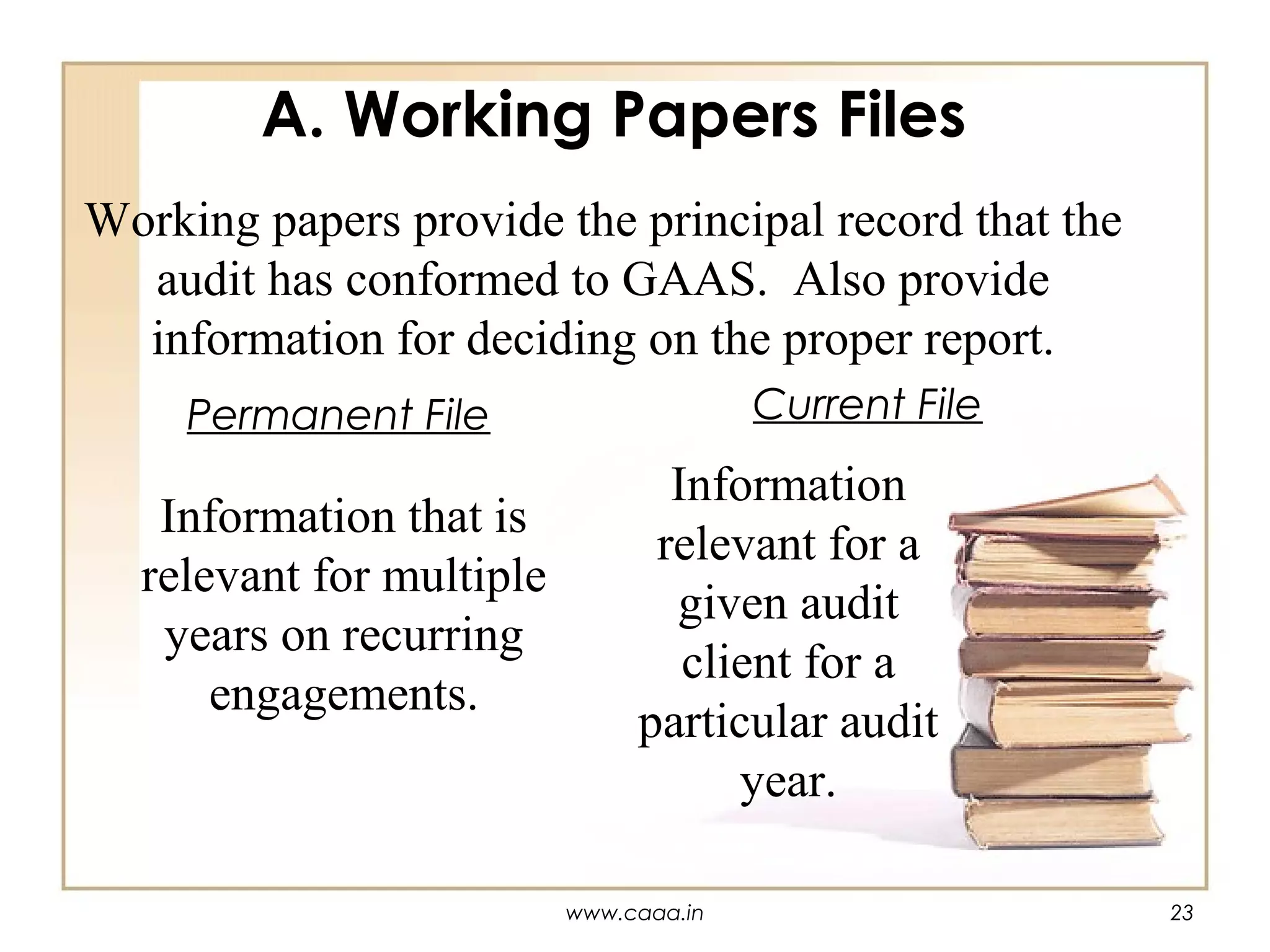

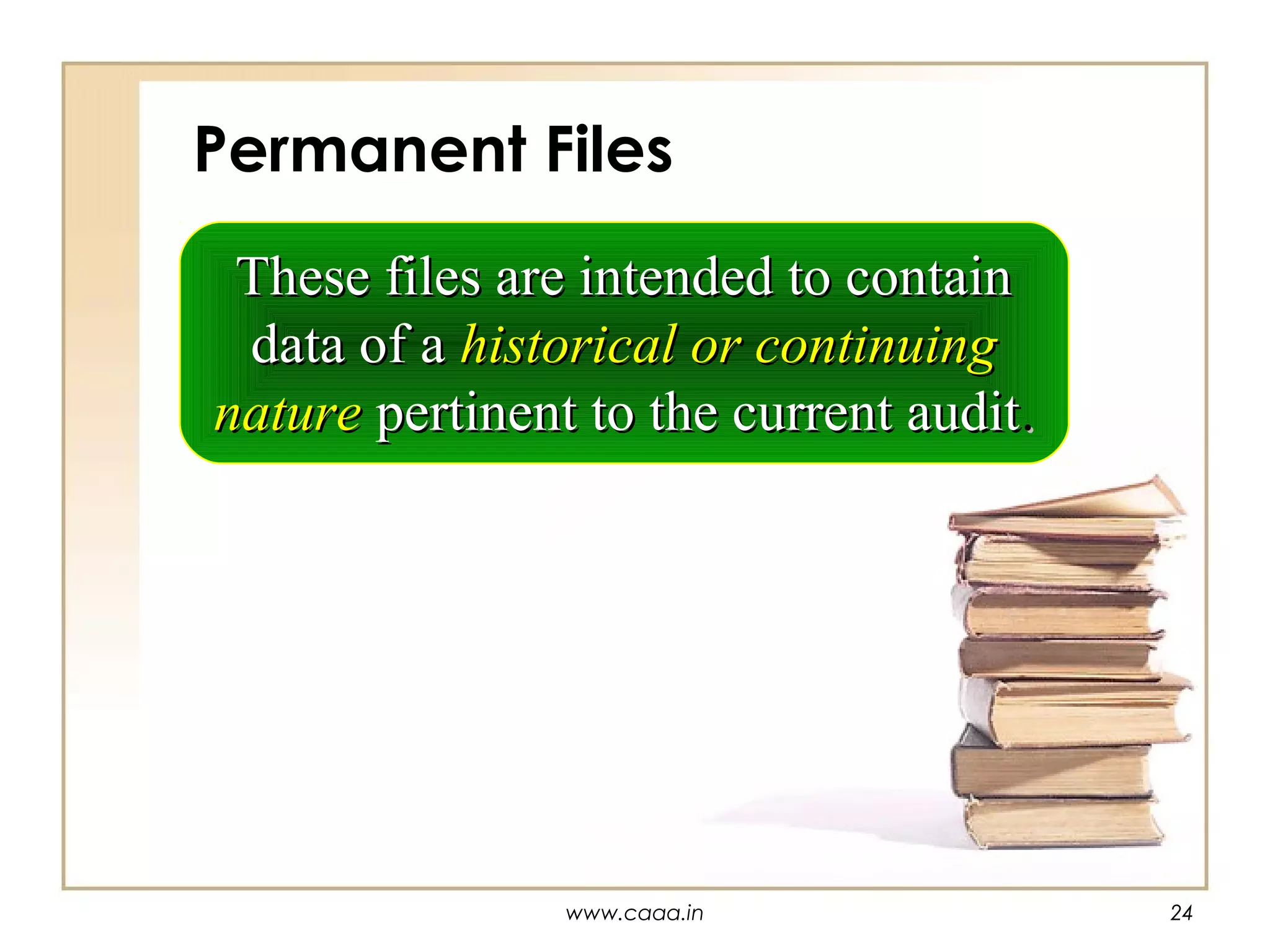

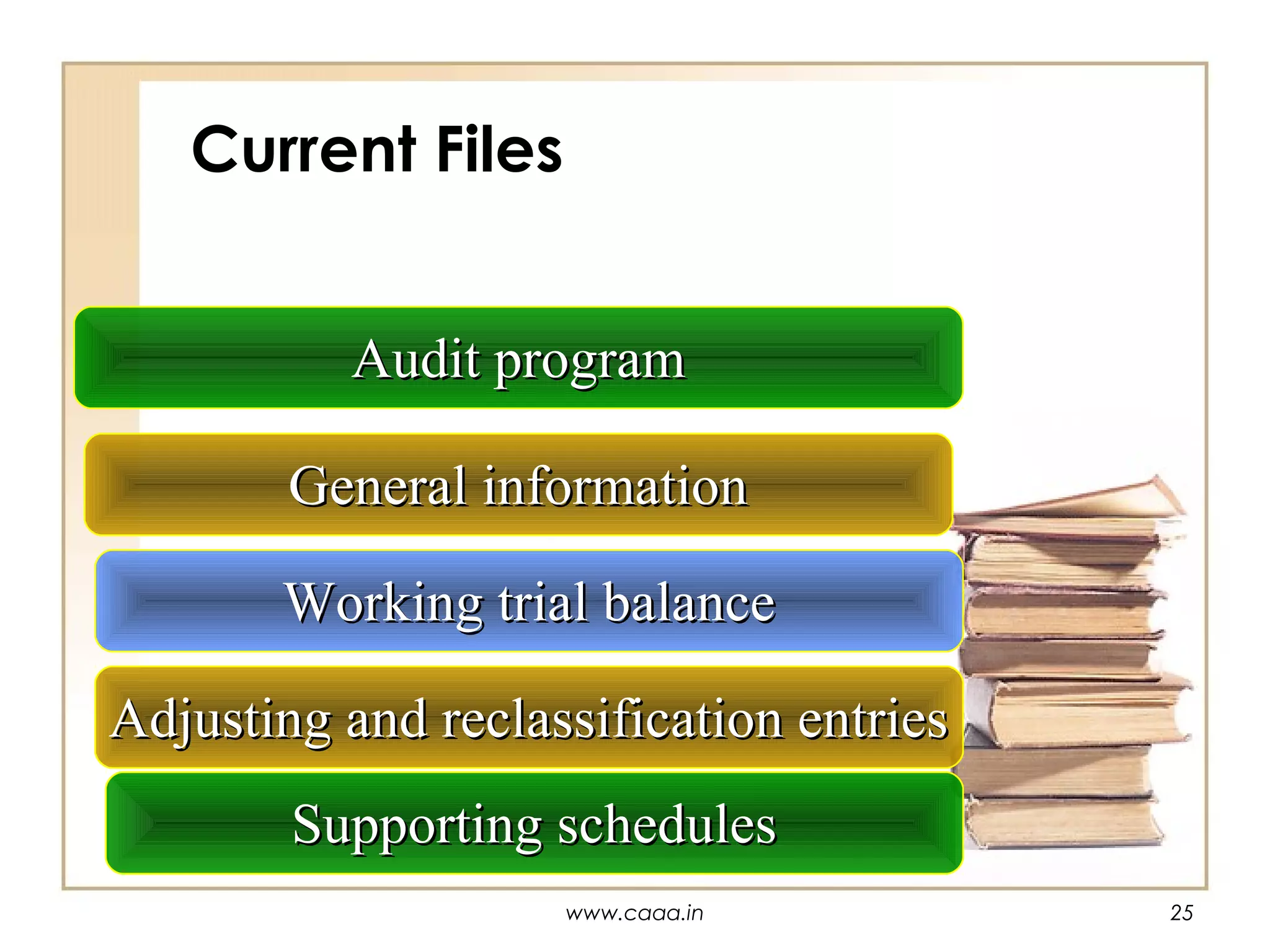

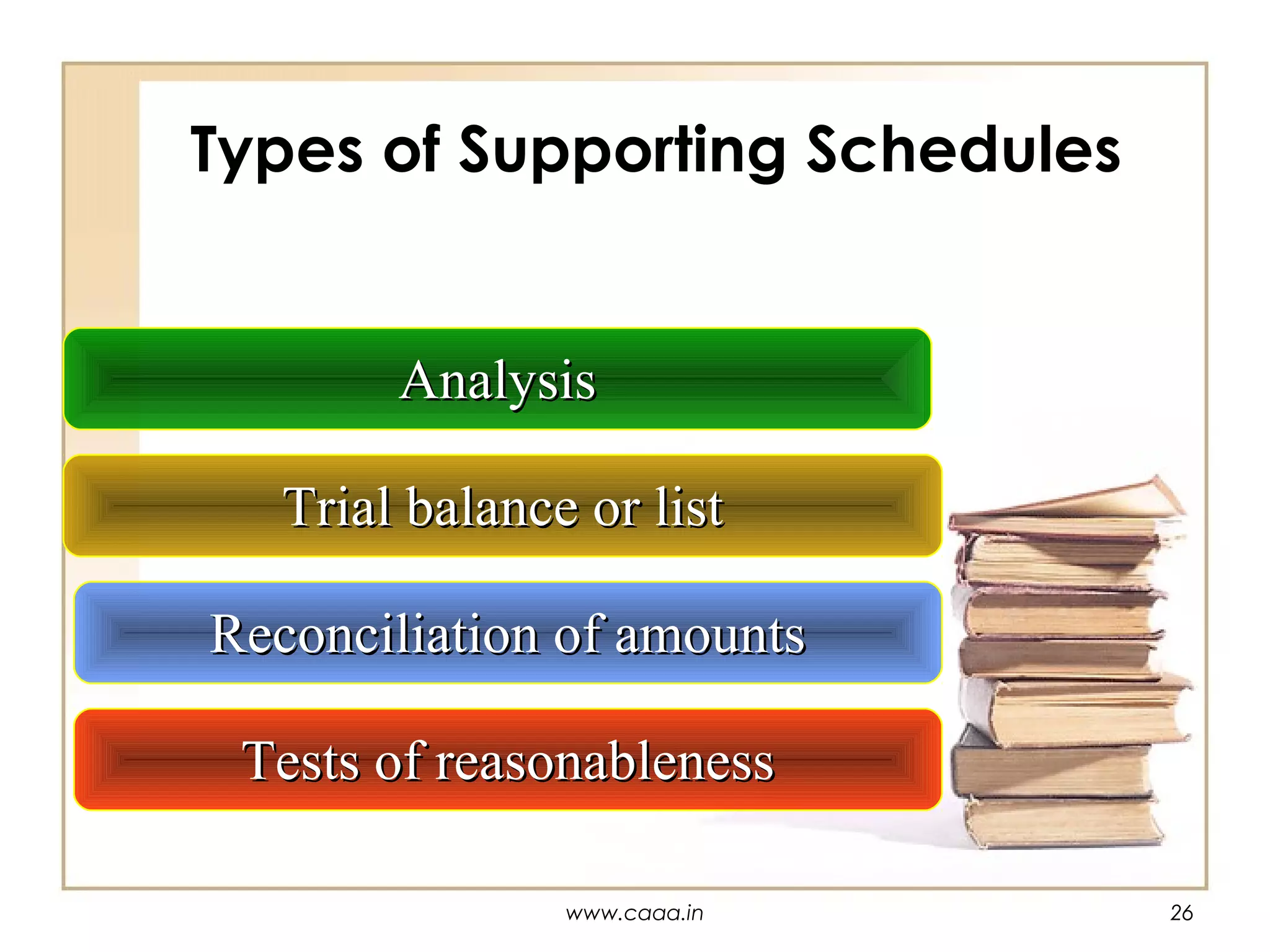

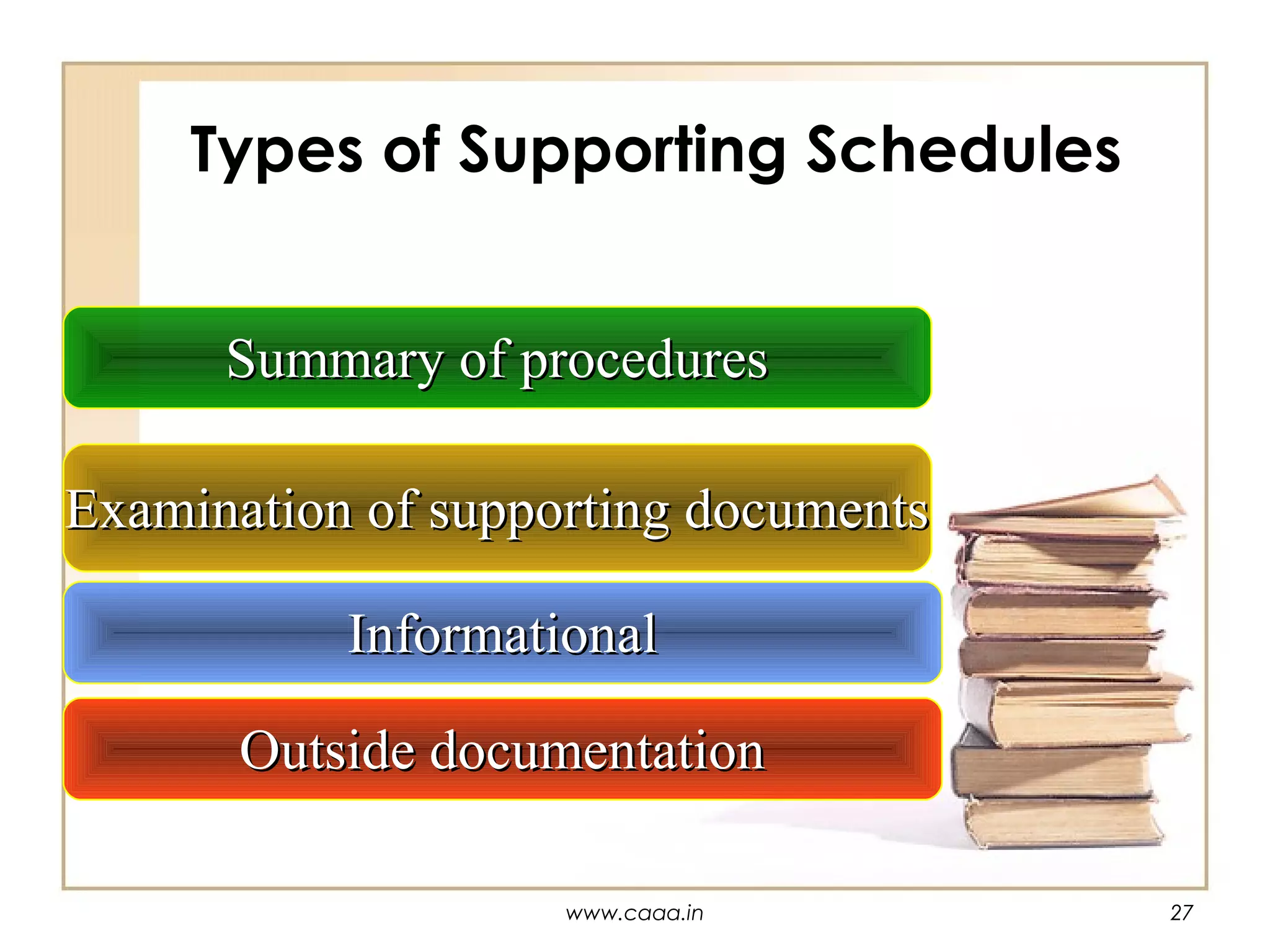

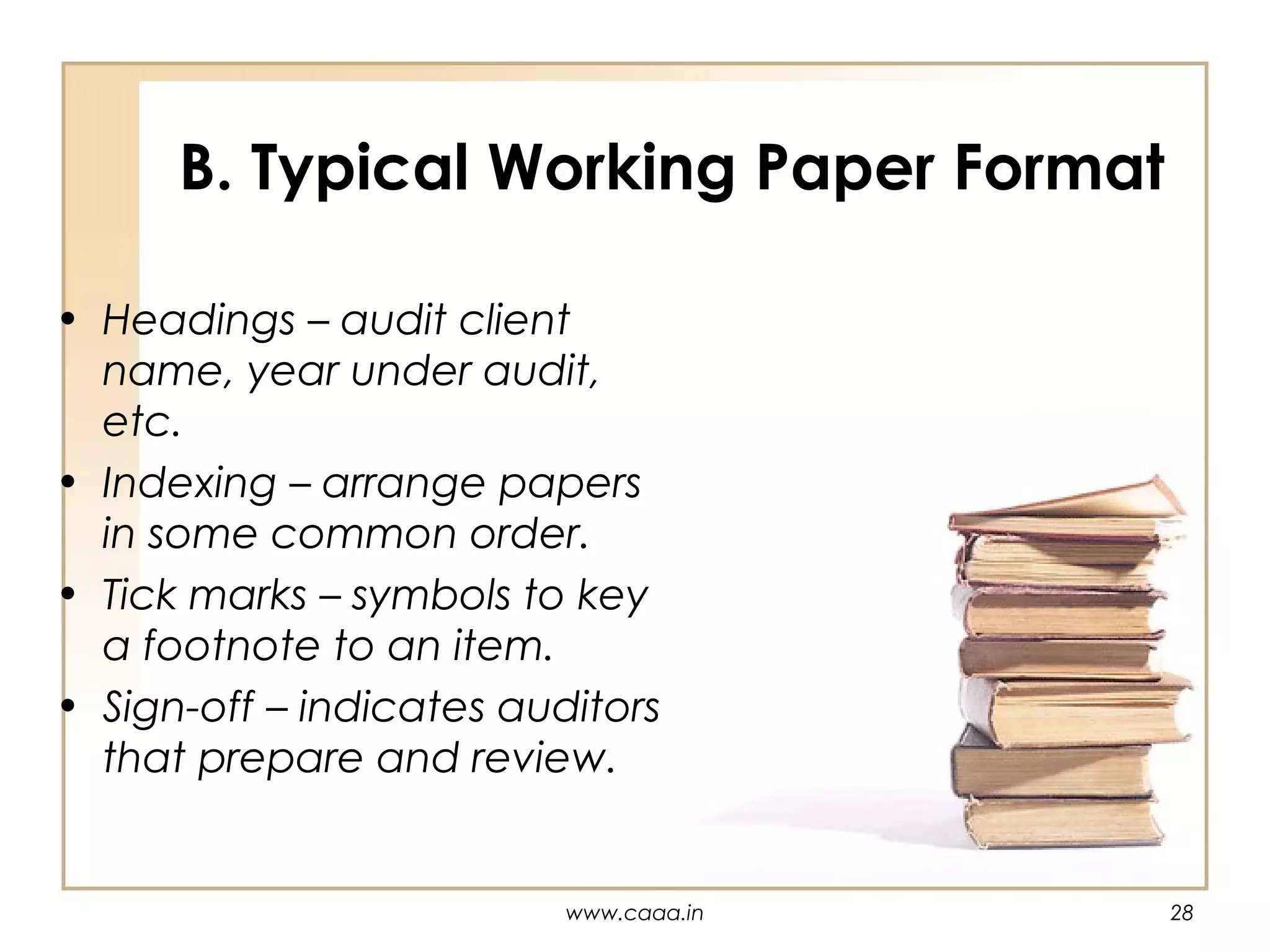

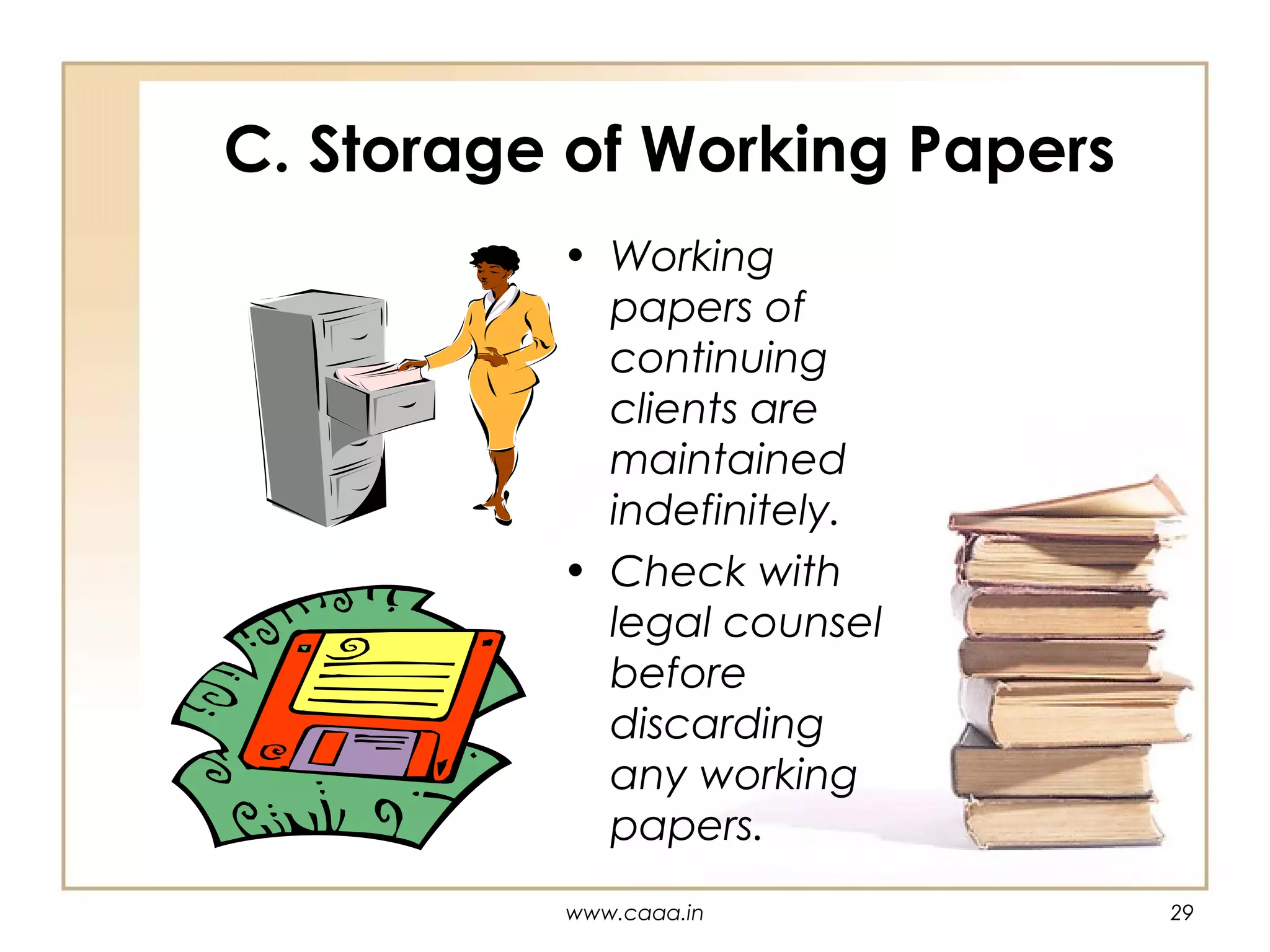

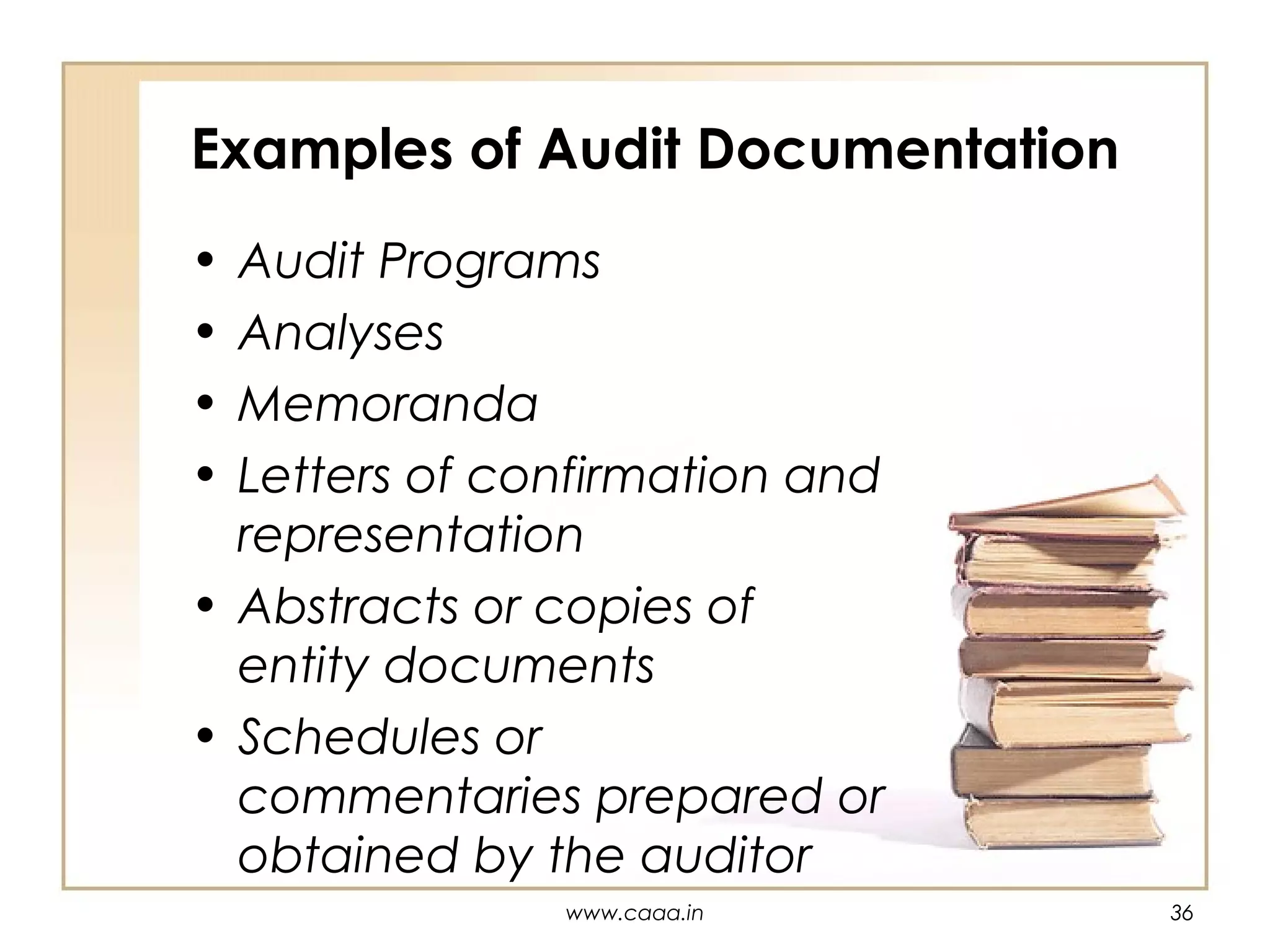

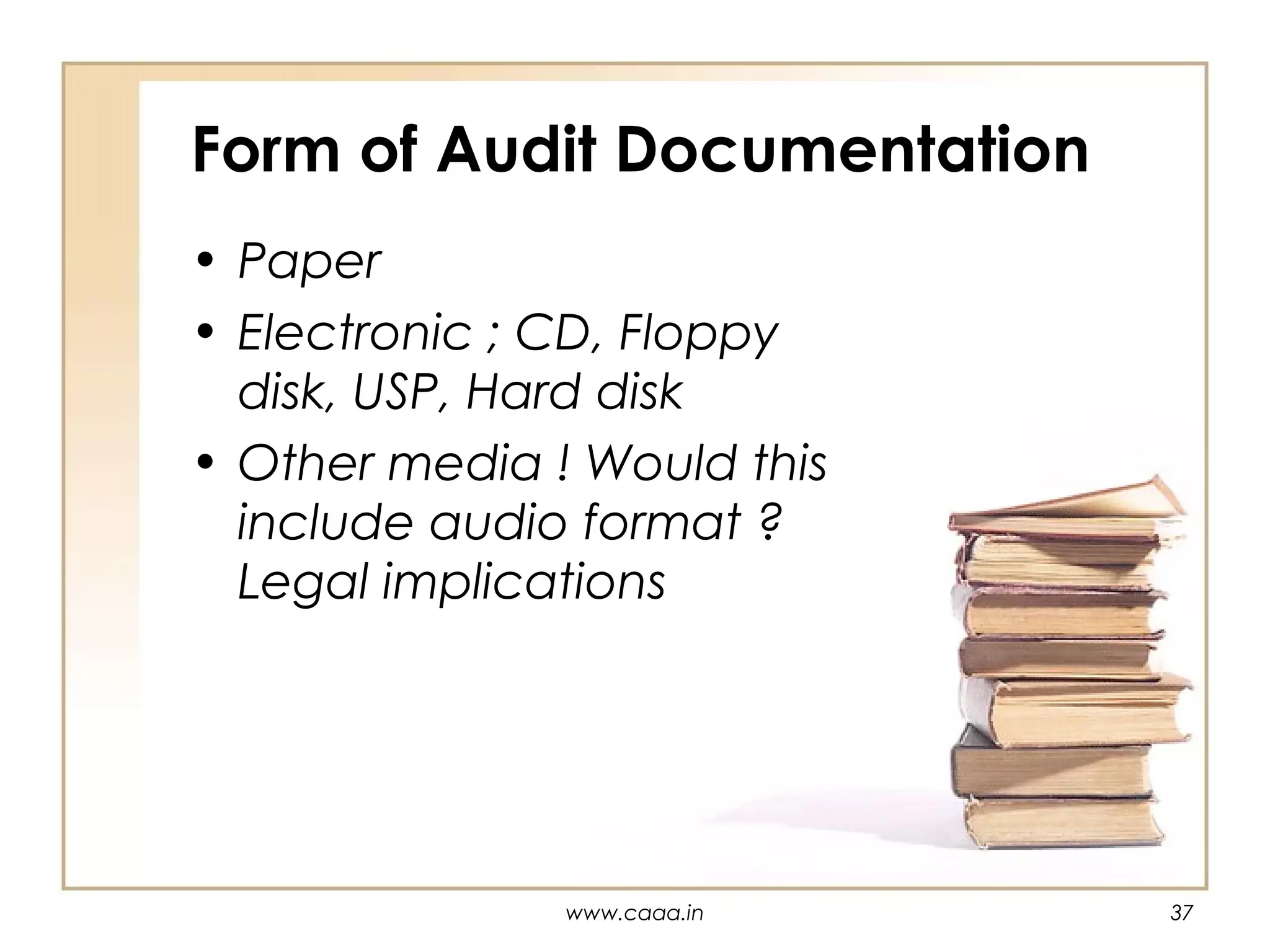

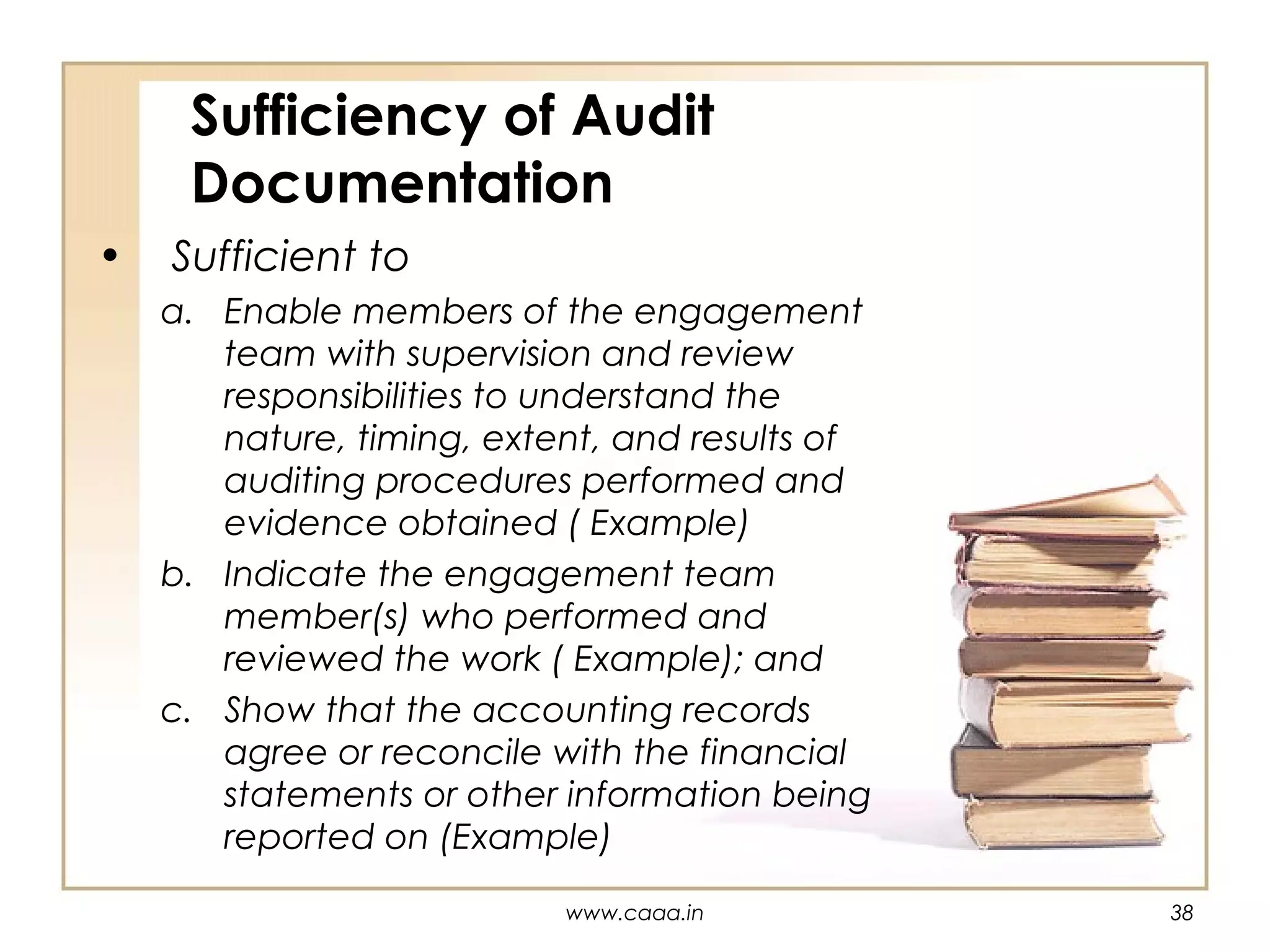

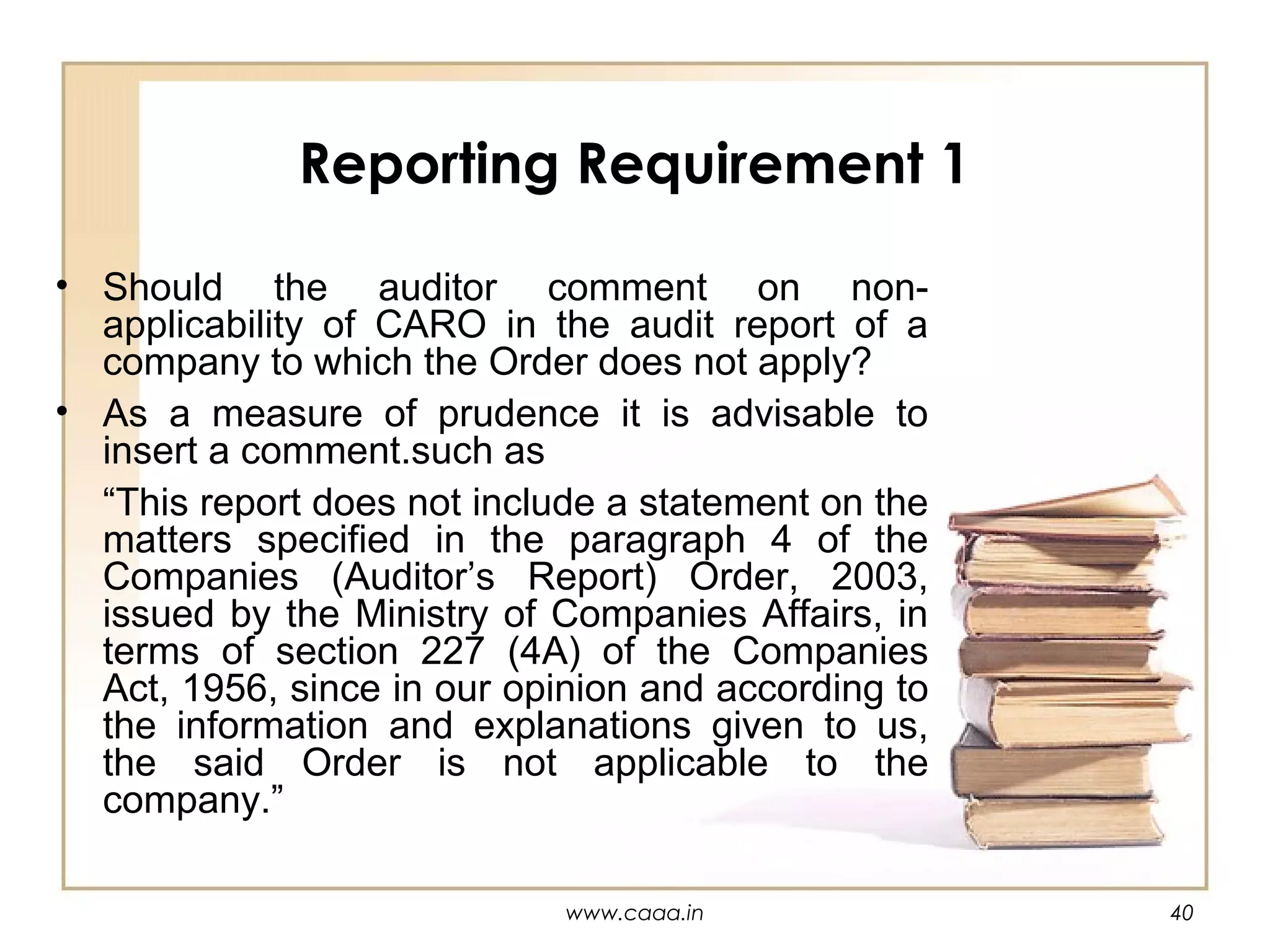

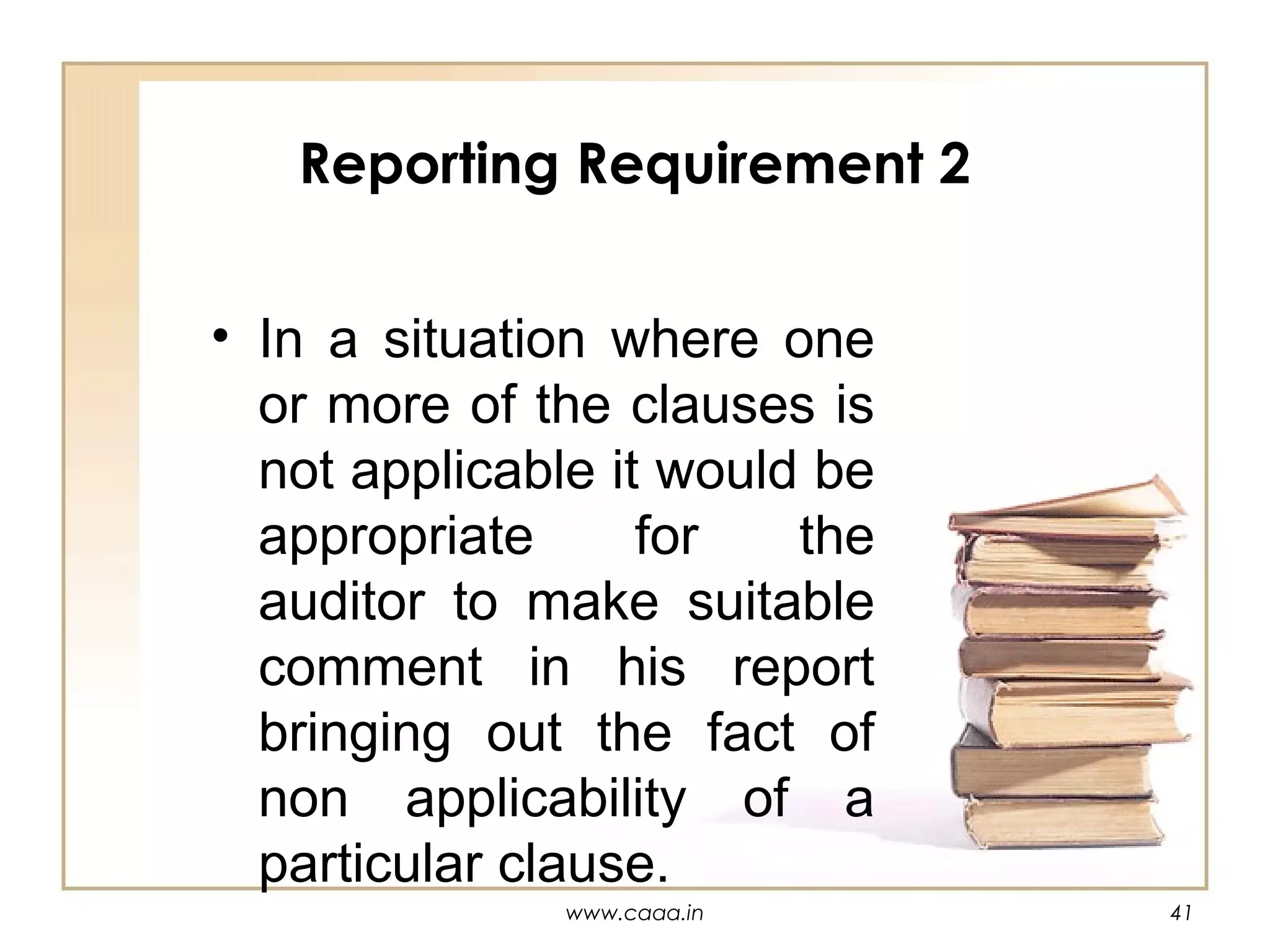

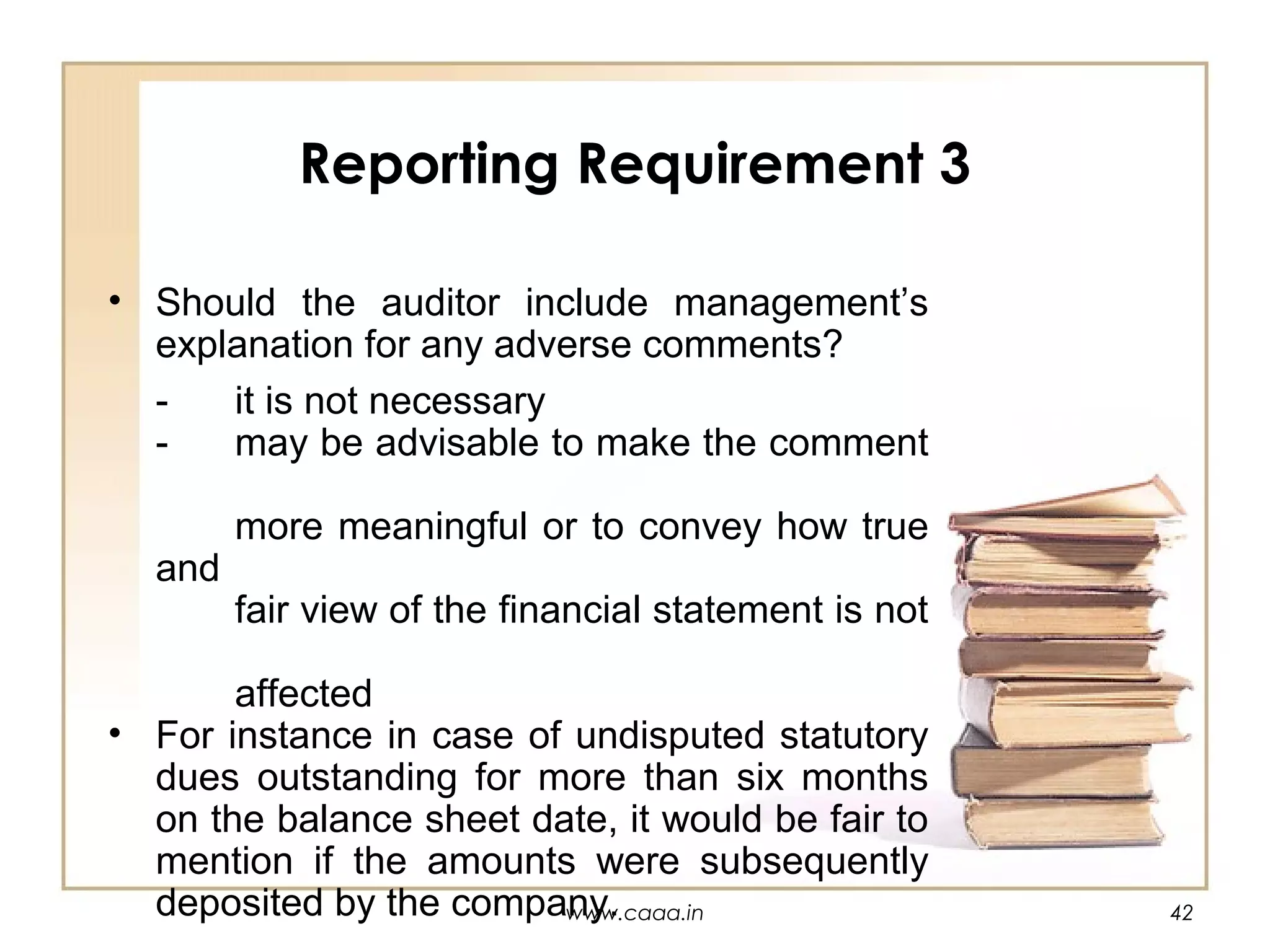

The document discusses audit documentation and reporting requirements. It defines audit documentation as the principal record of audit procedures applied, evidence obtained, and conclusions reached by the auditor. Audit documentation serves to demonstrate that the audit was performed in accordance with standards and to provide a record of evidence in case it is needed for legal or regulatory proceedings. The document outlines the purpose, ownership, and confidentiality of audit documentation, as well as requirements for its organization, storage, and retention. It also discusses reporting requirements for auditors under the Companies Act regarding matters such as the Companies (Auditor's Report) Order and management explanations for adverse comments.

![AUDIT REPORT [ AUDITING ]](https://cdn.slidesharecdn.com/ss_thumbnails/auditingtypesofauditreport-210303052610-thumbnail.jpg?width=600ounds&width=560&fit=bounds)

![AUDIT PLANNING AND PROCEDURES [Autosaved].ppt](https://cdn.slidesharecdn.com/ss_thumbnails/4777auditplanningandproceduresautosaved-240818090542-6370a7b2-thumbnail.jpg?width=600ounds&width=560&fit=bounds)