Downloaded 221 times

The document outlines the characteristics of successful consumer technology companies, emphasizing the need for a highly profitable core business and the development of ecosystems that enable value creation across multiple domains. It discusses various business models, including direct monetization and non-monetized approaches, highlighting the shift towards subscription models as a dominant trend. The key takeaway is that while software is prevalent, it is often monetized through hardware or related services, with successful companies leveraging their ecosystems to thrive.

Jan Dawson introduces the presentation, outlining its purpose and relevance to consumer technology companies.

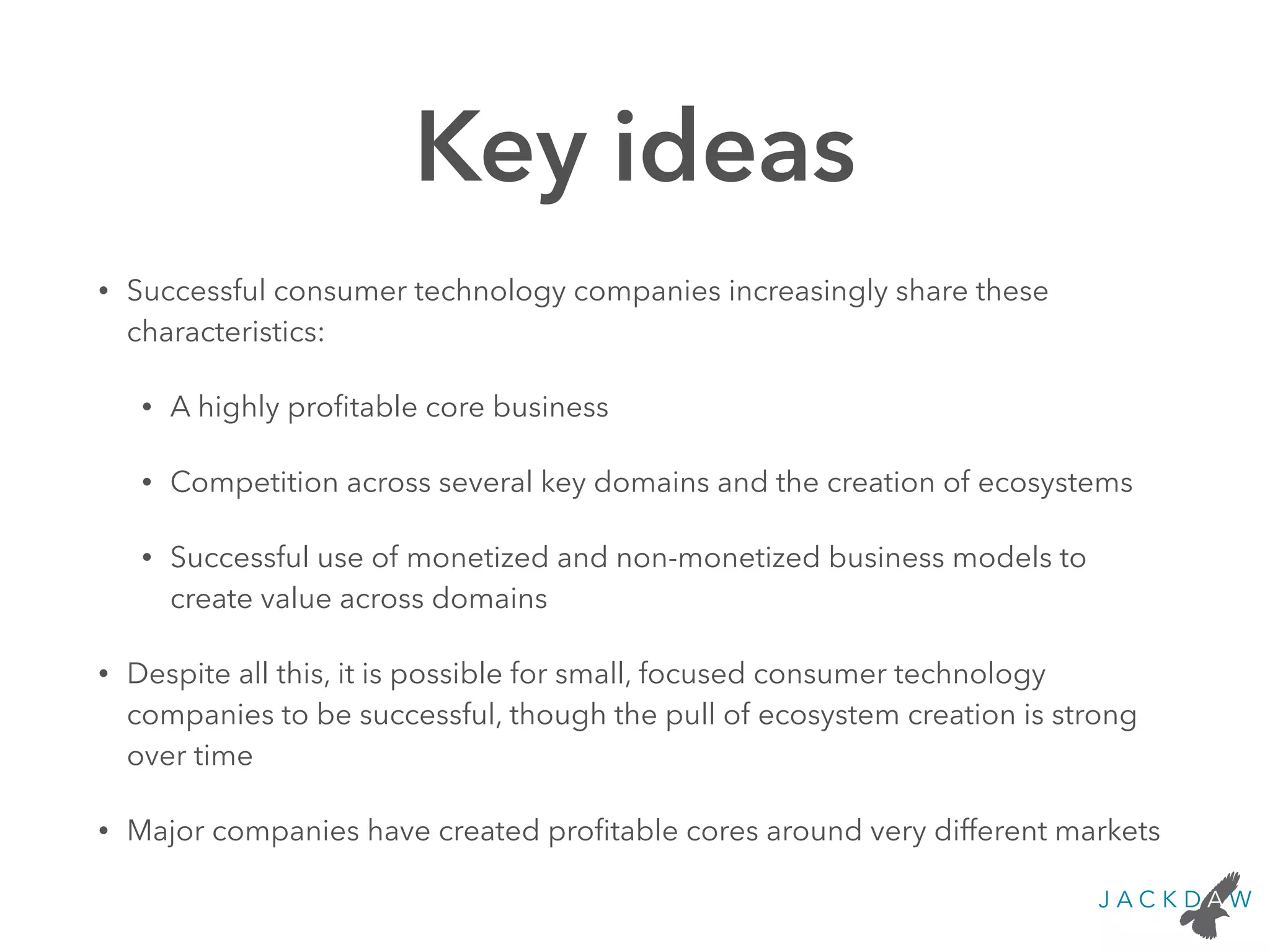

Highlights key traits of successful consumer tech firms: profitable core, ecosystem creation, and multiple revenue models.

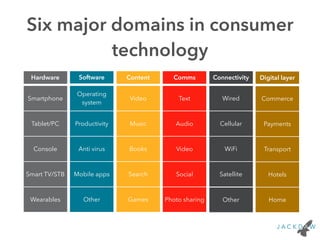

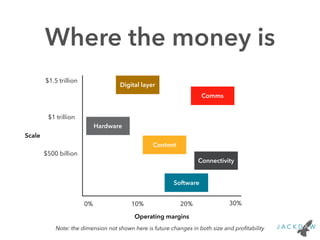

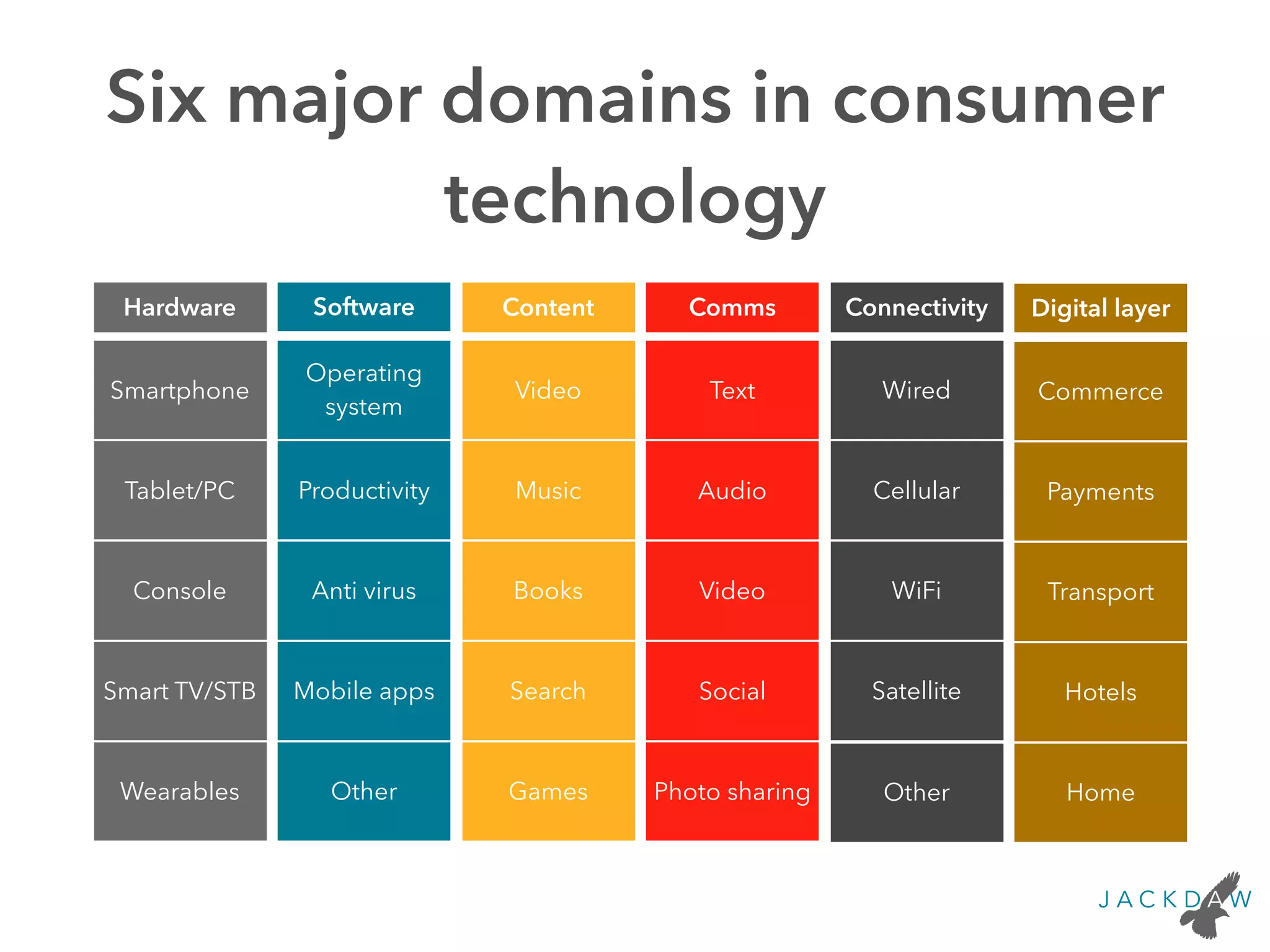

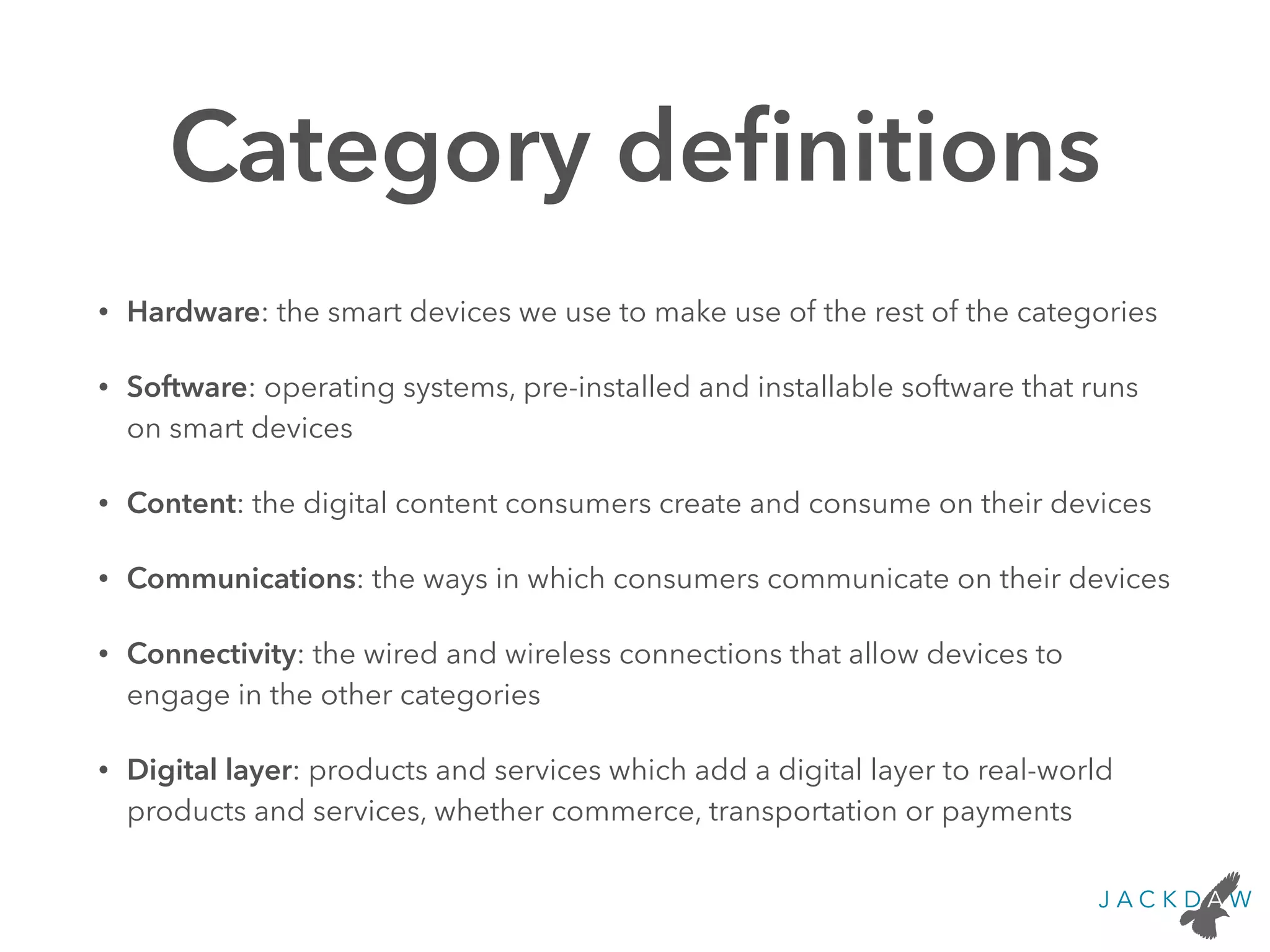

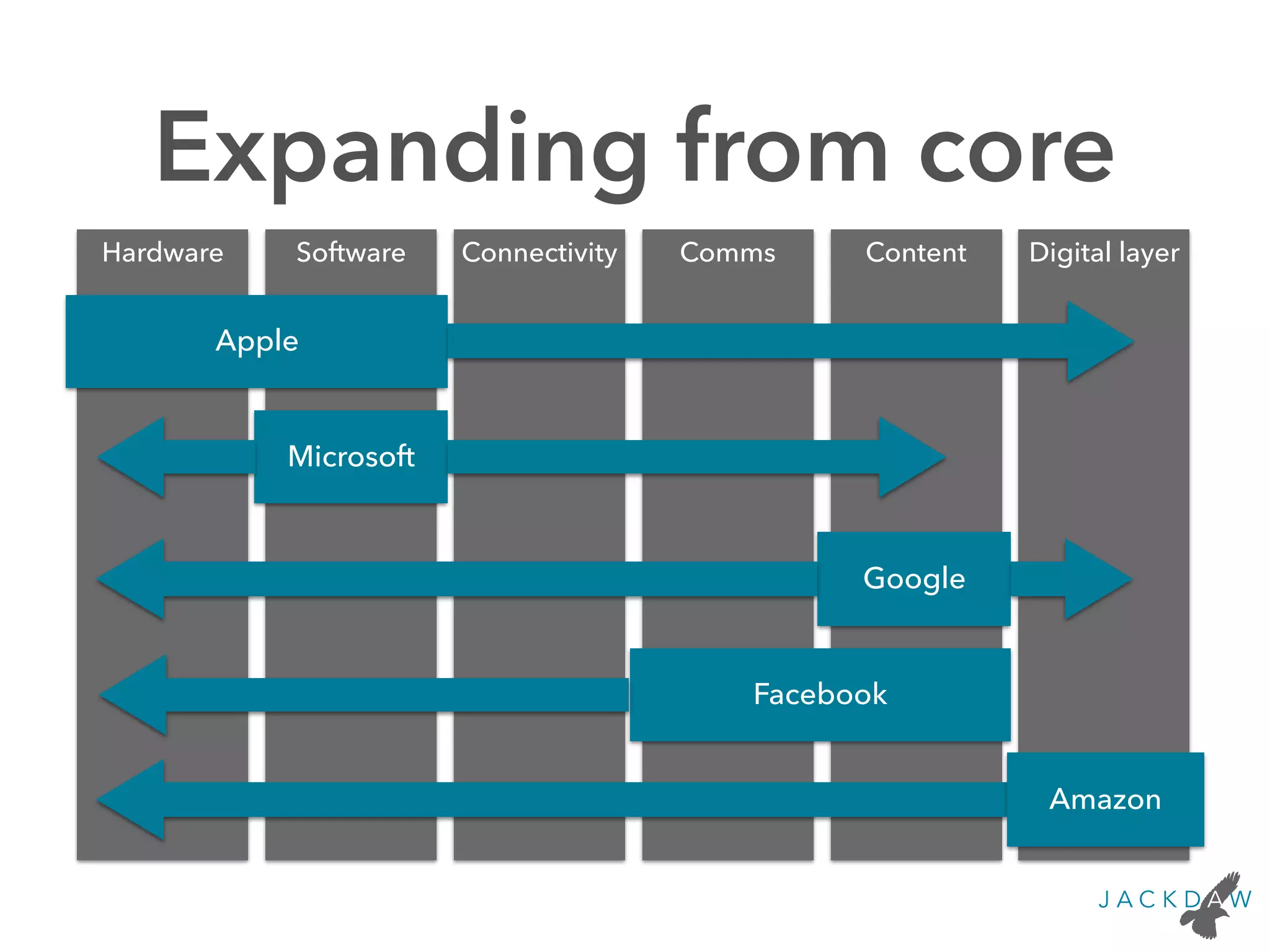

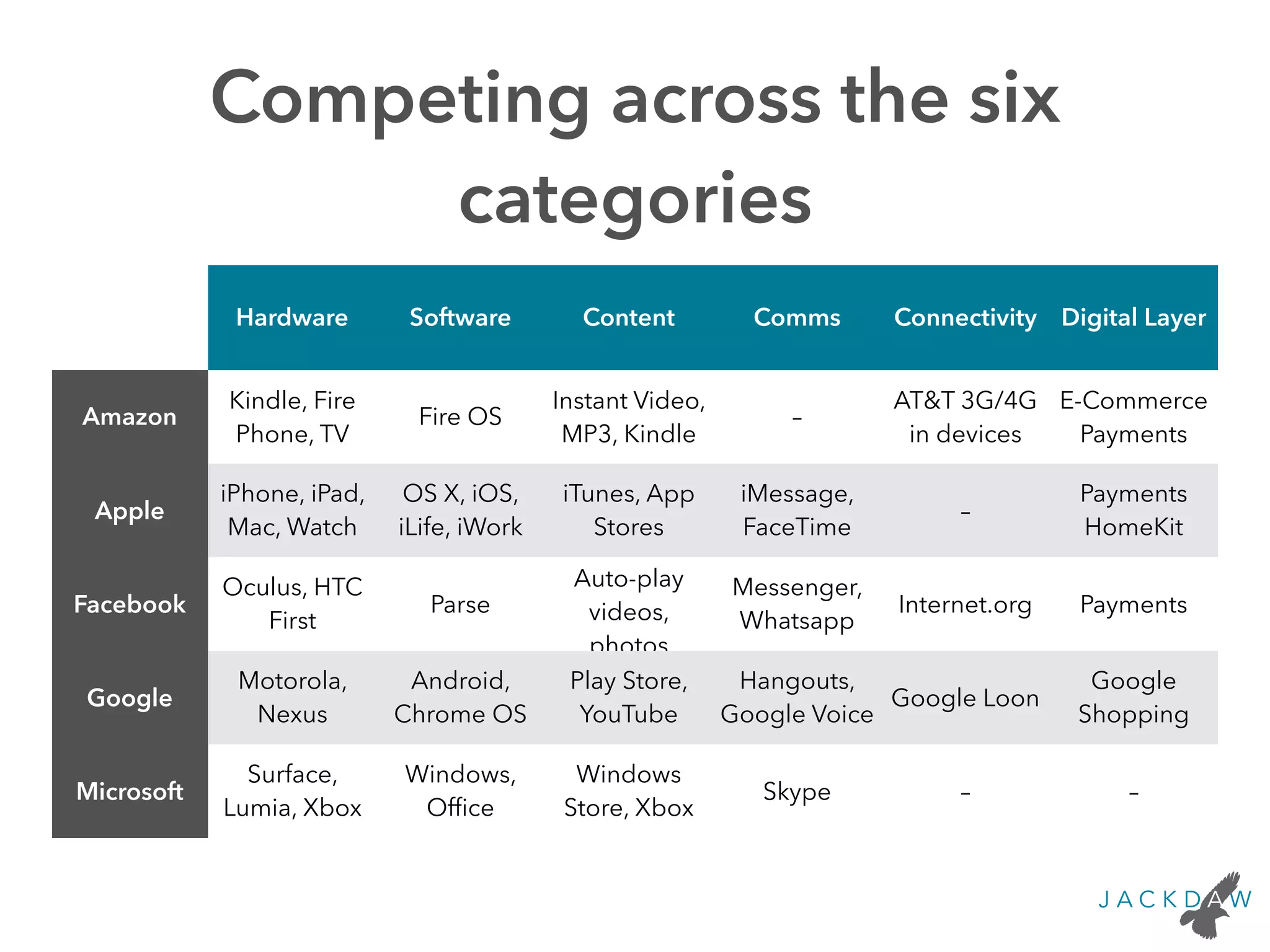

Defines six major domains: Content, Comms, Connectivity, Software, Hardware, and Digital Layer.

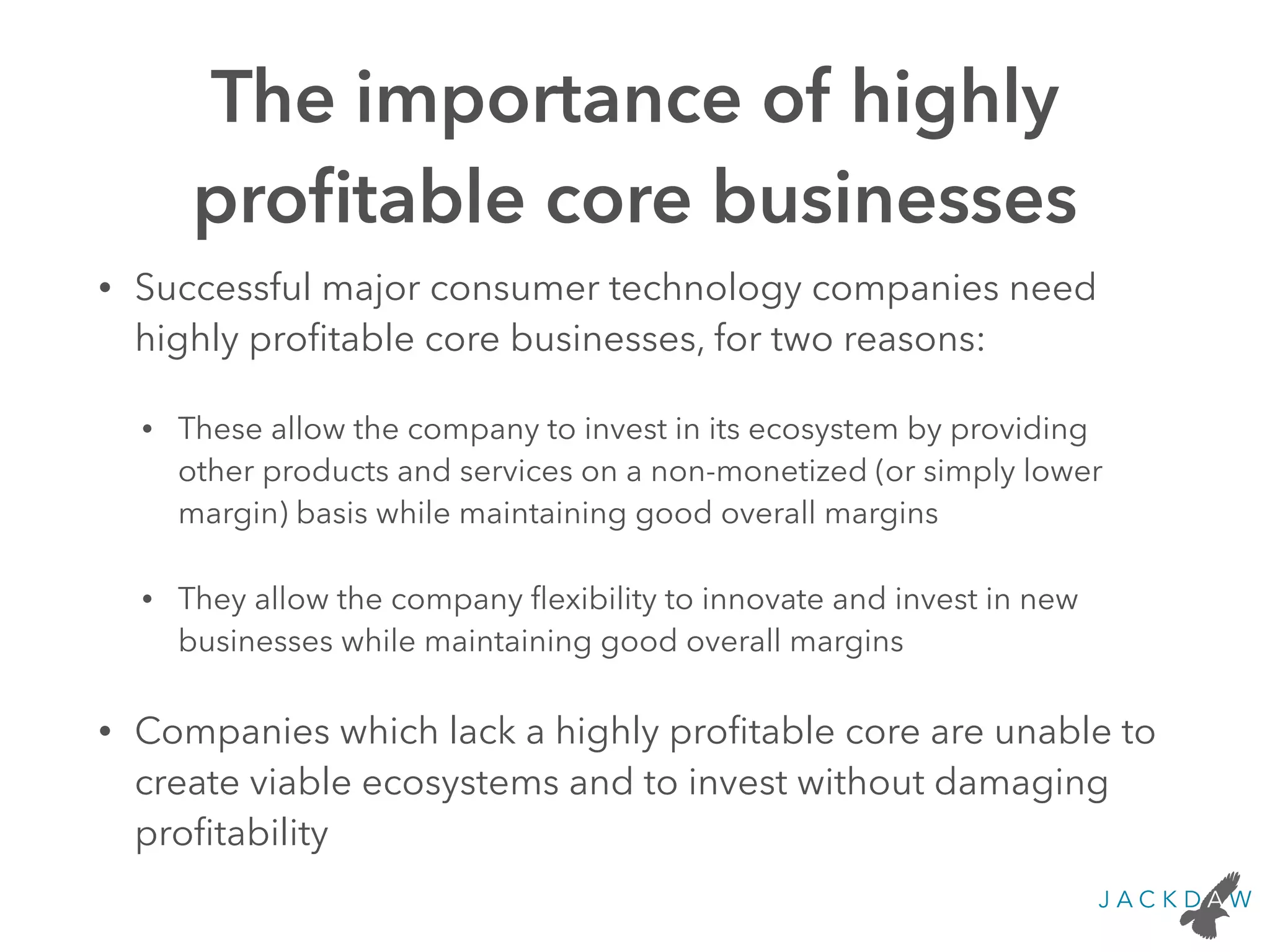

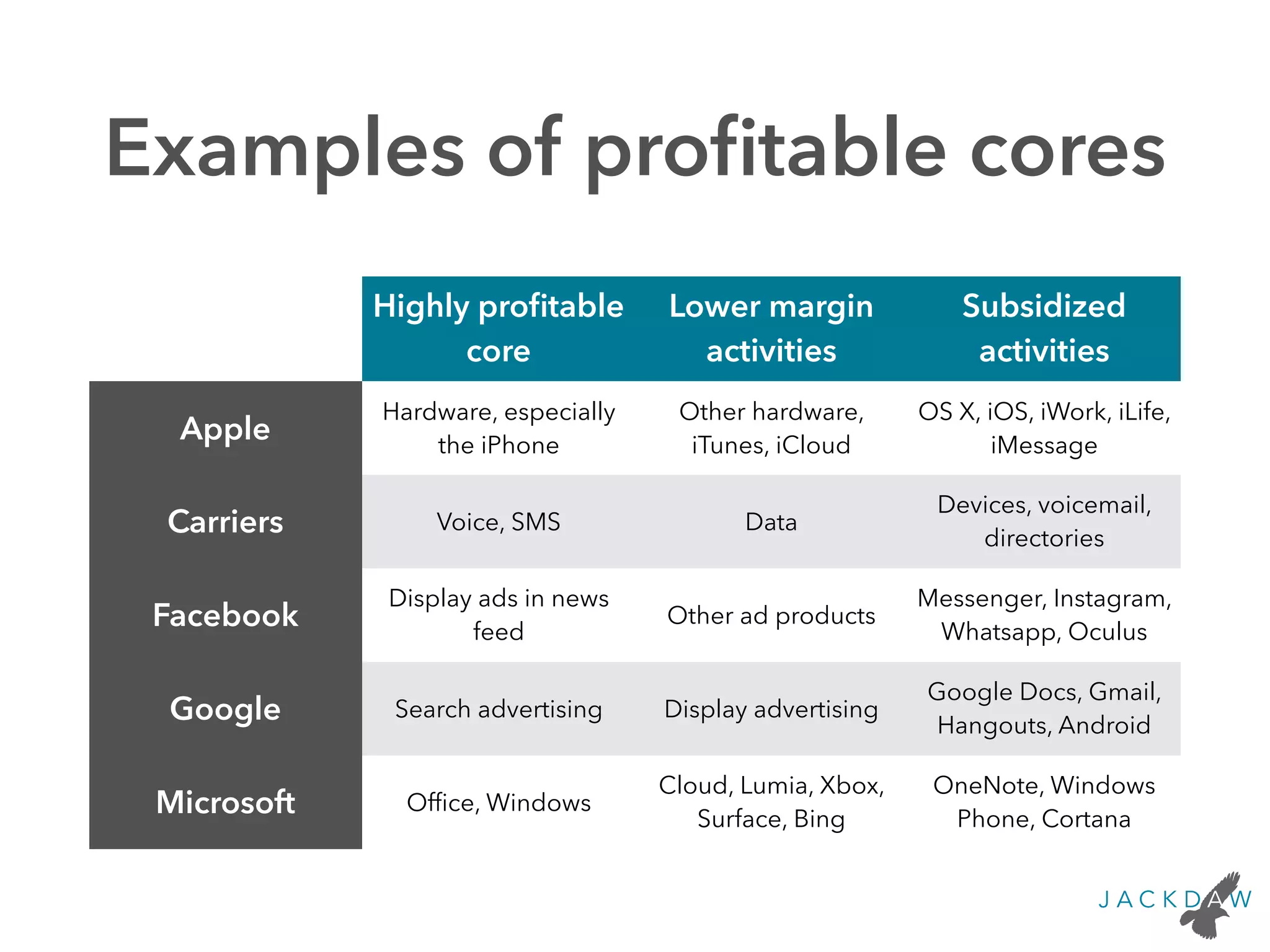

Details the need for highly profitable cores for investment and innovation in consumer tech companies.

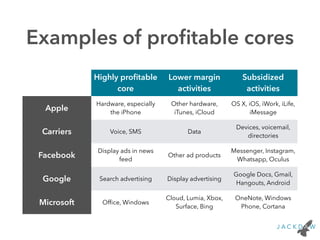

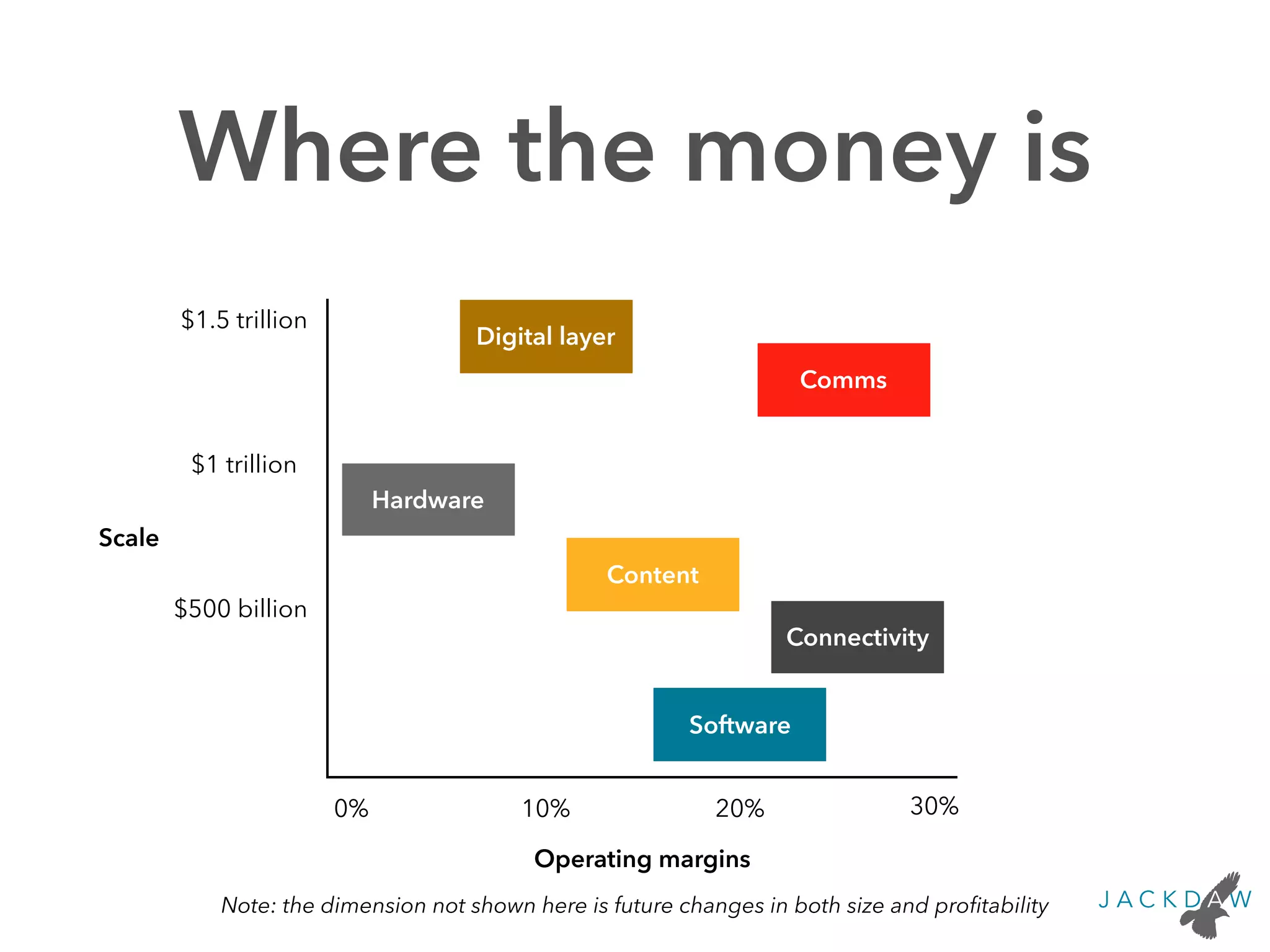

Different tech firms thrive on varied profitable cores: hardware, software, content, etc.

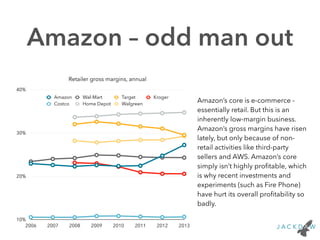

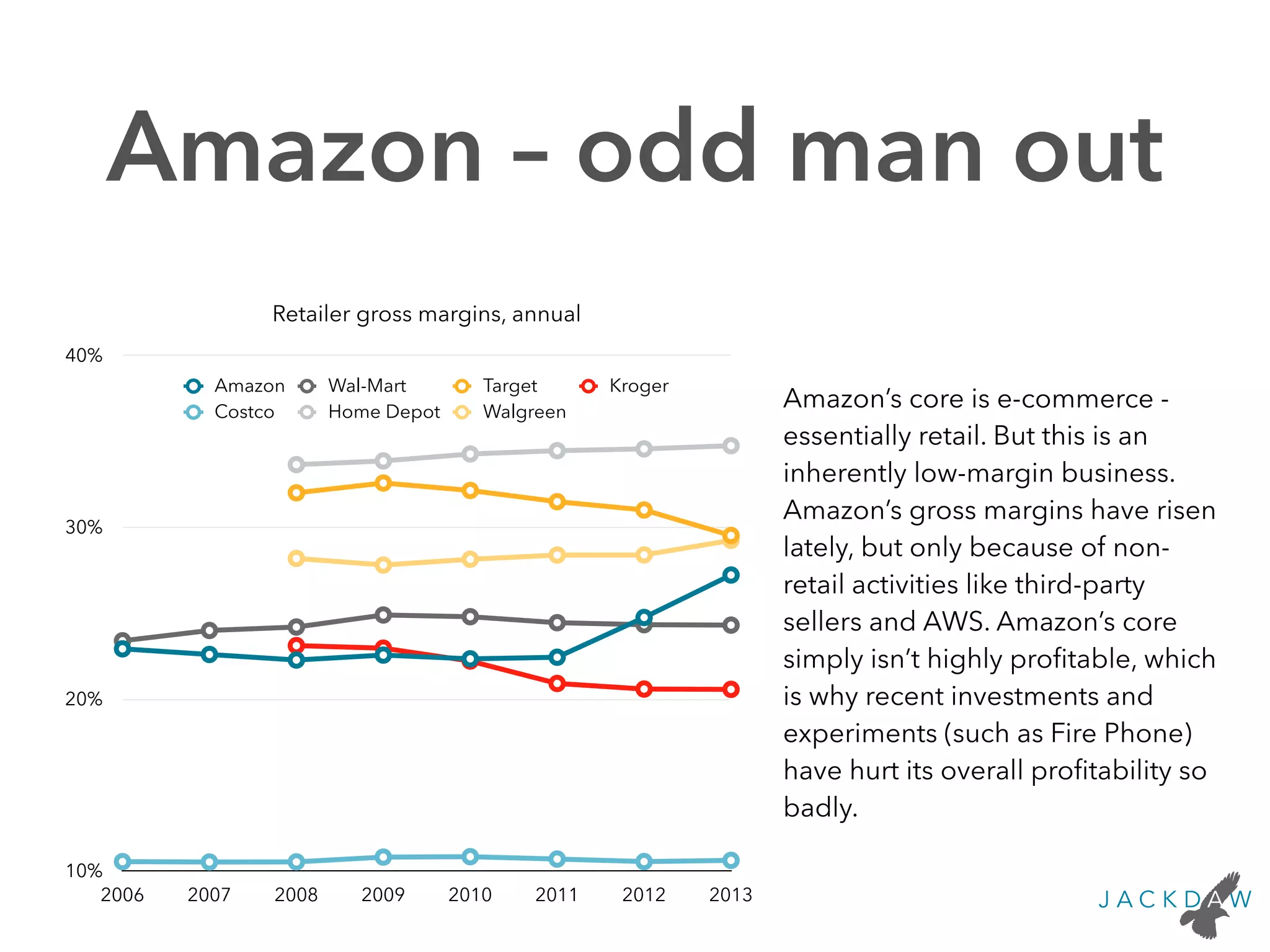

Amazon's core is low-margin e-commerce, contrasting with high-profit tech companies' models.

Two categories of business models: monetized and non-monetized, with various subcategories.

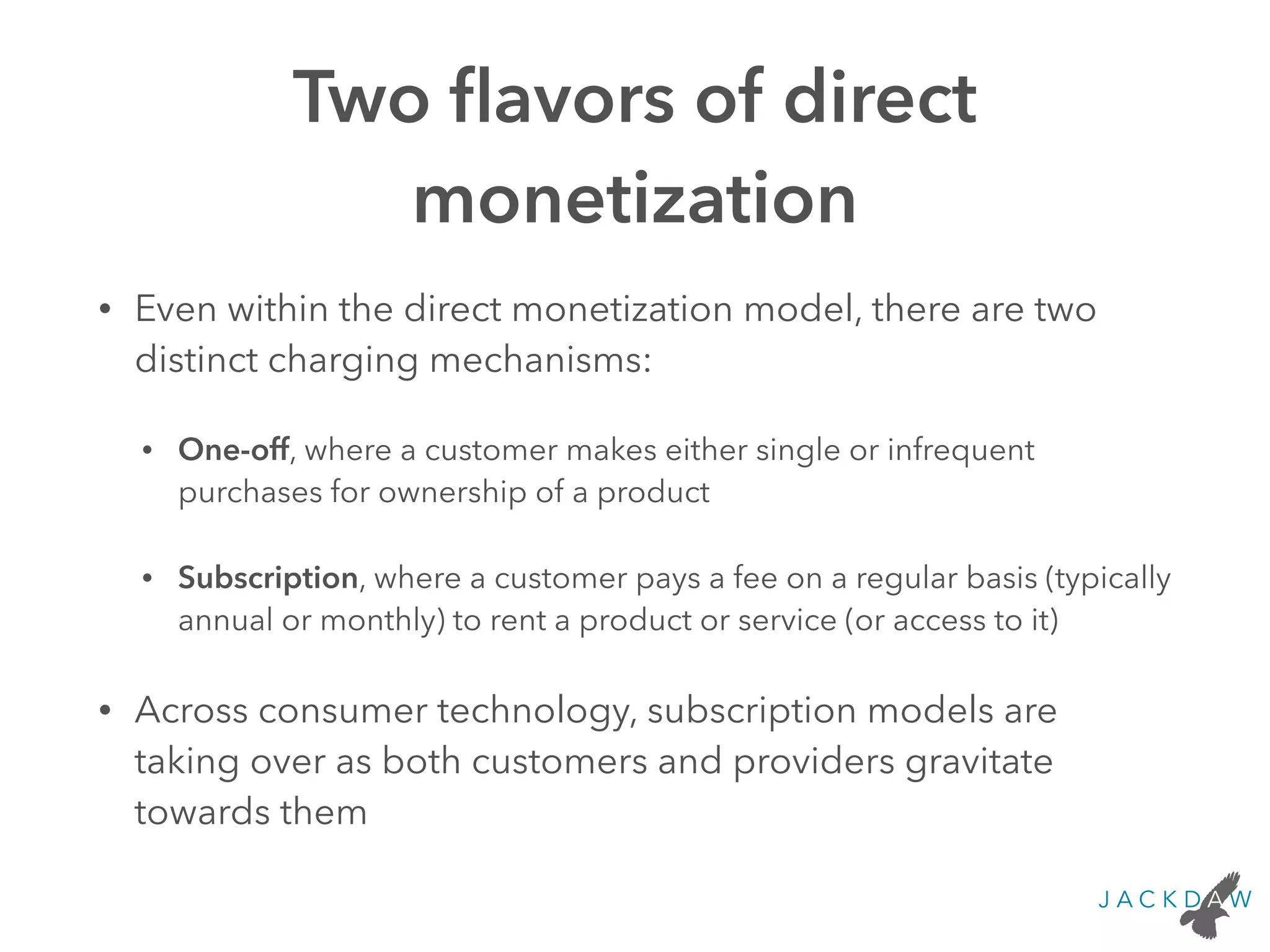

Explains one-off and subscription-based direct monetization models in consumer technology.

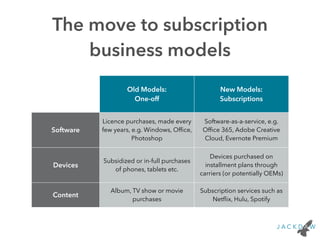

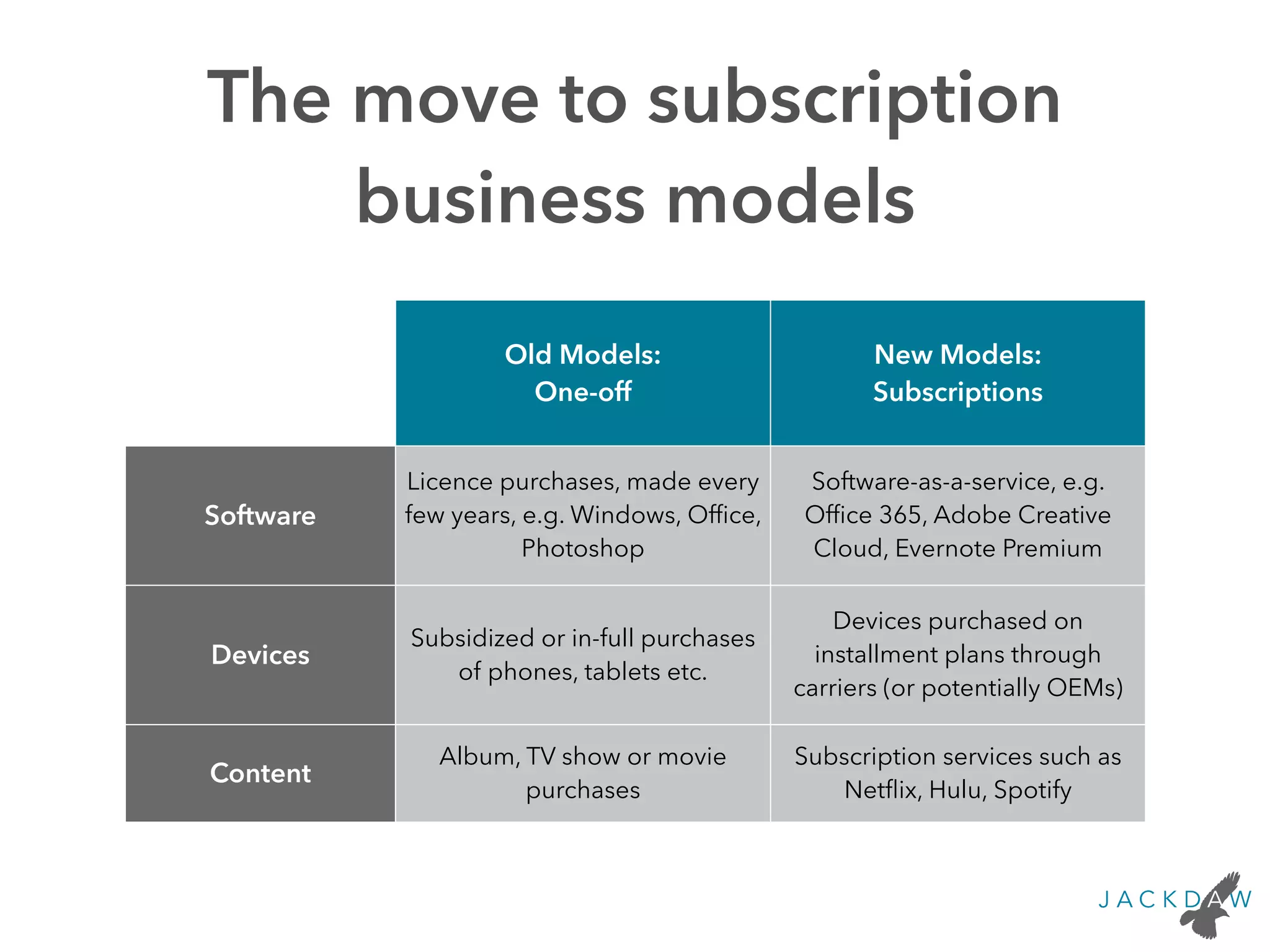

Trends from one-off purchases to subscription models in software, devices, and content.

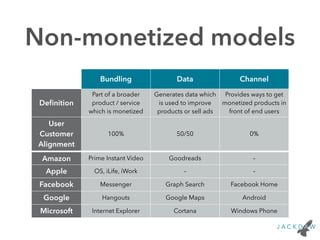

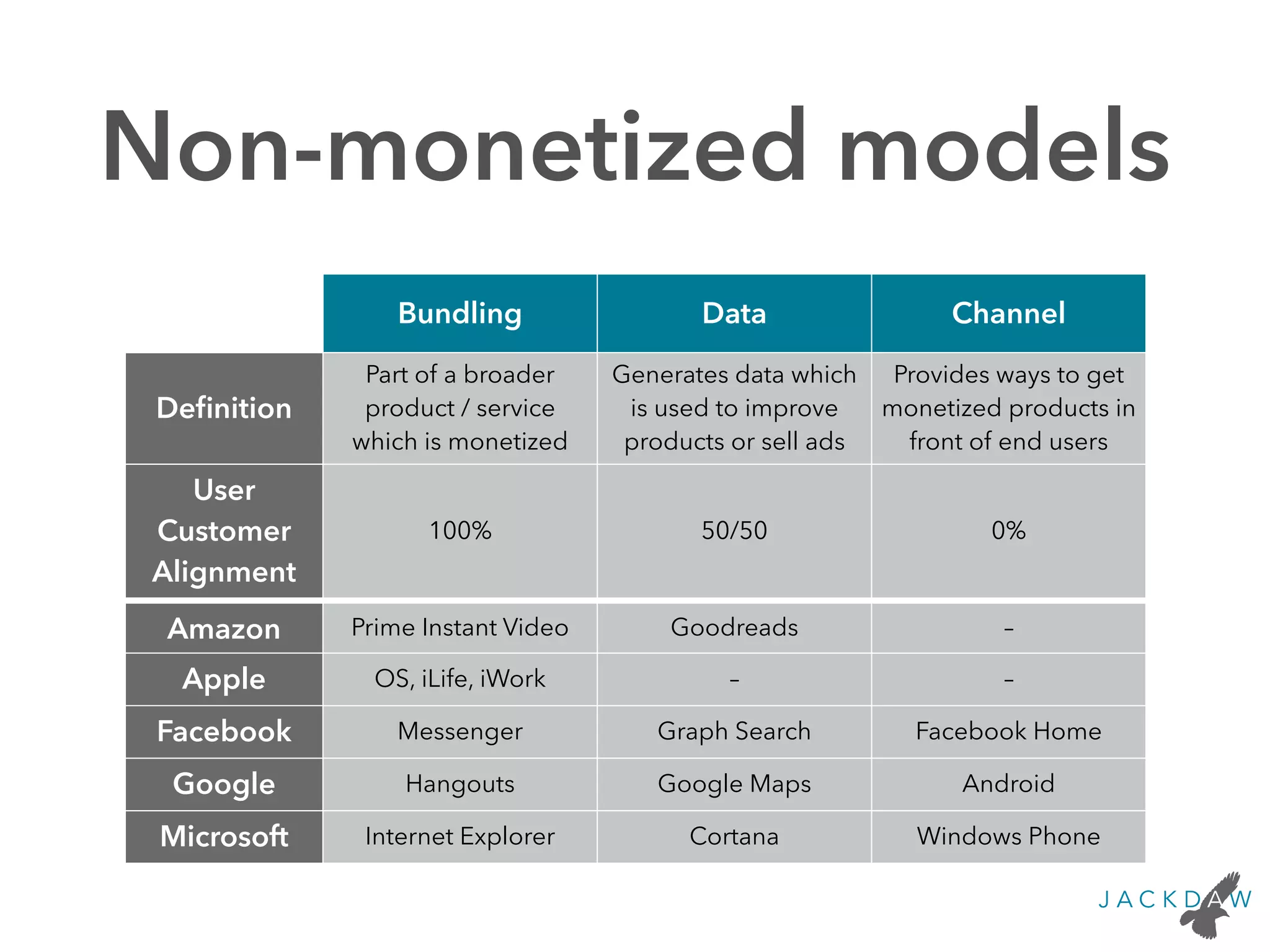

Identifies types of non-monetized models: bundling, data generation, and channel strategies.

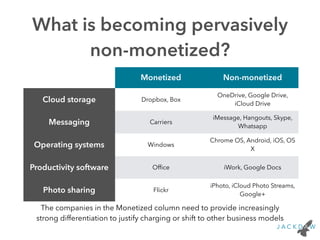

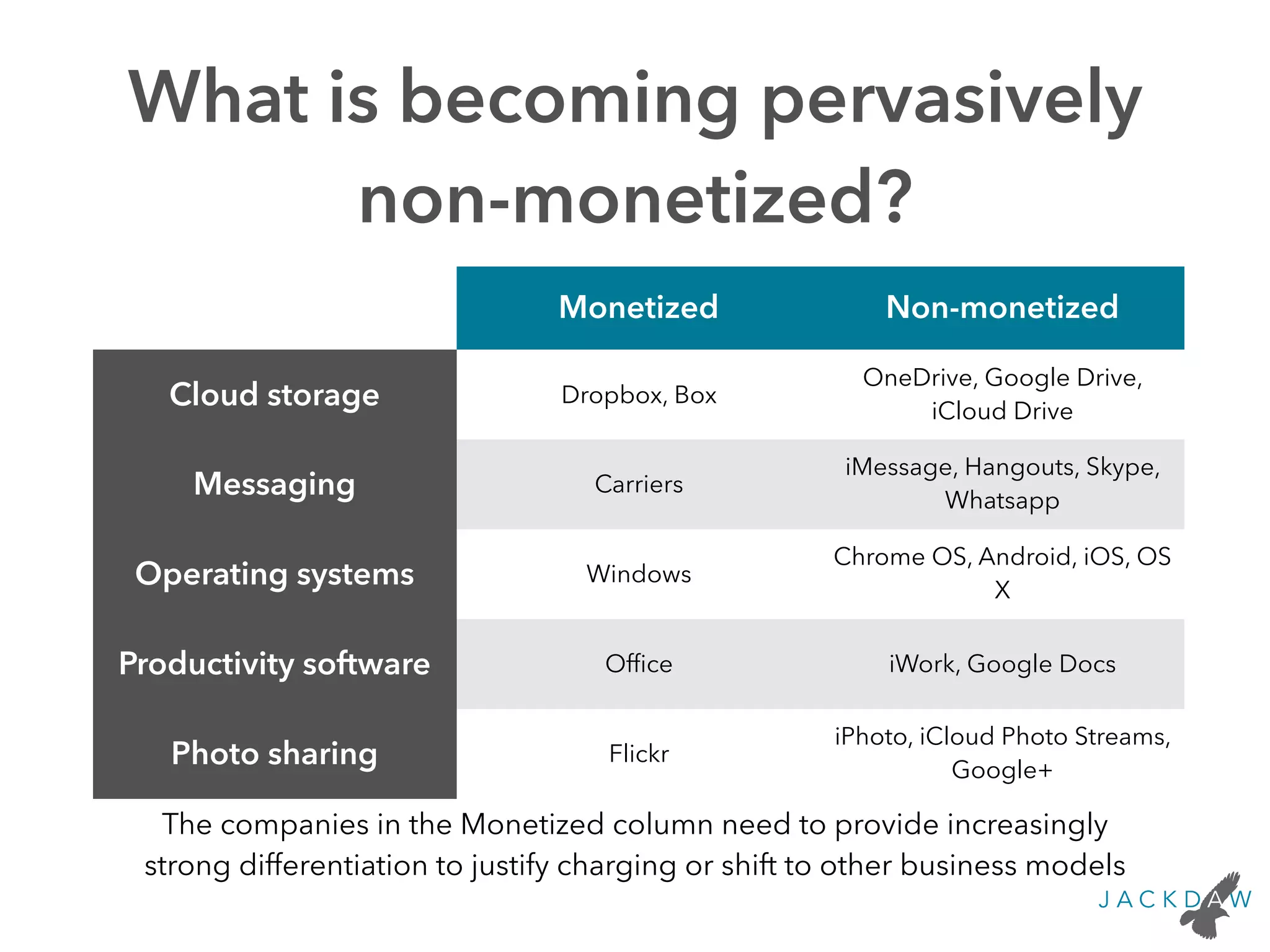

Lists current services becoming non-monetized, which require differentiation from monetized firms.

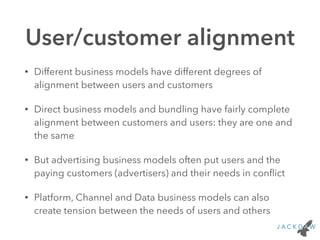

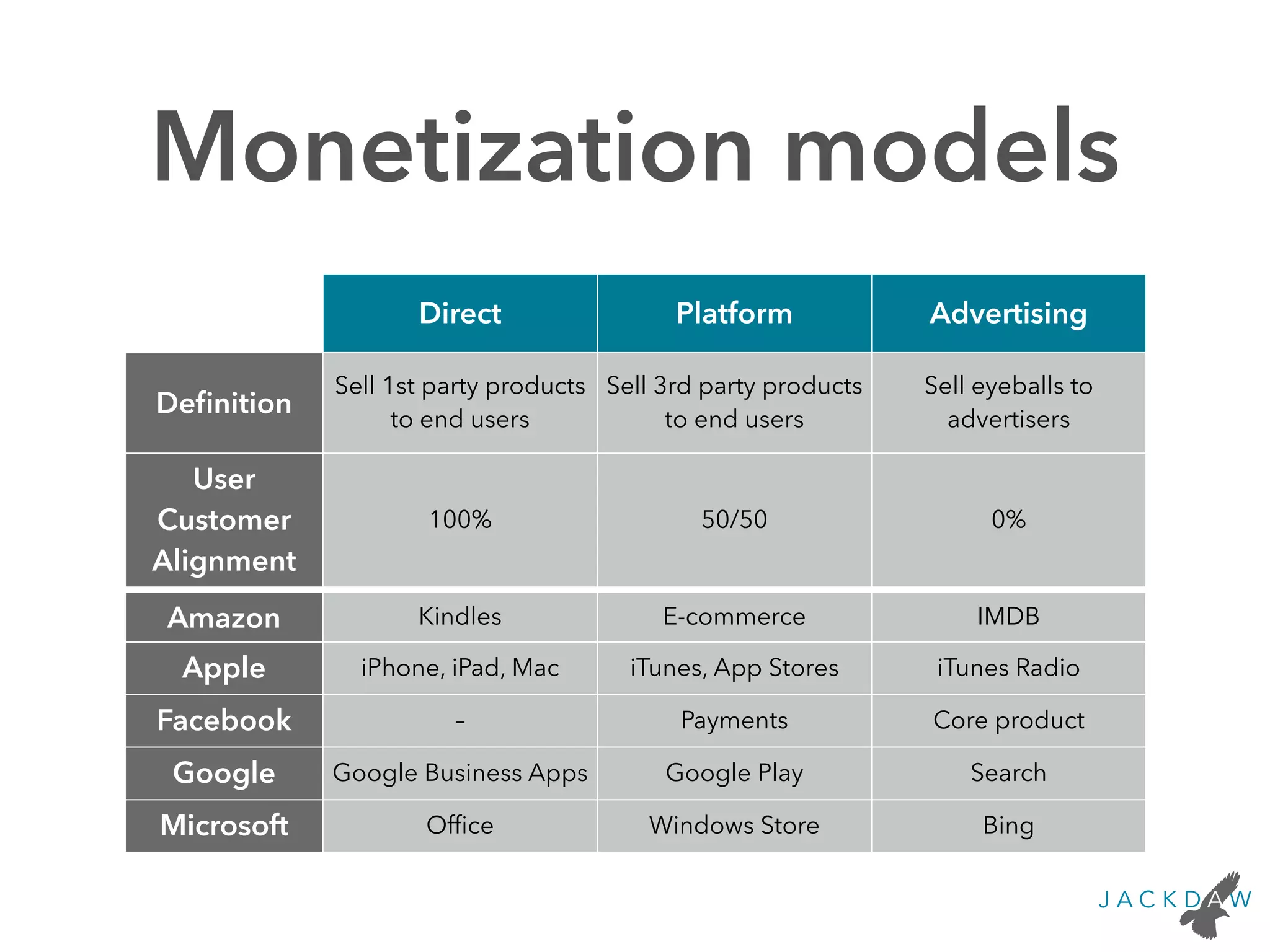

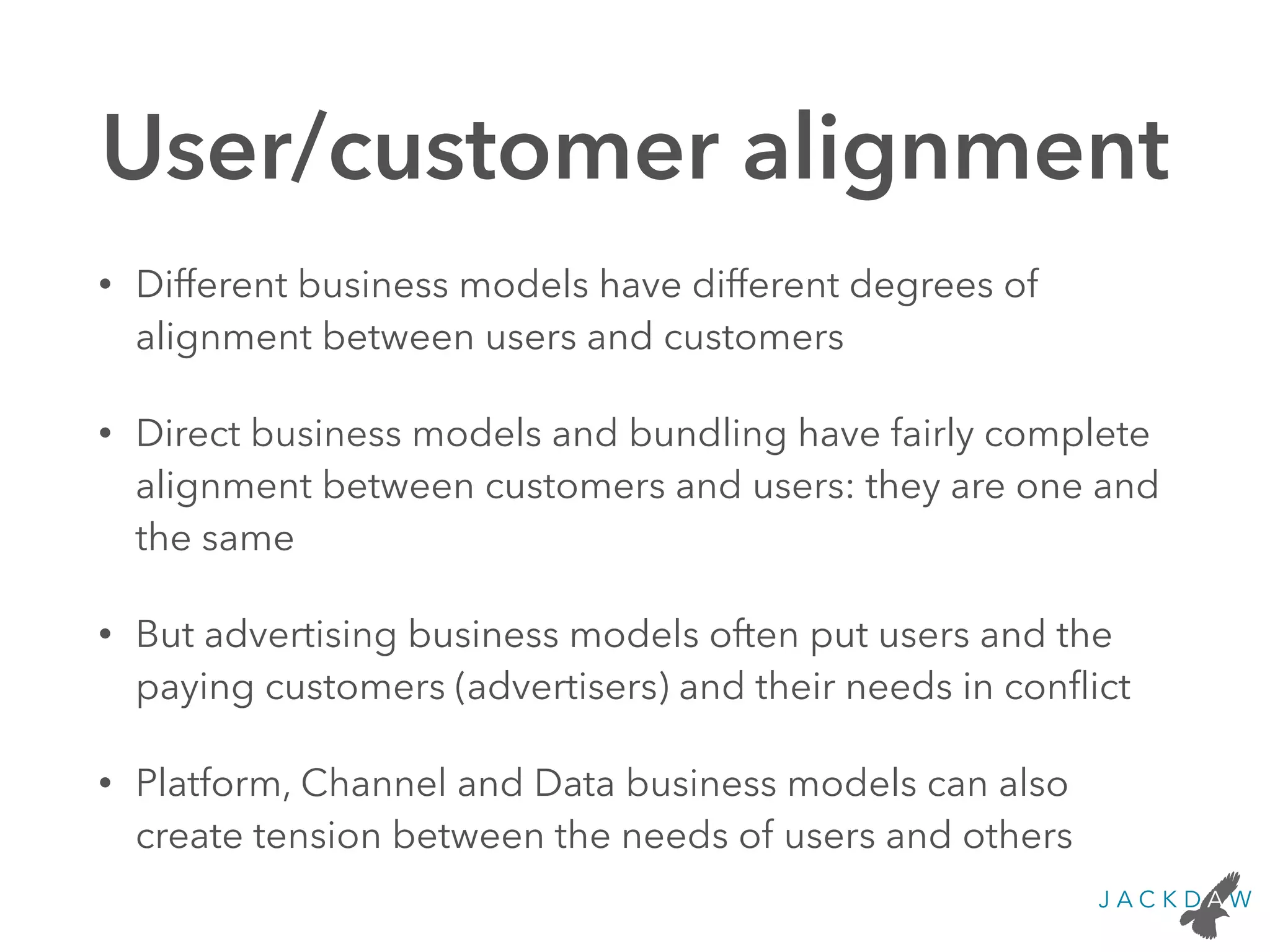

Discusses alignment levels in different business models and conflicts between users and advertisers.

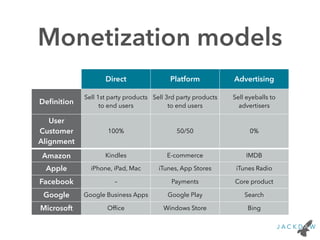

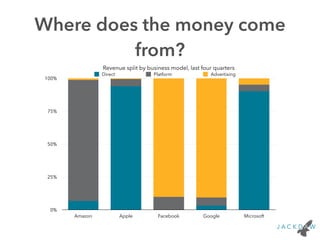

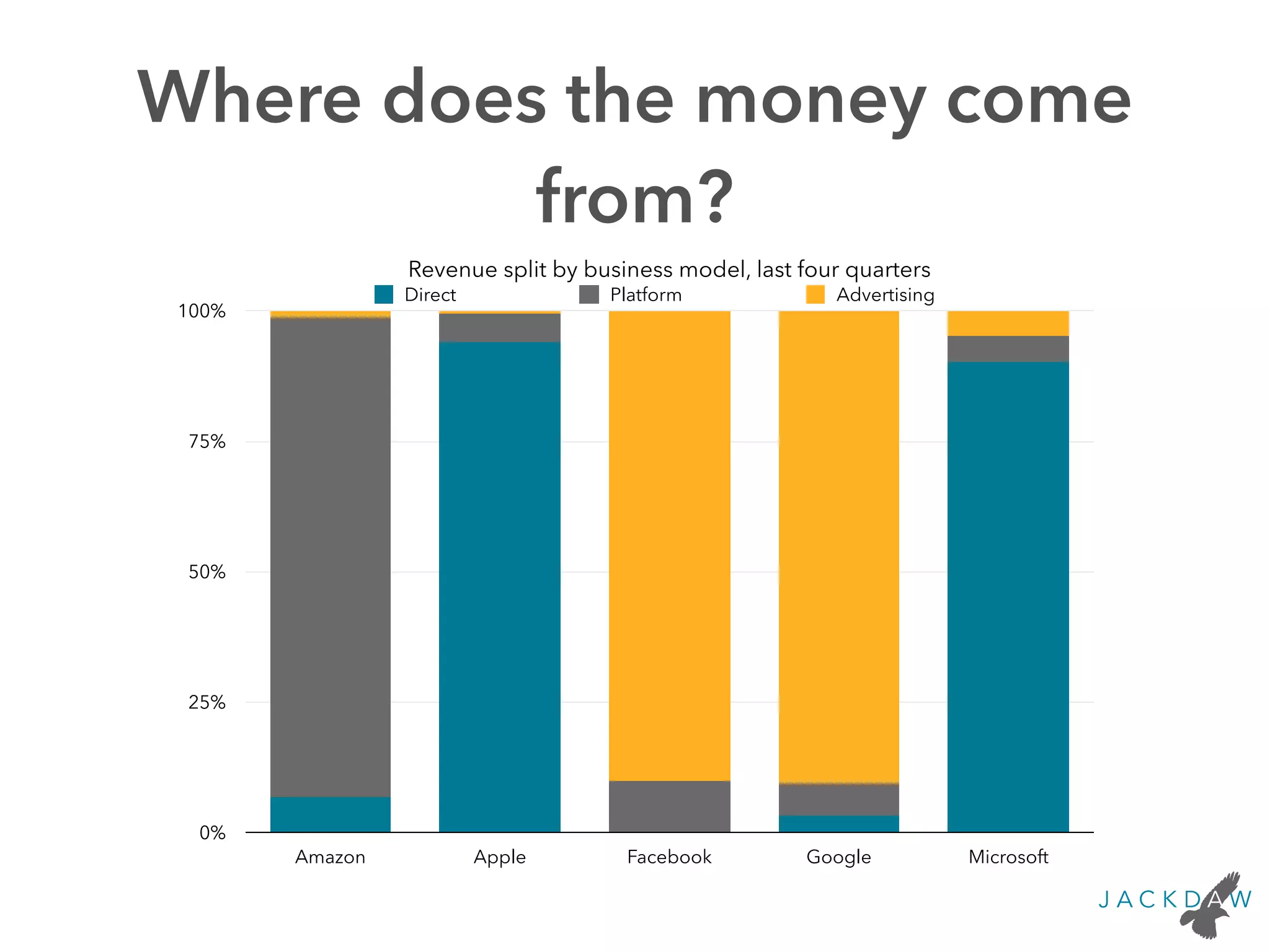

Presents revenue splits among business models for Amazon, Apple, Facebook, Google, and Microsoft.

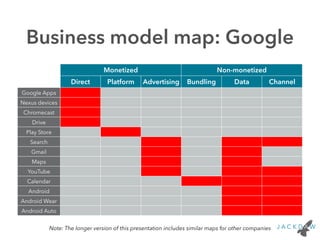

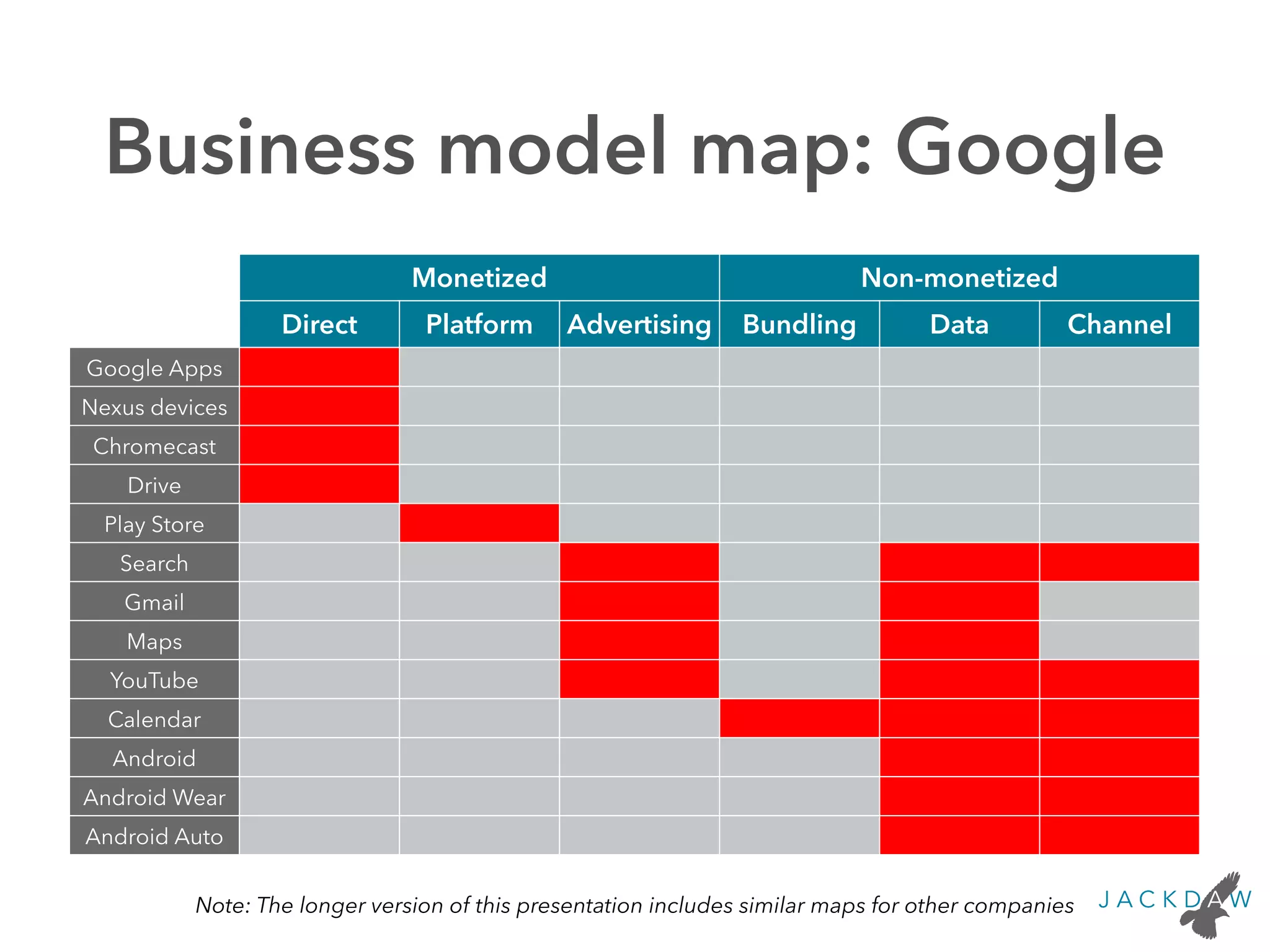

Visualizes Google's monetized and non-monetized offerings across direct, platform, and advertising models.

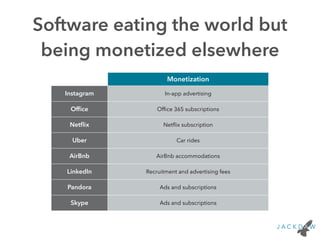

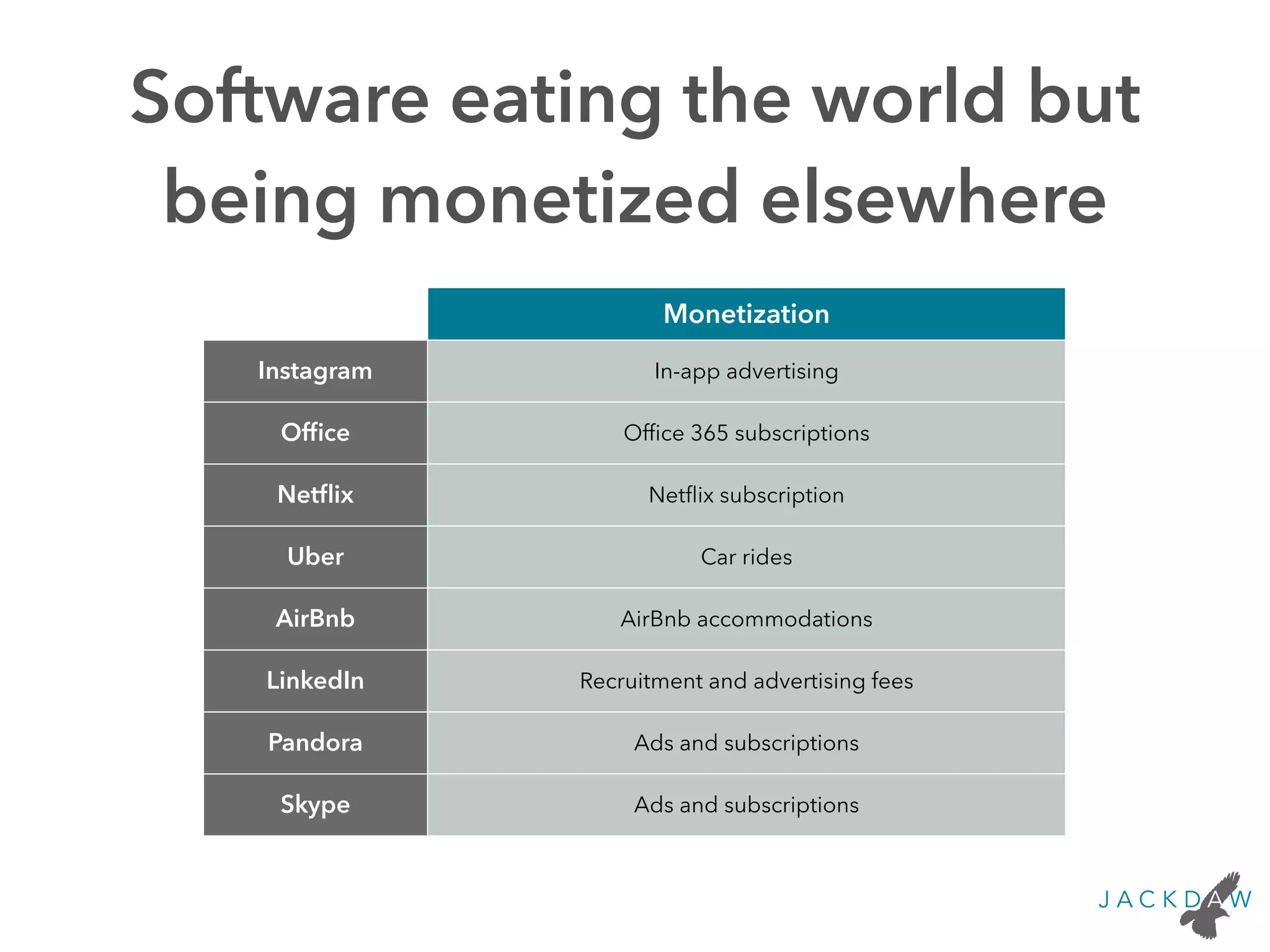

Discusses how software drives monetization through associated services rather than direct sales.

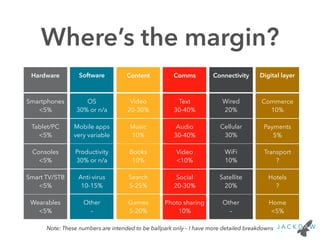

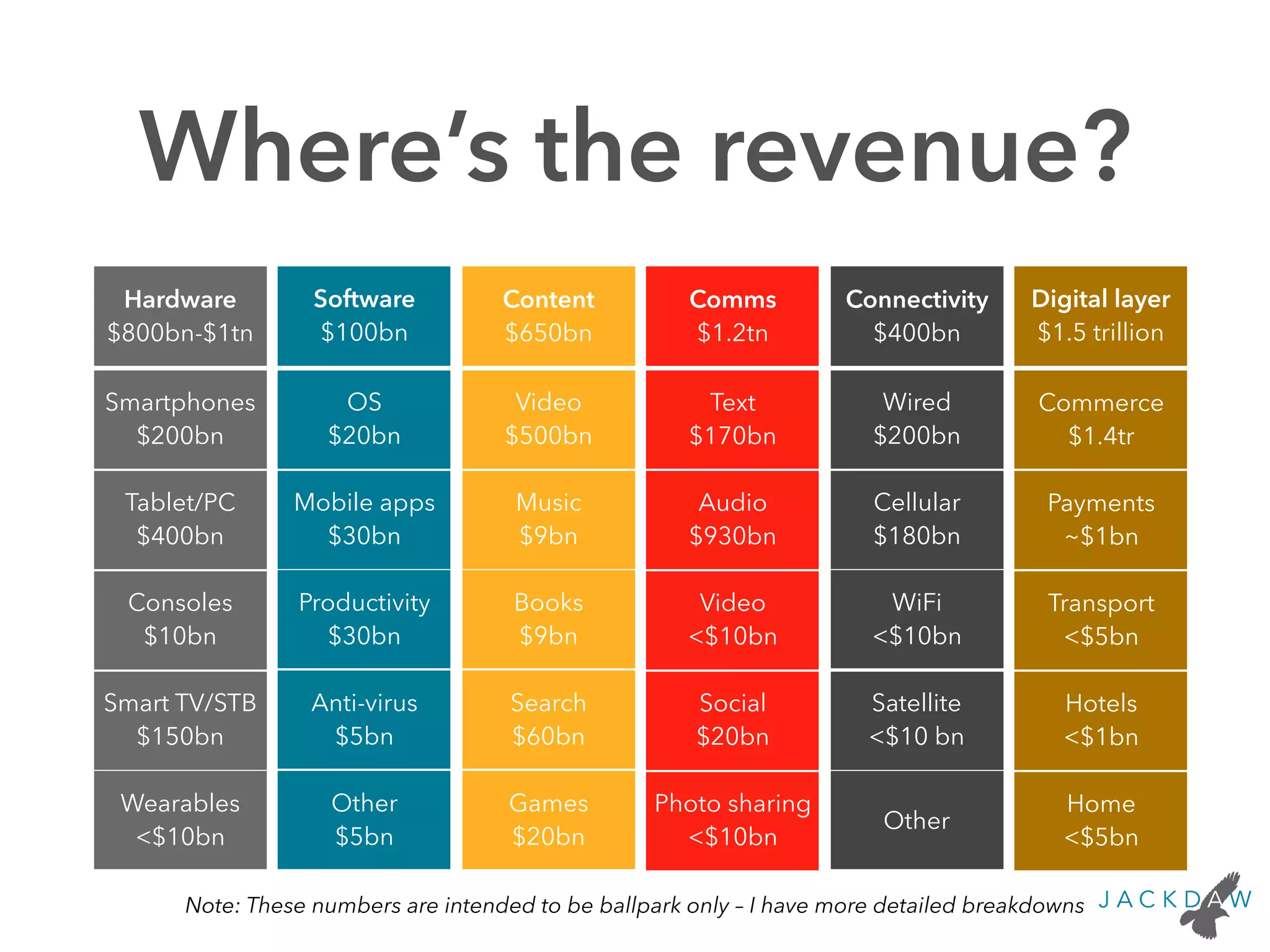

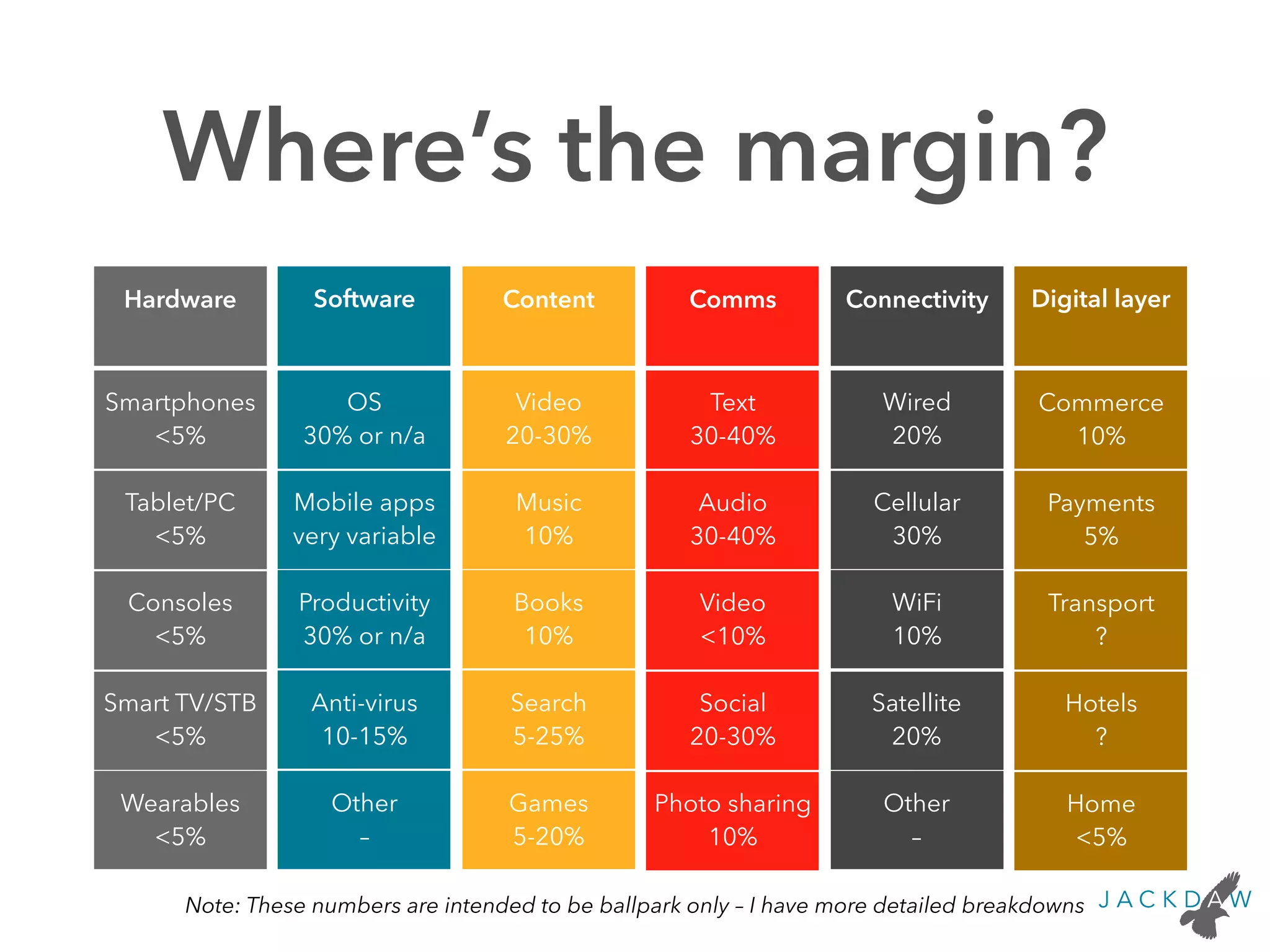

Presents revenue breakdowns across various consumer technology sectors and services.

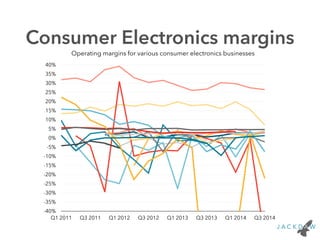

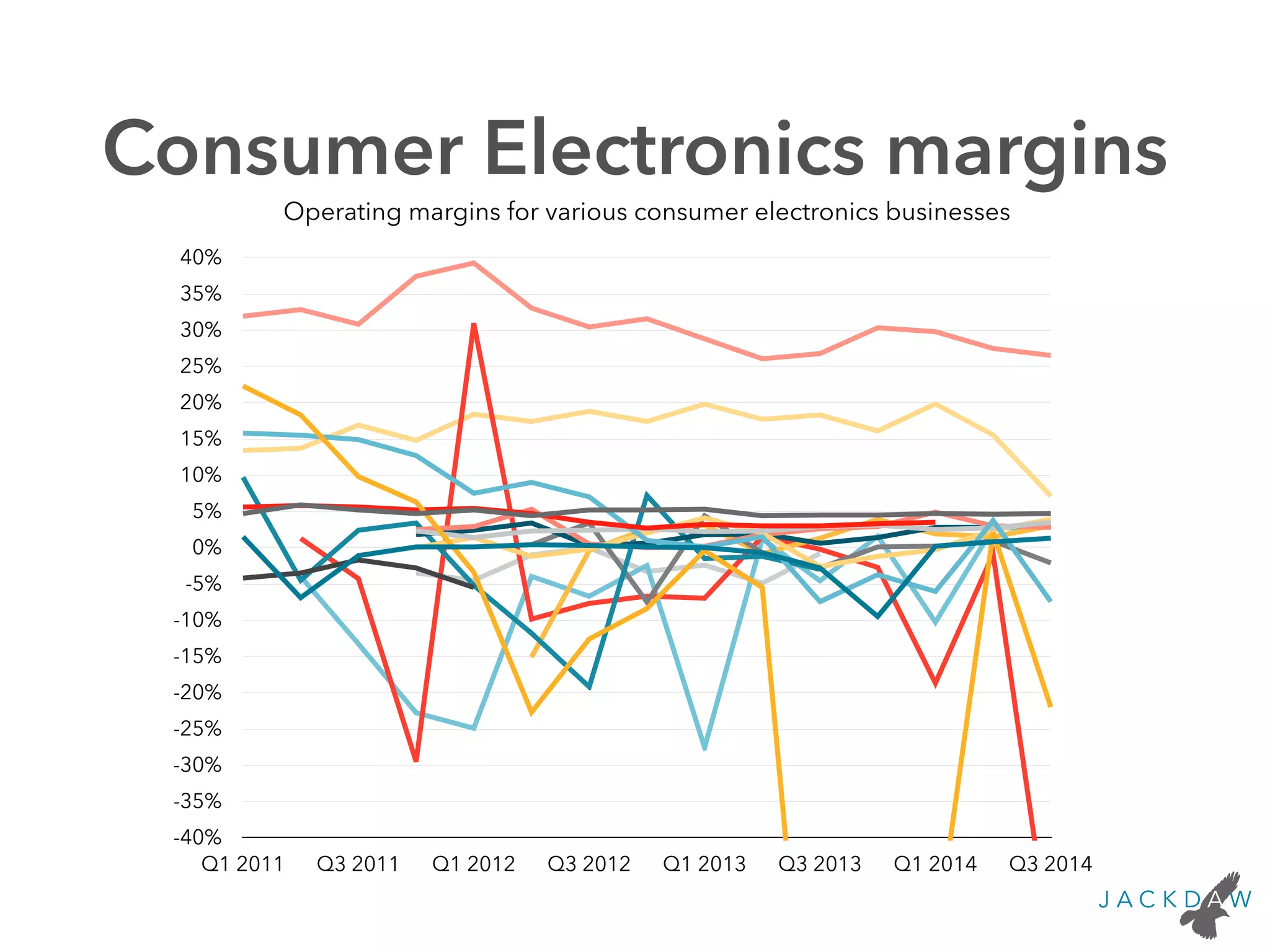

Analyzes operating margins in different consumer technology sectors with ballpark figures.

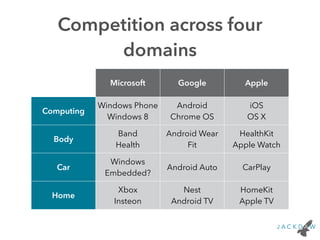

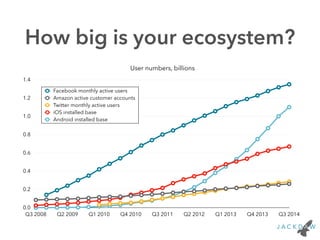

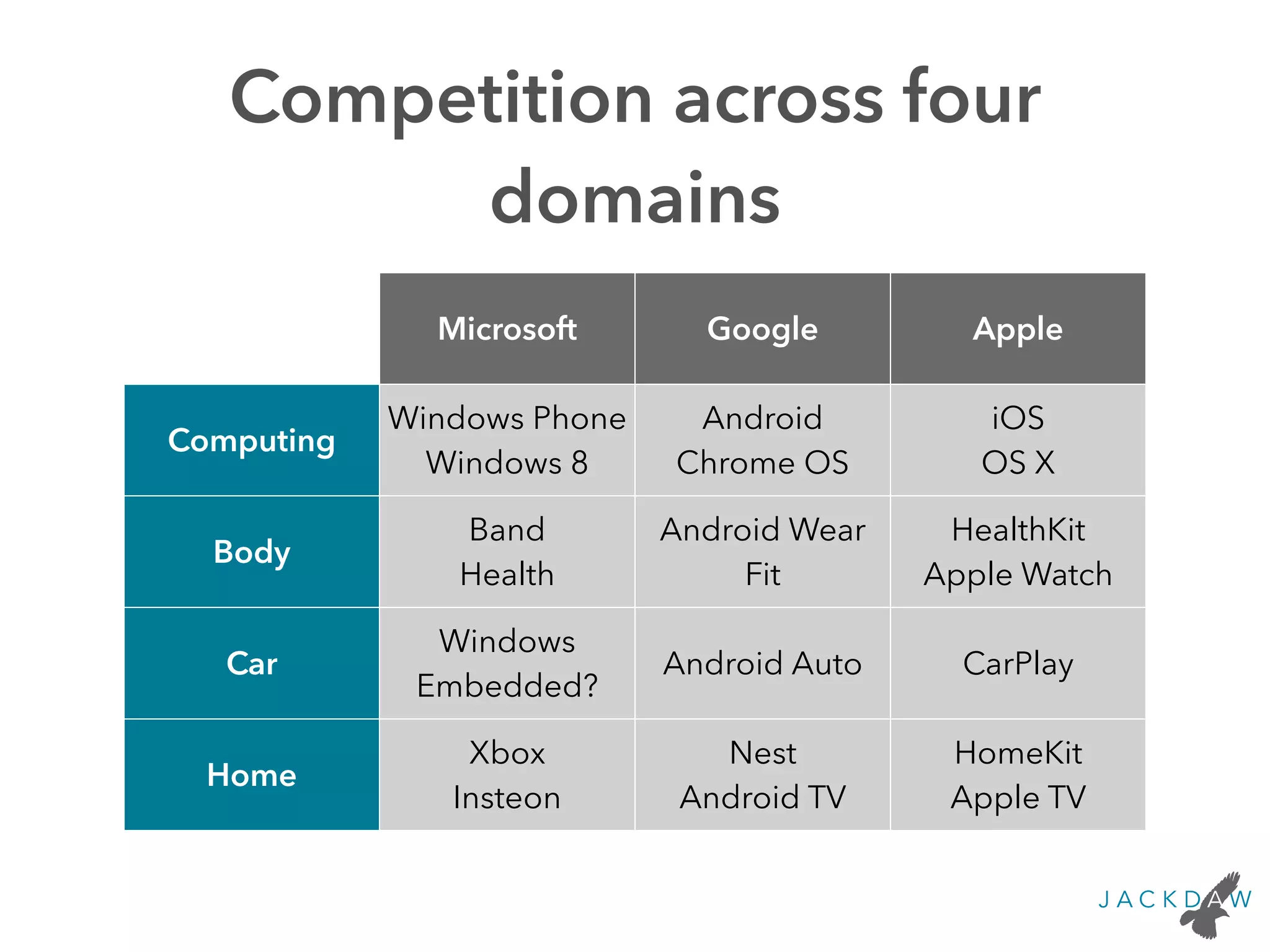

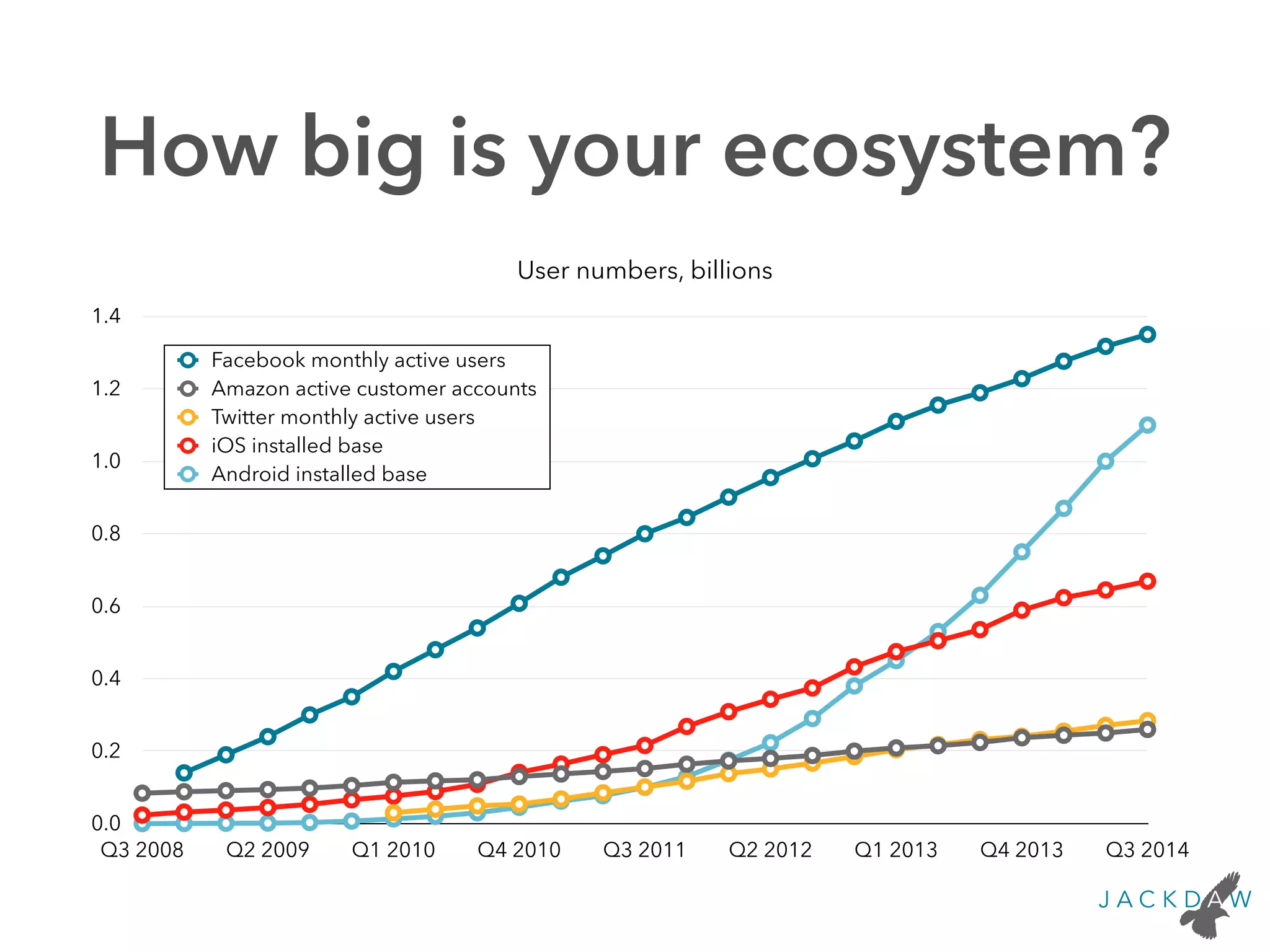

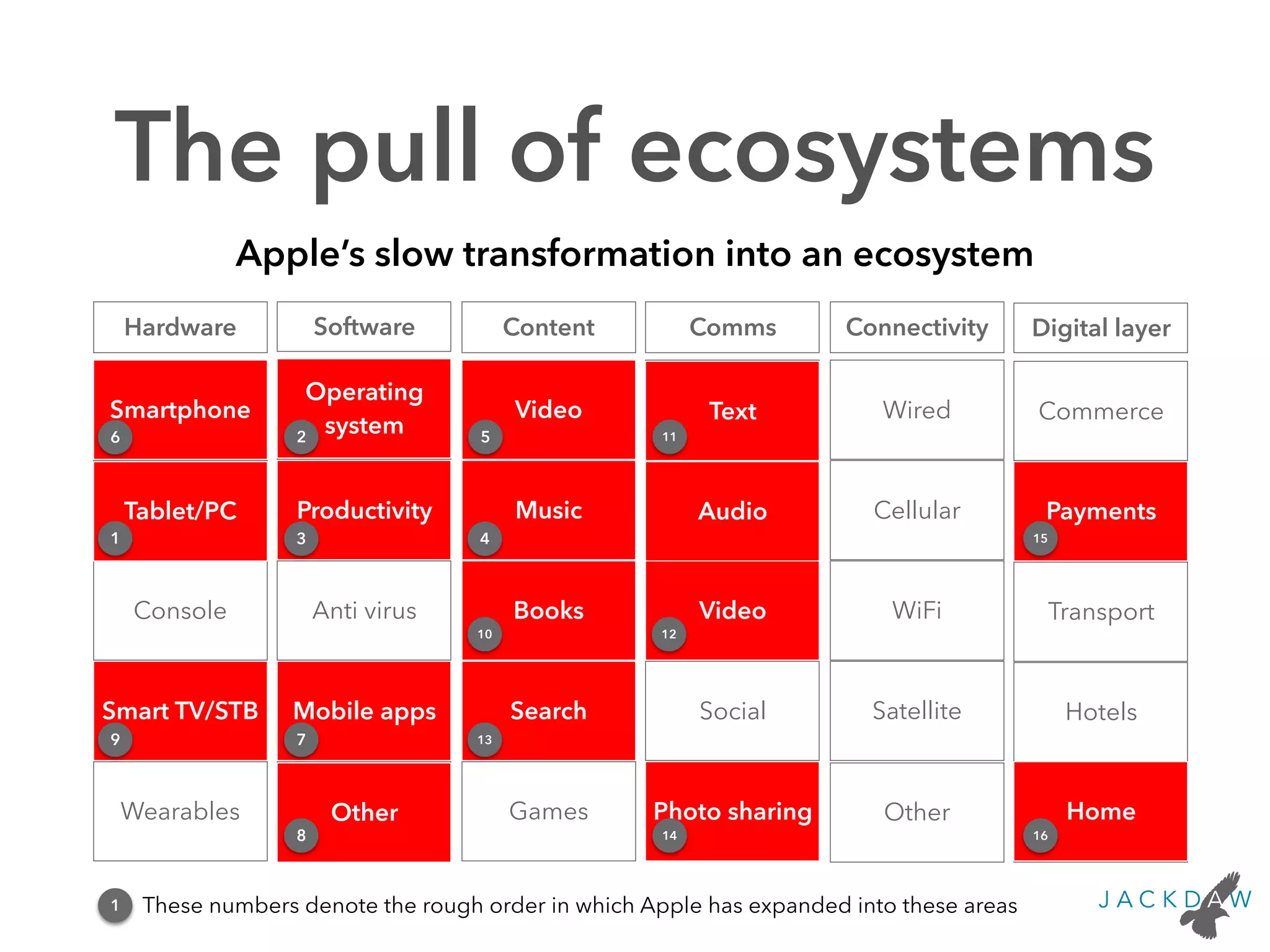

Highlights ecosystems' role in providing value and synergies, emphasizing competition across domains.

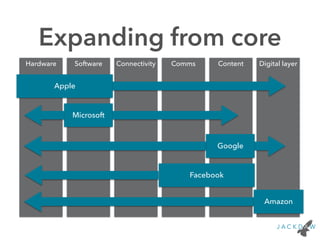

Outlines how tech companies expand into ecosystems, competing in various categories.

Summarizes key points: ecosystems' importance, competition across categories, and profitability nuances.

Jan Dawson concludes the presentation, reiterating contact details for further inquiries.