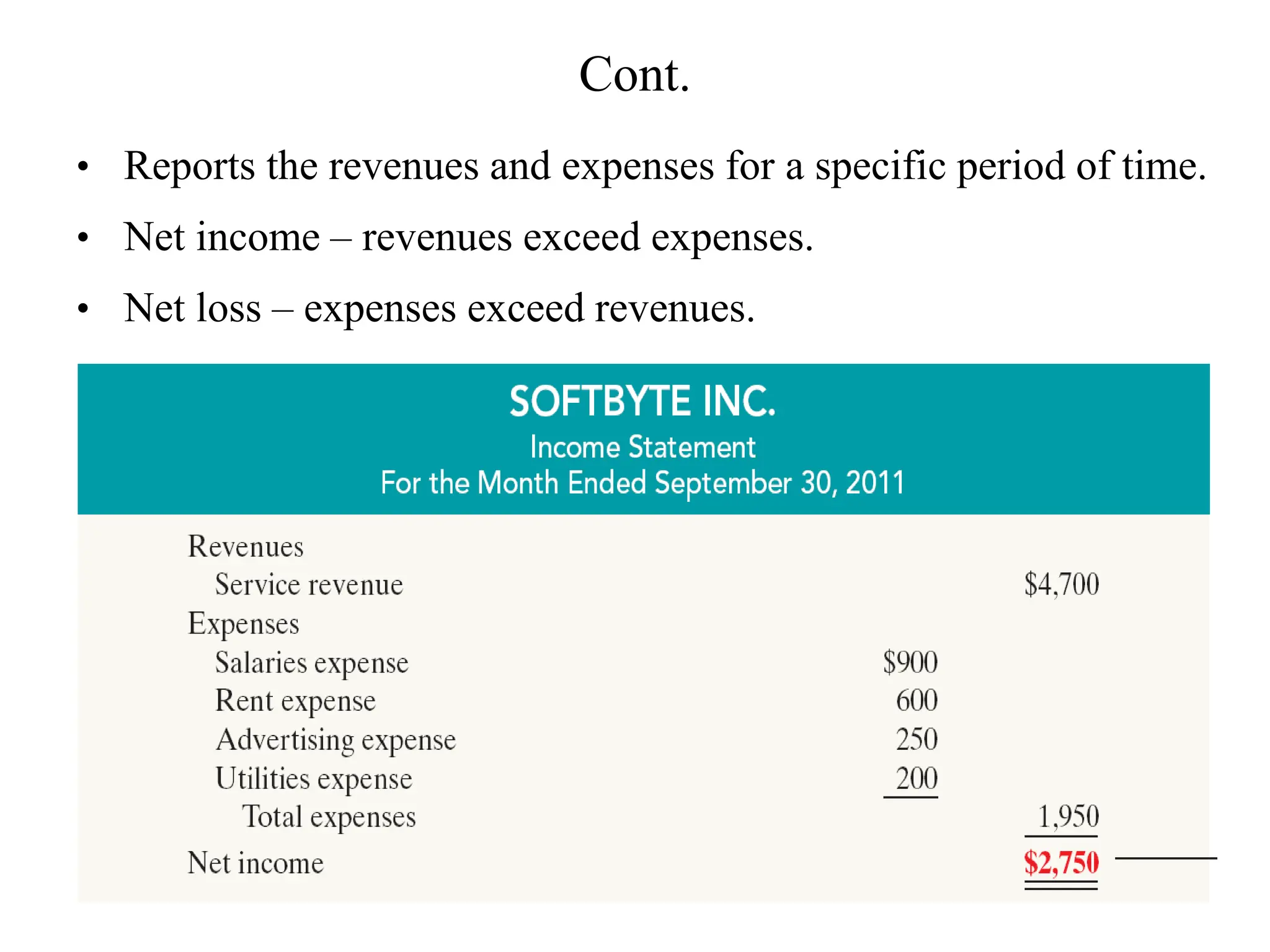

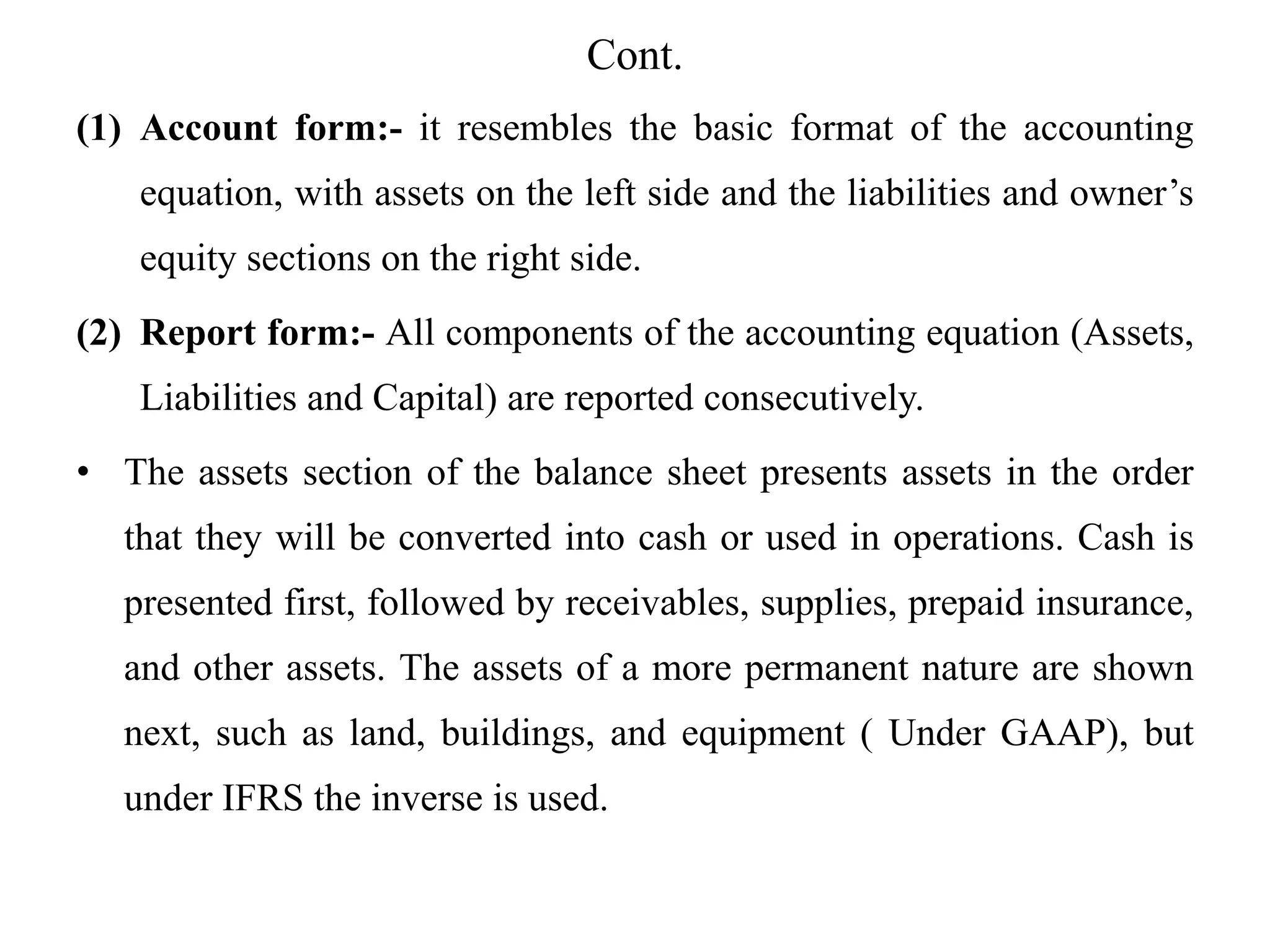

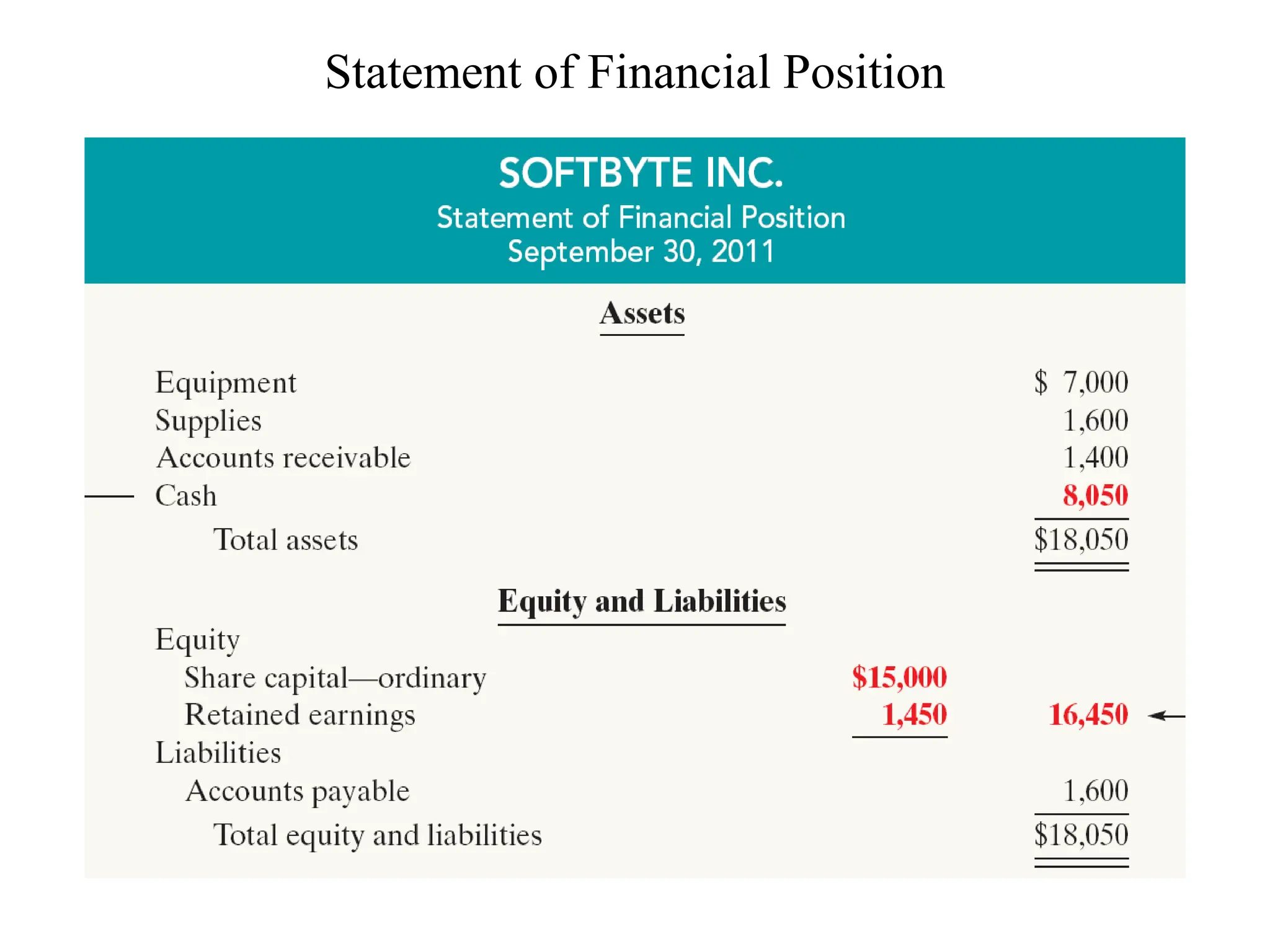

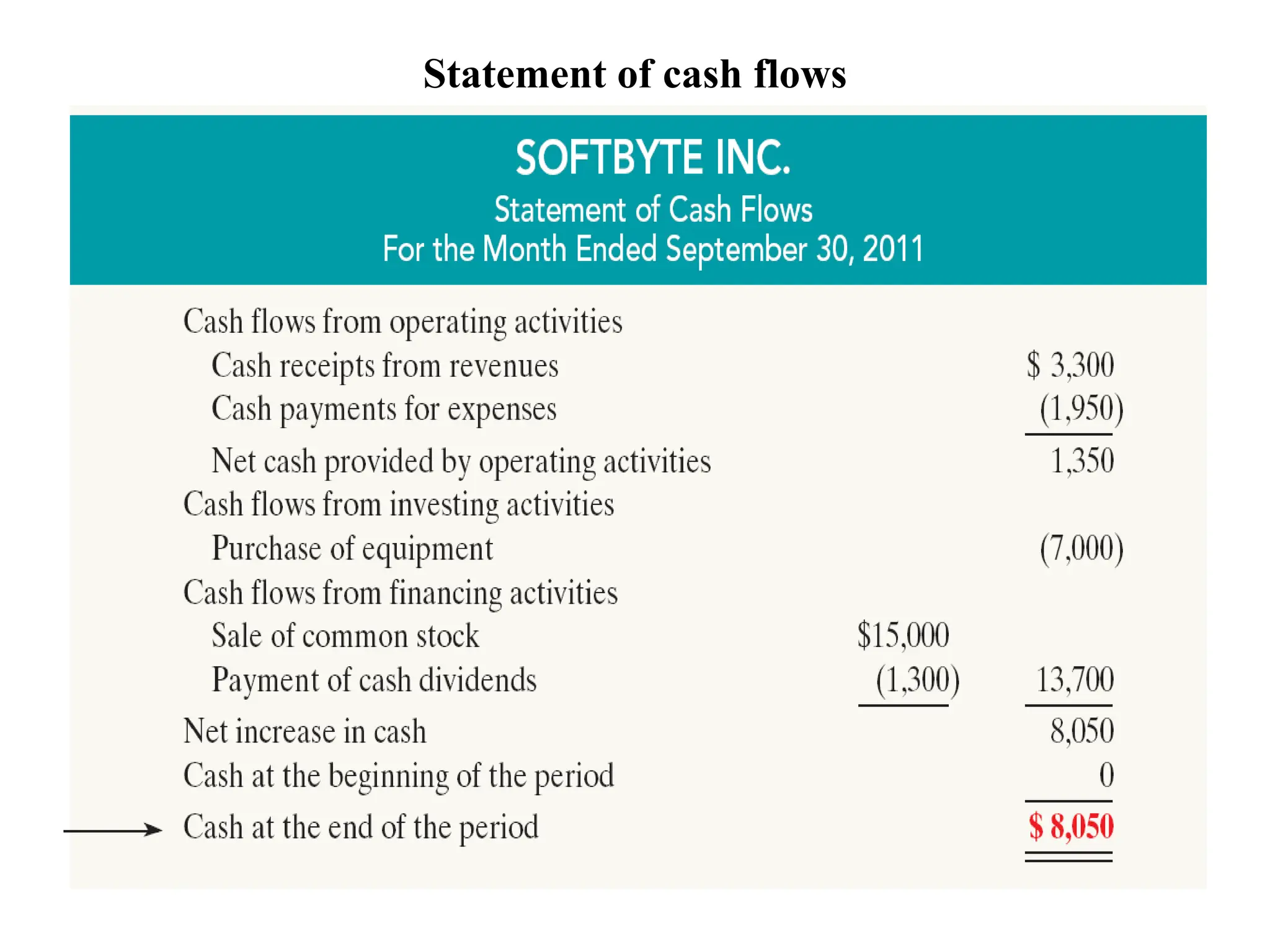

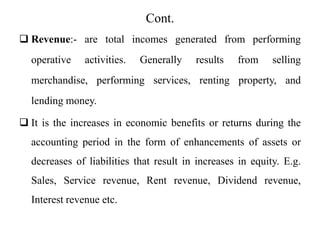

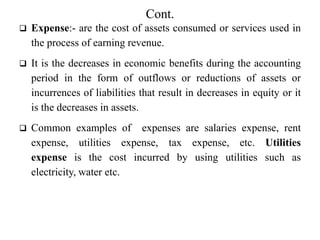

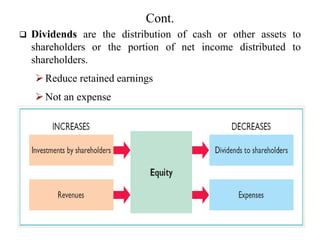

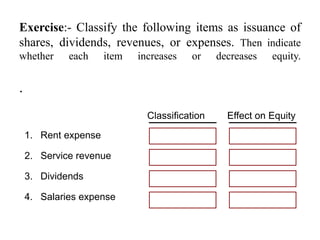

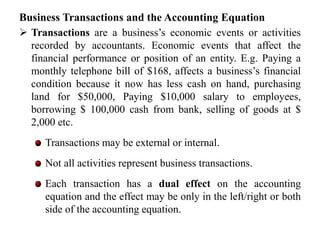

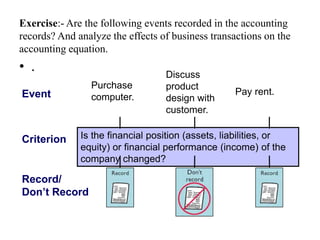

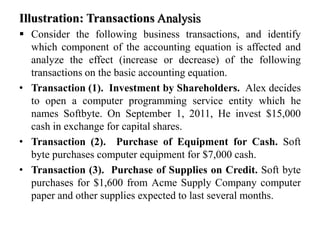

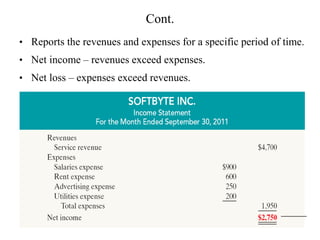

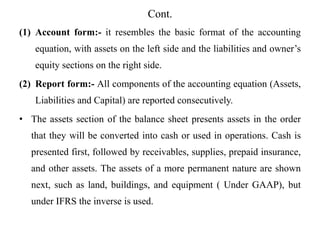

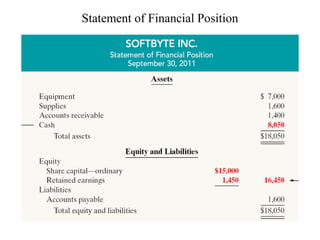

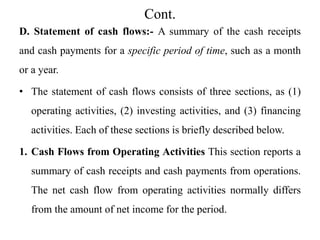

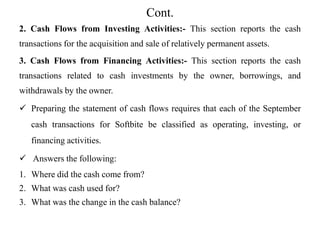

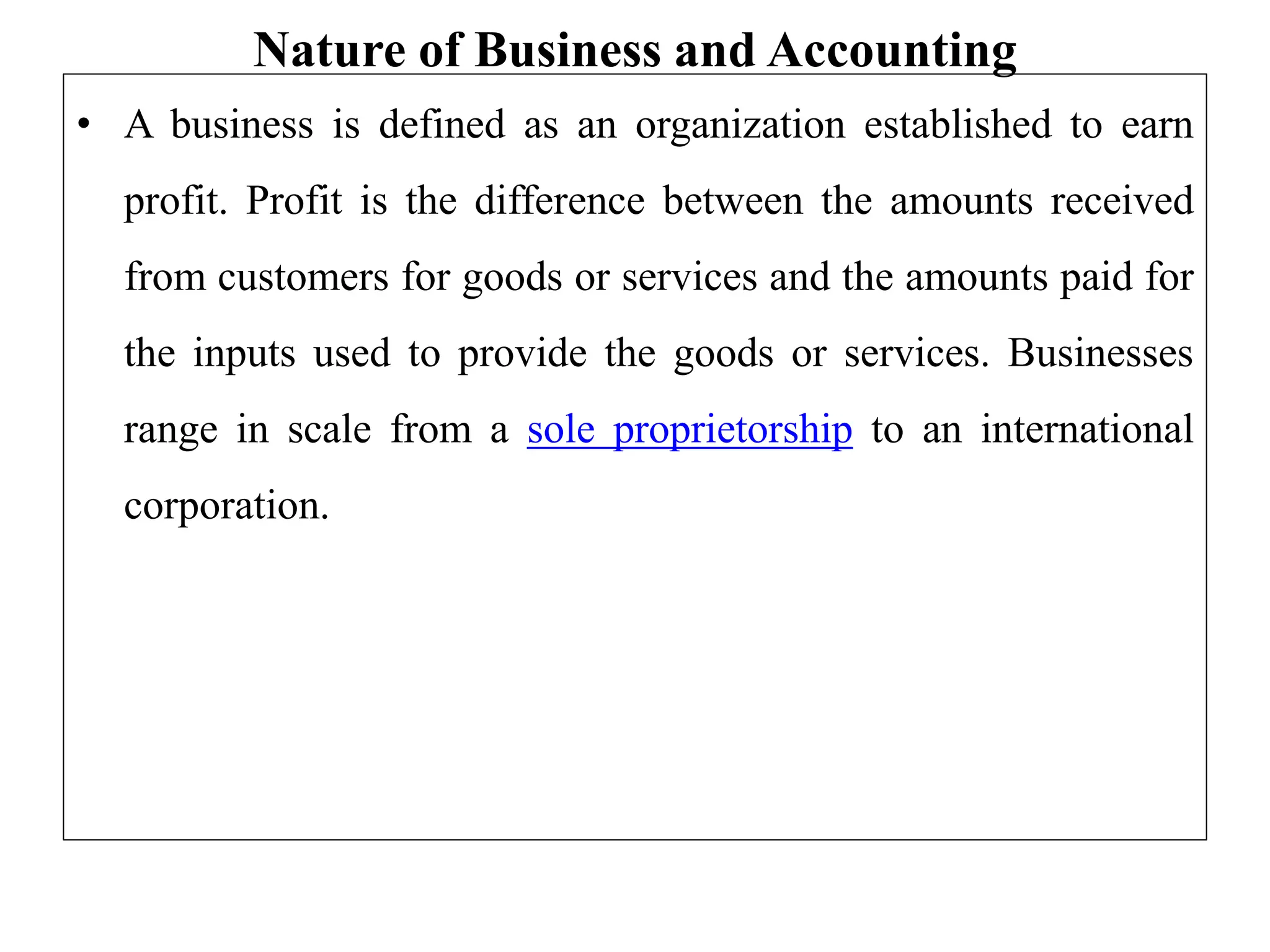

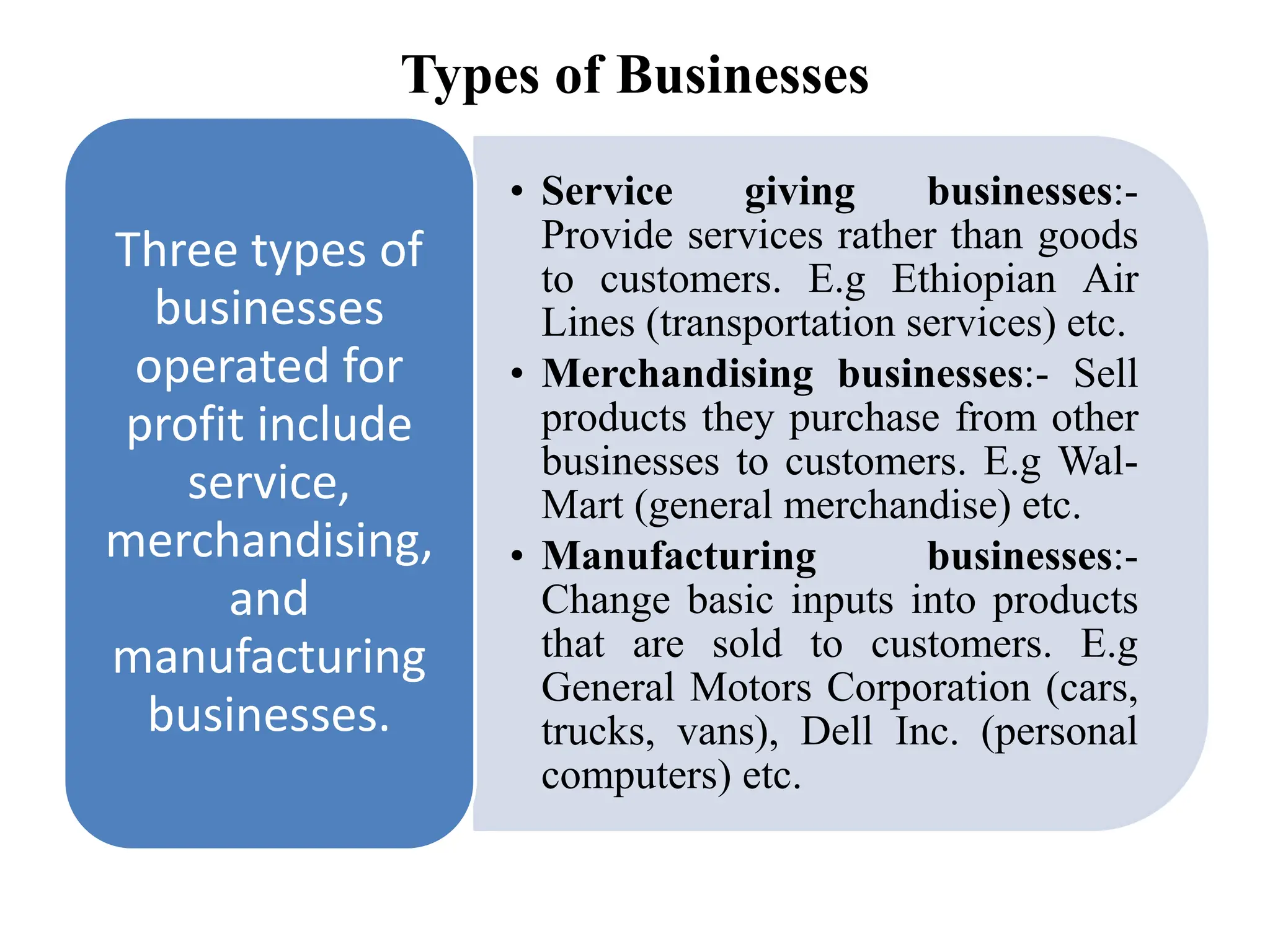

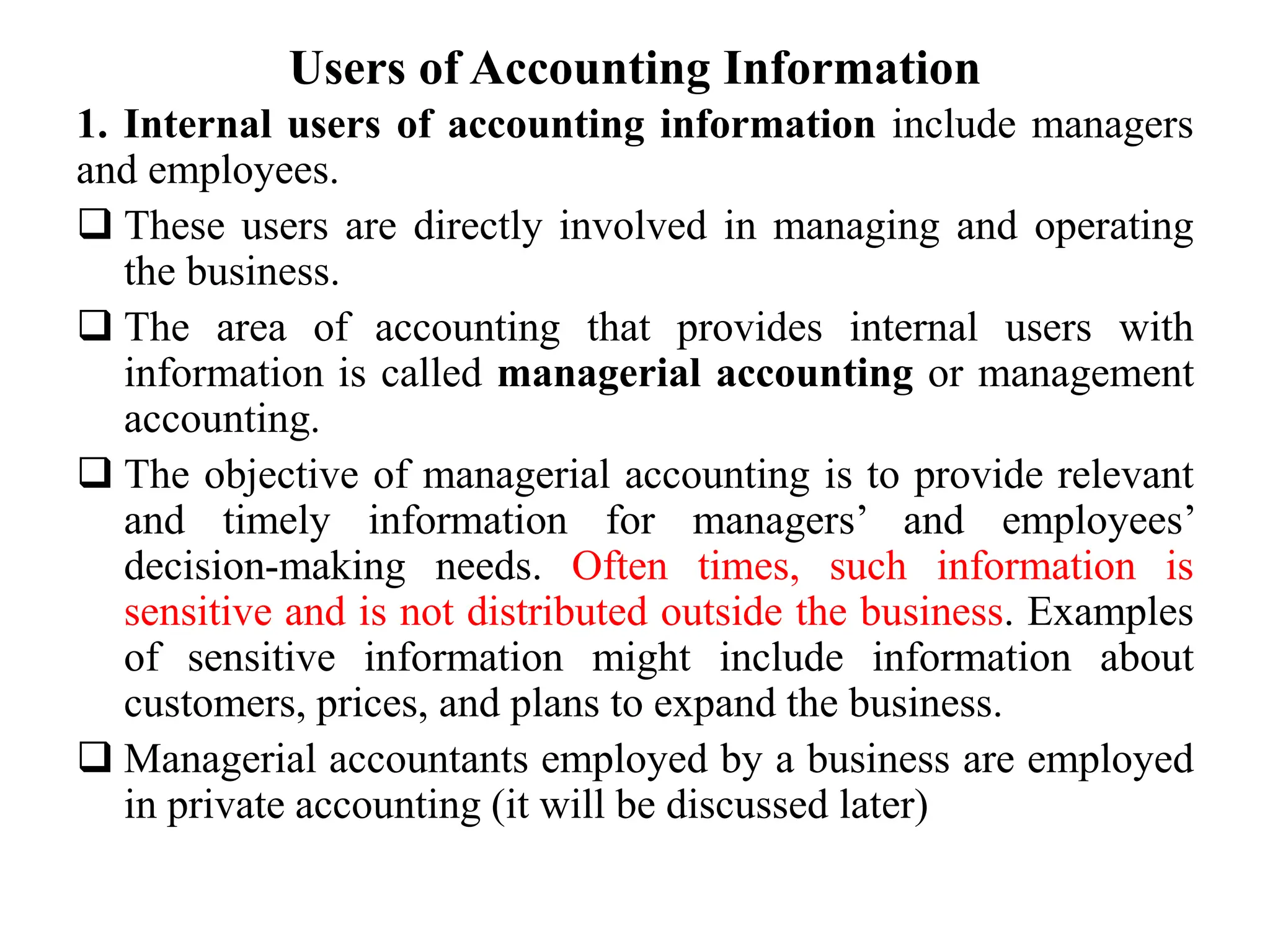

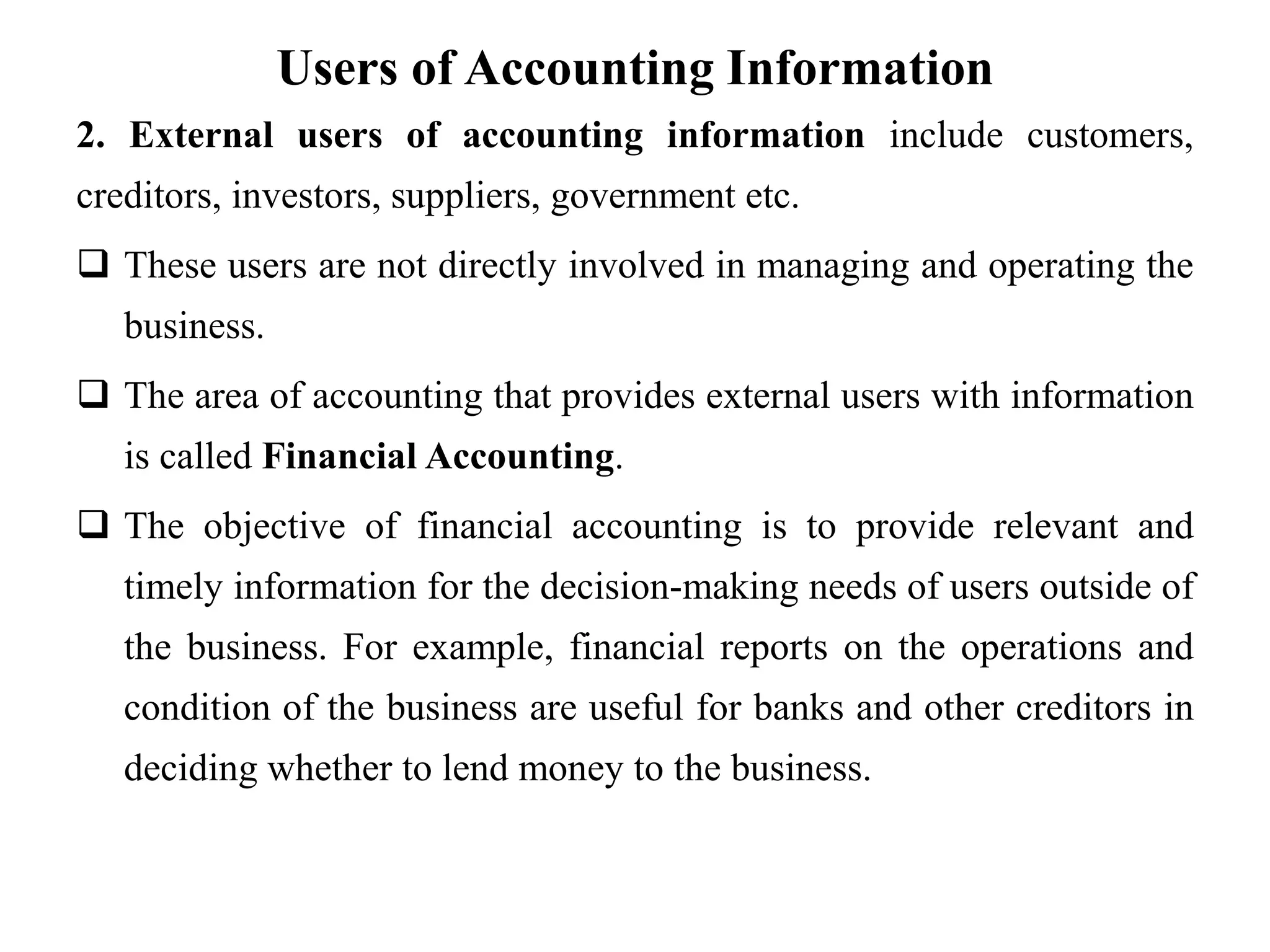

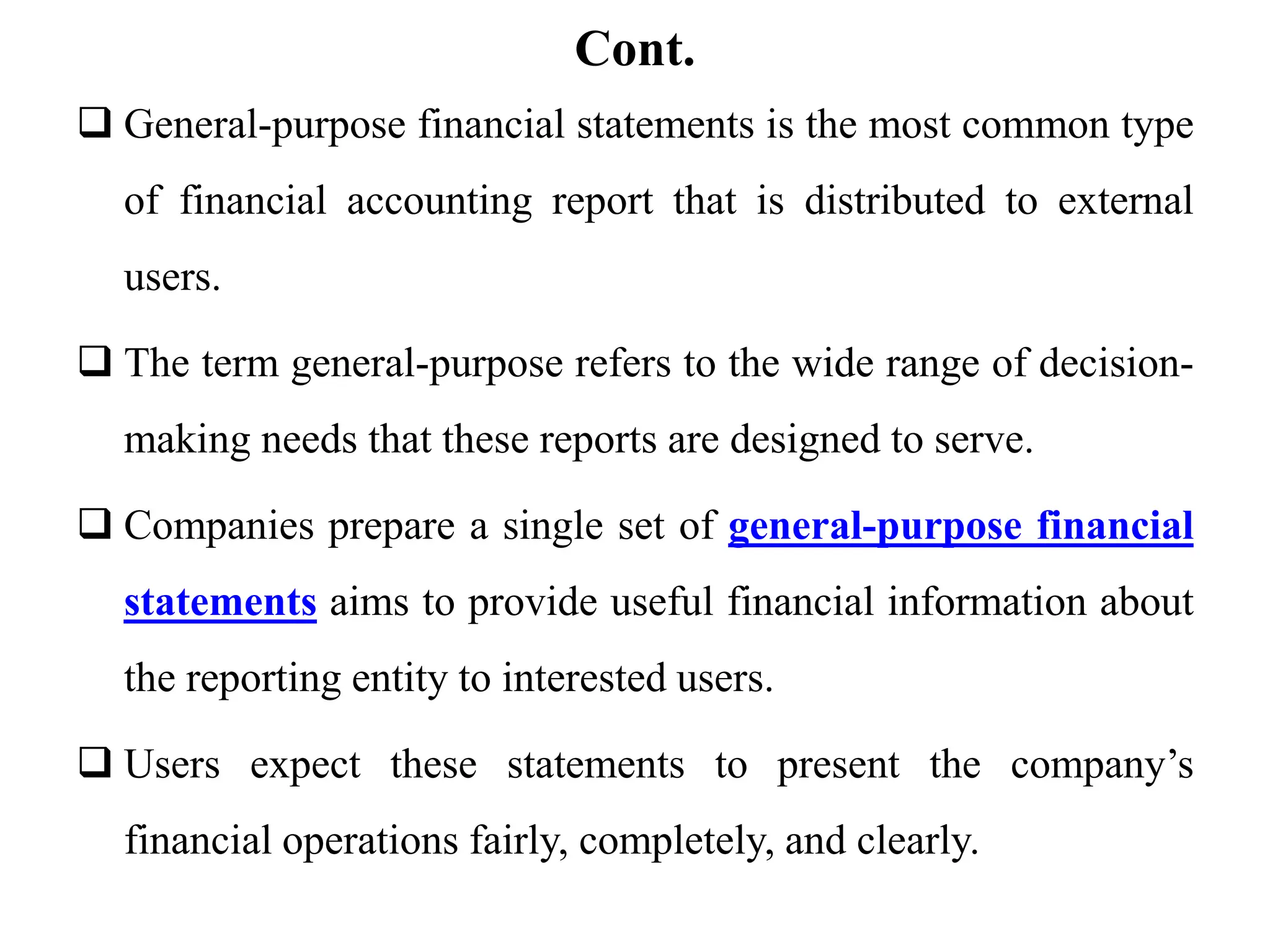

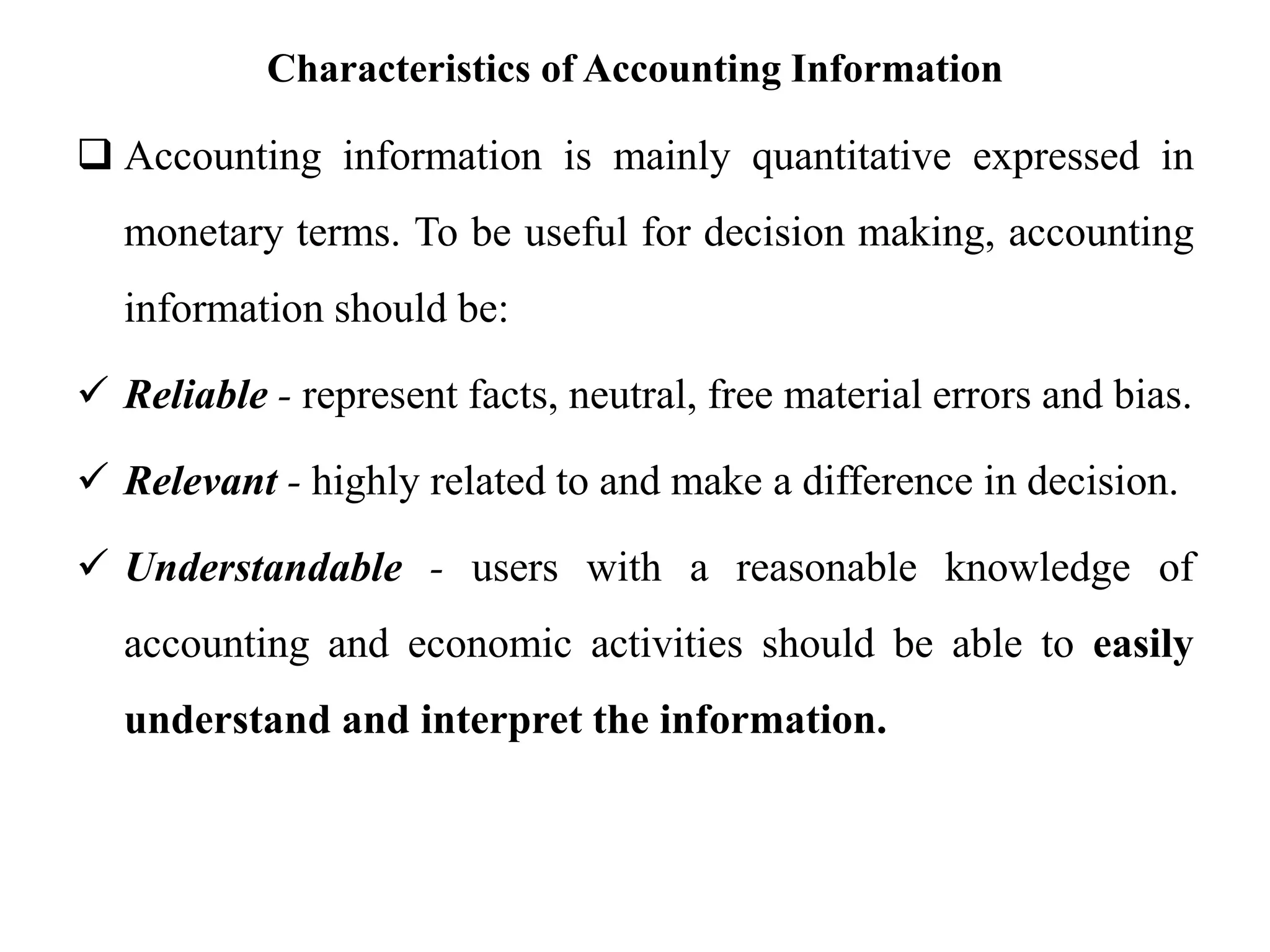

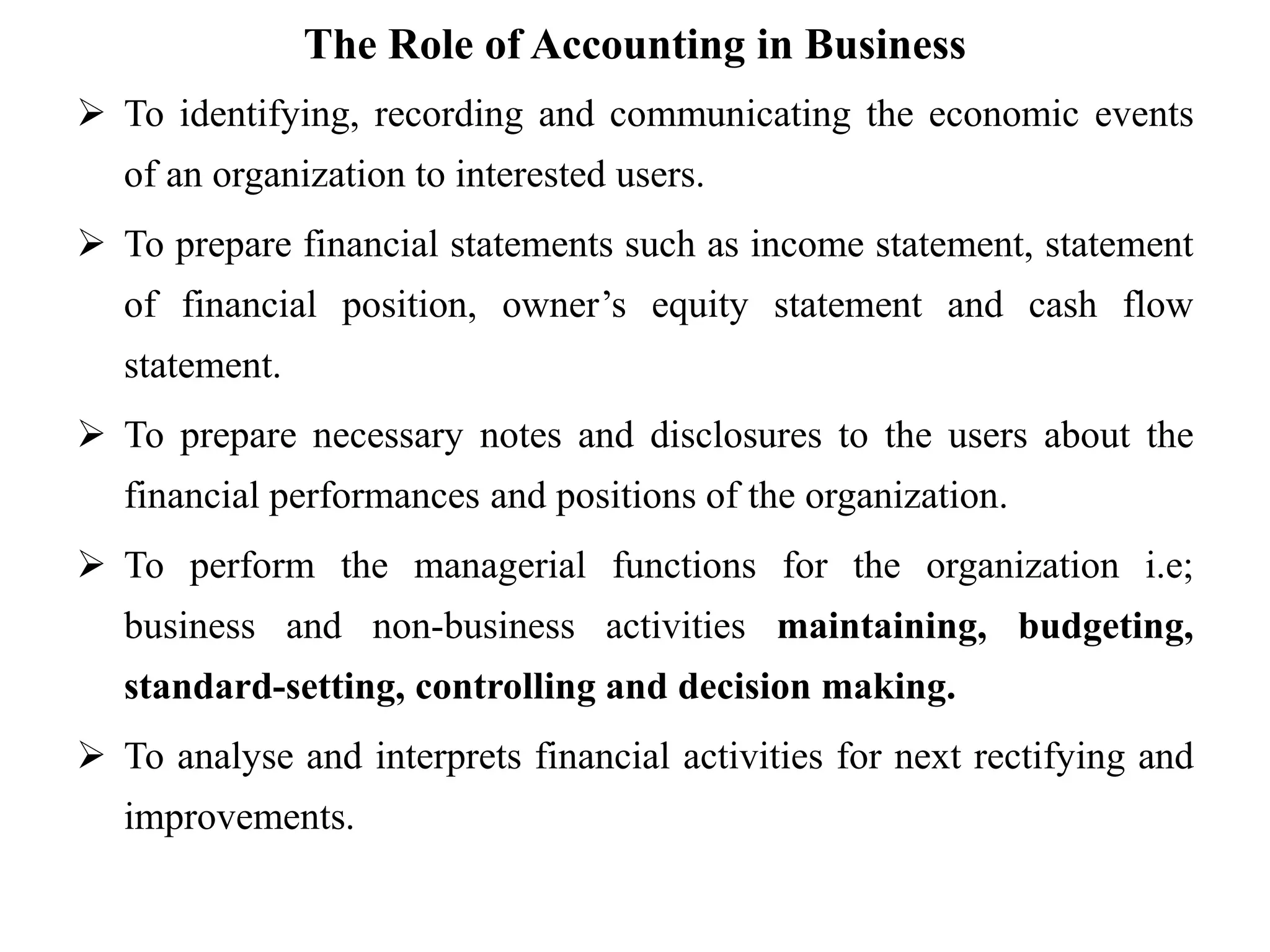

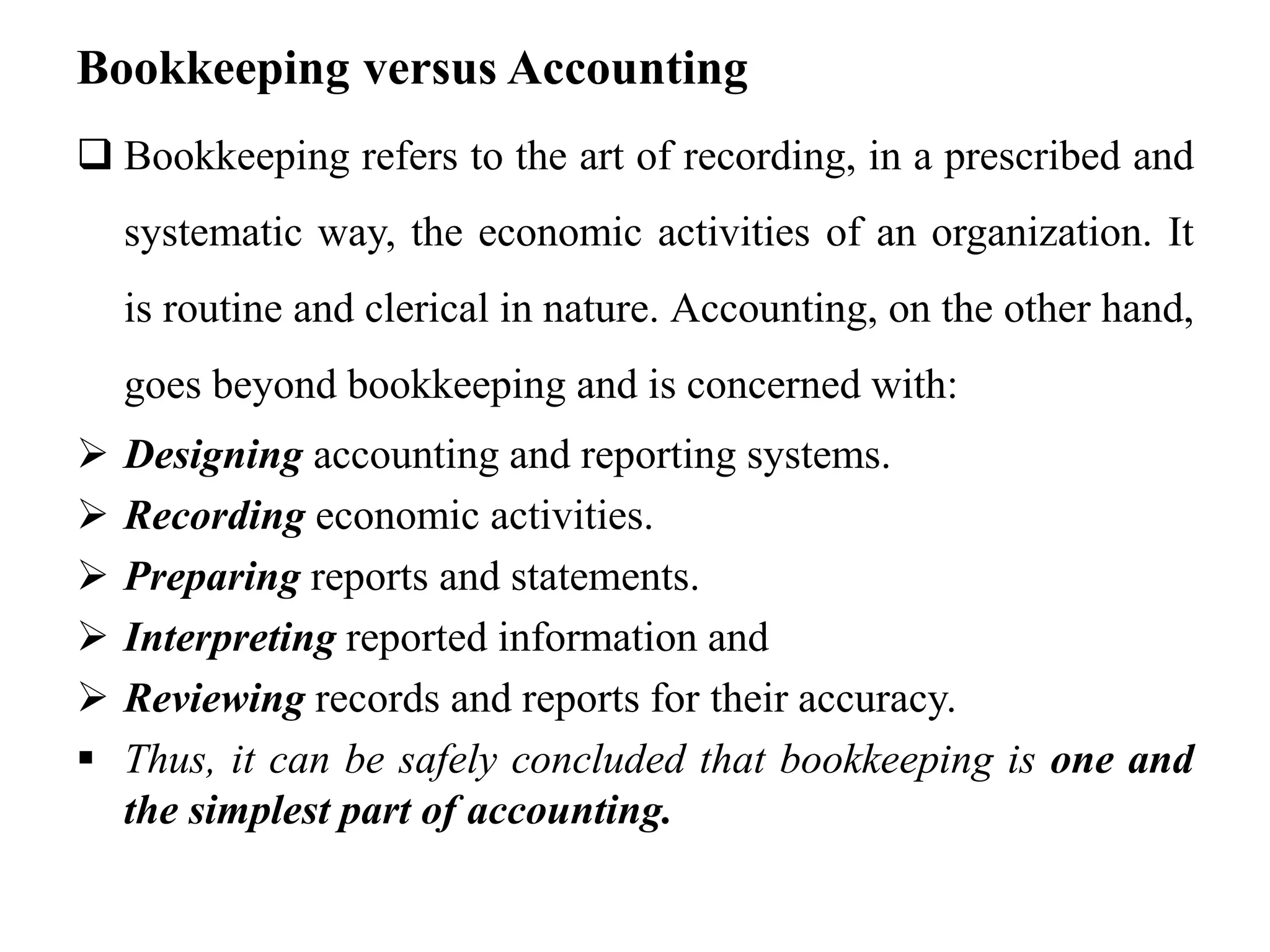

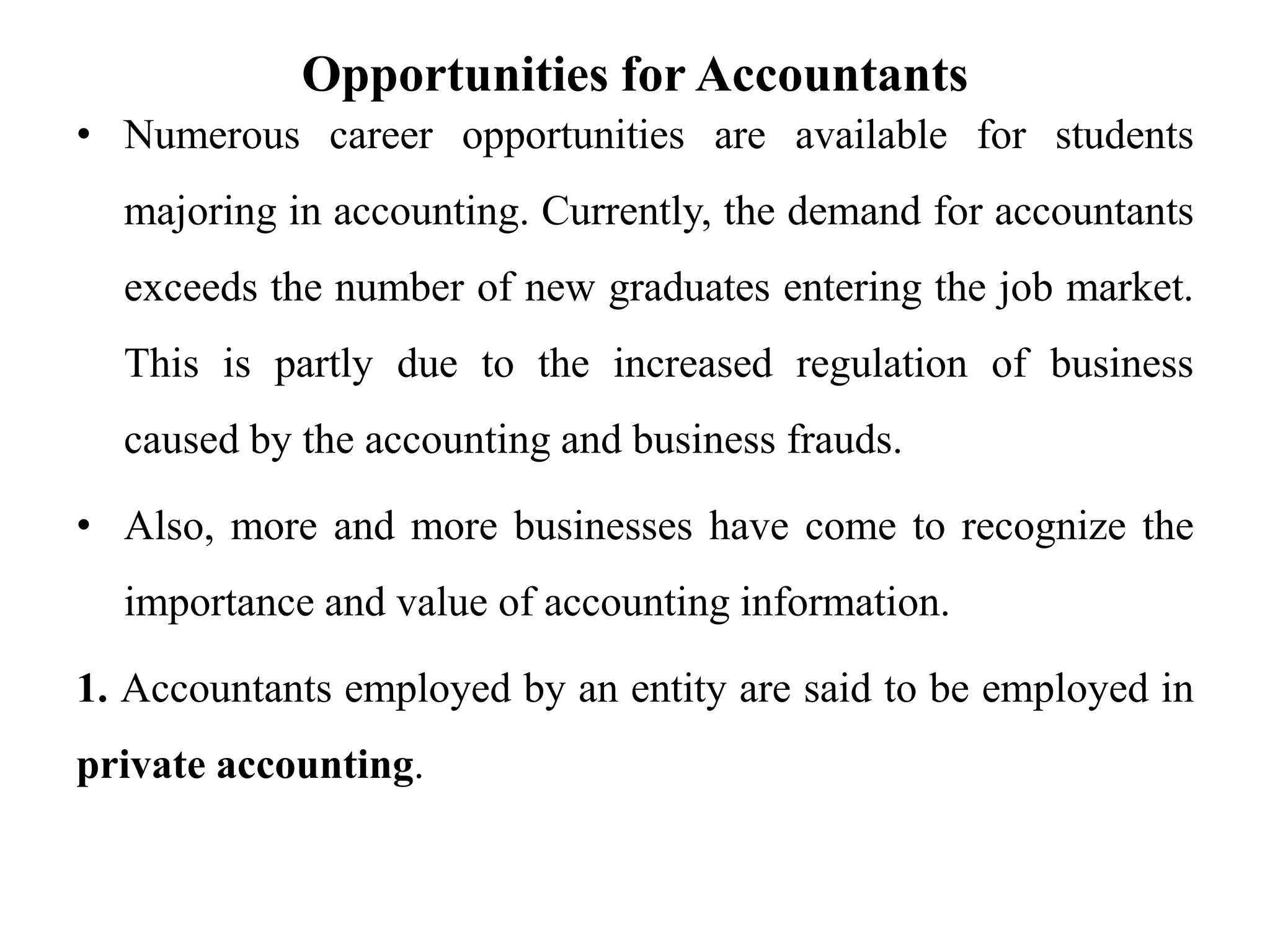

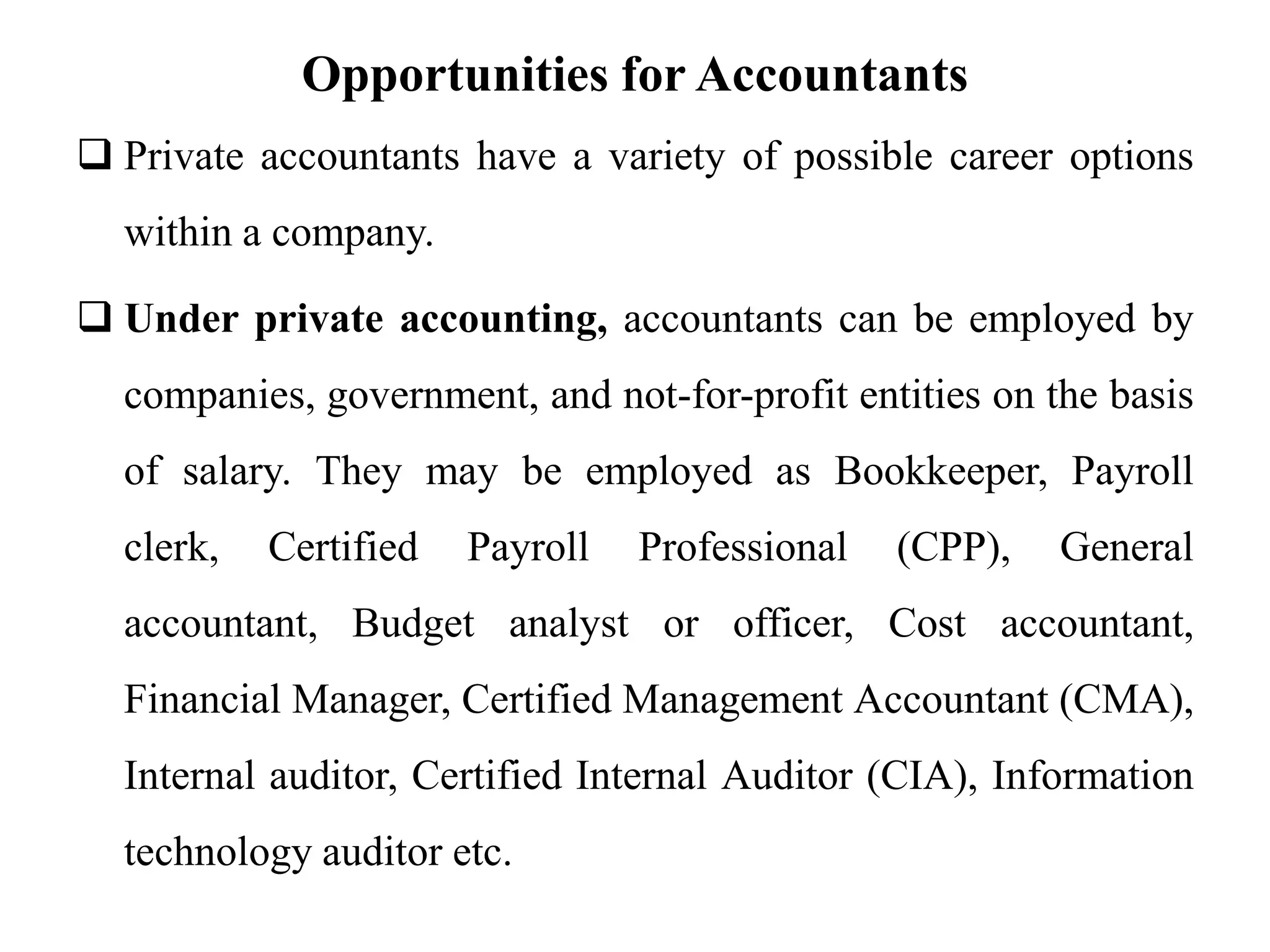

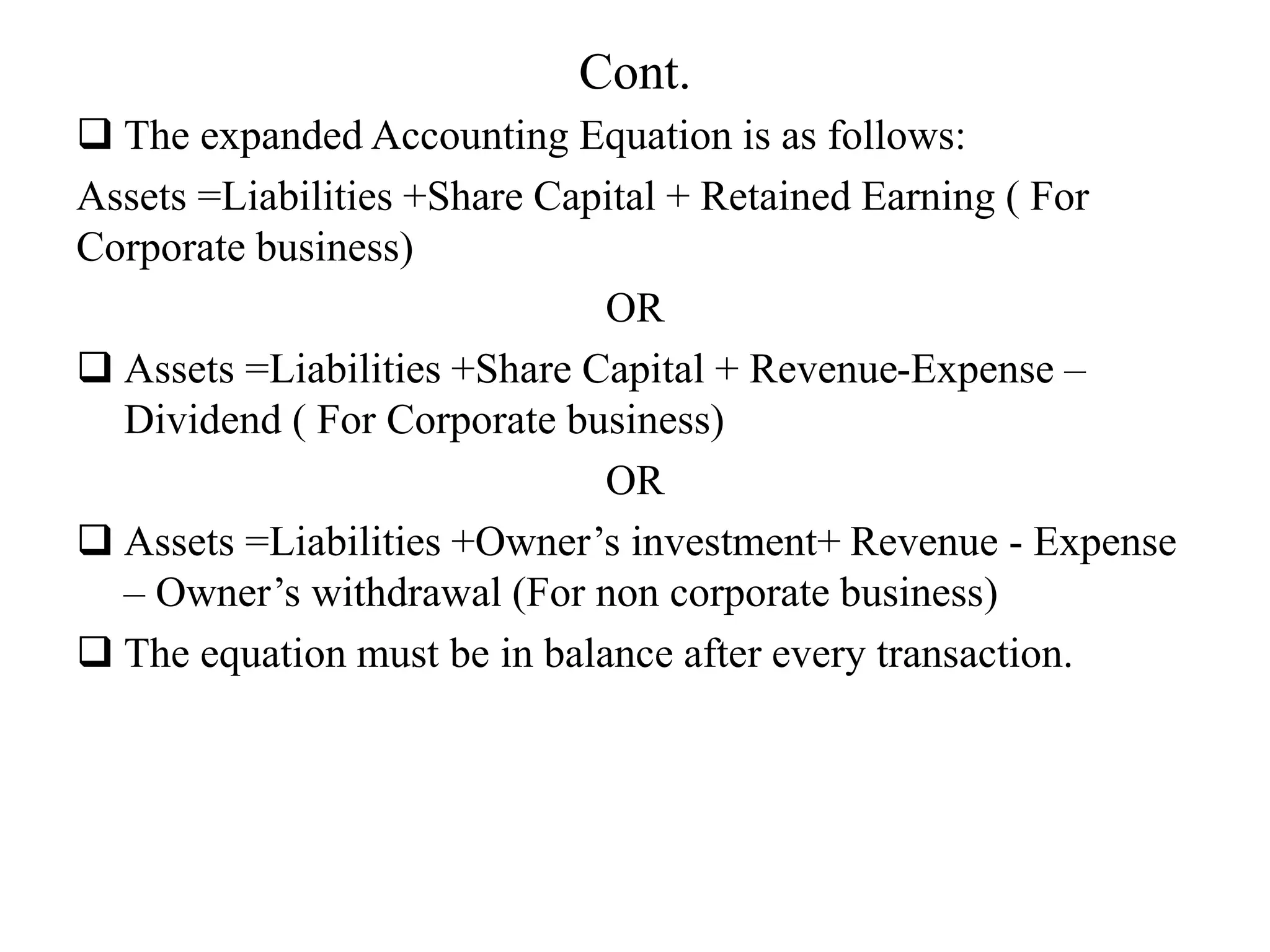

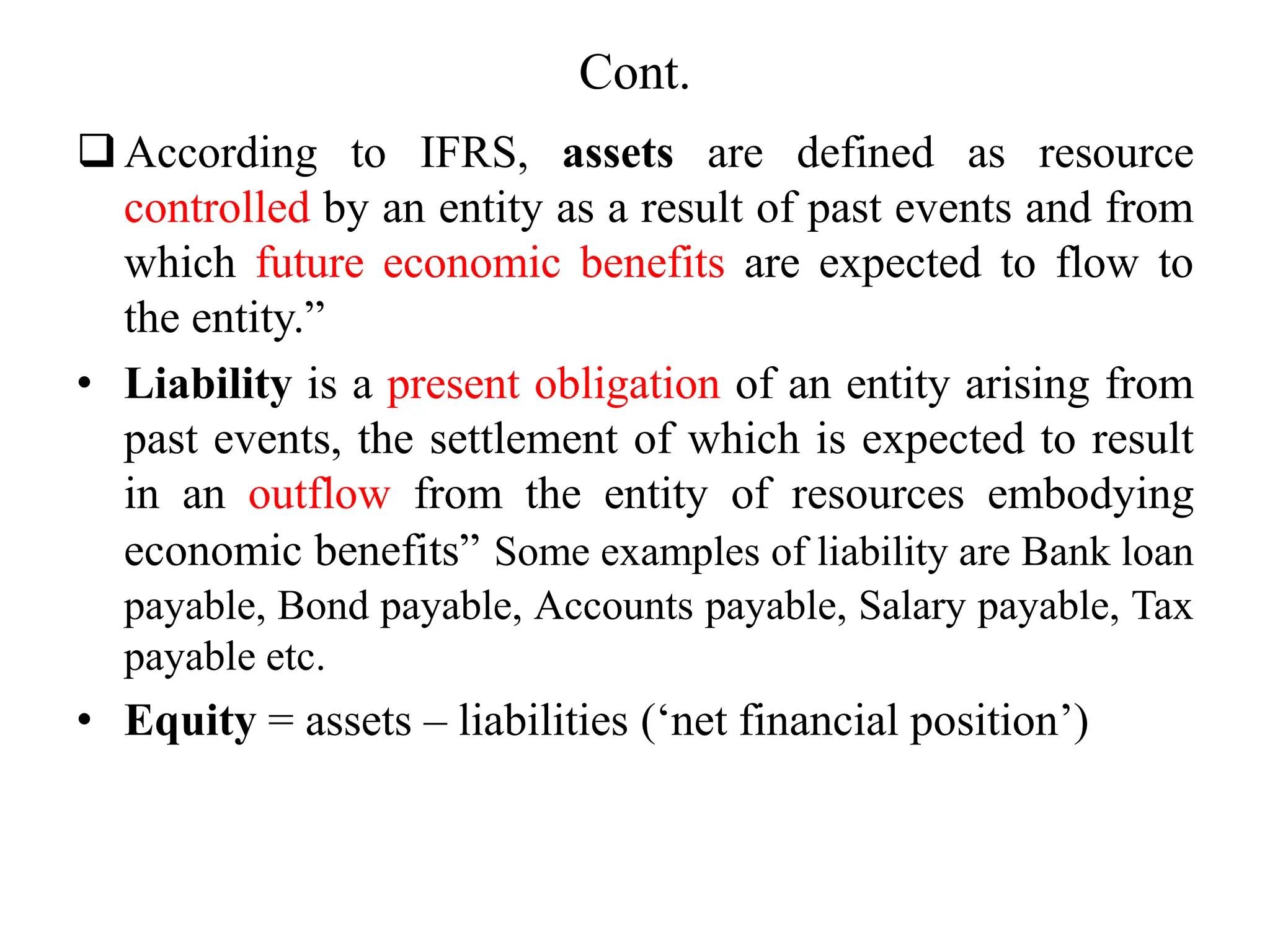

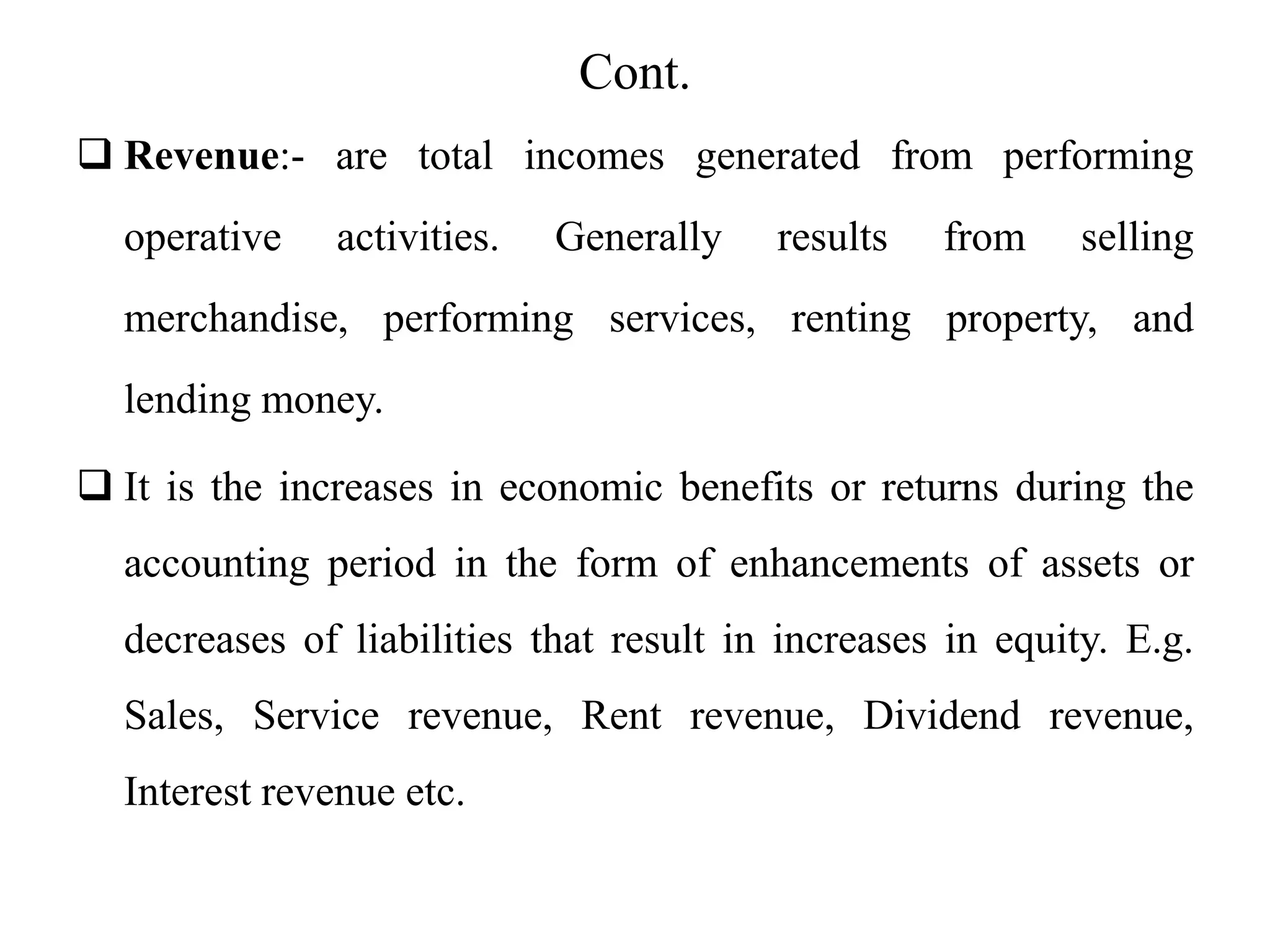

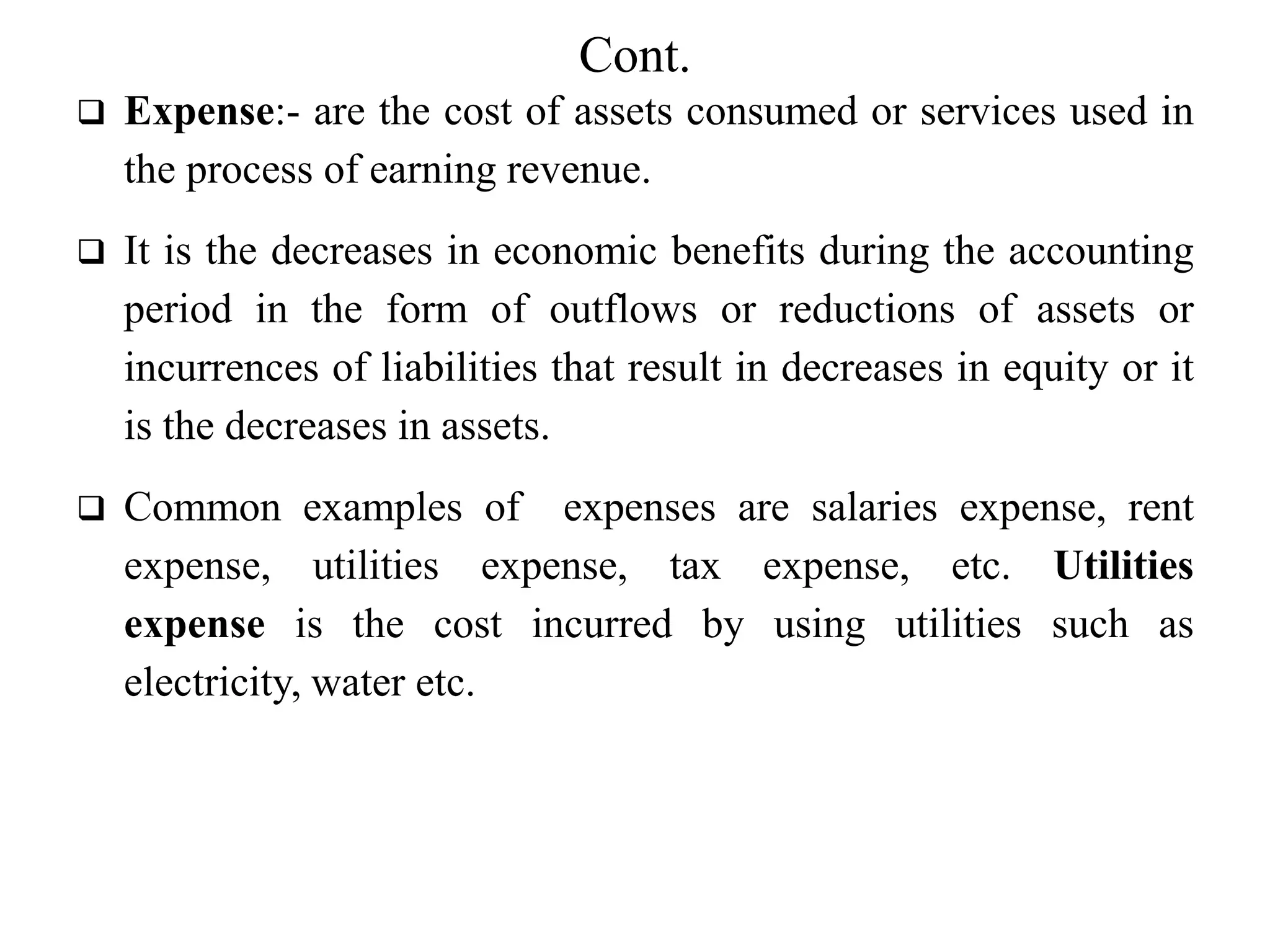

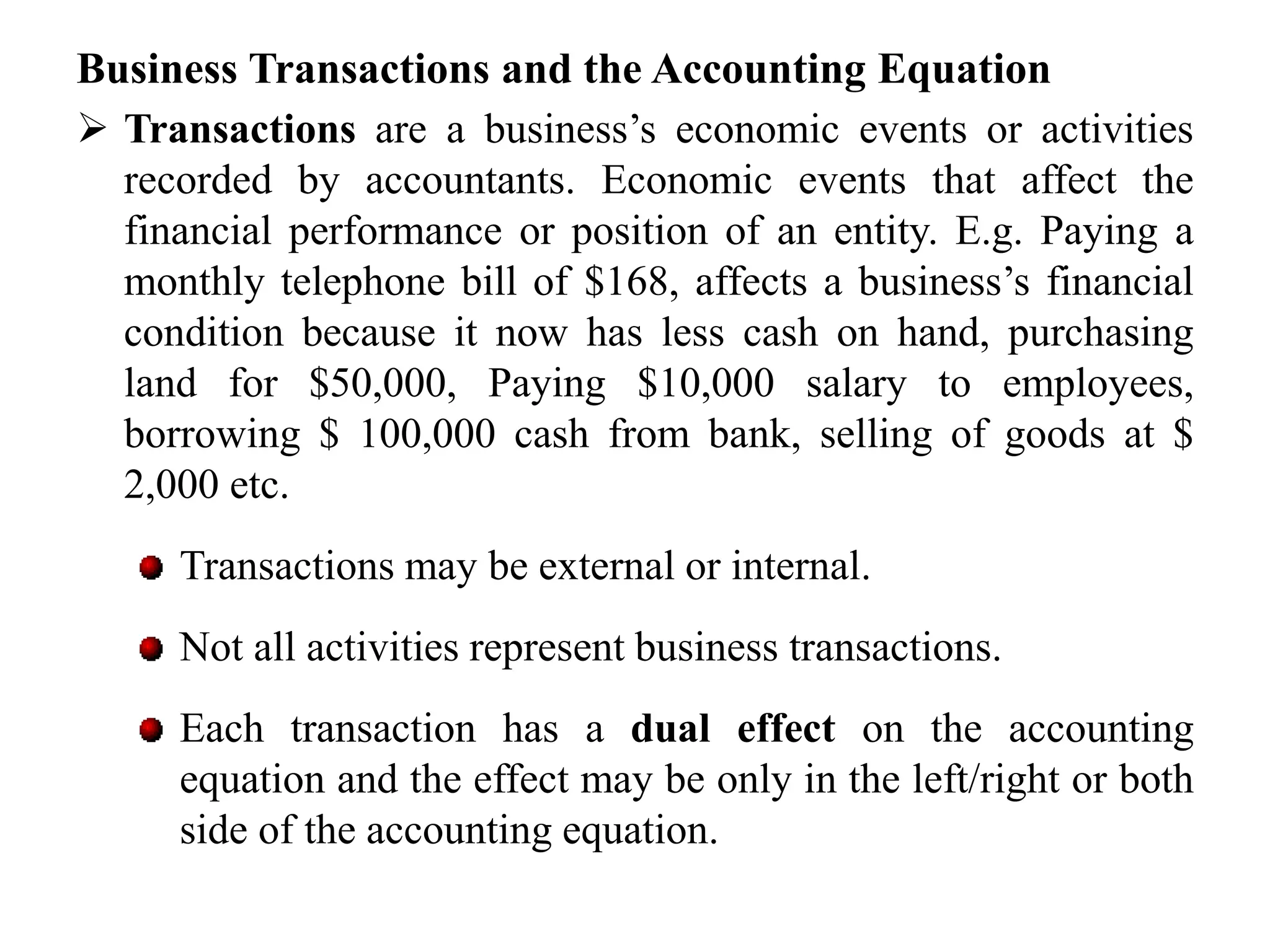

The document introduces the fundamentals of accounting, defining a business as an organization aimed at earning profit and outlining different types such as service, merchandising, and manufacturing businesses. It explains the accounting process as an information system that identifies, records, and communicates economic events to various users, both internal and external. Important concepts such as the accounting equation, types of reports, and ethical considerations within accounting practices are also discussed.

![Cont.

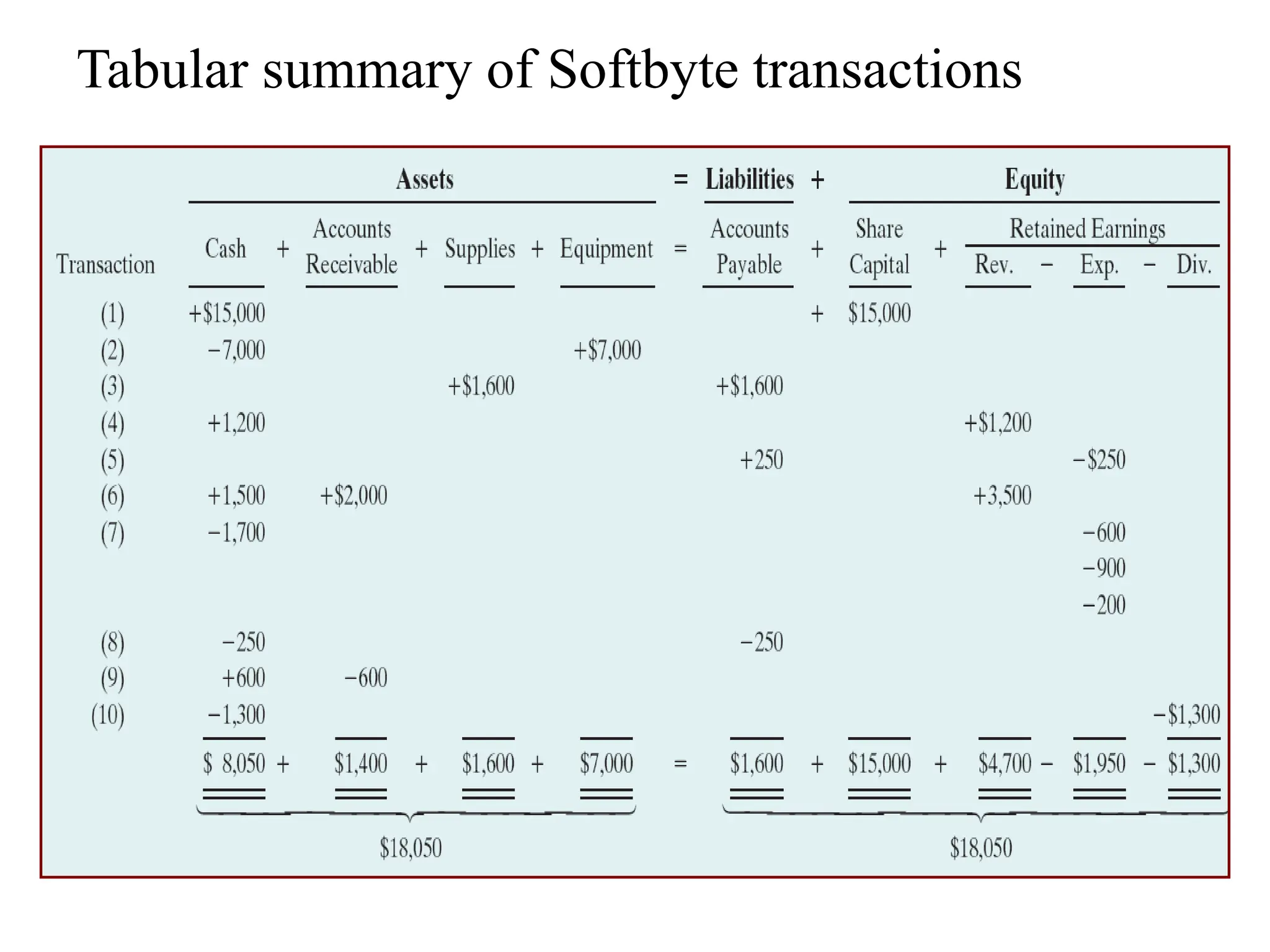

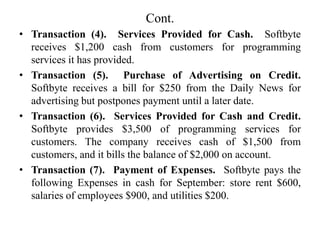

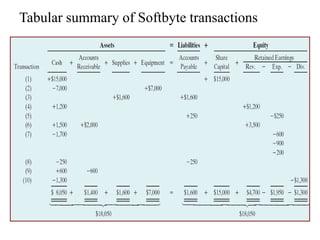

• Transaction (8). Payment of Accounts Payable. Softbyte

pays its $250 Daily News bill in cash.

• Transaction (9). Receipt of Cash on Account. Softbyte

receives $600 in cash from customers who had been billed for

services [in Transaction (6)].

• Transaction (10). Dividends. The corporation pays a

dividend of $1,300 in cash.](https://image.slidesharecdn.com/foaipptchapter-1-240512080411-3c8811c1/85/FoA-I-PPT-Chapter-1-pptx-for-undergraduate-students-42-320.jpg)

![Cont.

• Transaction (8). Payment of Accounts Payable. Softbyte

pays its $250 Daily News bill in cash.

• Transaction (9). Receipt of Cash on Account. Softbyte

receives $600 in cash from customers who had been billed for

services [in Transaction (6)].

• Transaction (10). Dividends. The corporation pays a

dividend of $1,300 in cash.](https://image.slidesharecdn.com/foaipptchapter-1-240512080411-3c8811c1/75/FoA-I-PPT-Chapter-1-pptx-for-undergraduate-students-42-2048.jpg)