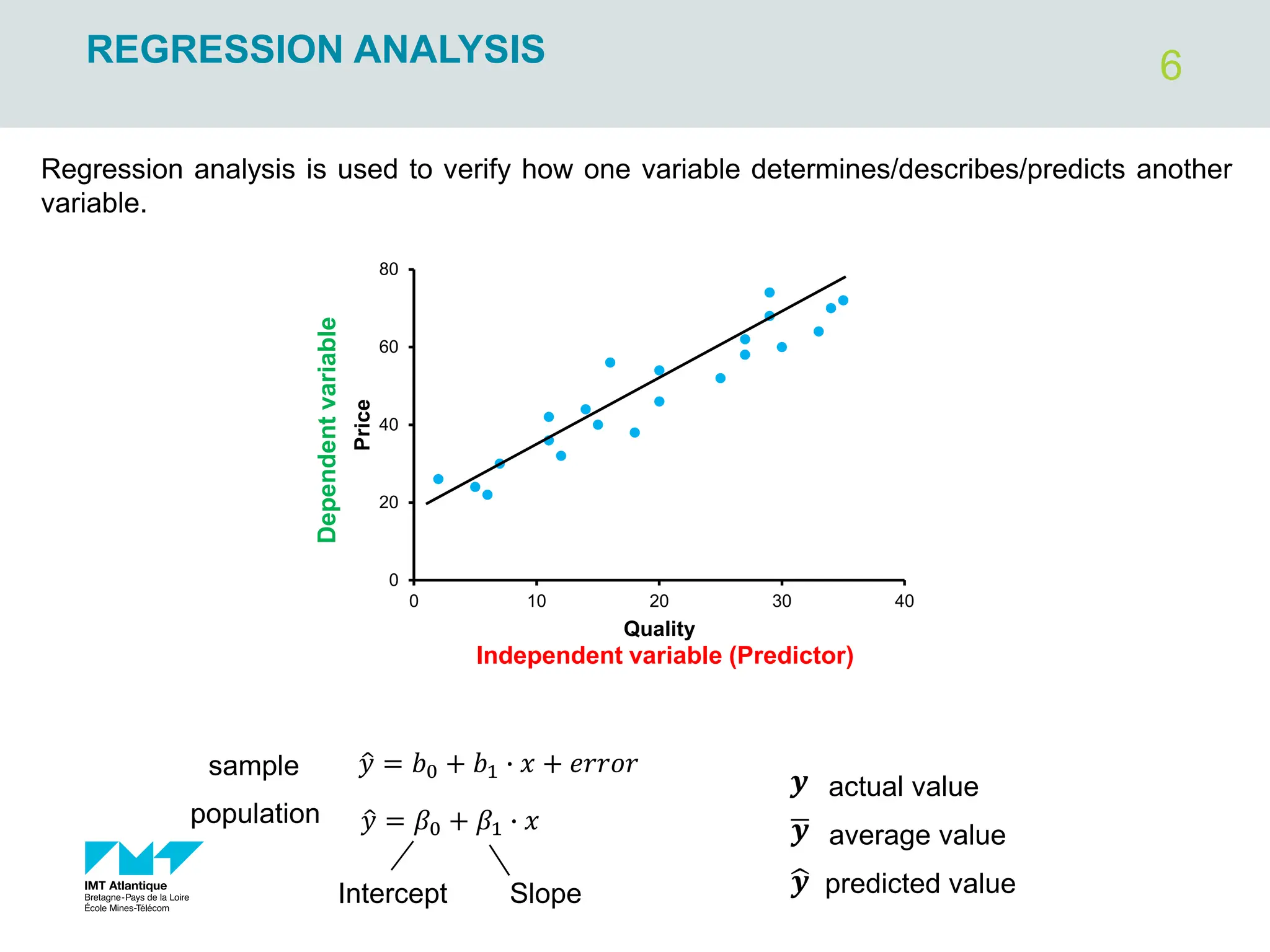

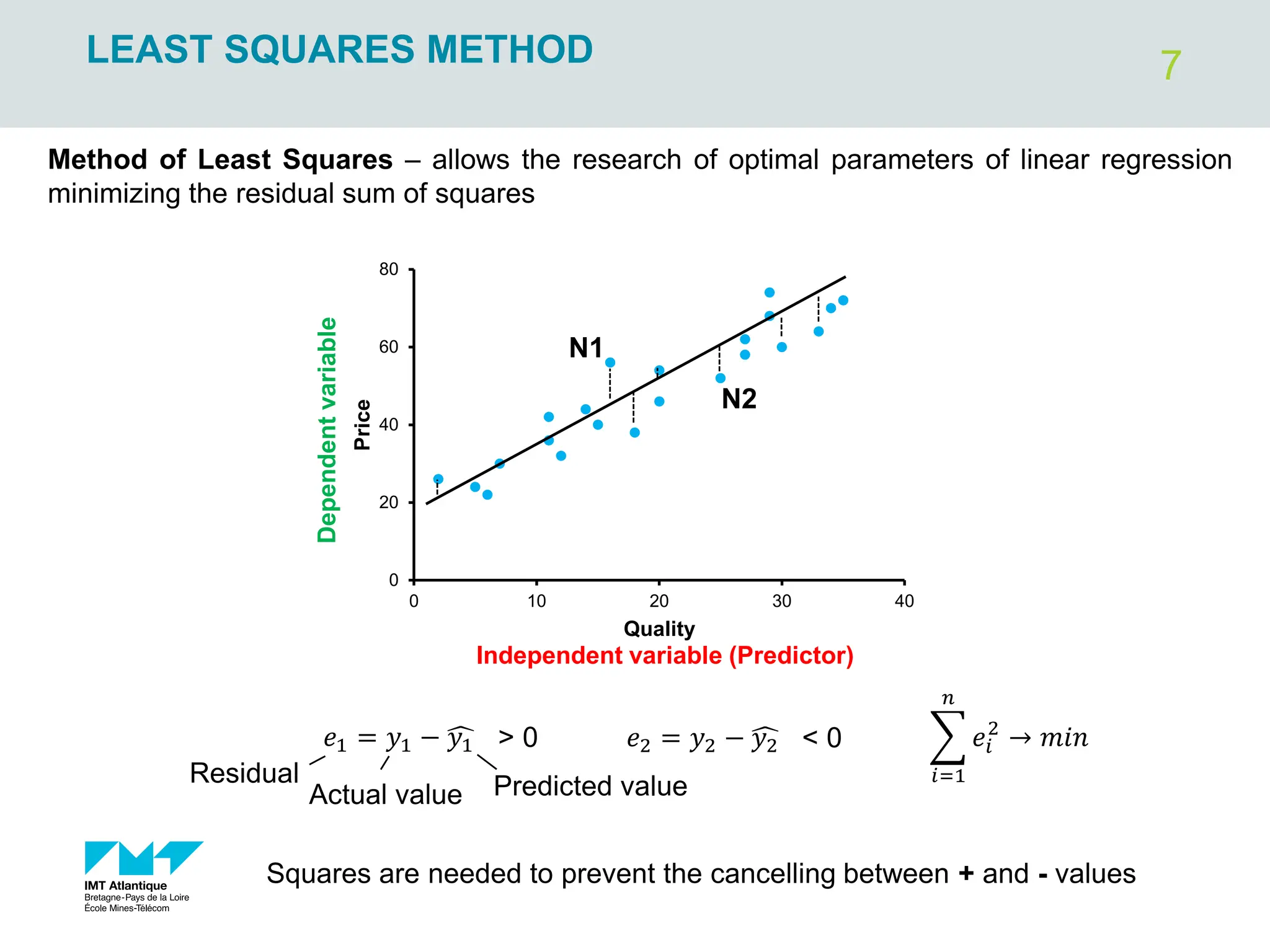

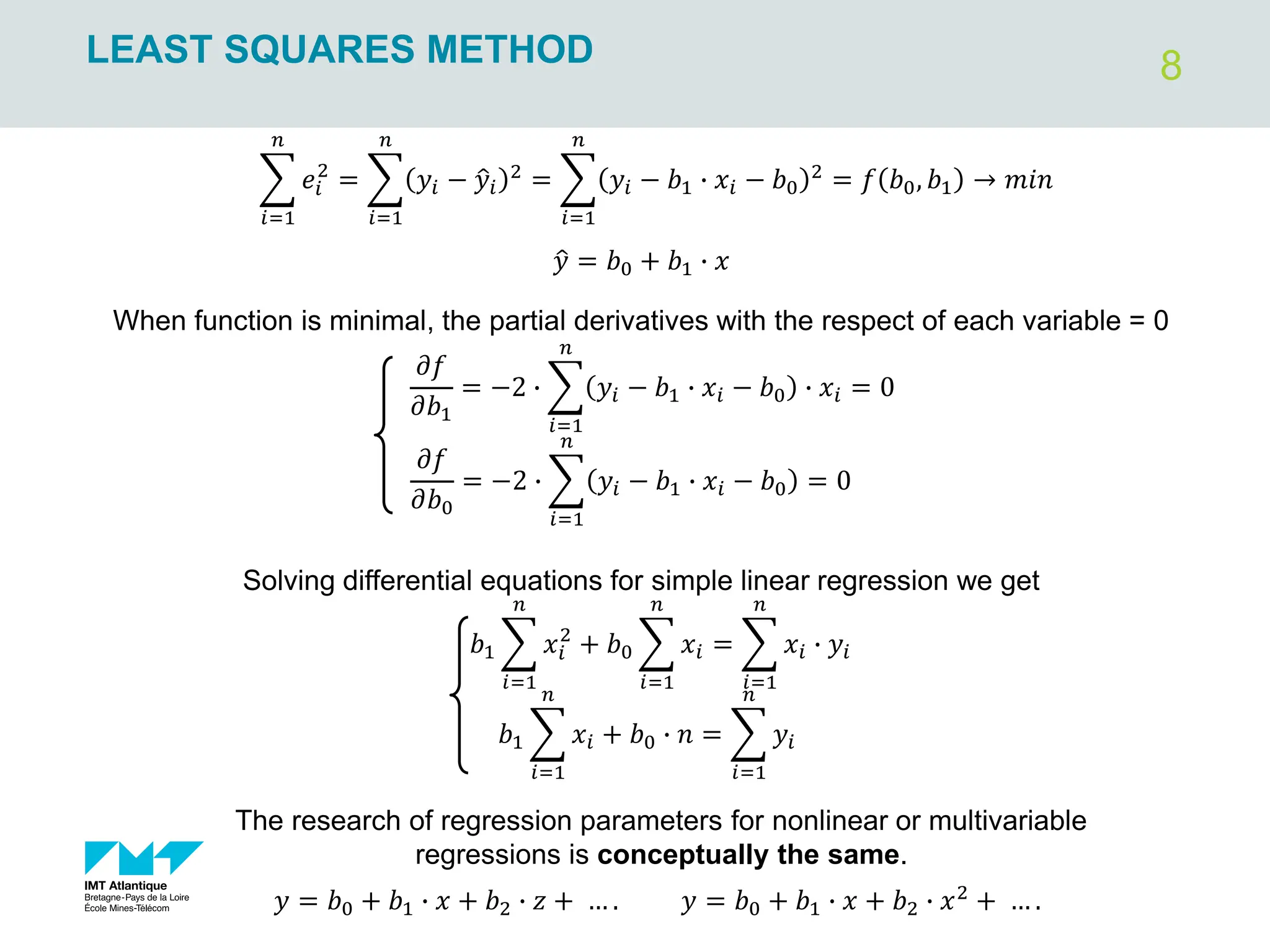

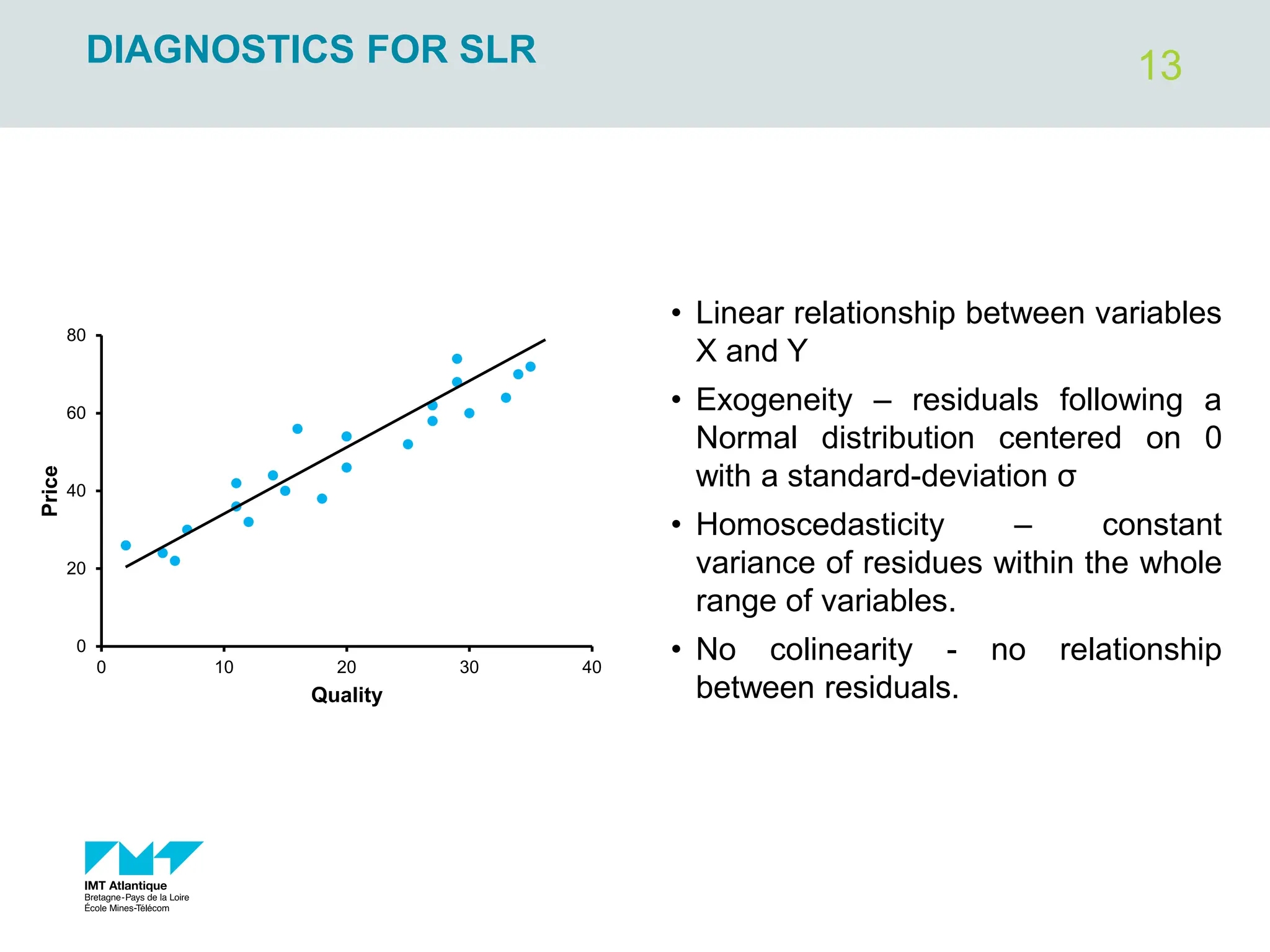

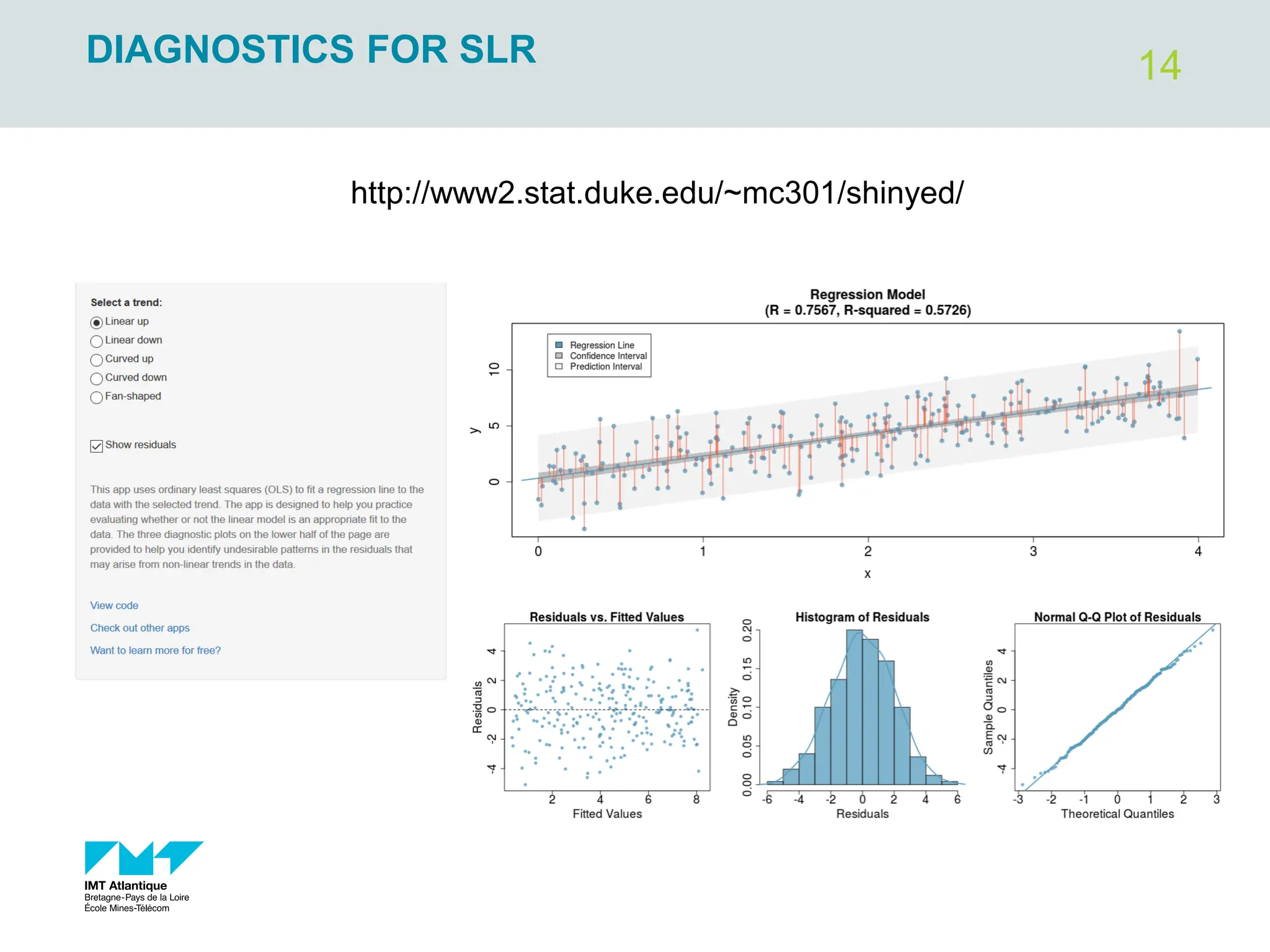

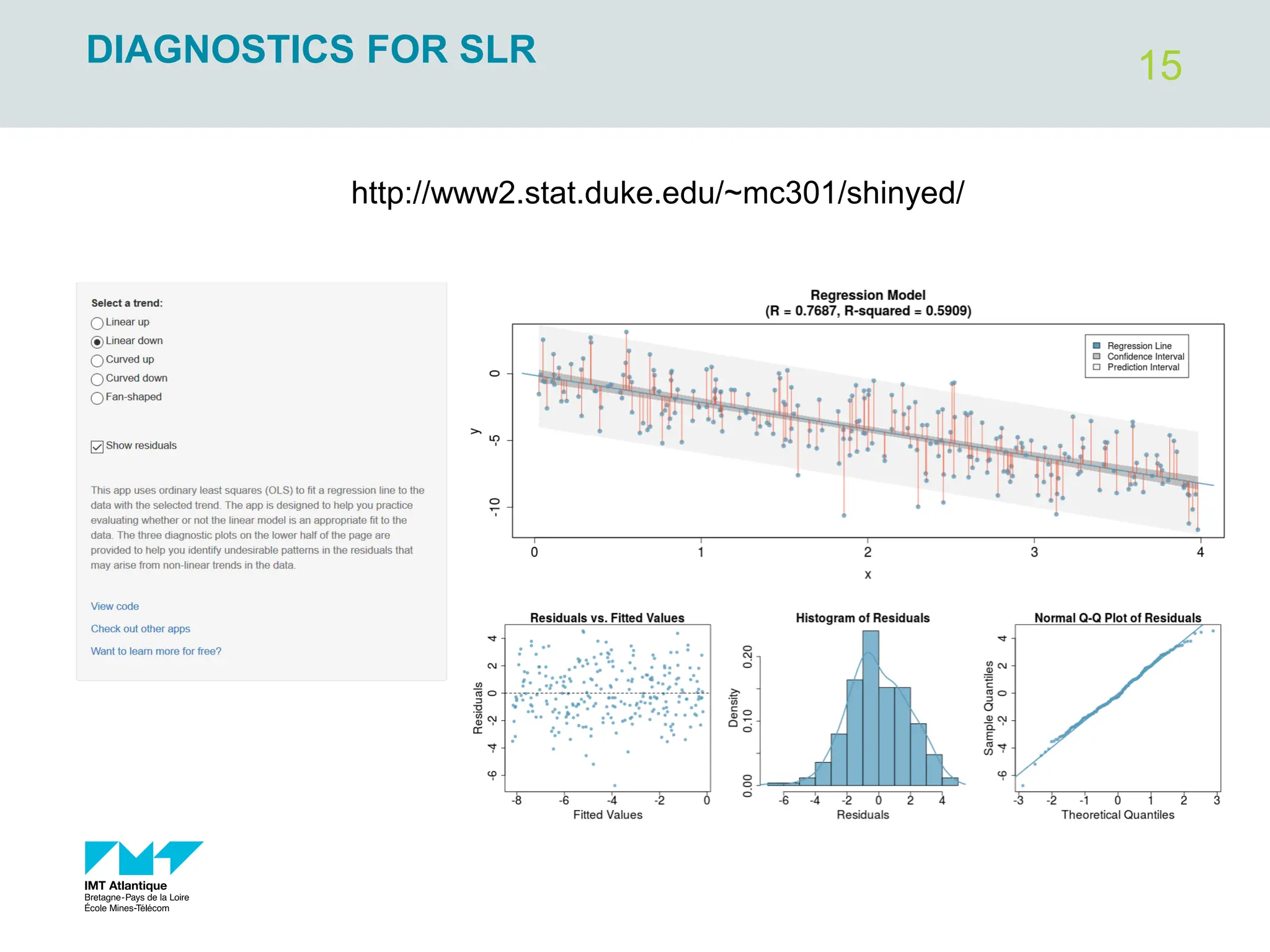

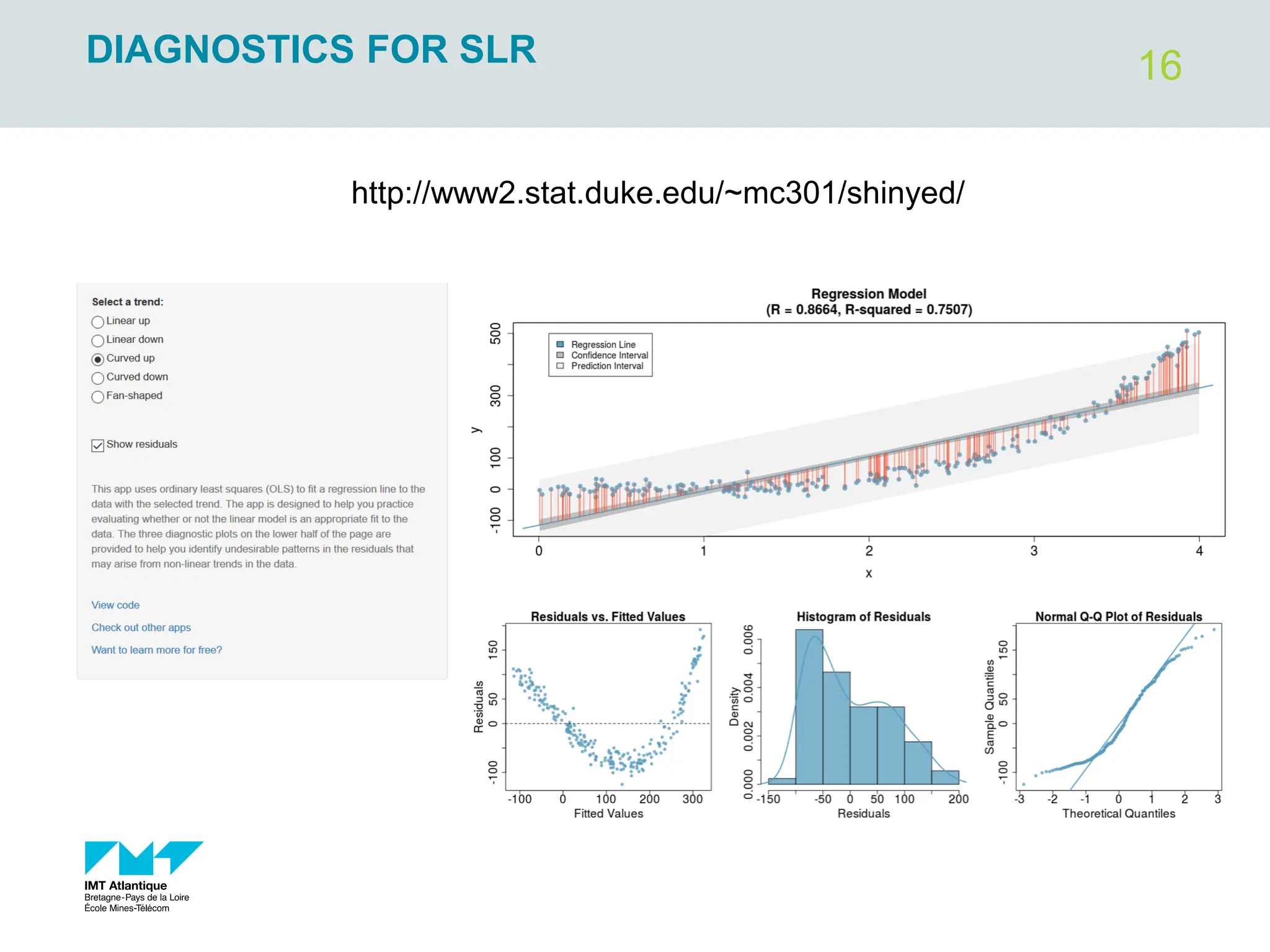

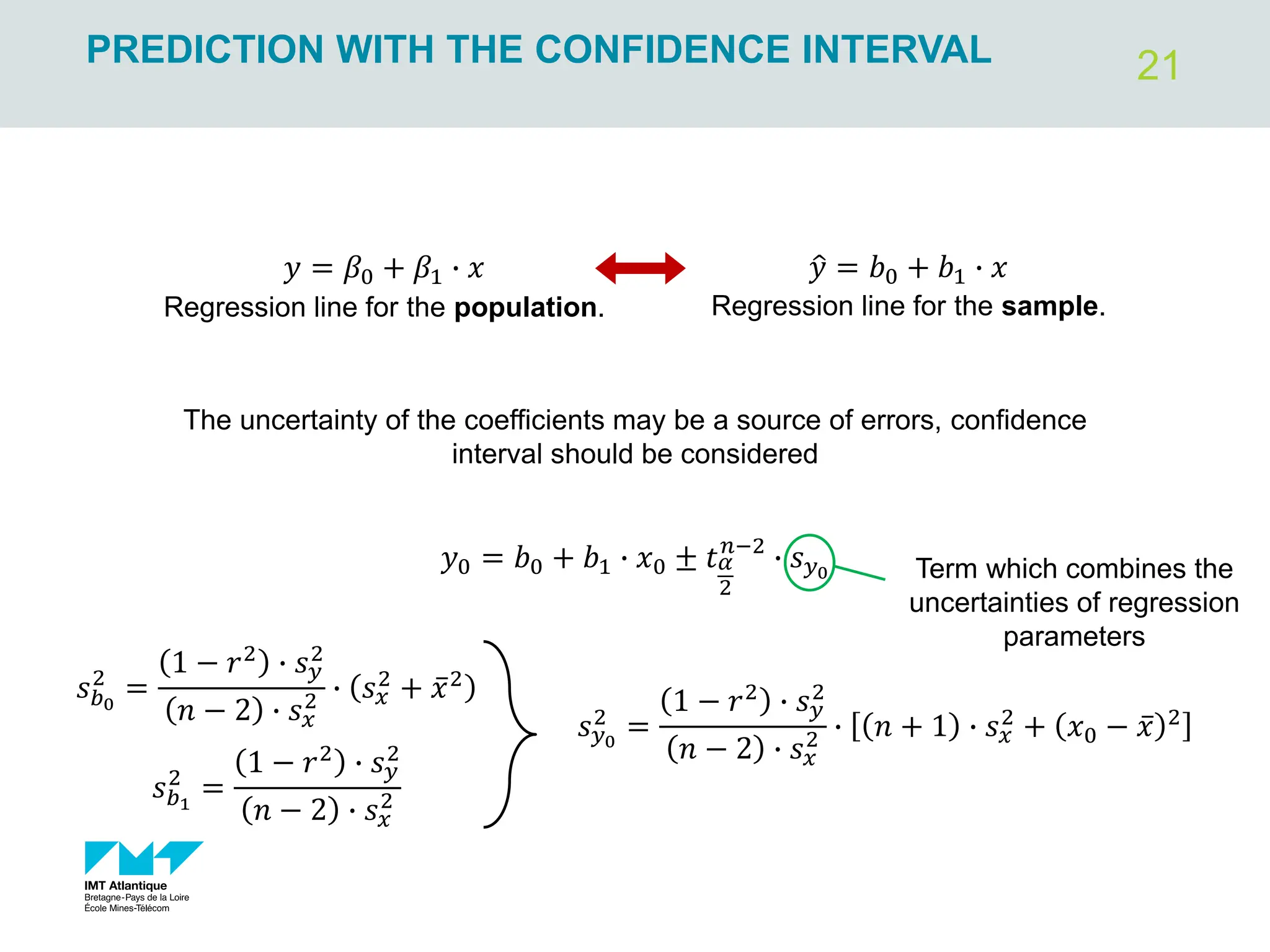

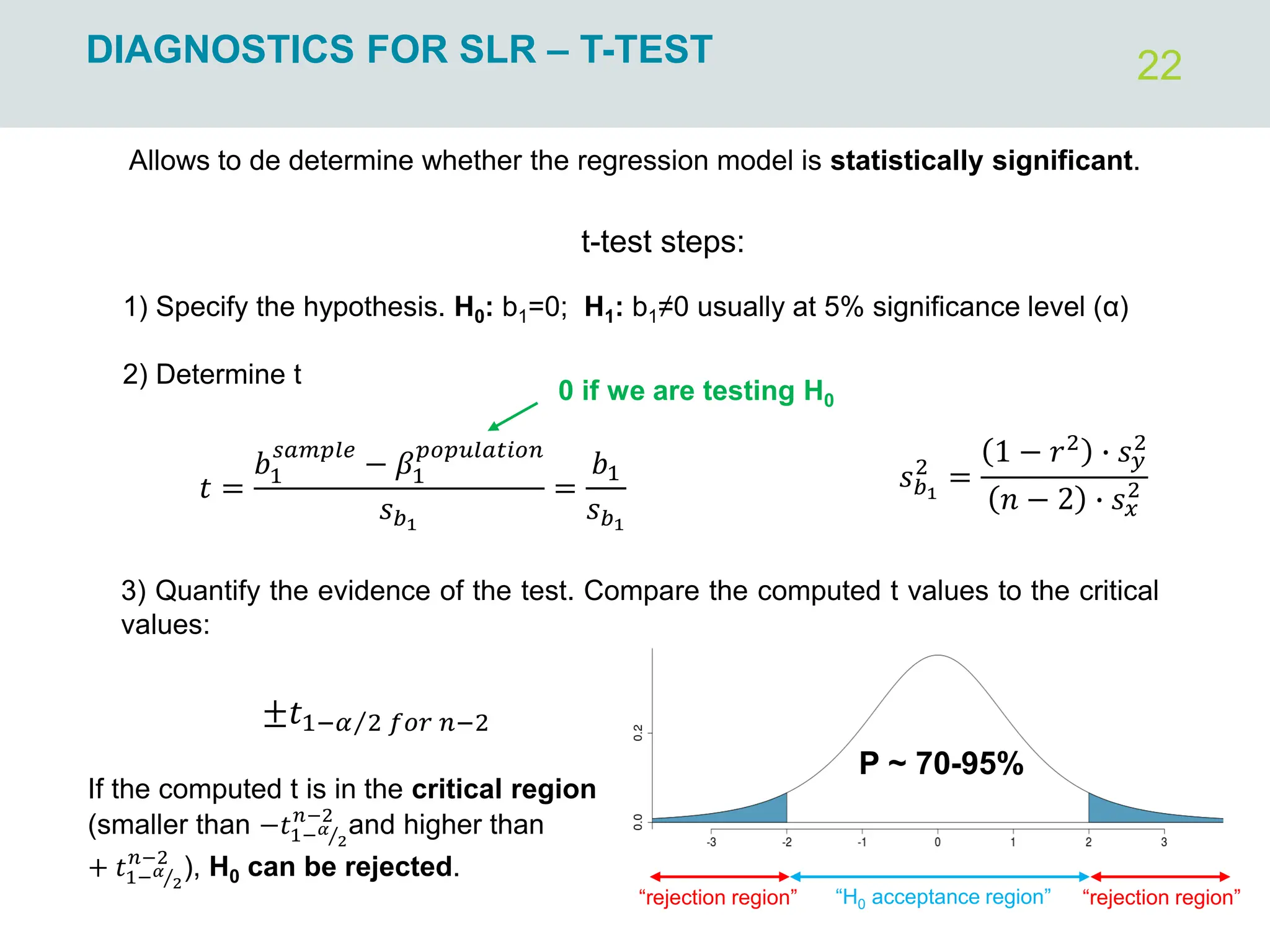

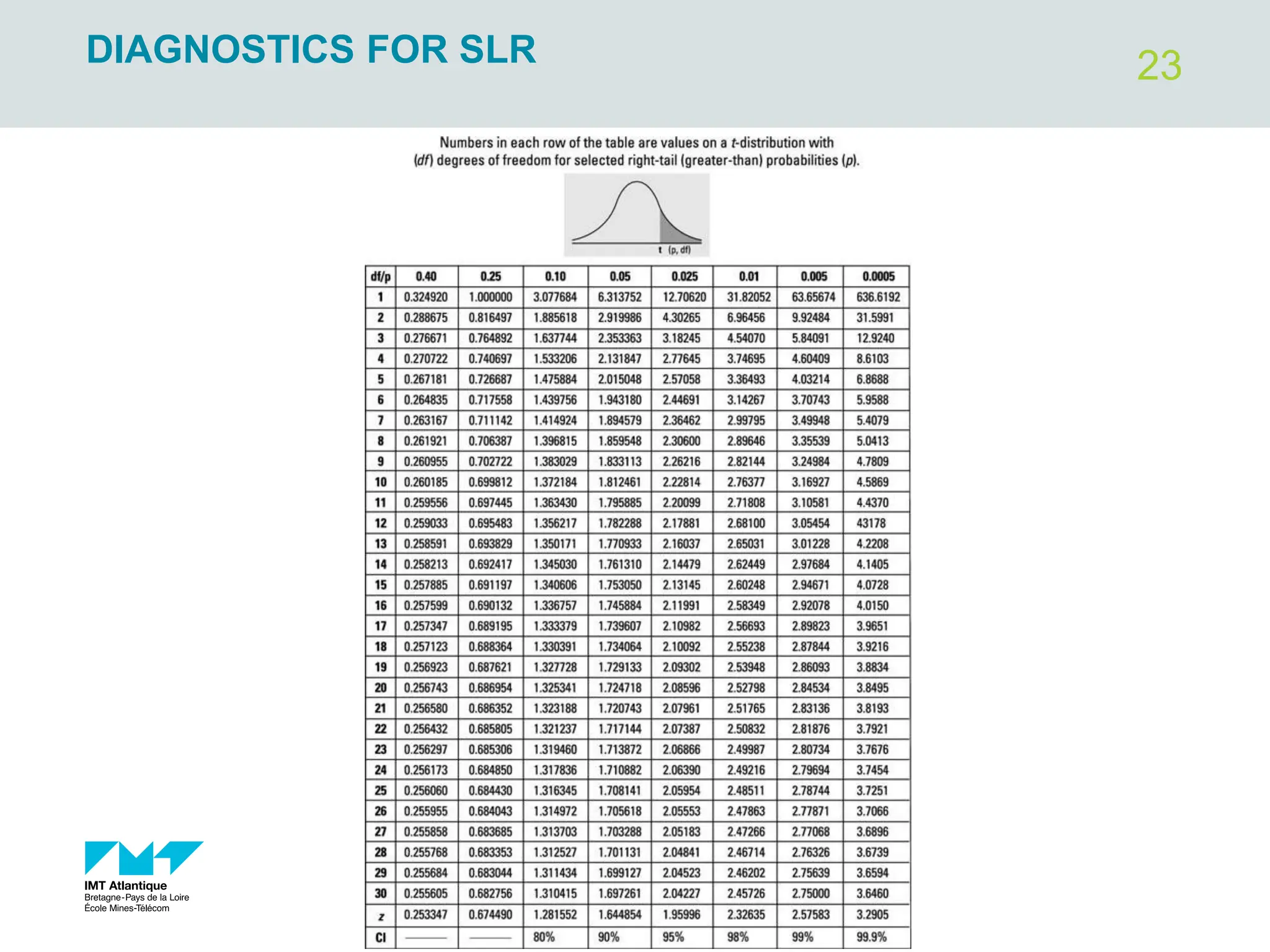

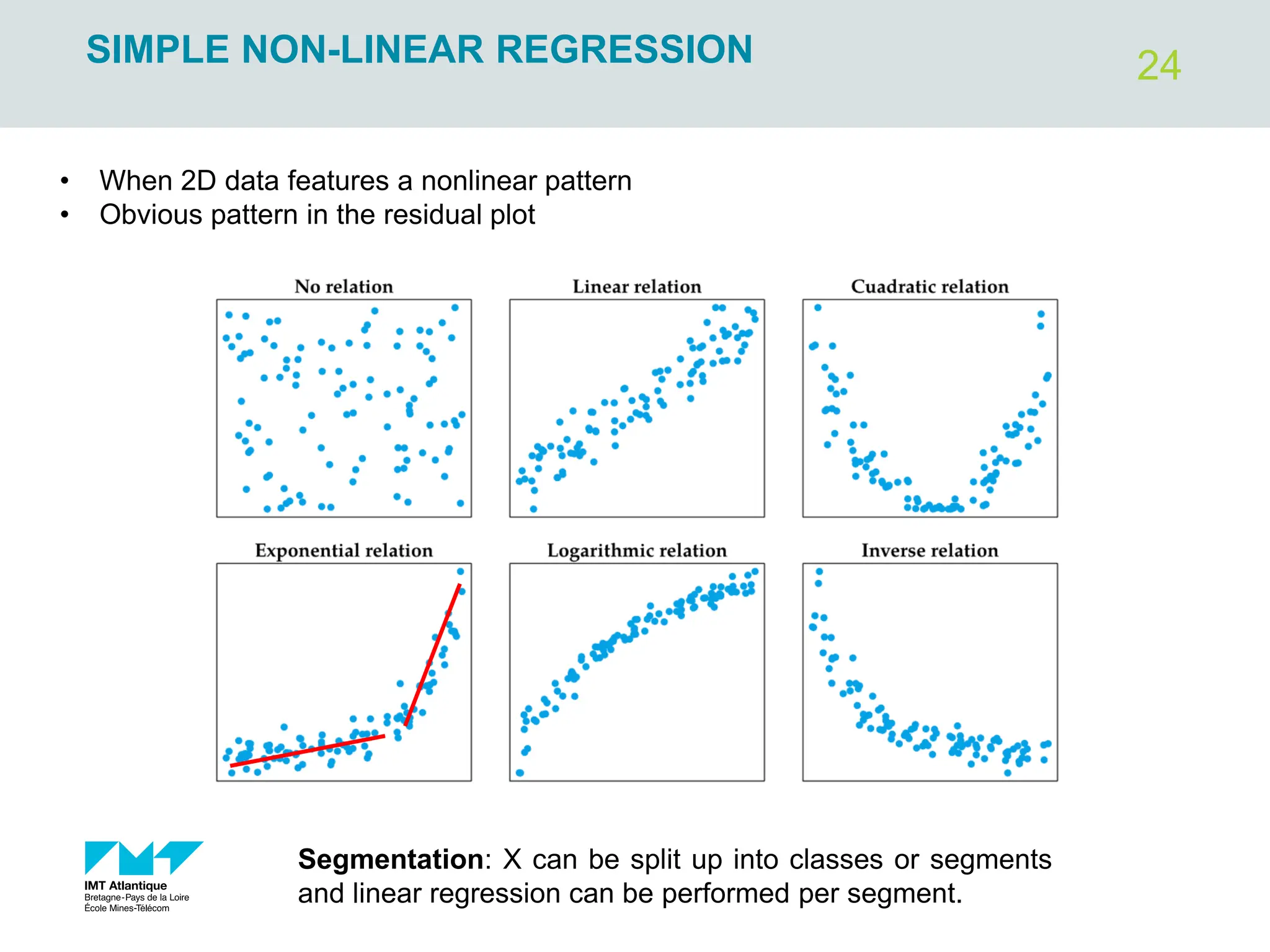

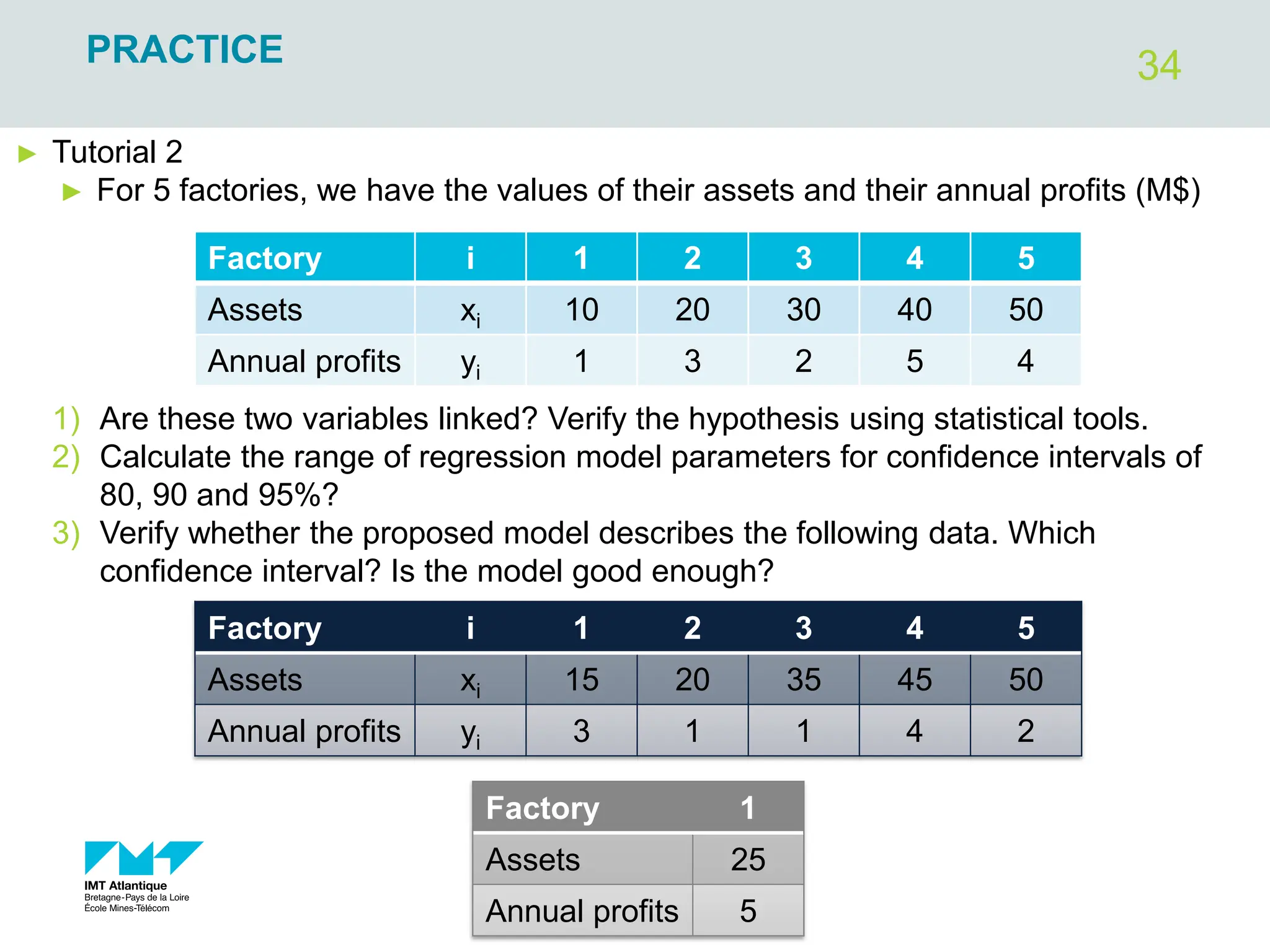

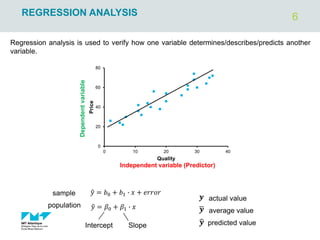

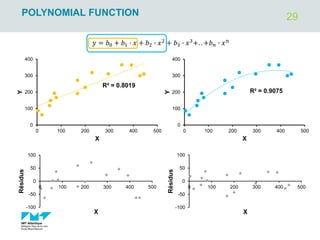

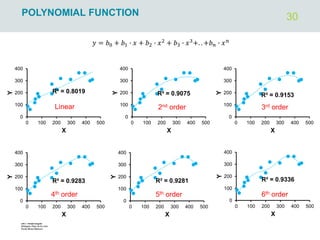

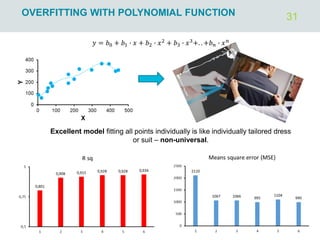

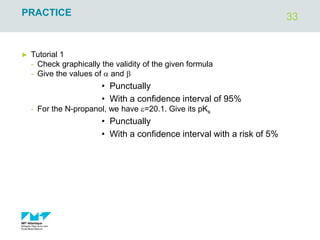

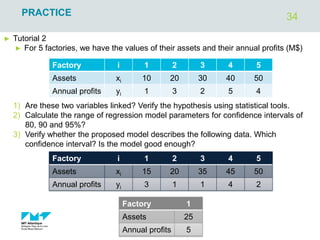

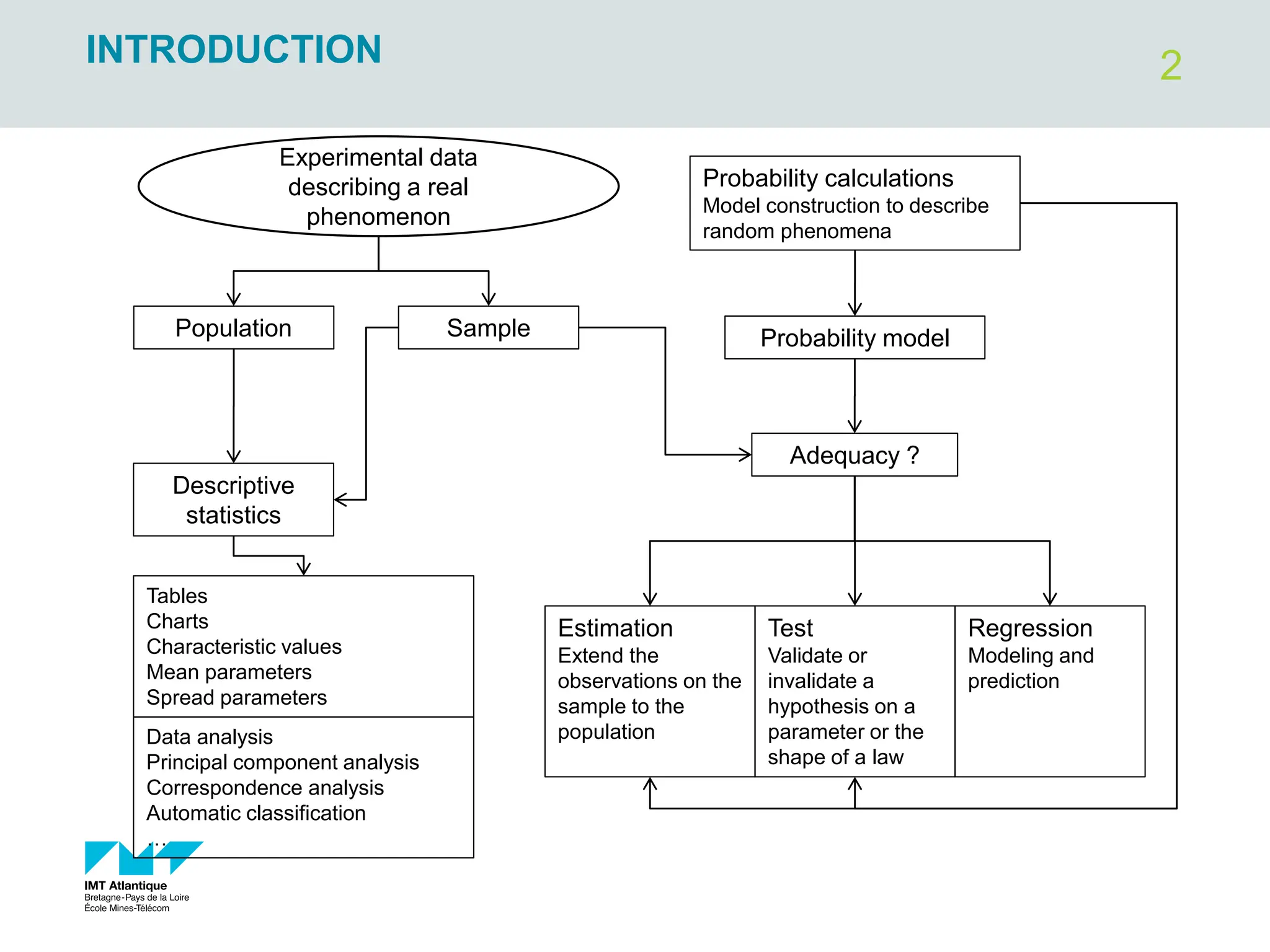

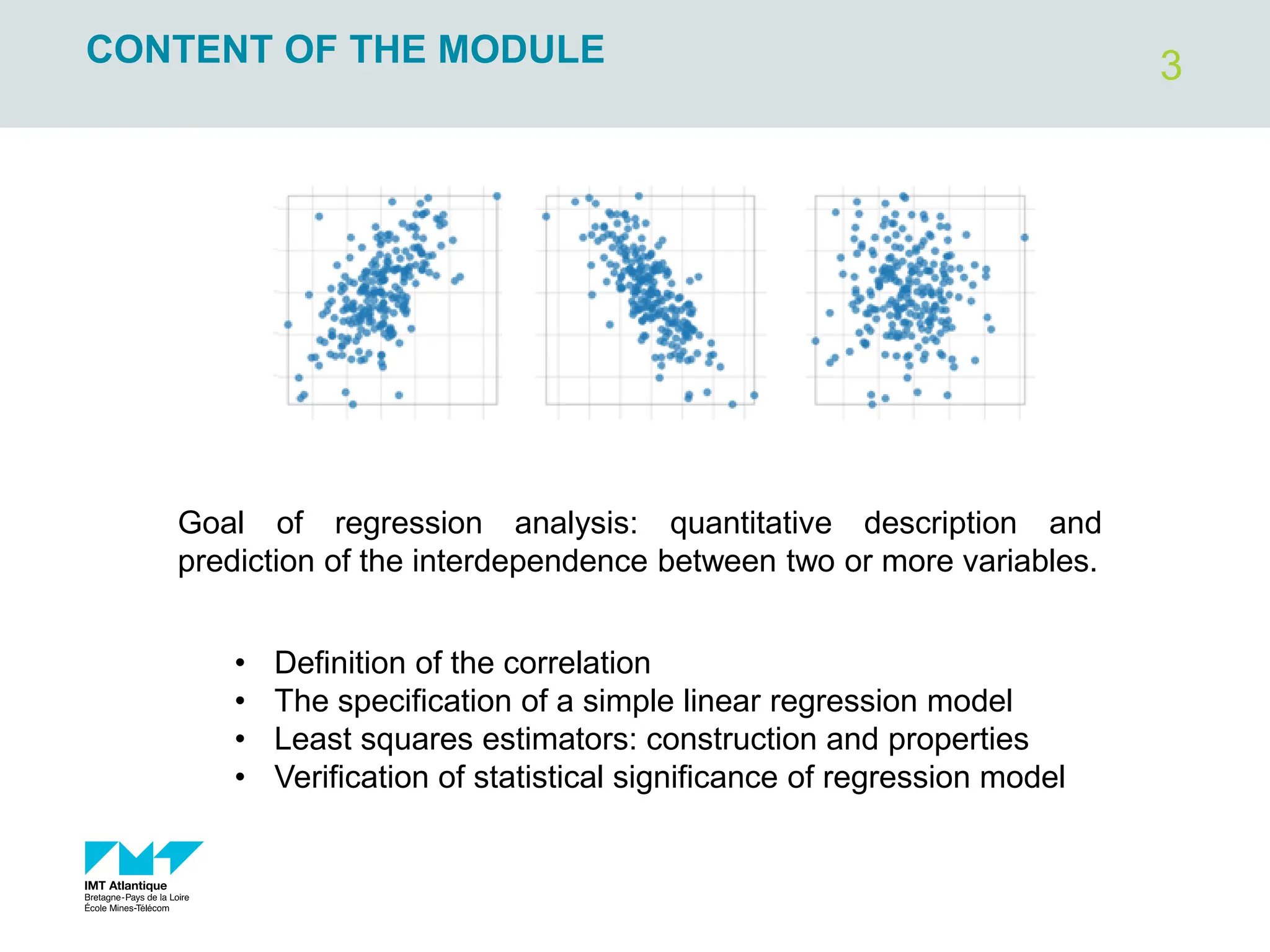

The document outlines regression analysis principles, including correlation and regression modeling, focusing on quantitative description and prediction of variable interdependence. It discusses methods like least squares for determining optimal regression parameters and the importance of statistical diagnostics for validating models. Additionally, it covers practical applications and examples related to linear and nonlinear regression, including confidence intervals and hypothesis testing.

![4

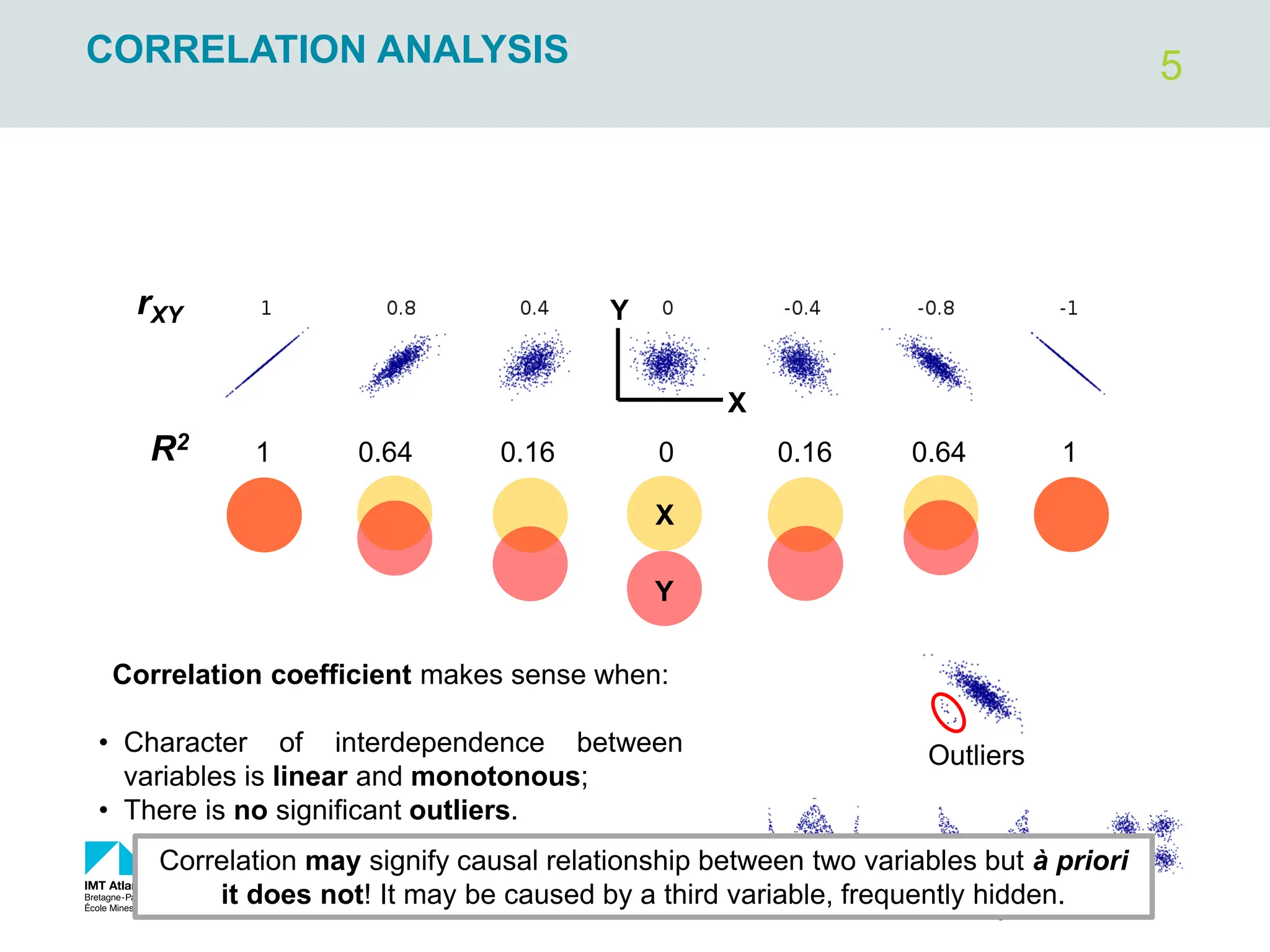

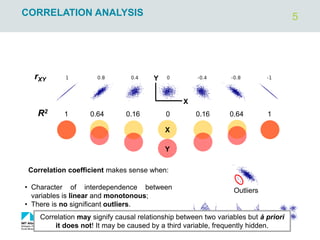

CORRELATION ANALYSIS

X

Y

X

_

Y

_

N1

N2

+

+

-

-

X

_

Y

_

Mean height and weight within the

sample

X : Independent or explanatory or exogenous variable

Y: Dependent or response or endogenous variable

Product of deviations from an average

>0 for most of points in case of

positive correlation between X and Y

𝑋1 − ത

𝑋 ∙ 𝑌1 − ത

𝑌 >0

𝑋2 − ത

𝑋 ∙ 𝑌2 − ത

𝑌 >0

𝑋𝑖 − ത

𝑋 ∙ 𝑌𝑖 − ത

𝑌

.

.

.

𝑐𝑜𝑣 =

σ 𝑋𝑖 − ത

𝑋 ∙ 𝑌𝑖 − ത

𝑌

𝑁 − 1

Covariance – quantitatively describes

the strength and the sense of

correlation between variables X and Y

𝑟𝑋𝑌 =

𝑐𝑜𝑣

𝜎𝑋 ∙ 𝜎𝑌

Correlation coefficient (Pearson’s

coefficient) – the same meaning as

covariance but independent on raw

data magnitude. Range: [-1; +1].

Coefficient of determination 𝑟𝑋𝑌

2

(shared variance) – determine how

the variance of variable 1 is influenced

by variable 2. Range: [0; 1].](https://image.slidesharecdn.com/simplelinearregression2022-240305024922-d5c9bf8c/85/simple-linear-regression-brief-introduction-4-320.jpg)

![4

CORRELATION ANALYSIS

X

Y

X

_

Y

_

N1

N2

+

+

-

-

X

_

Y

_

Mean height and weight within the

sample

X : Independent or explanatory or exogenous variable

Y: Dependent or response or endogenous variable

Product of deviations from an average

>0 for most of points in case of

positive correlation between X and Y

𝑋1 − ത

𝑋 ∙ 𝑌1 − ത

𝑌 >0

𝑋2 − ത

𝑋 ∙ 𝑌2 − ത

𝑌 >0

𝑋𝑖 − ത

𝑋 ∙ 𝑌𝑖 − ത

𝑌

.

.

.

𝑐𝑜𝑣 =

σ 𝑋𝑖 − ത

𝑋 ∙ 𝑌𝑖 − ത

𝑌

𝑁 − 1

Covariance – quantitatively describes

the strength and the sense of

correlation between variables X and Y

𝑟𝑋𝑌 =

𝑐𝑜𝑣

𝜎𝑋 ∙ 𝜎𝑌

Correlation coefficient (Pearson’s

coefficient) – the same meaning as

covariance but independent on raw

data magnitude. Range: [-1; +1].

Coefficient of determination 𝑟𝑋𝑌

2

(shared variance) – determine how

the variance of variable 1 is influenced

by variable 2. Range: [0; 1].](https://image.slidesharecdn.com/simplelinearregression2022-240305024922-d5c9bf8c/75/simple-linear-regression-brief-introduction-4-2048.jpg)