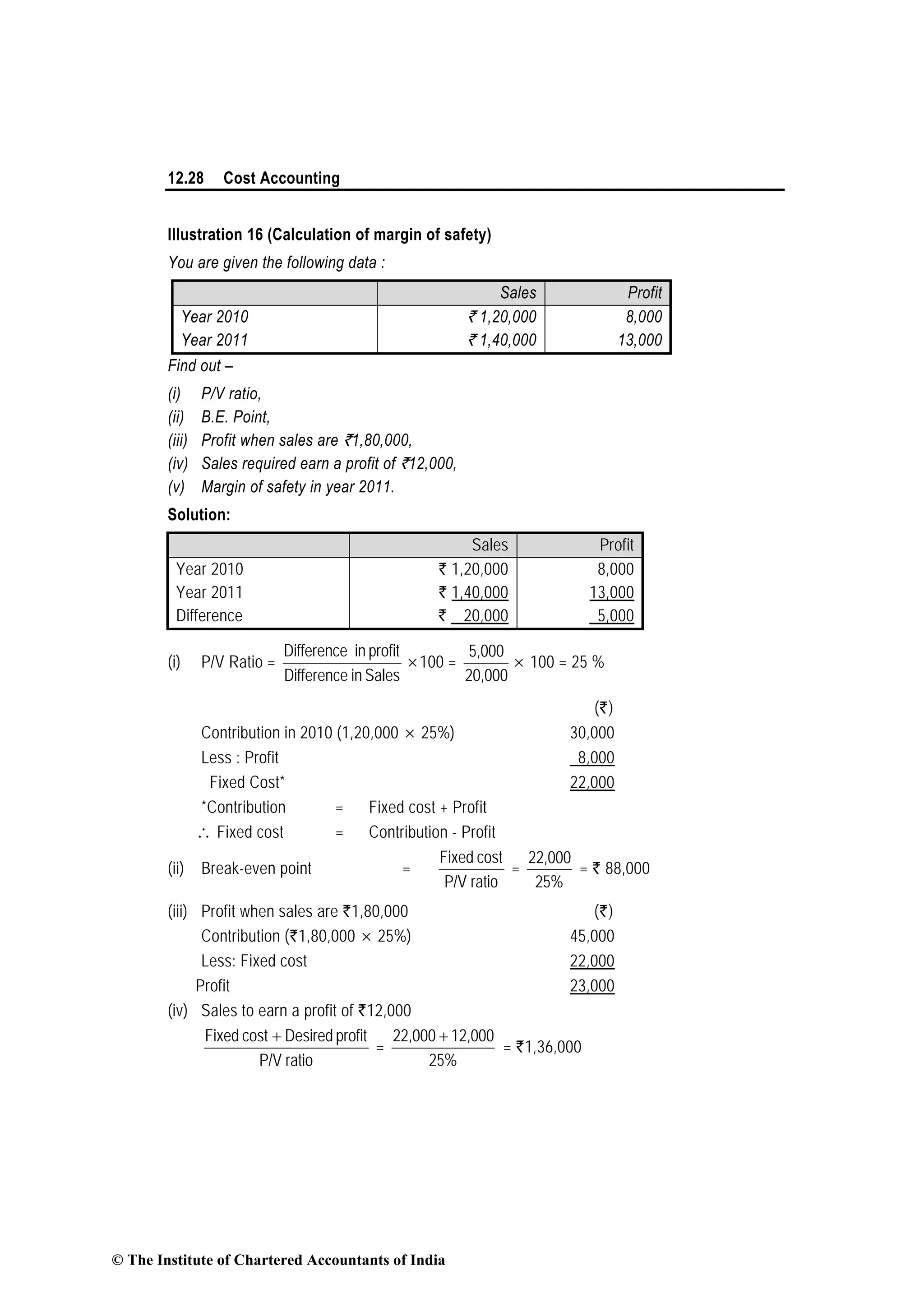

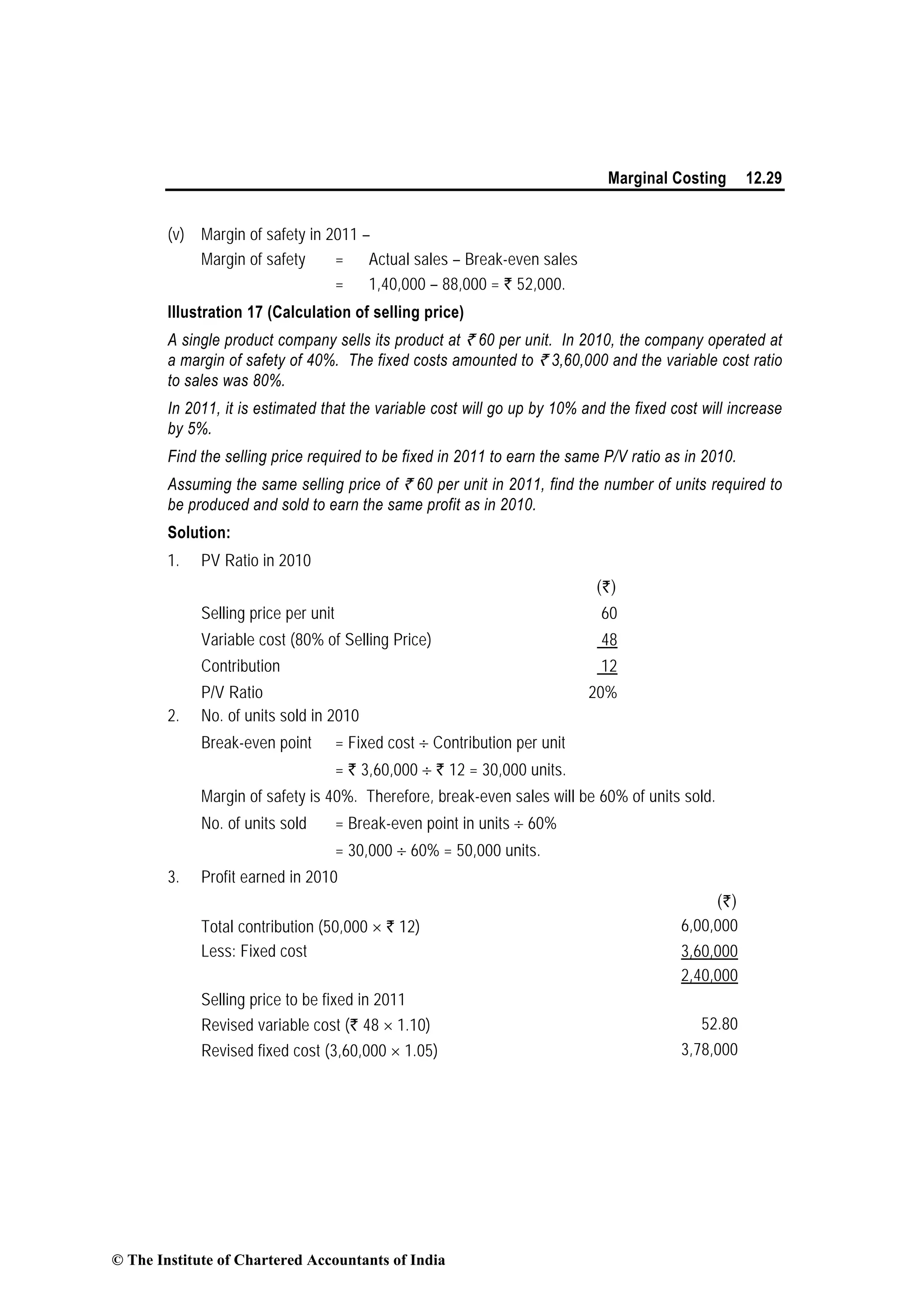

Downloaded 51 times

![12.2 Cost Accounting

change in specific elements of cost that result from any variation in operations”. It represents

an increase or decrease in total cost resulting out of:

(a) producing or distributing a few more or few less of the products;

(b) a change in the method of production or of distribution;

(c) an addition or deletion of a product or a territory; and

(d) selection of an additional sales channel.

Differential cost, thus includes fixed and semi-variable expenses. It is the difference between

the total costs of two alternatives. It is an adhoc cost determined for the purpose of choosing

between competing alternatives, each with its own combination of income and costs.

5. Incremental cost: It is defined as, “the additional costs of a change in the level or nature

of activity”. As such for all practical purposes there is no difference between incremental cost

and differential cost. However, from a conceptual point of view, differential cost refers to both

incremental as well as decremental cost. Incremental cost and differential cost calculated from

the same data will be the same. In practice, therefore, generally no distinction is made

between differential cost and incremental cost. One aspect which is worthy to note is that

incremental cost is not the same at all levels. Incremental cost between 50% and 60% level of

output may be different from that which is arrived at between 80% and 90% level of output.

Differential cost or incremental cost analysis deals with both short-term and long-term

problems. This analysis is more useful when various alternatives or various capacity levels are

being considered. (will be discussed in the next chapter i.e. Budgets and Budgetary Control)

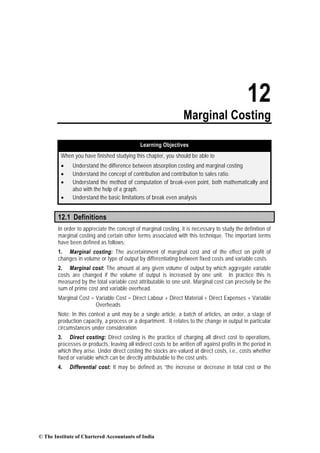

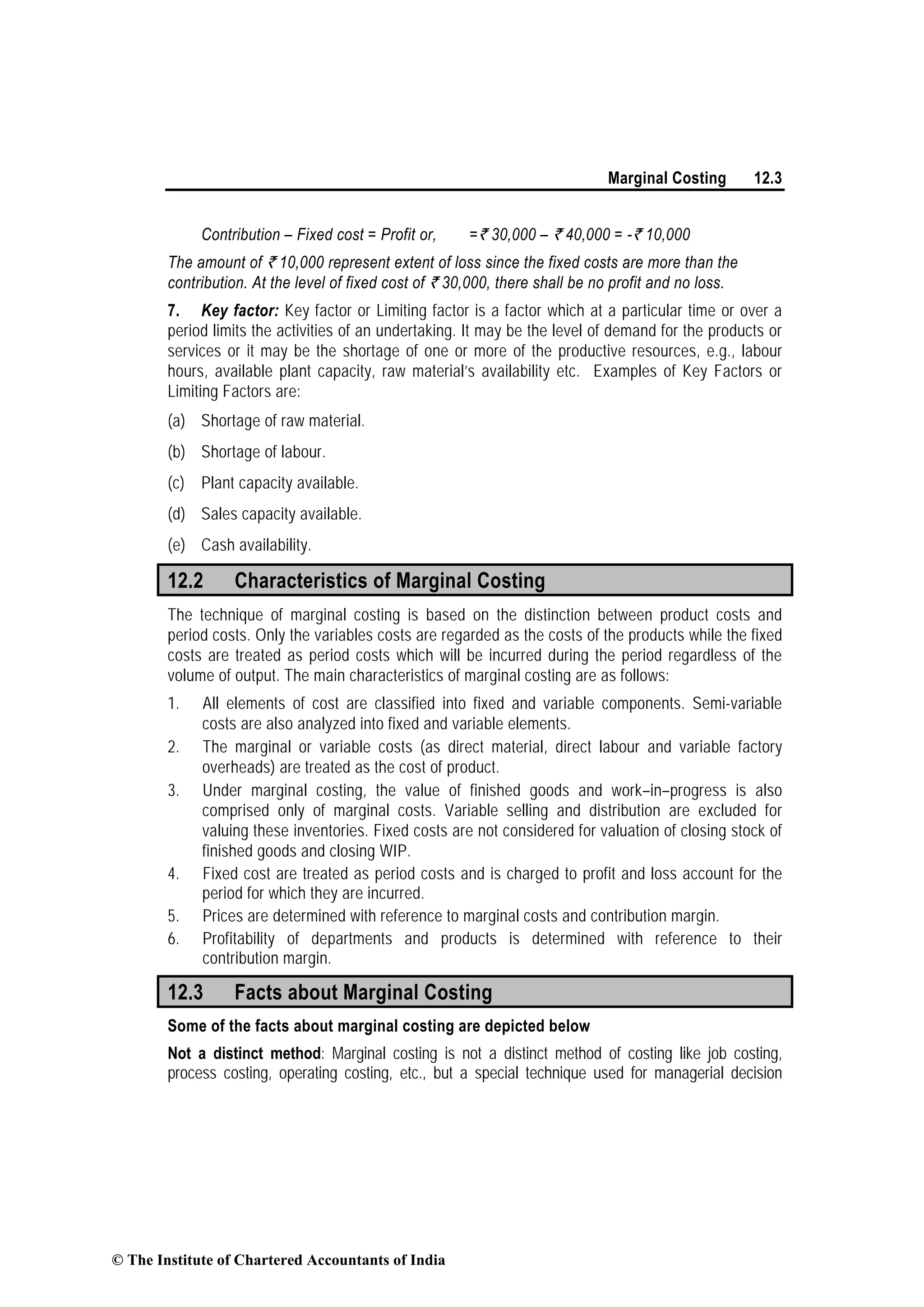

6. Contribution: Contribution or the contributory margin is the difference between sales

value and the marginal cost [Contribution (C) = Sales (S) – Variable Cost]. It is obtained by

subtracting marginal cost from sales revenue of a given activity. It can also be defined as

excess of sales revenue over the variable cost. The contribution concept is based on the

theory that the profit and fixed expenses of a business is a ‘joint cost’ which cannot be

equitably apportioned to different segments of the business. In view of this difficulty the

contribution serves as a measure of efficiency of operations of various segments of the

business. The contribution forms a fund for fixed expenses and profit as illustrated below:

Example:

Variable Cost = ` 50, 000, Fixed Cost = ` 20,000, Selling Price = ` 80,000

Contribution = Selling Price – Variable Cost

= ` 80,000 – ` 50,000 = ` 30,000

Profit = Contribution – Fixed Cost

= ` 30,000 – ` 20,000 = ` 10,000

Since, contribution exceeds fixed cost, the profit is of the magnitude of ` 10,000. Suppose the

fixed cost is ` 40,000 then the position shall be:

© The Institute of Chartered Accountants of India](https://image.slidesharecdn.com/chapter-12-marginal-costing-170602182407/85/marginal-costing-2-320.jpg)

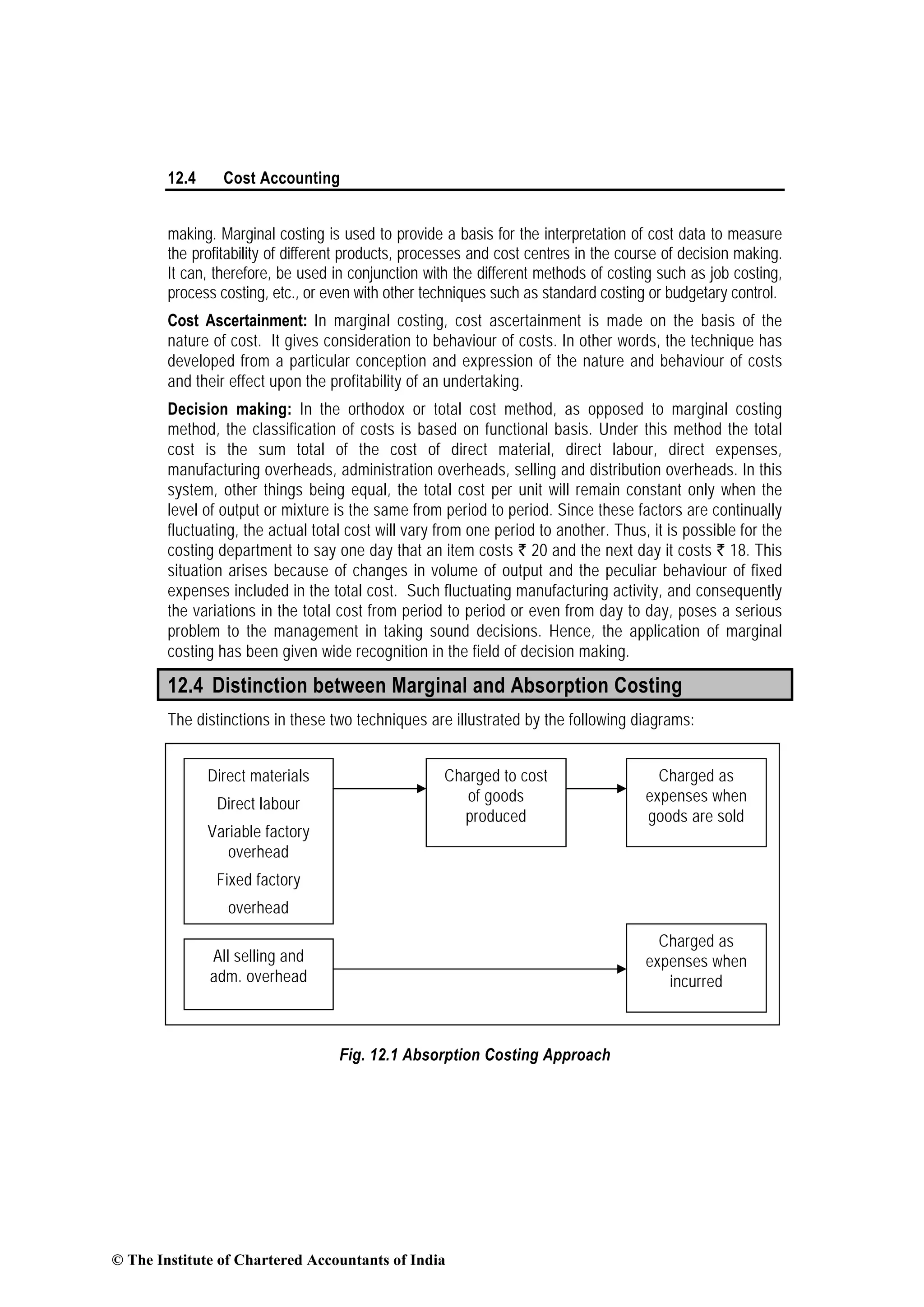

![12.30 Cost Accounting

P/V Ratio (Same as of 2010) 20%

Variable cost ratio to selling price 80%

Therefore revised selling price per unit = ` 52.80 ÷ 80% = ` 66.

No. of units to be produced and sold in 2011 to earn the same profit

We know that Fixed Cost plus profit = Contribution

(`)

Profit in 2010 2,40,000

Fixed cost in 2011 3,78,000

Desired contribution in 2011 6,18,000

Contribution per unit = Selling price per unit – Variable cost per unit.

= ` 60 – ` 52.80 = ` 7.20.

No. of units to be produced in 2012 = ` 6,18,000 ÷ ` 7.20 = 85,834 units.

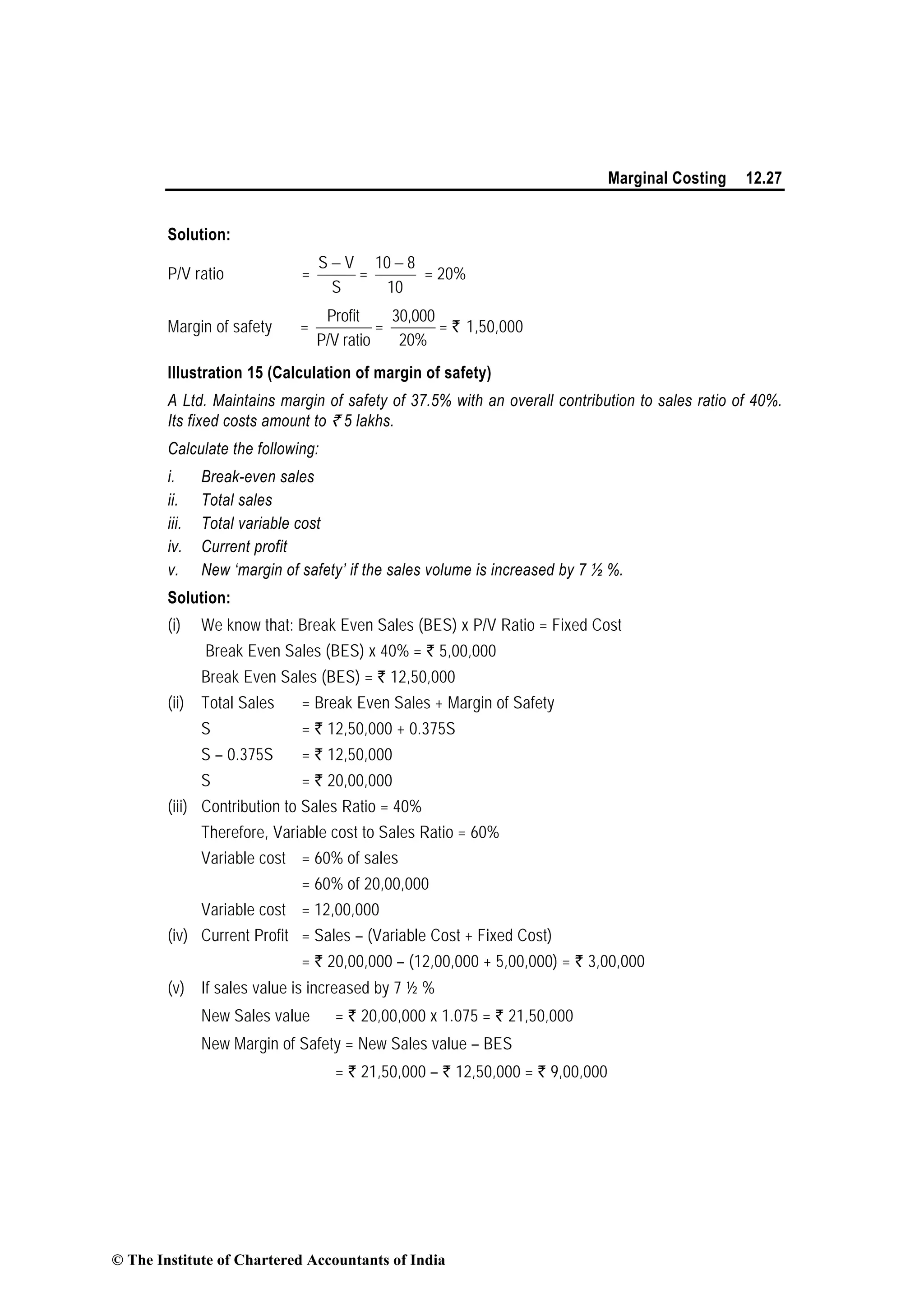

Illustration 18 (Calculation of margin of safety)

A company has made a profit of ` 50,000 during the year 2010-11. If the selling price and

marginal cost of the product are ` 15 and ` 12 per unit respectively, find out the amount of

margin of safety.

Solution:

P/V Ratio =

Contribution

Sales

x 100

= [(15 – 12)/15] x 100

= (3/15) x 100 = 20%

Marginal of Safety = (Profit)/ (P/V Ratio)

= 50,000/20% = ` 2,50,000

Illustration 19 (Calculation of break even sales)

(a) If margin of safety is ` 2,40,000 (40% of sales) and P/V ratio is 30% of AB Ltd, calculate

its (1) Break even sales, and (2) Amount of profit on sales of `9,00,000.

(b) X Ltd. has earned a contribution of `2,00,000 and net profit of `1,50,000 of sales of

` 8,00,000. What is its margin of safety?

Solution:

(a) Total Sales = 2,40,000 ×

100

40

= `6,00,000

Contribution = 6,00,000 × 30% = `1,80,000

Profit = M/S × P/V ratio = 2,40,000 × 30% = `72,000

© The Institute of Chartered Accountants of India](https://image.slidesharecdn.com/chapter-12-marginal-costing-170602182407/85/marginal-costing-30-320.jpg)

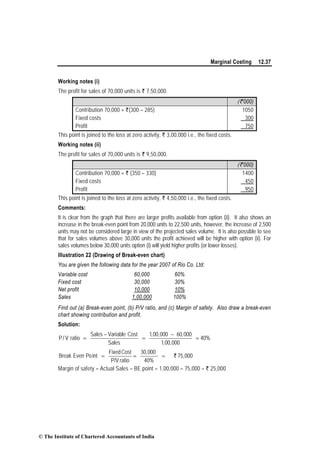

![12.2 Cost Accounting

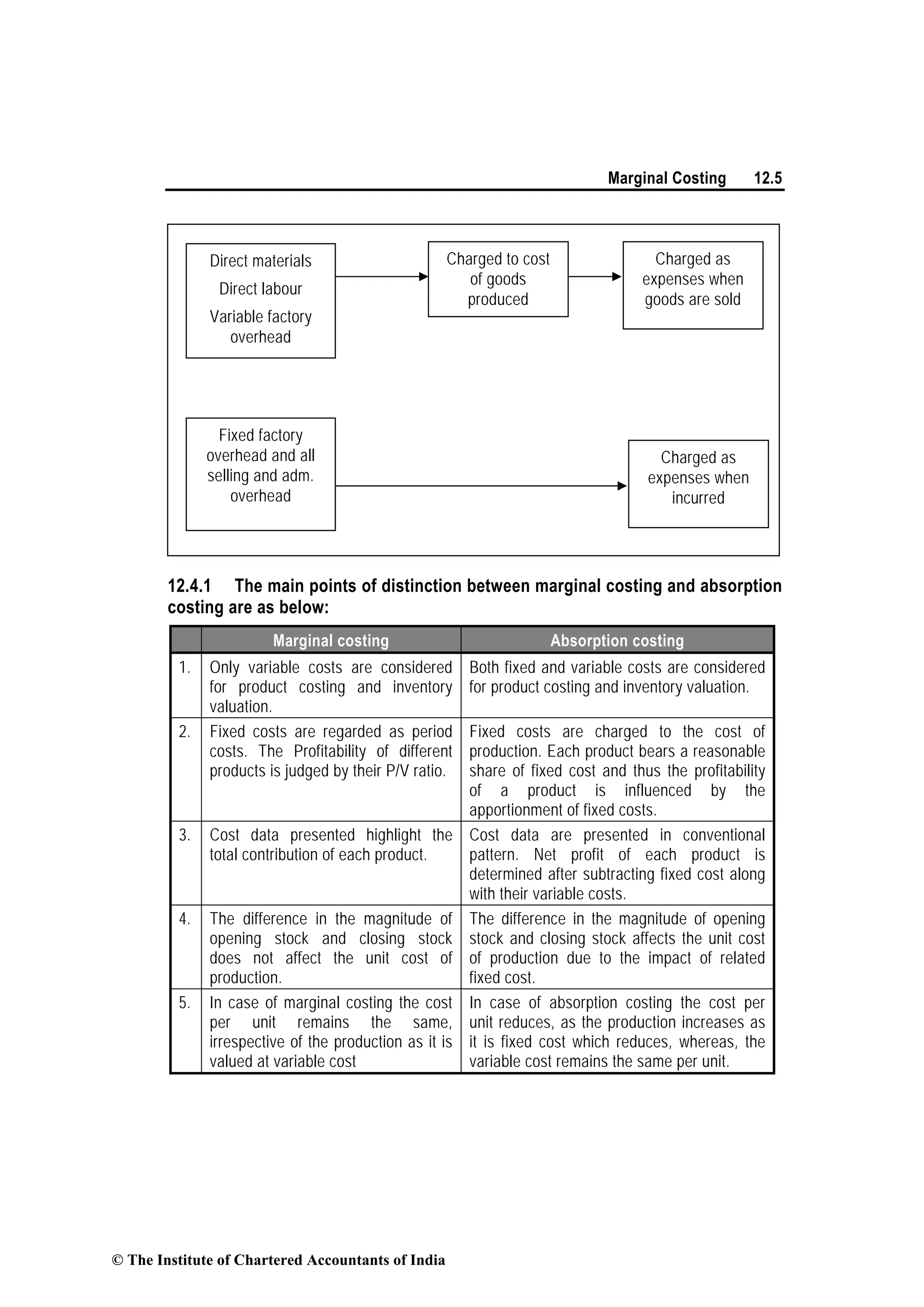

change in specific elements of cost that result from any variation in operations”. It represents

an increase or decrease in total cost resulting out of:

(a) producing or distributing a few more or few less of the products;

(b) a change in the method of production or of distribution;

(c) an addition or deletion of a product or a territory; and

(d) selection of an additional sales channel.

Differential cost, thus includes fixed and semi-variable expenses. It is the difference between

the total costs of two alternatives. It is an adhoc cost determined for the purpose of choosing

between competing alternatives, each with its own combination of income and costs.

5. Incremental cost: It is defined as, “the additional costs of a change in the level or nature

of activity”. As such for all practical purposes there is no difference between incremental cost

and differential cost. However, from a conceptual point of view, differential cost refers to both

incremental as well as decremental cost. Incremental cost and differential cost calculated from

the same data will be the same. In practice, therefore, generally no distinction is made

between differential cost and incremental cost. One aspect which is worthy to note is that

incremental cost is not the same at all levels. Incremental cost between 50% and 60% level of

output may be different from that which is arrived at between 80% and 90% level of output.

Differential cost or incremental cost analysis deals with both short-term and long-term

problems. This analysis is more useful when various alternatives or various capacity levels are

being considered. (will be discussed in the next chapter i.e. Budgets and Budgetary Control)

6. Contribution: Contribution or the contributory margin is the difference between sales

value and the marginal cost [Contribution (C) = Sales (S) – Variable Cost]. It is obtained by

subtracting marginal cost from sales revenue of a given activity. It can also be defined as

excess of sales revenue over the variable cost. The contribution concept is based on the

theory that the profit and fixed expenses of a business is a ‘joint cost’ which cannot be

equitably apportioned to different segments of the business. In view of this difficulty the

contribution serves as a measure of efficiency of operations of various segments of the

business. The contribution forms a fund for fixed expenses and profit as illustrated below:

Example:

Variable Cost = ` 50, 000, Fixed Cost = ` 20,000, Selling Price = ` 80,000

Contribution = Selling Price – Variable Cost

= ` 80,000 – ` 50,000 = ` 30,000

Profit = Contribution – Fixed Cost

= ` 30,000 – ` 20,000 = ` 10,000

Since, contribution exceeds fixed cost, the profit is of the magnitude of ` 10,000. Suppose the

fixed cost is ` 40,000 then the position shall be:

© The Institute of Chartered Accountants of India](https://image.slidesharecdn.com/chapter-12-marginal-costing-170602182407/75/marginal-costing-2-2048.jpg)

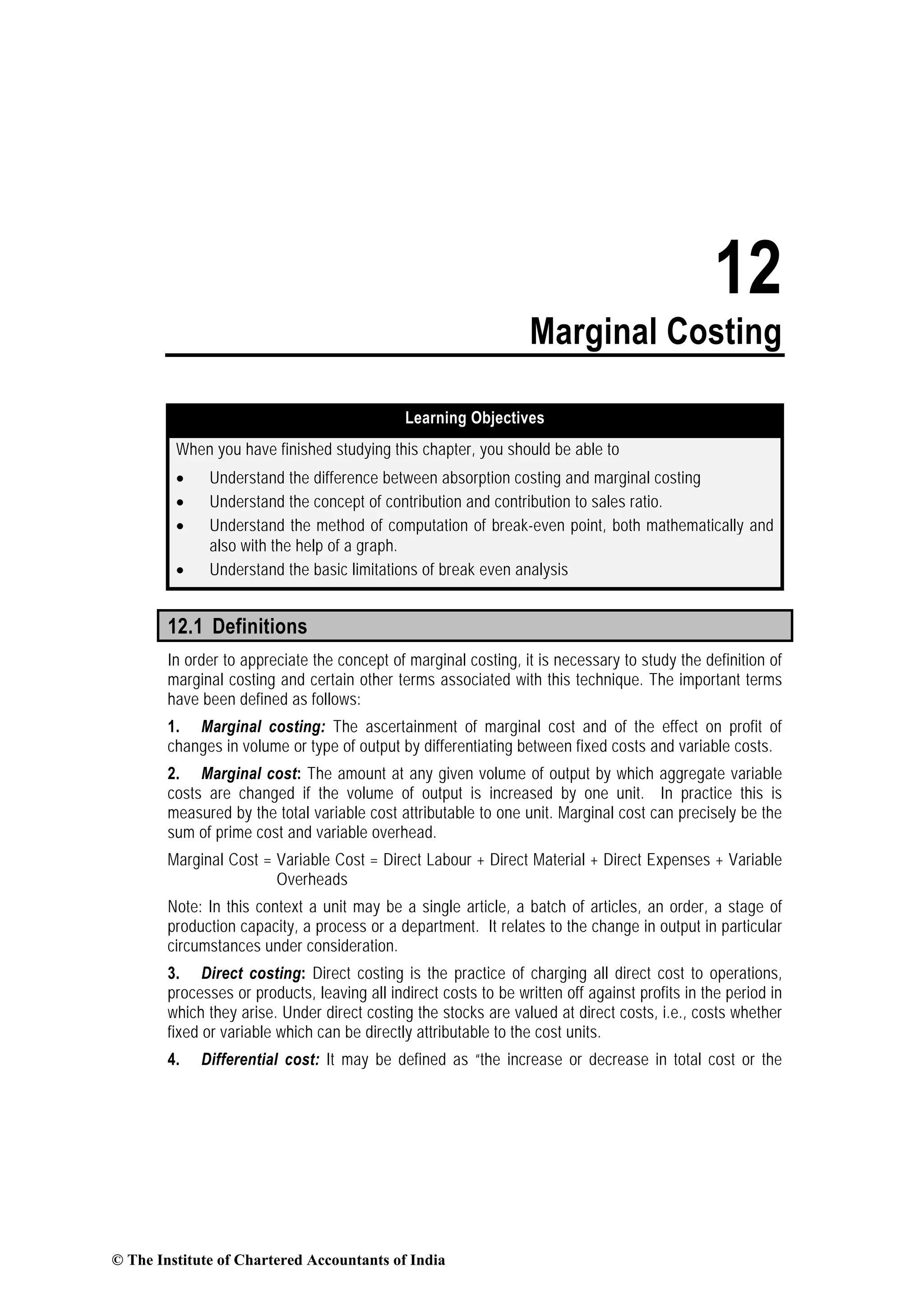

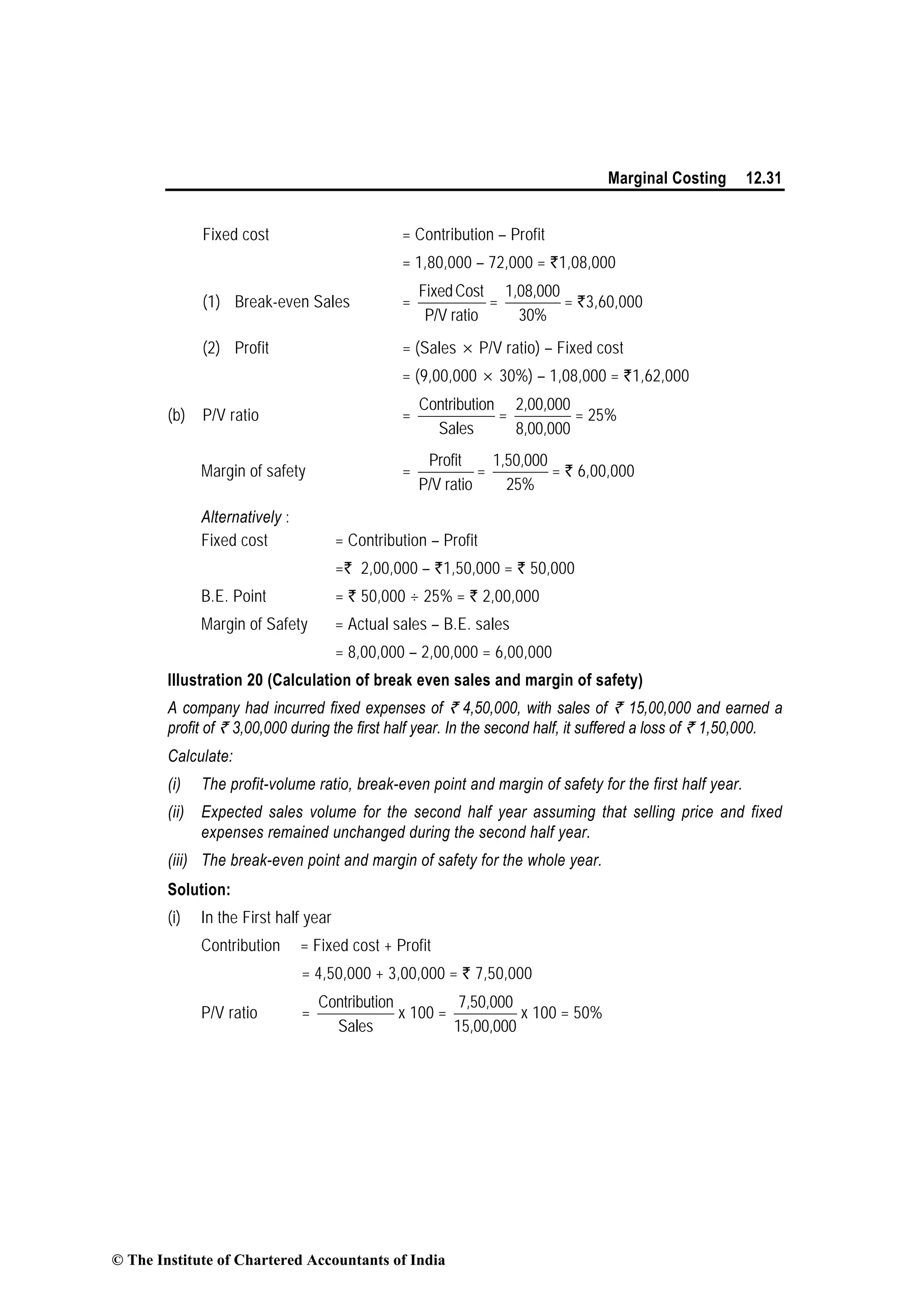

![12.30 Cost Accounting

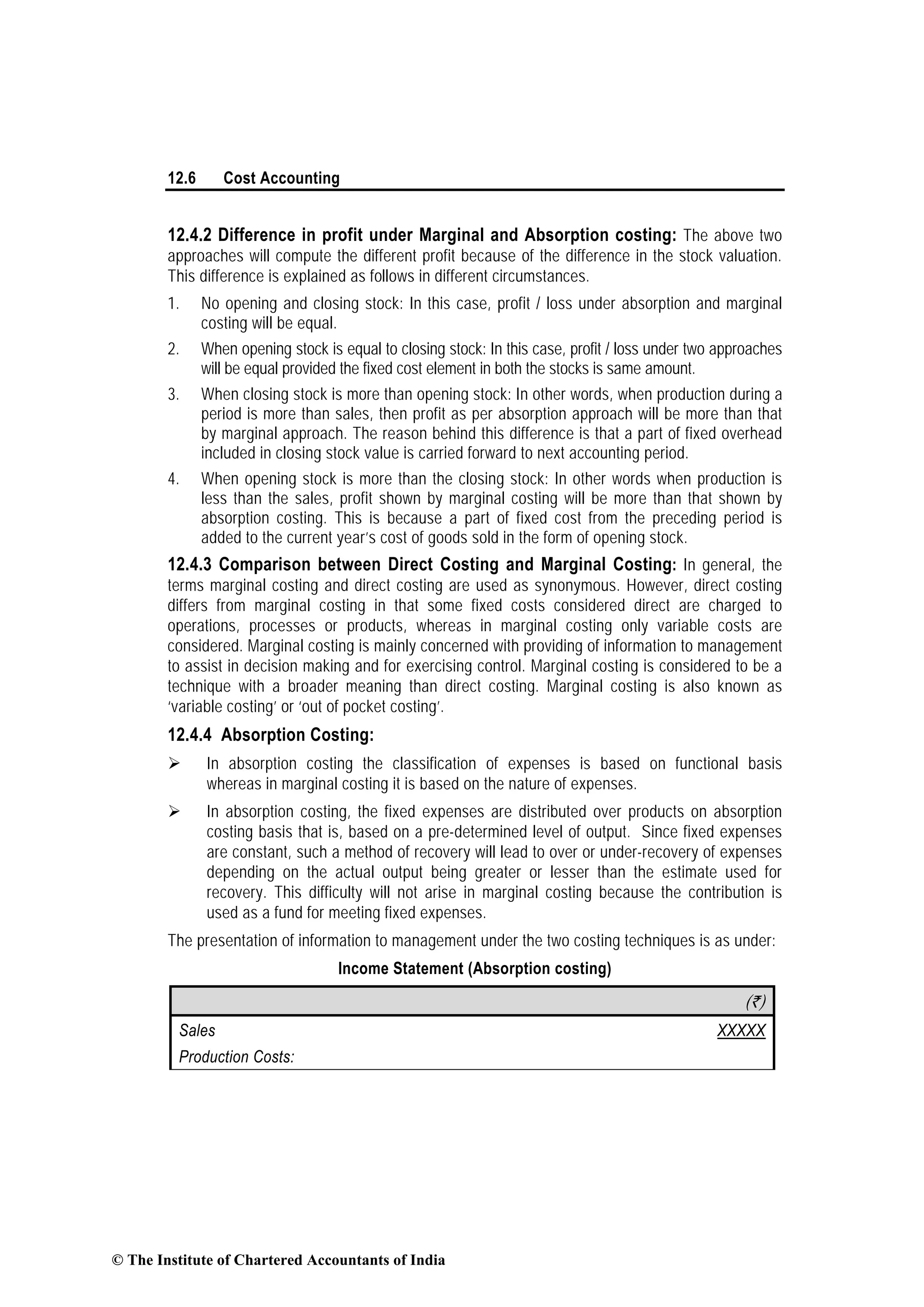

P/V Ratio (Same as of 2010) 20%

Variable cost ratio to selling price 80%

Therefore revised selling price per unit = ` 52.80 ÷ 80% = ` 66.

No. of units to be produced and sold in 2011 to earn the same profit

We know that Fixed Cost plus profit = Contribution

(`)

Profit in 2010 2,40,000

Fixed cost in 2011 3,78,000

Desired contribution in 2011 6,18,000

Contribution per unit = Selling price per unit – Variable cost per unit.

= ` 60 – ` 52.80 = ` 7.20.

No. of units to be produced in 2012 = ` 6,18,000 ÷ ` 7.20 = 85,834 units.

Illustration 18 (Calculation of margin of safety)

A company has made a profit of ` 50,000 during the year 2010-11. If the selling price and

marginal cost of the product are ` 15 and ` 12 per unit respectively, find out the amount of

margin of safety.

Solution:

P/V Ratio =

Contribution

Sales

x 100

= [(15 – 12)/15] x 100

= (3/15) x 100 = 20%

Marginal of Safety = (Profit)/ (P/V Ratio)

= 50,000/20% = ` 2,50,000

Illustration 19 (Calculation of break even sales)

(a) If margin of safety is ` 2,40,000 (40% of sales) and P/V ratio is 30% of AB Ltd, calculate

its (1) Break even sales, and (2) Amount of profit on sales of `9,00,000.

(b) X Ltd. has earned a contribution of `2,00,000 and net profit of `1,50,000 of sales of

` 8,00,000. What is its margin of safety?

Solution:

(a) Total Sales = 2,40,000 ×

100

40

= `6,00,000

Contribution = 6,00,000 × 30% = `1,80,000

Profit = M/S × P/V ratio = 2,40,000 × 30% = `72,000

© The Institute of Chartered Accountants of India](https://image.slidesharecdn.com/chapter-12-marginal-costing-170602182407/75/marginal-costing-30-2048.jpg)

Marginal costing is a technique that differentiates between fixed and variable costs. It treats variable costs as product costs and fixed costs as period costs. Under marginal costing, only variable costs are considered in inventory valuation. Absorption costing treats both fixed and variable costs as product costs and includes a share of fixed costs in inventory valuation. The chapter provides definitions and concepts related to marginal costing, characteristics that distinguish it from absorption costing, and how profit is calculated differently under each method.