TSX | NYSEAMERICAN | WRN

CAUTIONARY NOTES

The information provided in this presentation is not

intended to be a comprehensive review of all matters and

developments concerning Western Copper and Gold

Corporation and its subsidiaries (collectively, the

“Company”). This document should be read in conjunction

with all other disclosure documents of the Company. No

securities commission or regulatory authority has

reviewed the accuracy or adequacy of the information

presented herein.

Note Regarding Forward-Looking Statements

Certain of the statements and information in this

presentation constitute “forward-looking statements”

within the meaning of the United States Private Securities

Litigation Reform Act of 1995 and “forward-looking

information” within the meaning of applicable Canadian

securities laws (together referred to herein as “forward-

looking statements”). Any statements or information that

express or involve discussions with respect to predictions,

expectations, beliefs, plans, projections, objectives,

assumptions, or future events or performance (often, but

not always, using words or phrases such as “expects”, “is

expected”, “anticipates”, “believes”, “plans”, “projects”,

“estimates”, “assumes”, “intends”, “strategies”, “targets”,

“goals”, “forecasts”, “objectives”, “budgets”, “schedules”,

“potential” or variations thereof or stating that certain

actions, events or results “may”, “could”, “would”, “might”

or “will” be taken, occur or be achieved, or the negative of

any of these terms and similar expressions) are not

statements of historical fact and may be forward-looking

statements. Such statements include, but are not limited

to, statements regarding mineral reserve and mineral

resource estimates, planned exploration and development

activities, corporate objectives, the economic prospects of

the Company’s projects, the Company’s future plans or

future revenues, and timing of development, or potential

expansions or improvements.

The forward-looking statements are necessarily based on

a number of estimates, assumptions, beliefs, expectations

and opinions of management as of the date of this

presentation that, while considered reasonable by

management, are inherently subject to significant

business, economic and competitive uncertainties and

contingencies. These estimates, assumptions, beliefs,

expectations and opinions include, without limitation, with

respect to any mineral reserve or mineral resource

estimate, the key assumptions and parameters on which

such estimates are based, prevailing and projected

market prices and foreign exchange rates, projected

capital and operating costs, continued availability of

capital and financing, availability of equipment and

personnel required for construction and operations, the

Company not experiencing unforeseen delays,

unexpected geological or other effects, equipment

failures, permitting delays, and general economic, market

or business conditions.

Forward-looking statements are subject to known and

unknown risks and uncertainties which could cause actual

results to differ materially from estimated results. Such

risks and uncertainties include, but are not limited to, the

Company’s ability to raise sufficient capital to fund

development; changes in general economic conditions or

financial markets, changes in prices for the Company’s

mineral products or increases in input costs; uncertainties

relating to interpretation of drill results and the geological

continuity and grade of mineral deposits; that mineral

resources and mineral reserves are not as estimated;

risks related to cooperation of government agencies and

First Nations in the exploration and development of the

property; litigation; legislative, environmental and other

judicial, regulatory, political and competitive developments

in Canada; technological and operational difficulties or

inability to obtain permits encountered in connection with

exploration and development activities; labour relations

matters, changing foreign exchange rates, and other

factors described under the heading “Risk Factors” in the

Company’s annual information form for the most recently

completed financial year and its other publicly filed

disclosure documents. This list is not exhaustive of the

factors that may affect any of the Company’s forward-

looking statements.

Although the forward-looking statements contained in this

presentation are based upon what management believes

are reasonable assumptions, there can be no assurance

that actual results will be consistent with these forward-

looking statements. All forward-looking statements in this

presentation are qualified by this cautionary note.

Accordingly, readers should not place undue reliance on

such statements. Other than as specifically required by

applicable laws, the Company is under no obligation and

expressly disclaims any such obligation to update or alter

the forward-looking statements whether as a result of new

information, future events or otherwise. These forward-

looking statements are made as of the date of this

presentation.

Note to U.S. Readers/Investors

Information regarding the Company’s mining operations

included in this presentation has been prepared in

accordance with the requirements of the securities laws in

effect in Canada, which differ in certain material respects

from the disclosure requirements of United States

securities laws applicable to domestic United States

issuers. The terms “mineral reserve”, “proven mineral

reserve” and “probable mineral reserve” are Canadian

mining terms as defined in accordance with Canadian

National Instrument 43-101 – Standards of Disclosure for

Mineral Projects (“NI 43-101”) and the Canadian Institute

of Mining, Metallurgy and Petroleum (the “CIM”) Definition

Standards for Mineral Resources and Mineral Reserves,

adopted by the CIM Council, as amended. NI 43-101 is a

rule developed by the Canadian Securities Administrators

that establishes standards for all public disclosure an

issuer makes of scientific and technical information

concerning mineral projects. The definitions of these

terms and other mining terms, such as “inferred mineral

resource”, differ from the definitions of such terms, if any,

for purposes of the disclosure requirements of the U.S.

Securities and Exchange Commission (the “SEC”).

Accordingly, information in this presentation describing

the Company’s mineral deposits may not be comparable

to similar information made public by issuers subject to

the SEC’s reporting and disclosure requirements

applicable to domestic United States issuers.

Note Regarding Inferred Mineral Resources

Under Canadian rules, estimates of inferred mineral

resources are considered too speculative geologically to

have the economic considerations applied to them to

enable them to be categorized as mineral reserves and,

accordingly, may not form the basis of feasibility or pre-

feasibility studies, or economic studies except for a

preliminary economic assessment as defined under NI

43-101. Investors are cautioned not to assume that part or

all of an inferred mineral resource exists or is

economically or legally mineable. Mineral resources that

are not mineral reserves do not have demonstrated

economic viability.

2

TSX | NYSEAMERICAN | WRN

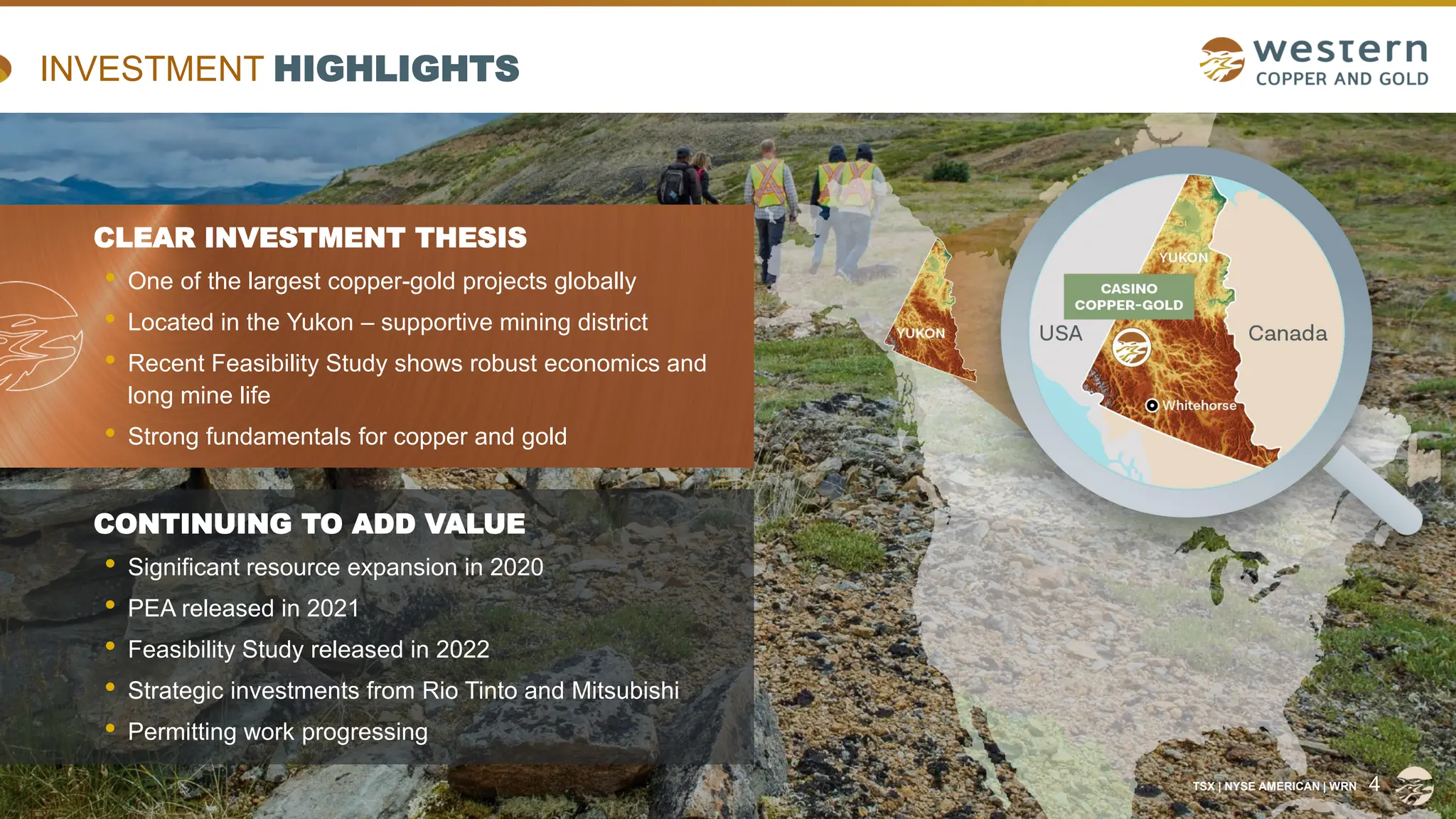

INVESTMENT HIGHLIGHTS

CLEAR INVESTMENT THESIS

• One of the largest copper-gold projects globally

• Located in the Yukon – supportive mining district

• Recent Feasibility Study shows robust economics and

long mine life

• Strong fundamentals for copper and gold

CONTINUING TO ADD VALUE

• Significant resource expansion in 2020

• PEA released in 2021

• Feasibility Study released in 2022

• Strategic investments from Rio Tinto and Mitsubishi

• Permitting work progressing

TSX | NYSE AMERICAN | WRN 4

5.

TSX | NYSEAMERICAN | WRN

STRATEGIC INVESTMENTS

5

Endorsed by two of the most respected companies across the mining and materials value chain

Participation on Technical and Sustainability Committee adds multidisciplinary expertise to project development

Second-largest mining company in the world

Operations in 35 countries

Pursuing growth in energy transition materials

Investment resides within Rio Tinto’s Copper division

Roots of metals business trace back ~150 years

Minority interests in three producing copper mines

Focused on securing reliable, long-term sources of clean

copper concentrate for smelting operations in Japan

Aims to triple its volume of secured concentrate by 2031

C$25.6M

C$2.3M

C$6.0M

C$0.3M

C$5.0M

May 2021 (initial investment)

April 2023 (top-up)

November 2023 (rights extension)

March 2024 (top-up)

April 2023 (top-up)

C$25.6M March 2023 (initial investment)

May 2025 (rights extension)

2.0M shares

open market

6.

TSX | NYSEAMERICAN | WRN

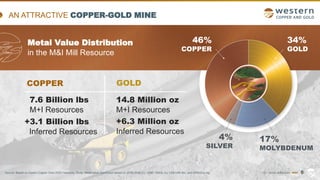

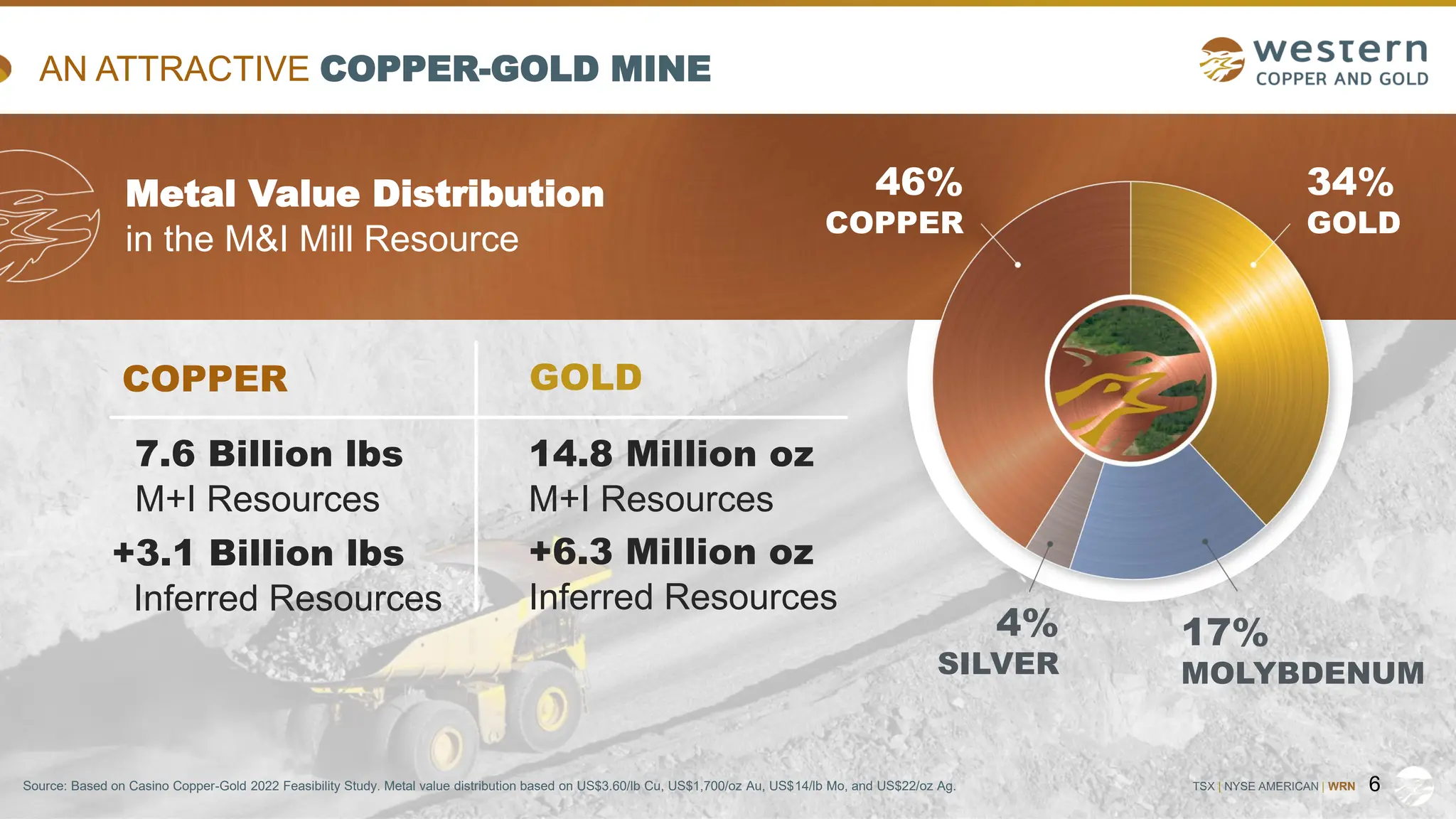

AN ATTRACTIVE COPPER-GOLD MINE

6

Metal Value Distribution

in the M&I Mill Resource

46%

COPPER

34%

GOLD

4%

SILVER

17%

MOLYBDENUM

COPPER GOLD

7.6 Billion lbs

M+I Resources

+3.1 Billion lbs

Inferred Resources

14.8 Million oz

M+I Resources

+6.3 Million oz

Inferred Resources

Source: Based on Casino Copper-Gold 2022 Feasibility Study. Metal value distribution based on US$3.60/lb Cu, US$1,700/oz Au, US$14/lb Mo, and US$22/oz Ag.

7.

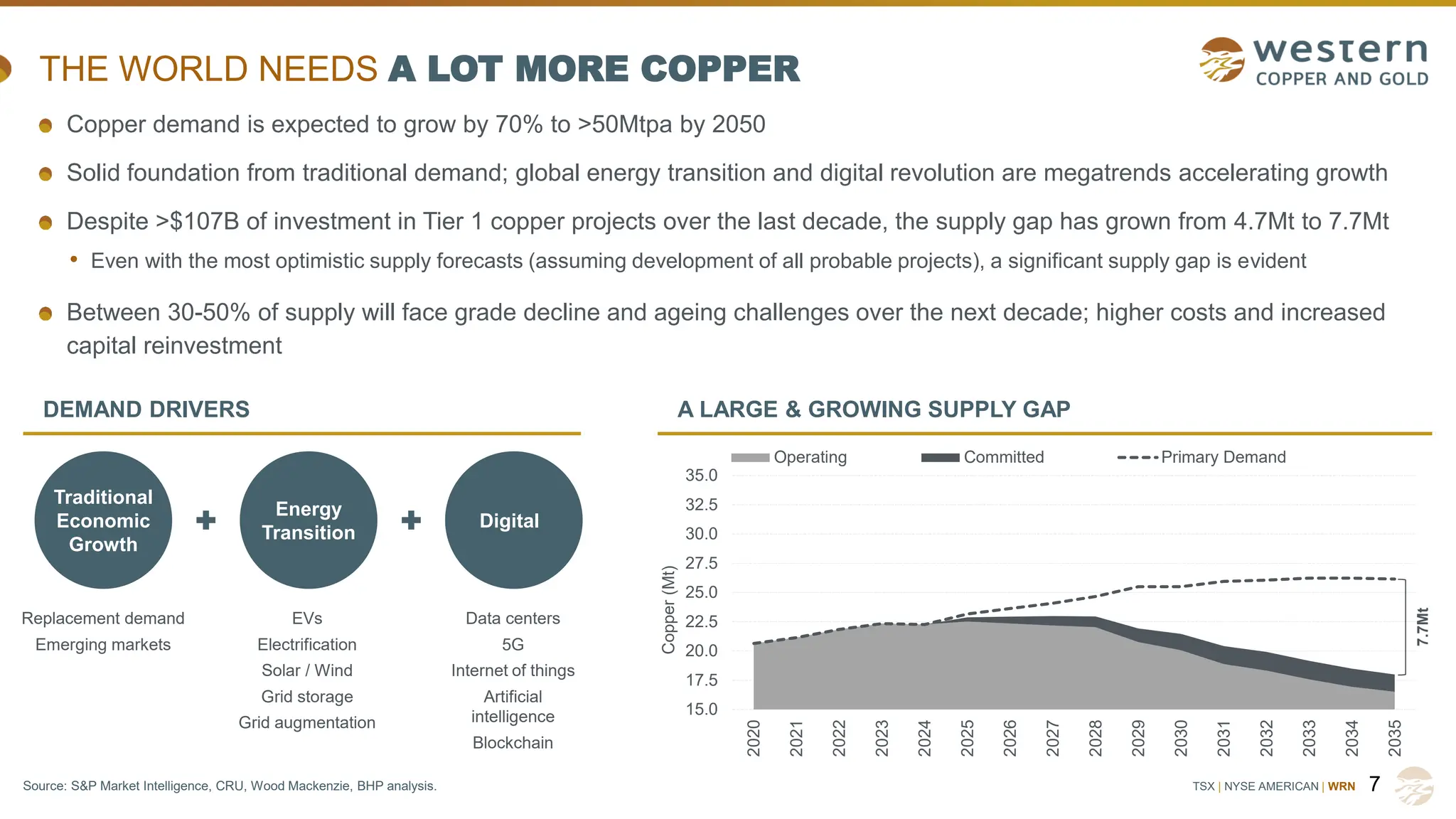

TSX | NYSEAMERICAN | WRN

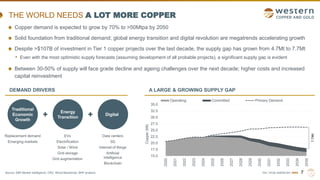

Source: S&P Market Intelligence, CRU, Wood Mackenzie, BHP analysis.

DEMAND DRIVERS

THE WORLD NEEDS A LOT MORE COPPER

7

Copper demand is expected to grow by 70% to >50Mtpa by 2050

Solid foundation from traditional demand; global energy transition and digital revolution are megatrends accelerating growth

Despite >$107B of investment in Tier 1 copper projects over the last decade, the supply gap has grown from 4.7Mt to 7.7Mt

• Even with the most optimistic supply forecasts (assuming development of all probable projects), a significant supply gap is evident

Between 30-50% of supply will face grade decline and ageing challenges over the next decade; higher costs and increased

capital reinvestment

A LARGE & GROWING SUPPLY GAP

Traditional

Economic

Growth

Energy

Transition

Digital

EVs

Electrification

Solar / Wind

Grid storage

Grid augmentation

Data centers

5G

Internet of things

Artificial

intelligence

Blockchain

Replacement demand

Emerging markets

15.0

17.5

20.0

22.5

25.0

27.5

30.0

32.5

35.0

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

Copper

(Mt)

Operating Committed Primary Demand

7.7Mt

8.

TSX | NYSEAMERICAN | WRN

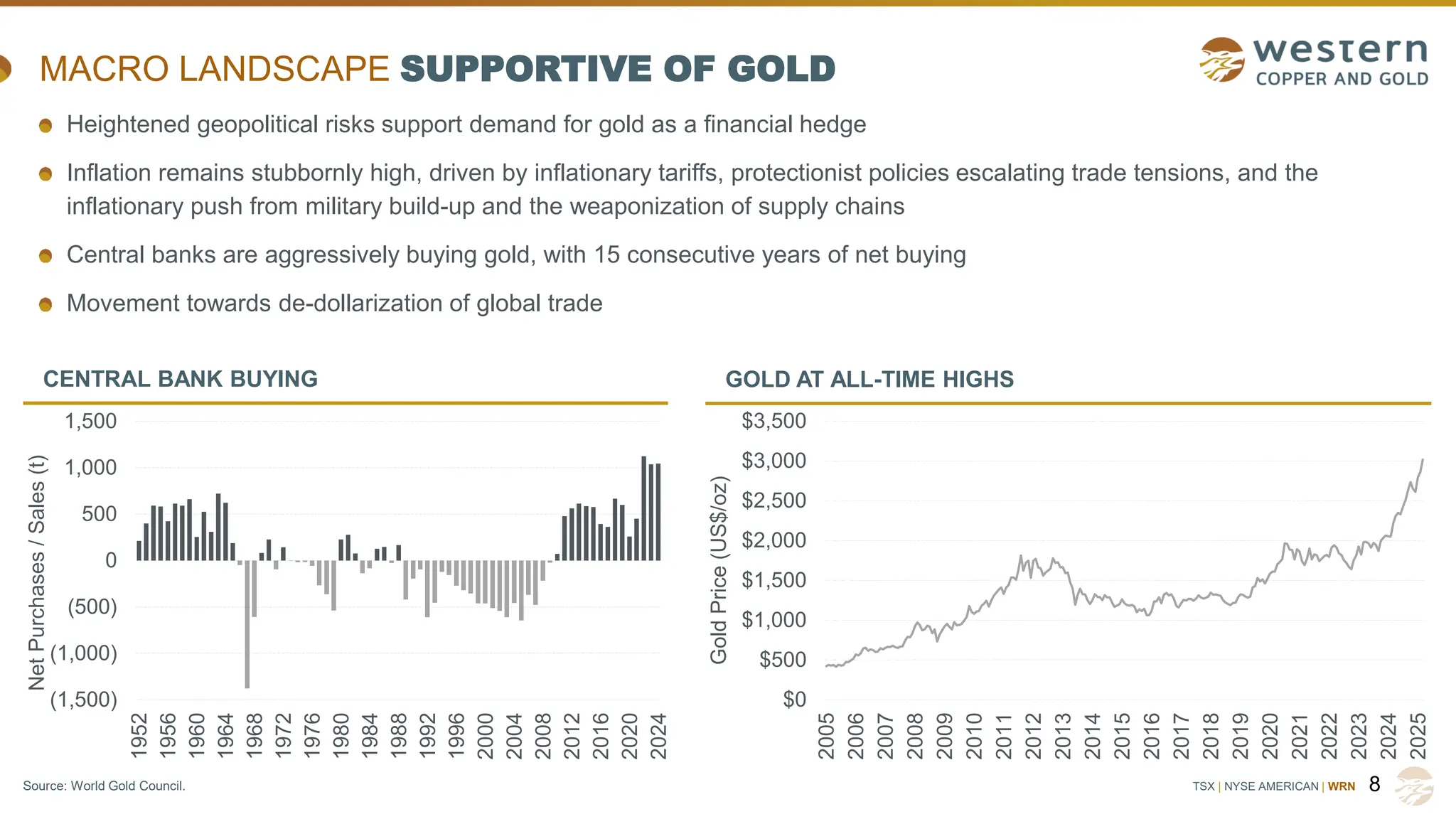

MACRO LANDSCAPE SUPPORTIVE OF GOLD

8

GOLD AT ALL-TIME HIGHS

CENTRAL BANK BUYING

(1,500)

(1,000)

(500)

0

500

1,000

1,500

1952

1956

1960

1964

1968

1972

1976

1980

1984

1988

1992

1996

2000

2004

2008

2012

2016

2020

2024

Net

Purchases

/

Sales

(t)

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

Gold

Price

(US$/oz)

Heightened geopolitical risks support demand for gold as a financial hedge

Inflation remains stubbornly high, driven by inflationary tariffs, protectionist policies escalating trade tensions, and the

inflationary push from military build-up and the weaponization of supply chains

Central banks are aggressively buying gold, with 15 consecutive years of net buying

Movement towards de-dollarization of global trade

Source: World Gold Council.

9.

TSX | NYSEAMERICAN | WRN

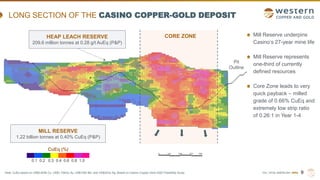

Note: CuEq based on US$3.60/lb Cu, US$1,700/oz Au, US$14/lb Mo, and US$22/oz Ag. Based on Casino Copper-Gold 2022 Feasibility Study.

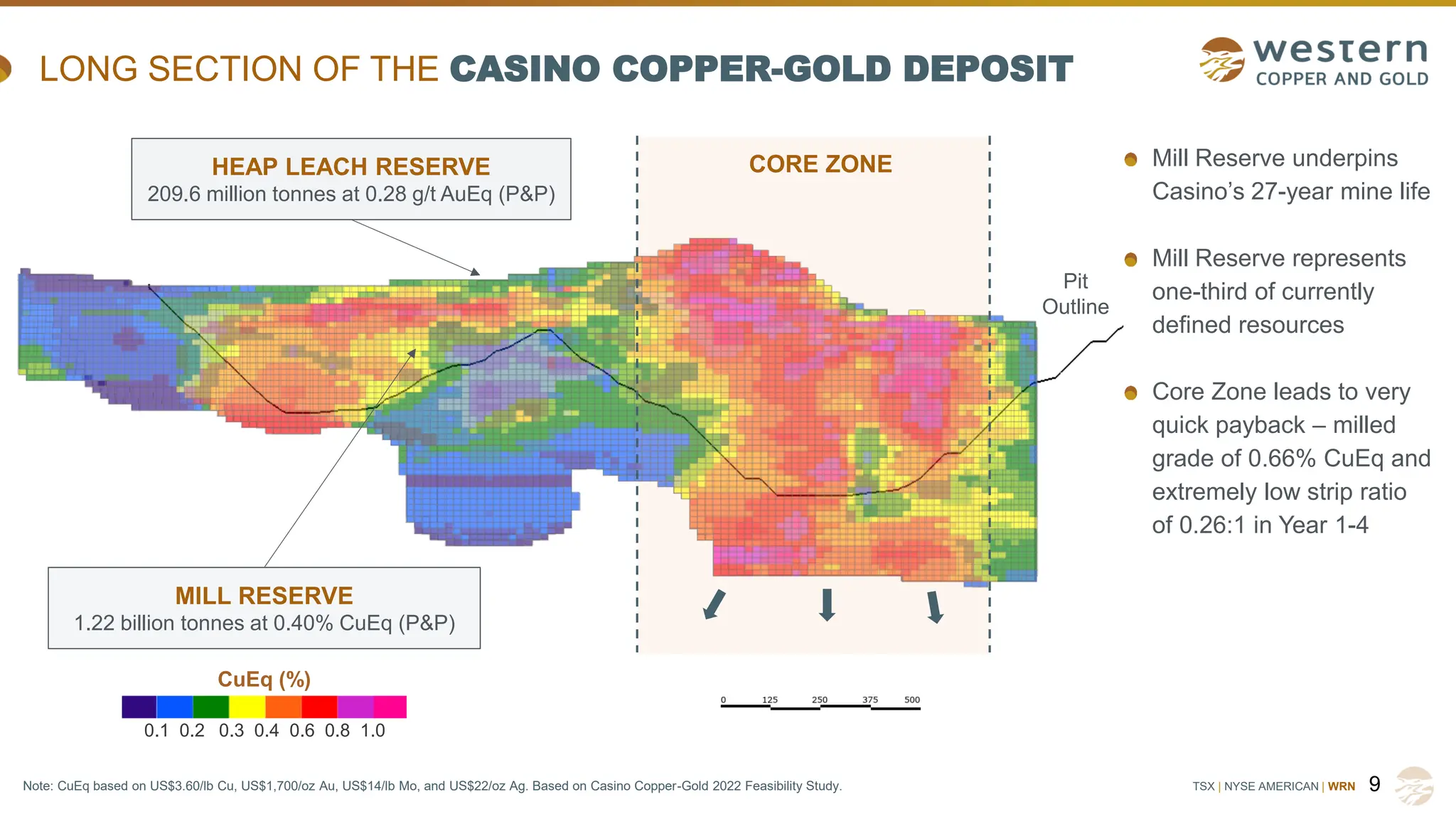

LONG SECTION OF THE CASINO COPPER-GOLD DEPOSIT

9

HEAP LEACH RESERVE

209.6 million tonnes at 0.28 g/t AuEq (P&P)

MILL RESERVE

1.22 billion tonnes at 0.40% CuEq (P&P)

CORE ZONE

Pit

Outline

CuEq (%)

1.0

0.8

0.6

0.4

0.3

0.2

0.1

Mill Reserve underpins

Casino’s 27-year mine life

Mill Reserve represents

one-third of currently

defined resources

Core Zone leads to very

quick payback – milled

grade of 0.66% CuEq and

extremely low strip ratio

of 0.26:1 in Year 1-4

10.

TSX | NYSEAMERICAN | WRN

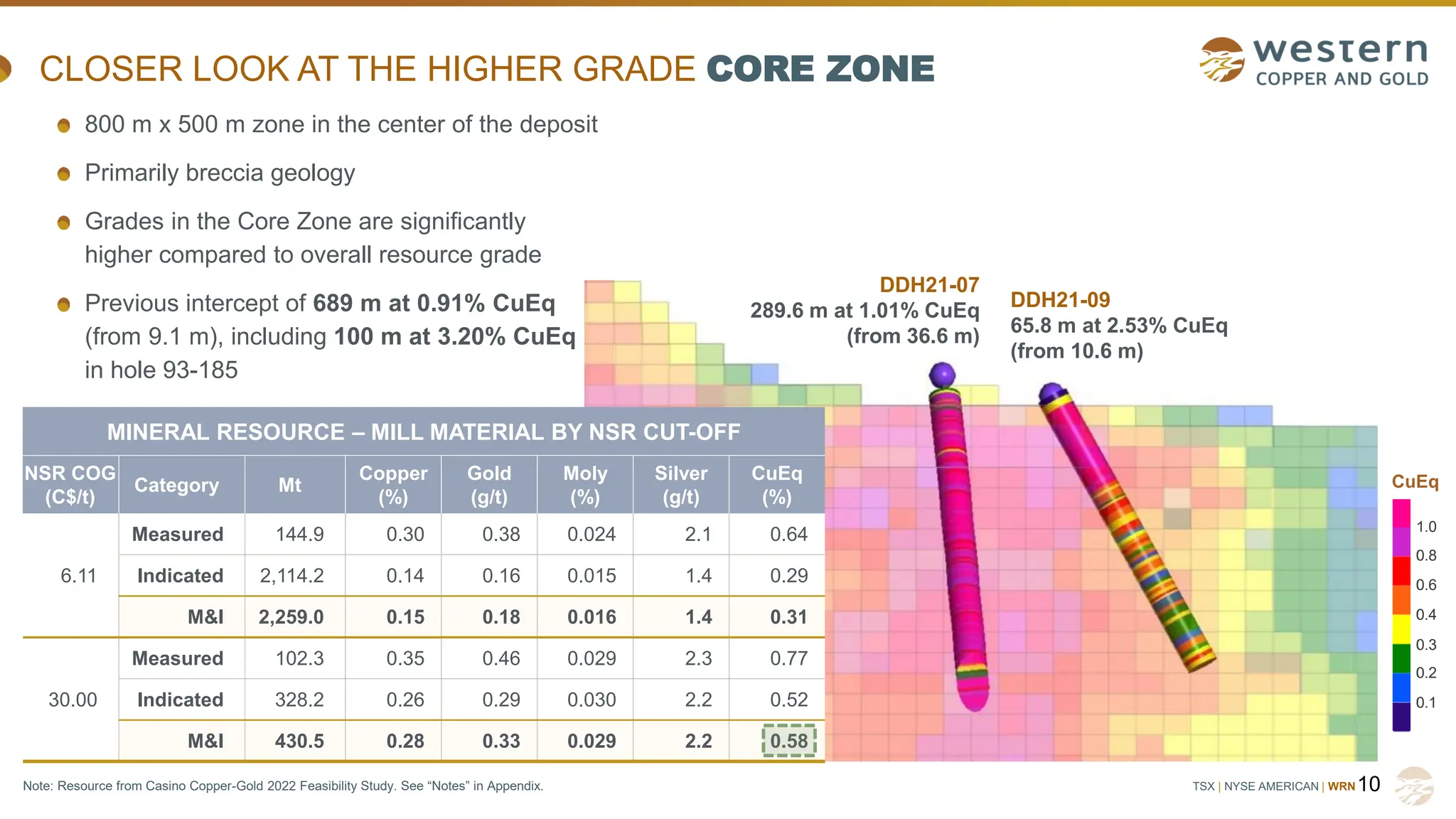

CLOSER LOOK AT THE HIGHER GRADE CORE ZONE

10

DDH21-09

65.8 m at 2.53% CuEq

(from 10.6 m)

DDH21-07

289.6 m at 1.01% CuEq

(from 36.6 m)

CuEq

1.0

0.8

0.6

0.4

0.3

0.2

0.1

MINERAL RESOURCE – MILL MATERIAL BY NSR CUT-OFF

NSR COG

(C$/t)

Category Mt

Copper

(%)

Gold

(g/t)

Moly

(%)

Silver

(g/t)

CuEq

(%)

6.11

Measured 144.9 0.30 0.38 0.024 2.1 0.64

Indicated 2,114.2 0.14 0.16 0.015 1.4 0.29

M&I 2,259.0 0.15 0.18 0.016 1.4 0.31

30.00

Measured 102.3 0.35 0.46 0.029 2.3 0.77

Indicated 328.2 0.26 0.29 0.030 2.2 0.52

M&I 430.5 0.28 0.33 0.029 2.2 0.58

800 m x 500 m zone in the center of the deposit

Primarily breccia geology

Grades in the Core Zone are significantly

higher compared to overall resource grade

Previous intercept of 689 m at 0.91% CuEq

(from 9.1 m), including 100 m at 3.20% CuEq

in hole 93-185

Note: Resource from Casino Copper-Gold 2022 Feasibility Study. See “Notes” in Appendix.

11.

TSX | NYSEAMERICAN | WRN 11

CASINO

PROJECT

OPERATING

MINES

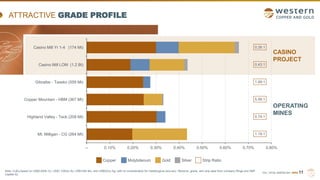

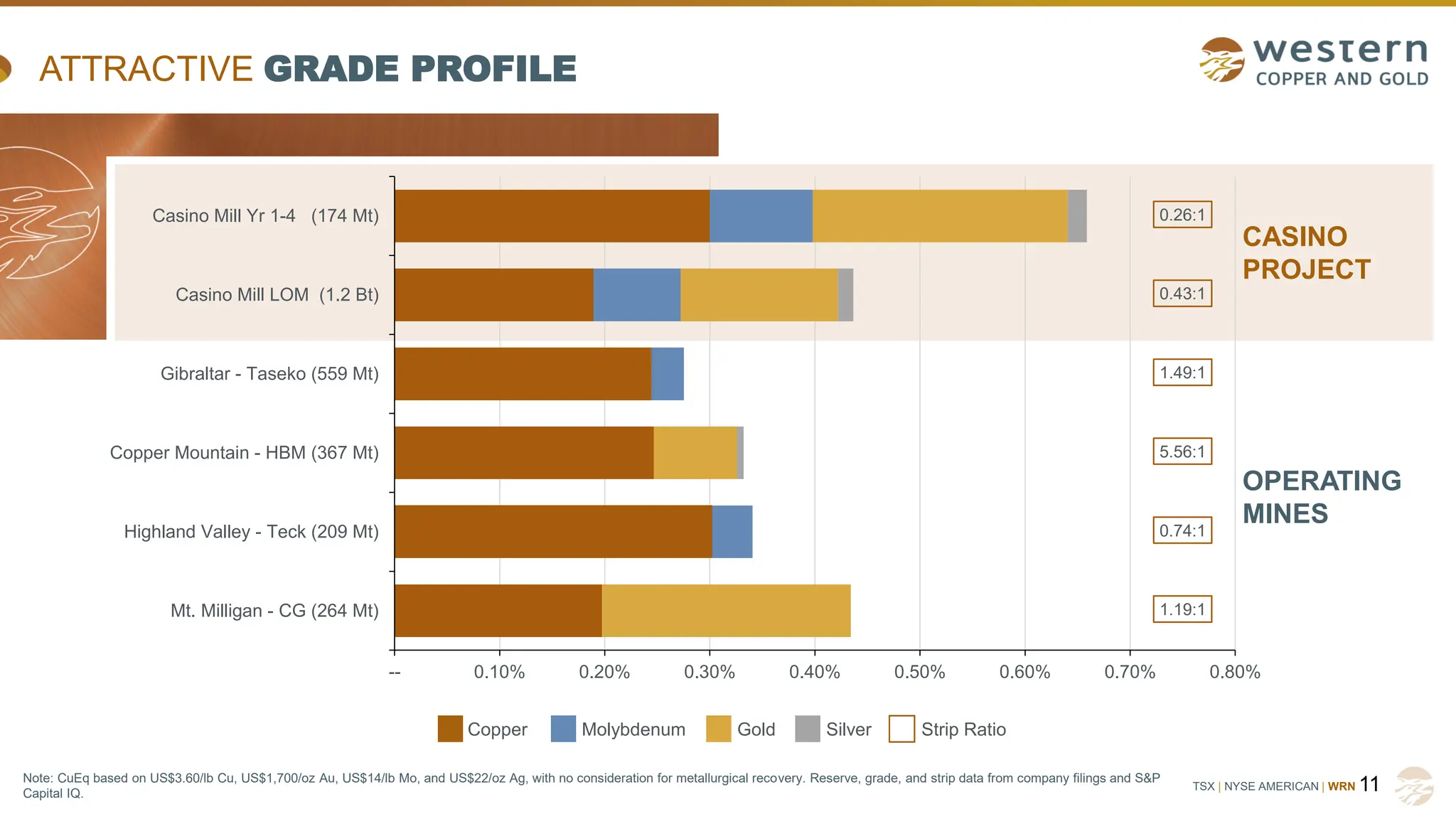

ATTRACTIVE GRADE PROFILE

Copper Molybdenum Gold Silver Strip Ratio

Note: CuEq based on US$3.60/lb Cu, US$1,700/oz Au, US$14/lb Mo, and US$22/oz Ag, with no consideration for metallurgical recovery. Reserve, grade, and strip data from company filings and S&P

Capital IQ.

1.19:1

0.74:1

5.56:1

1.49:1

0.43:1

0.26:1

-- 0.10% 0.20% 0.30% 0.40% 0.50% 0.60% 0.70% 0.80%

Mt. Milligan - CG (264 Mt)

Highland Valley - Teck (209 Mt)

Copper Mountain - HBM (367 Mt)

Gibraltar - Taseko (559 Mt)

Casino Mill LOM (1.2 Bt)

Casino Mill Yr 1-4 (174 Mt)

12.

TSX | NYSEAMERICAN | WRN

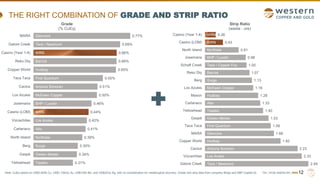

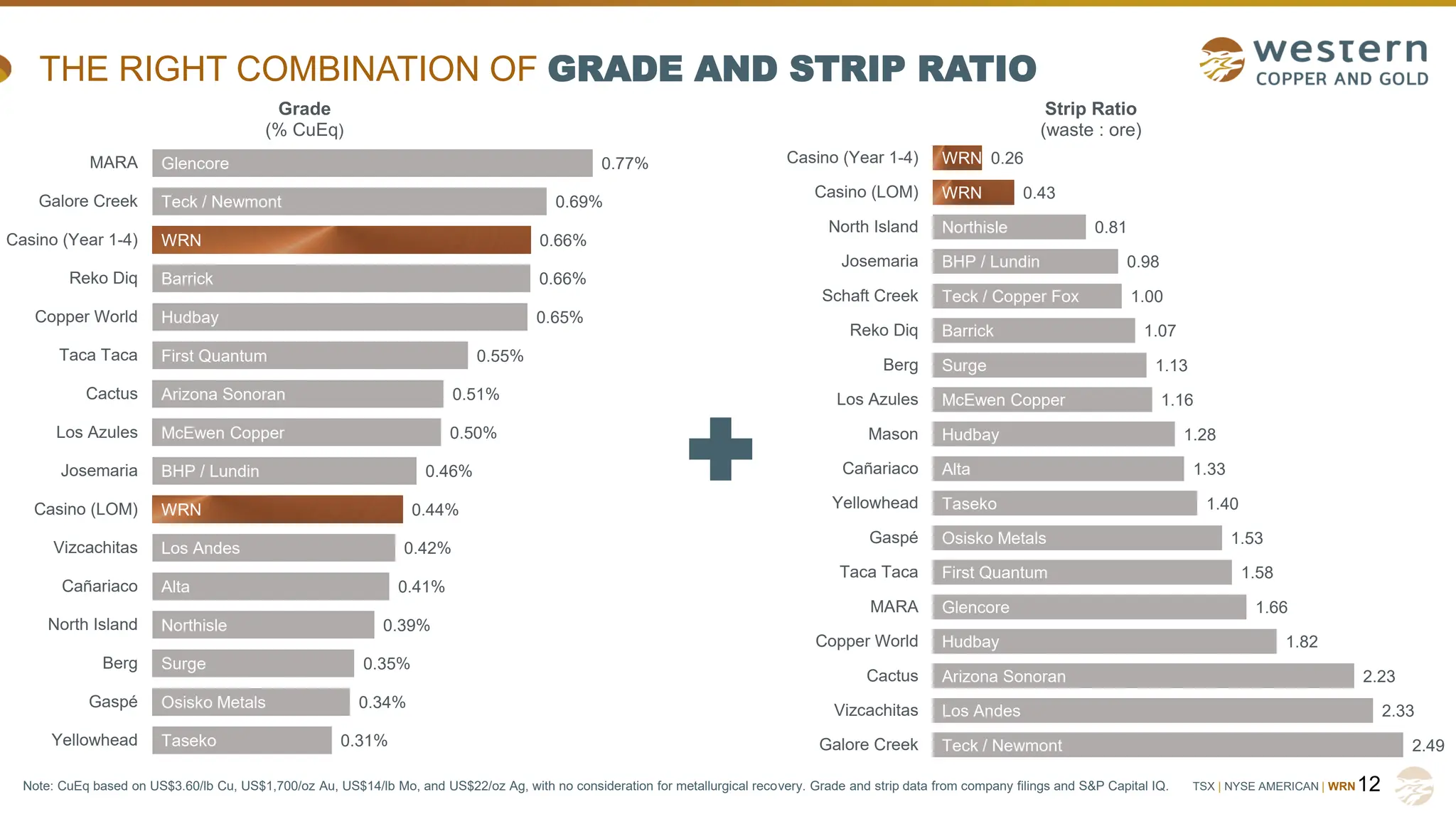

THE RIGHT COMBINATION OF GRADE AND STRIP RATIO

12

Note: CuEq based on US$3.60/lb Cu, US$1,700/oz Au, US$14/lb Mo, and US$22/oz Ag, with no consideration for metallurgical recovery. Grade and strip data from company filings and S&P Capital IQ.

Taseko

Osisko Metals

Surge

Northisle

Alta

Los Andes

WRN

BHP / Lundin

McEwen Copper

Arizona Sonoran

First Quantum

Hudbay

Barrick

WRN

Teck / Newmont

Glencore

0.31%

0.34%

0.35%

0.39%

0.41%

0.42%

0.44%

0.46%

0.50%

0.51%

0.55%

0.65%

0.66%

0.66%

0.69%

0.77%

Yellowhead

Gaspé

Berg

North Island

Cañariaco

Vizcachitas

Casino (LOM)

Josemaria

Los Azules

Cactus

Taca Taca

Copper World

Reko Diq

Casino (Year 1-4)

Galore Creek

MARA

Grade

(% CuEq)

Teck / Newmont

Los Andes

Arizona Sonoran

Hudbay

Glencore

First Quantum

Osisko Metals

Taseko

Alta

Hudbay

McEwen Copper

Surge

Barrick

Teck / Copper Fox

BHP / Lundin

Northisle

WRN

WRN

2.49

2.33

2.23

1.82

1.66

1.58

1.53

1.40

1.33

1.28

1.16

1.13

1.07

1.00

0.98

0.81

0.43

0.26

Galore Creek

Vizcachitas

Cactus

Copper World

MARA

Taca Taca

Gaspé

Yellowhead

Cañariaco

Mason

Los Azules

Berg

Reko Diq

Schaft Creek

Josemaria

North Island

Casino (LOM)

Casino (Year 1-4)

Strip Ratio

(waste : ore)

TSX | NYSEAMERICAN | WRN

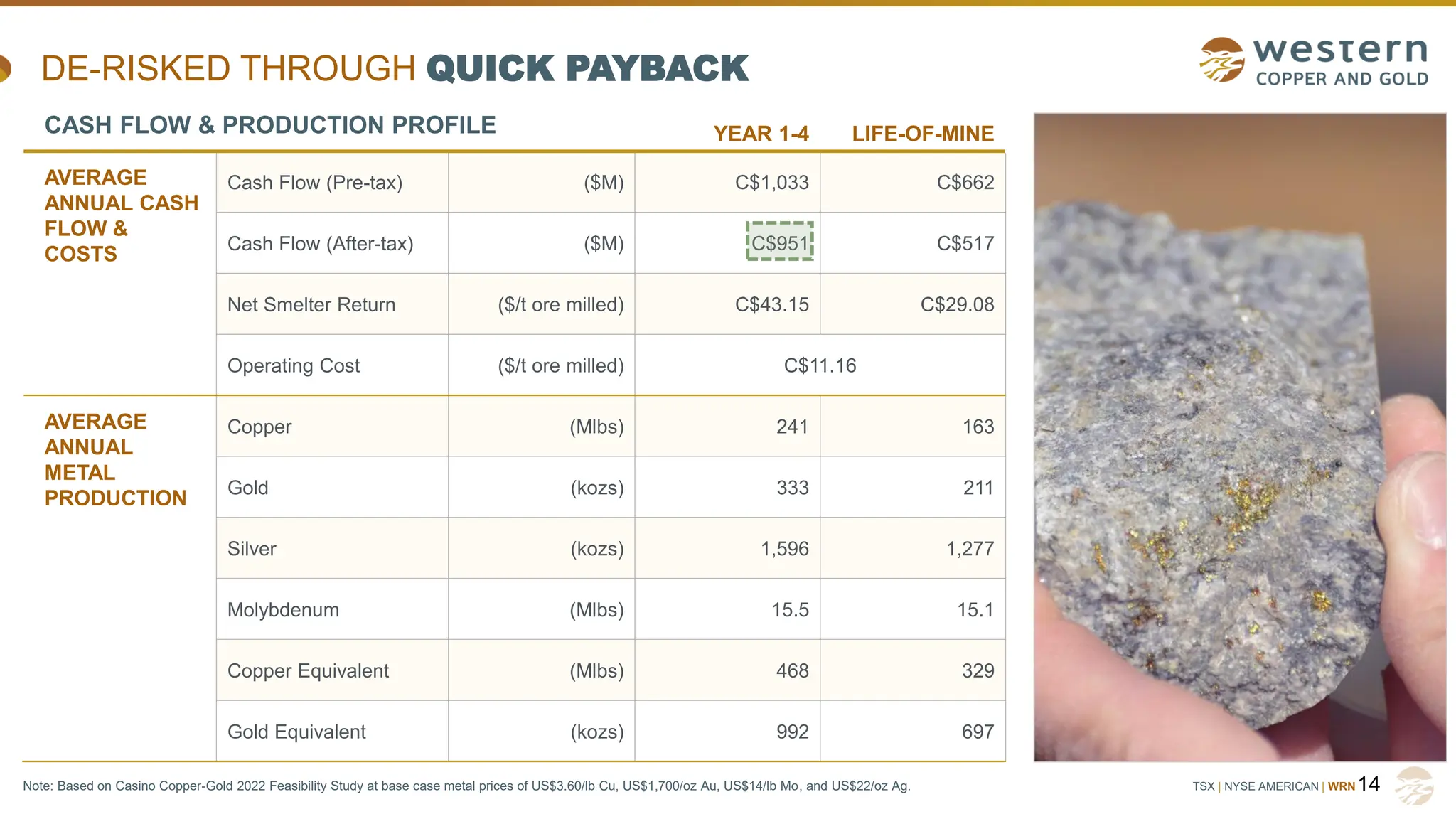

DE-RISKED THROUGH QUICK PAYBACK

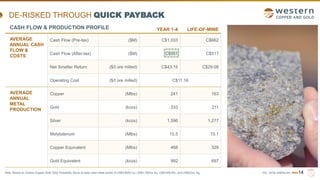

14

CASH FLOW & PRODUCTION PROFILE YEAR 1-4 LIFE-OF-MINE

AVERAGE

ANNUAL CASH

FLOW &

COSTS

Cash Flow (Pre-tax) ($M) C$1,033 C$662

Cash Flow (After-tax) ($M) C$951 C$517

Net Smelter Return ($/t ore milled) C$43.15 C$29.08

Operating Cost ($/t ore milled) C$11.16

AVERAGE

ANNUAL

METAL

PRODUCTION

Copper (Mlbs) 241 163

Gold (kozs) 333 211

Silver (kozs) 1,596 1,277

Molybdenum (Mlbs) 15.5 15.1

Copper Equivalent (Mlbs) 468 329

Gold Equivalent (kozs) 992 697

Note: Based on Casino Copper-Gold 2022 Feasibility Study at base case metal prices of US$3.60/lb Cu, US$1,700/oz Au, US$14/lb Mo, and US$22/oz Ag.

15.

TSX | NYSEAMERICAN | WRN

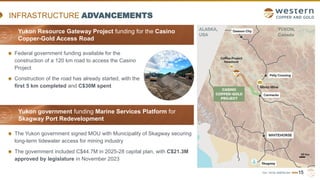

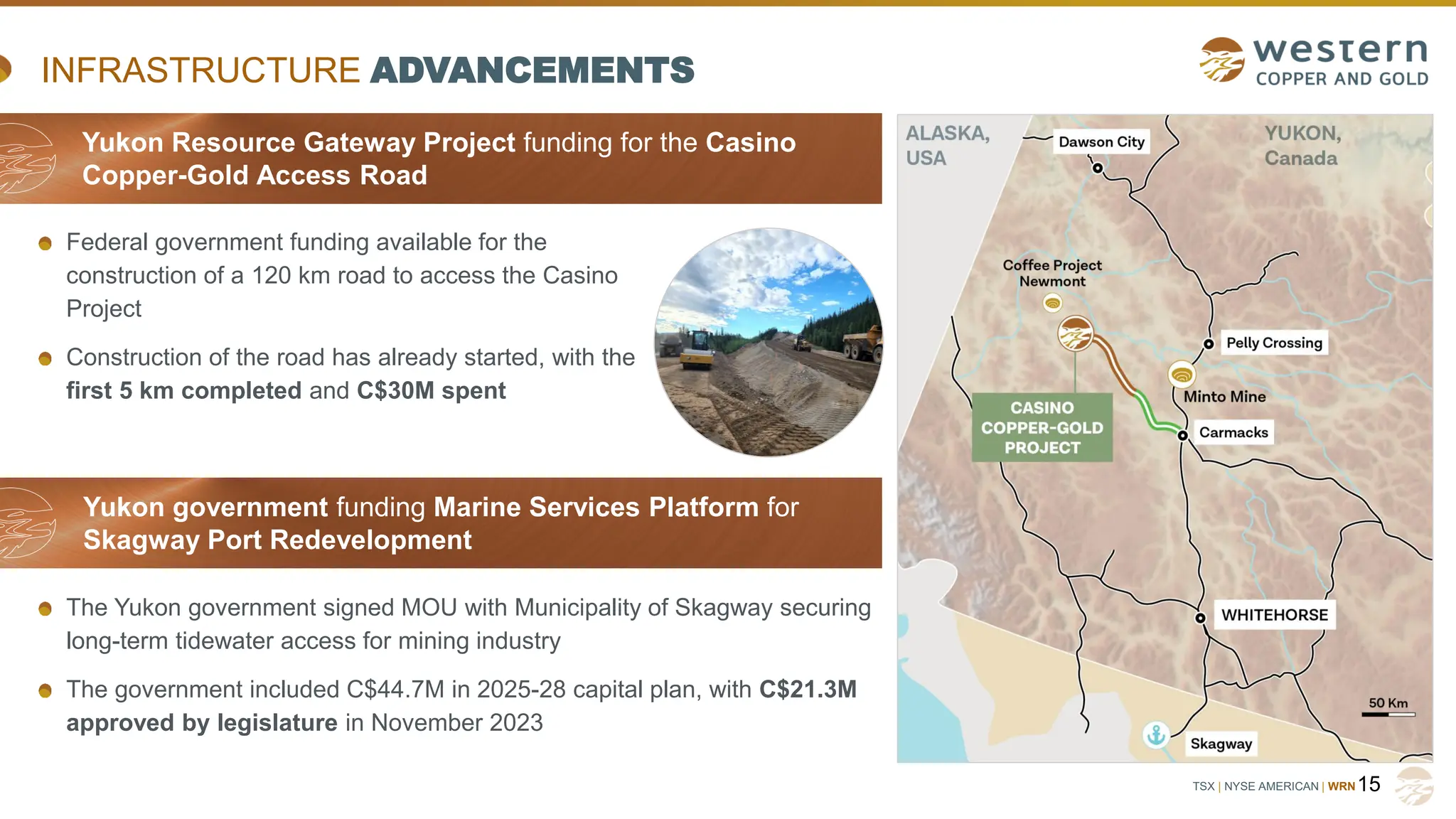

INFRASTRUCTURE ADVANCEMENTS

15

Yukon Resource Gateway Project funding for the Casino

Copper-Gold Access Road

Yukon government funding Marine Services Platform for

Skagway Port Redevelopment

Federal government funding available for the

construction of a 120 km road to access the Casino

Project

Construction of the road has already started, with the

first 5 km completed and C$30M spent

The Yukon government signed MOU with Municipality of Skagway securing

long-term tidewater access for mining industry

The government included C$44.7M in 2025-28 capital plan, with C$21.3M

approved by legislature in November 2023

16.

TSX | NYSEAMERICAN | WRN

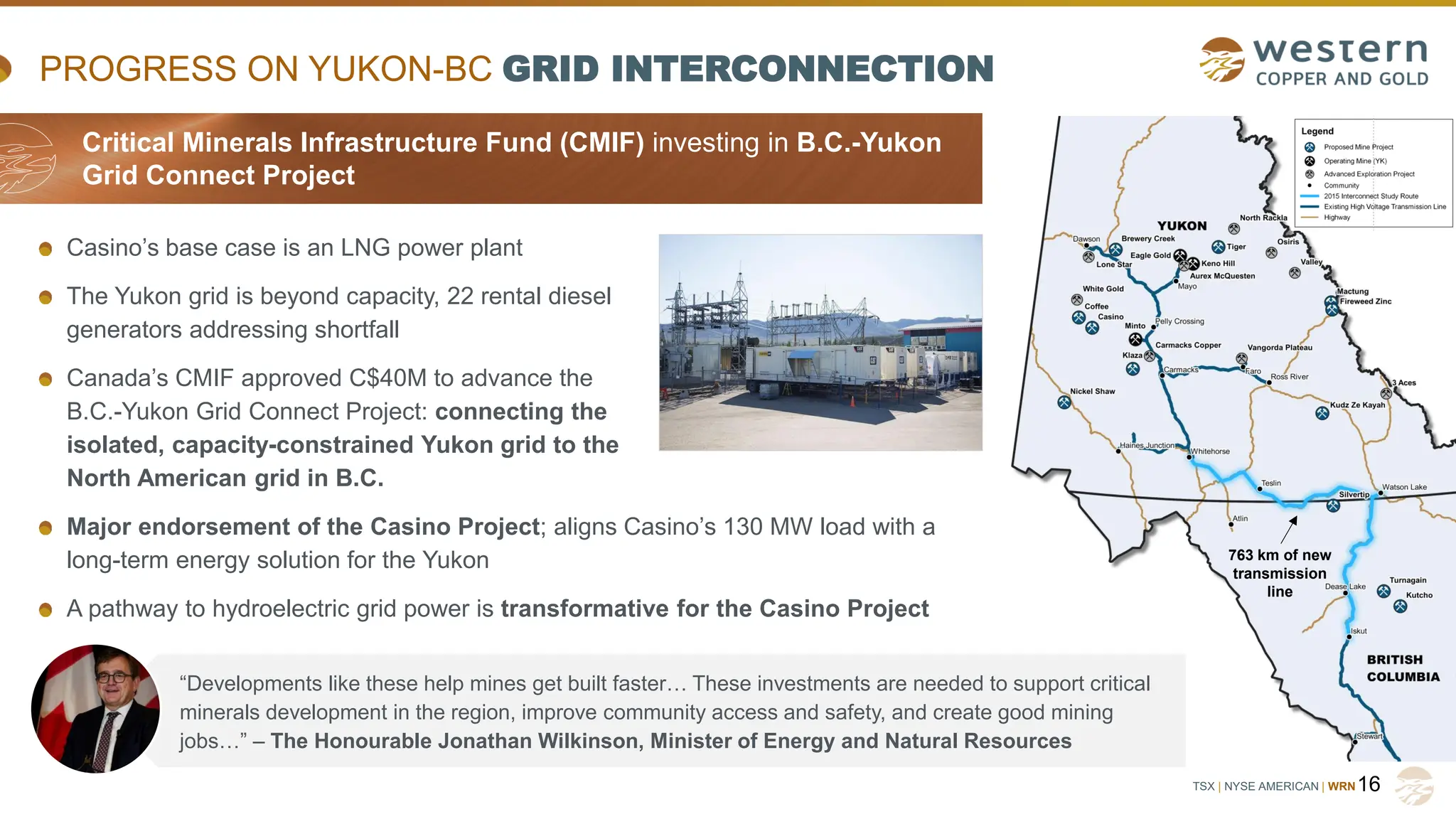

Casino’s base case is an LNG power plant

The Yukon grid is beyond capacity, 22 rental diesel

generators addressing shortfall

Canada’s CMIF approved C$40M to advance the

B.C.-Yukon Grid Connect Project: connecting the

isolated, capacity-constrained Yukon grid to the

North American grid in B.C.

Major endorsement of the Casino Project; aligns Casino’s 130 MW load with a

long-term energy solution for the Yukon

A pathway to hydroelectric grid power is transformative for the Casino Project

PROGRESS ON YUKON-BC GRID INTERCONNECTION

16

763 km of new

transmission

line

“Developments like these help mines get built faster… These investments are needed to support critical

minerals development in the region, improve community access and safety, and create good mining

jobs…” – The Honourable Jonathan Wilkinson, Minister of Energy and Natural Resources

Critical Minerals Infrastructure Fund (CMIF) investing in B.C.-Yukon

Grid Connect Project

17.

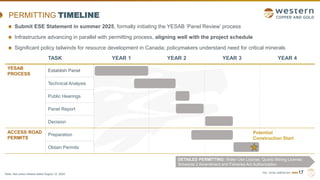

TSX | NYSEAMERICAN | WRN

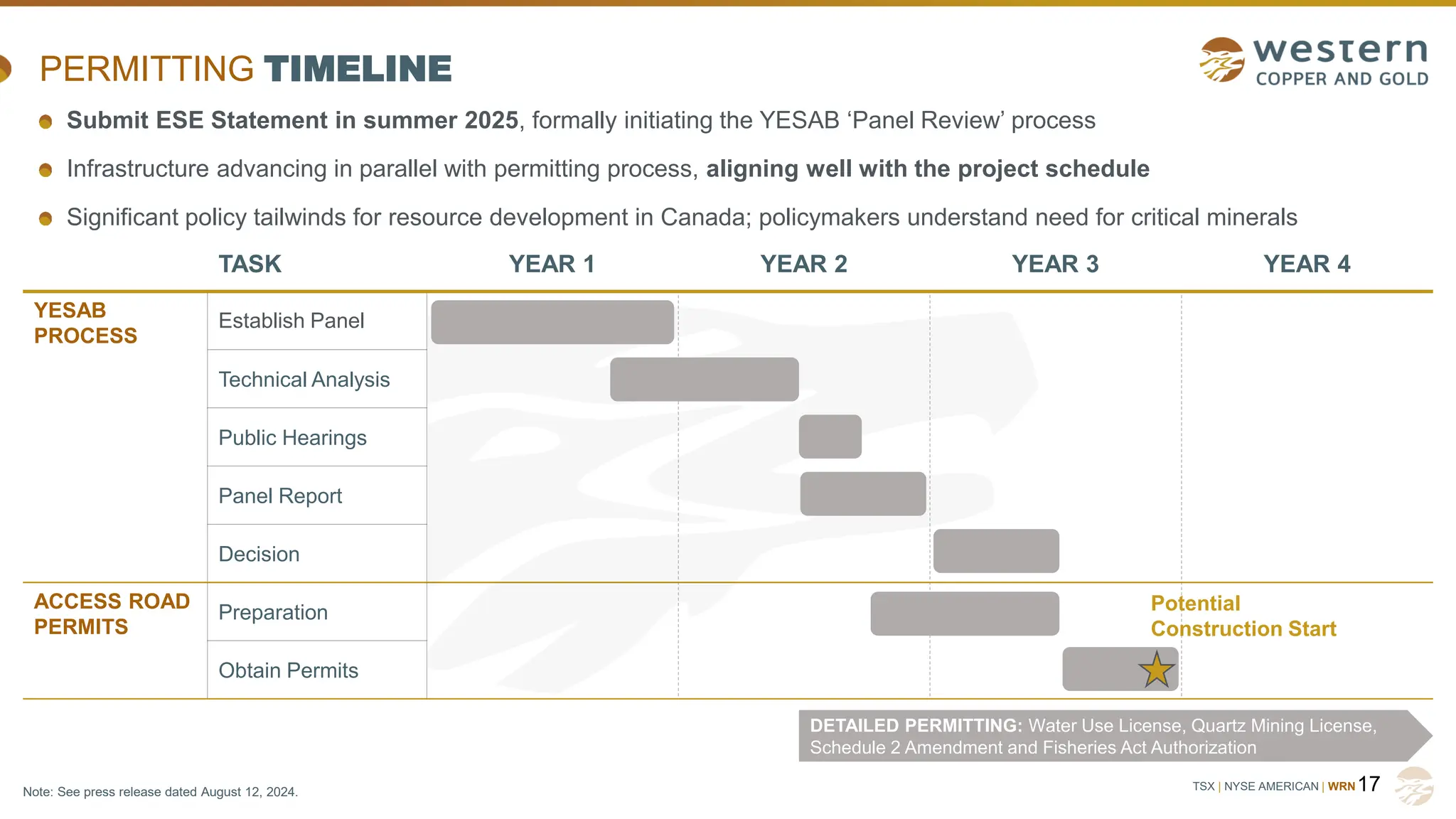

TASK YEAR 1 YEAR 2 YEAR 3 YEAR 4

YESAB

PROCESS

Establish Panel

Technical Analysis

Public Hearings

Panel Report

Decision

ACCESS ROAD

PERMITS

Preparation

Obtain Permits

PERMITTING TIMELINE

17

Potential

Construction Start

DETAILED PERMITTING: Water Use License, Quartz Mining License,

Schedule 2 Amendment and Fisheries Act Authorization

Submit ESE Statement in summer 2025, formally initiating the YESAB ‘Panel Review’ process

Infrastructure advancing in parallel with permitting process, aligning well with the project schedule

Significant policy tailwinds for resource development in Canada; policymakers understand need for critical minerals

Note: See press release dated August 12, 2024.

18.

TSX | NYSEAMERICAN | WRN18

INVESTMENT HIGHLIGHTS

Multi-decade copper and gold resource

High-grade core leads to quick payback

Low strip ratio drives attractive cost profile

Improving infrastructure backdrop through government initiatives

Major endorsements and partnerships

Immense scarcity value of similar projects

TSX | NYSEAMERICAN | WRN

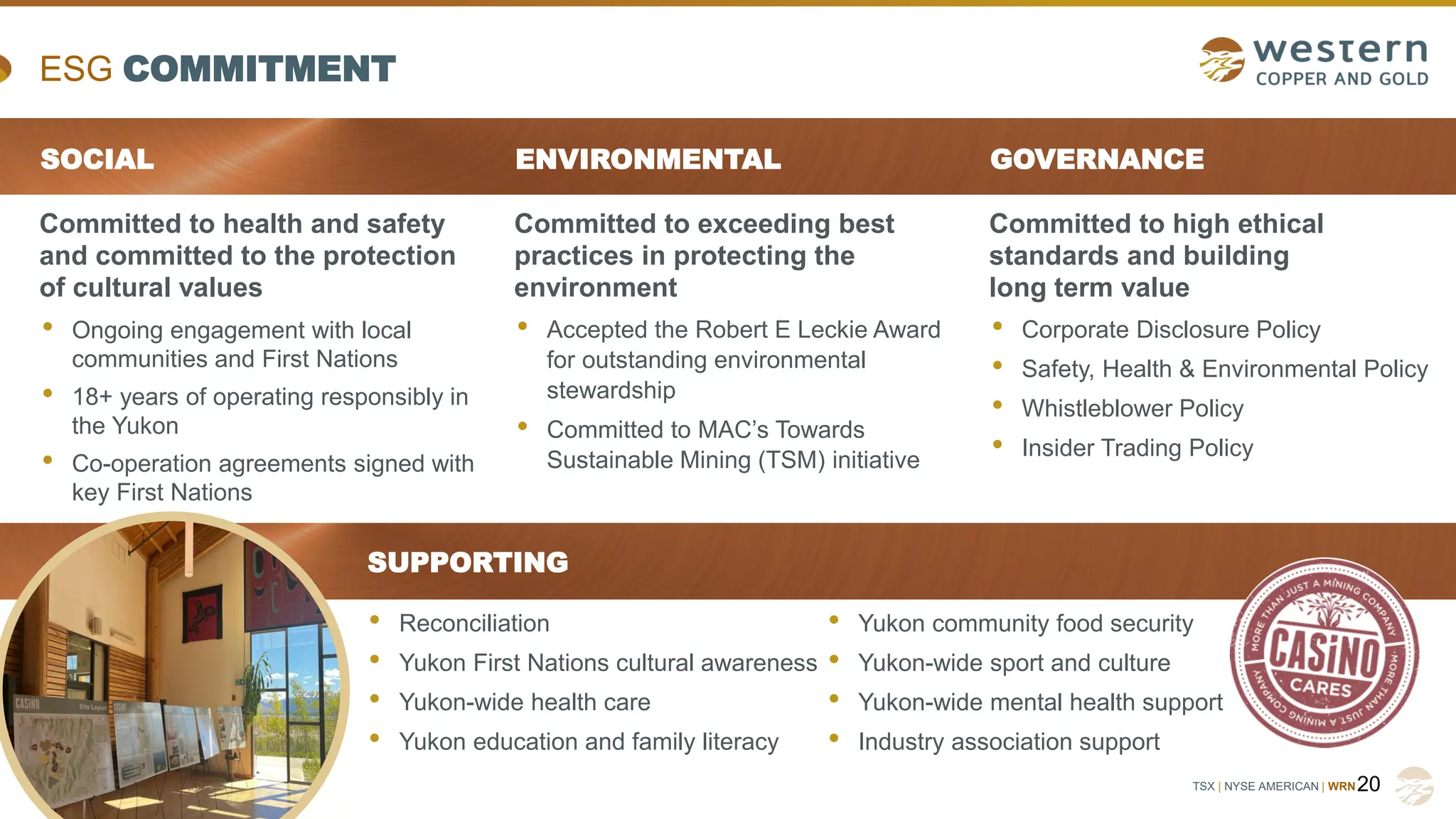

ESG COMMITMENT

20

Committed to health and safety

and committed to the protection

of cultural values

• Ongoing engagement with local

communities and First Nations

• 18+ years of operating responsibly in

the Yukon

• Co-operation agreements signed with

key First Nations

SOCIAL ENVIRONMENTAL

Committed to exceeding best

practices in protecting the

environment

• Accepted the Robert E Leckie Award

for outstanding environmental

stewardship

• Committed to MAC’s Towards

Sustainable Mining (TSM) initiative

Committed to high ethical

standards and building

long term value

• Corporate Disclosure Policy

• Safety, Health & Environmental Policy

• Whistleblower Policy

• Insider Trading Policy

GOVERNANCE

SUPPORTING

• Yukon community food security

• Yukon-wide sport and culture

• Yukon-wide mental health support

• Industry association support

• Reconciliation

• Yukon First Nations cultural awareness

• Yukon-wide health care

• Yukon education and family literacy

21.

TSX | NYSEAMERICAN | WRN

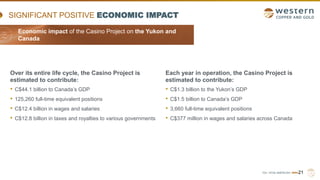

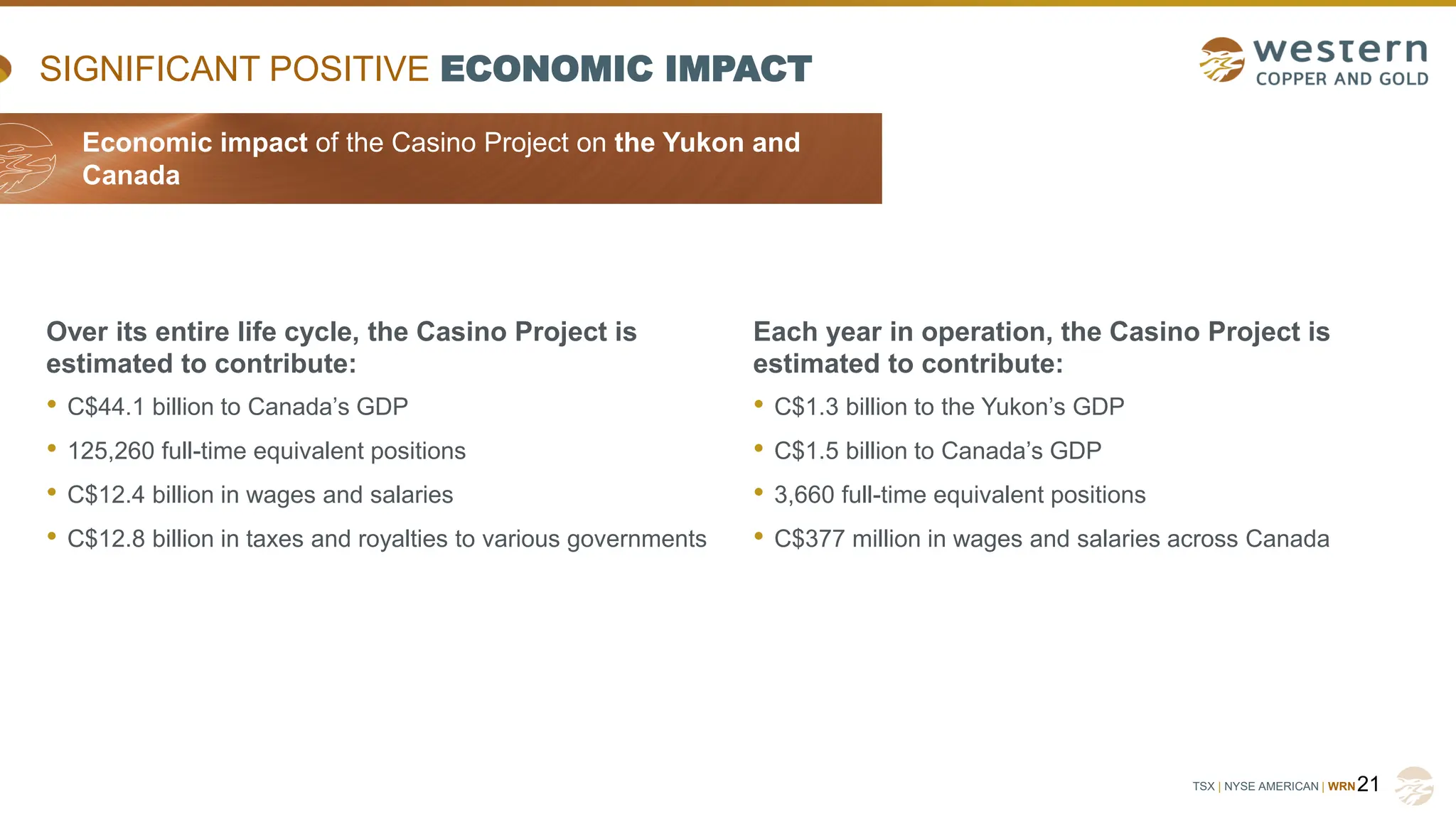

SIGNIFICANT POSITIVE ECONOMIC IMPACT

Over its entire life cycle, the Casino Project is

estimated to contribute:

• C$44.1 billion to Canada’s GDP

• 125,260 full-time equivalent positions

• C$12.4 billion in wages and salaries

• C$12.8 billion in taxes and royalties to various governments

21

Each year in operation, the Casino Project is

estimated to contribute:

• C$1.3 billion to the Yukon’s GDP

• C$1.5 billion to Canada’s GDP

• 3,660 full-time equivalent positions

• C$377 million in wages and salaries across Canada

Economic Impact Casino Project

on the Yukon and Canada

Economic impact of the Casino Project on the Yukon and

Canada

22.

TSX | NYSEAMERICAN | WRN

x

157

144

--

20

40

60

80

100

120

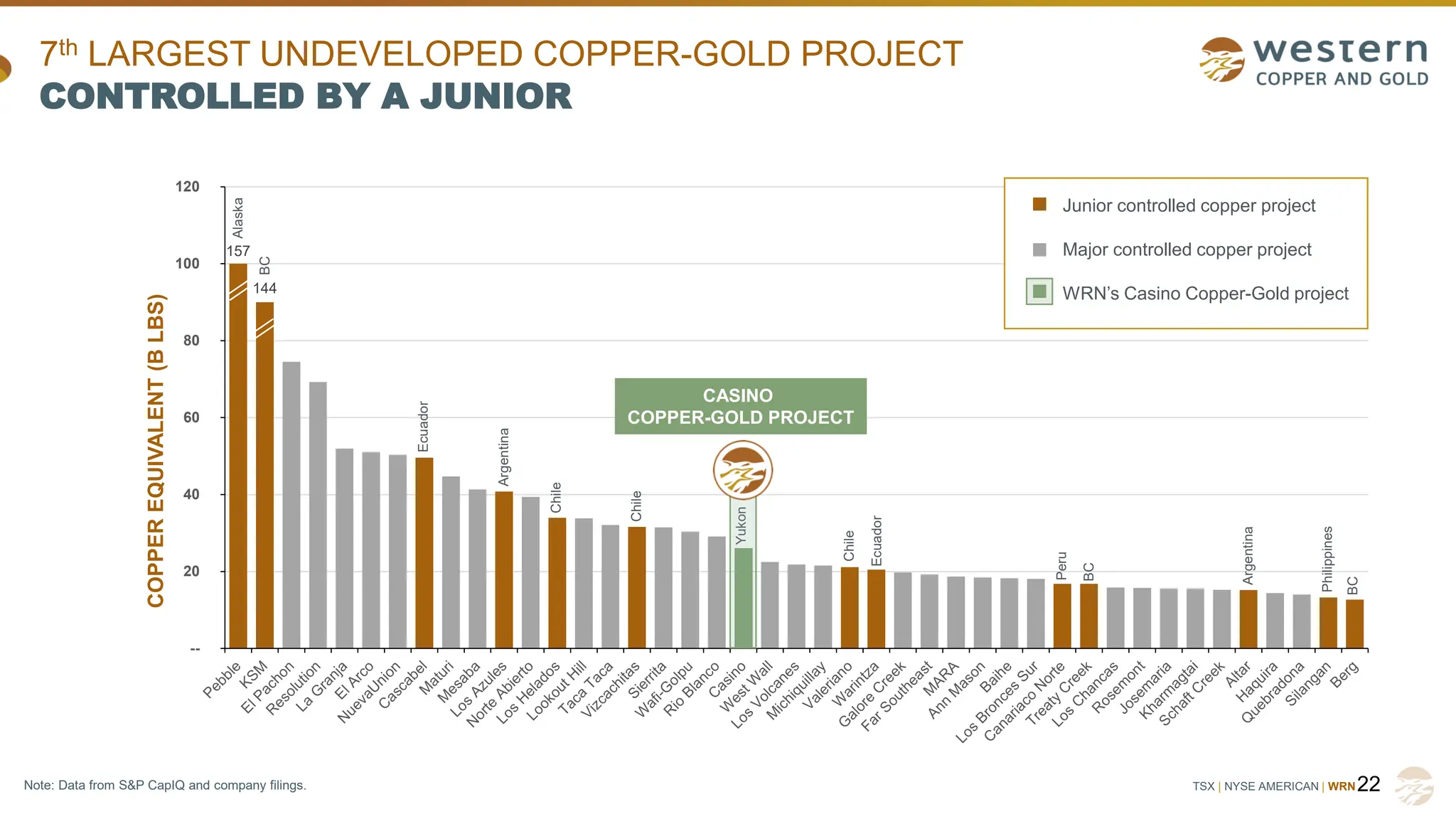

7th LARGEST UNDEVELOPED COPPER-GOLD PROJECT

CONTROLLED BY A JUNIOR

22

CASINO

COPPER-GOLD PROJECT

Junior controlled copper project

Major controlled copper project

WRN’s Casino Copper-Gold project

Ecuador

Argentina

Chile

Ecuador

Peru

Yukon

Alaska

BC

BC

Philippines

BC

Argentina

COPPER

EQUIVALENT

(B

LBS)

Chile

Chile

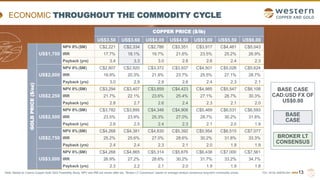

Note: Data from S&P CapIQ and company filings.

23.

TSX | NYSEAMERICAN | WRN

x

23

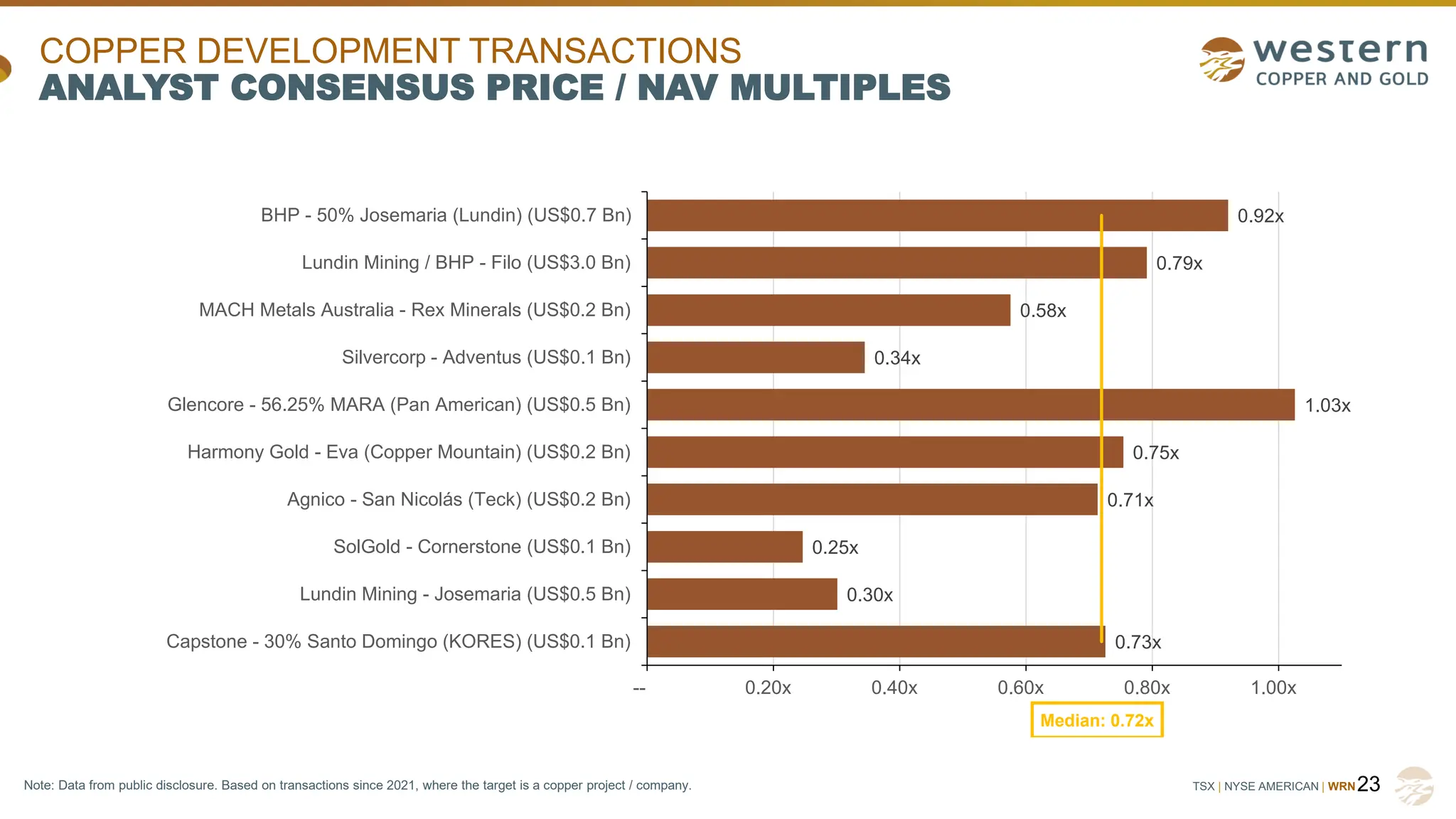

COPPER DEVELOPMENT TRANSACTIONS

ANALYST CONSENSUS PRICE / NAV MULTIPLES

0.92x

0.79x

0.58x

0.34x

1.03x

0.75x

0.71x

0.25x

0.30x

0.73x

-- 0.20x 0.40x 0.60x 0.80x 1.00x

BHP - 50% Josemaria (Lundin) (US$0.7 Bn)

Lundin Mining / BHP - Filo (US$3.0 Bn)

MACH Metals Australia - Rex Minerals (US$0.2 Bn)

Silvercorp - Adventus (US$0.1 Bn)

Glencore - 56.25% MARA (Pan American) (US$0.5 Bn)

Harmony Gold - Eva (Copper Mountain) (US$0.2 Bn)

Agnico - San Nicolás (Teck) (US$0.2 Bn)

SolGold - Cornerstone (US$0.1 Bn)

Lundin Mining - Josemaria (US$0.5 Bn)

Capstone - 30% Santo Domingo (KORES) (US$0.1 Bn)

Median: 0.72x

Note: Data from public disclosure. Based on transactions since 2021, where the target is a copper project / company.

24.

TSX | NYSEAMERICAN | WRN24

FEASIBILITY STUDY CAPITAL COSTS

PROJECTED CAPITAL COSTS

PROCESS PLANT &

INFRASTRUCTURE

Project Directs (Including Freight) C$2,116

Project Indirects C$431

Contingency C$369

Subtotal C$2,916

MINE Mine Equipment C$433

Mine Pre-production C$228

Subtotal C$661

Owners Costs C$41

SUSTAINING & TOTAL Total Initial Capital C$3,618

Total Sustaining Capital C$751

Total Life-Of-Mine Capital C$4,369

Note: Based on Casino Copper-Gold 2022 Feasibility Study at base case metal prices. See “Notes” in Appendix.

25.

TSX | NYSEAMERICAN | WRN

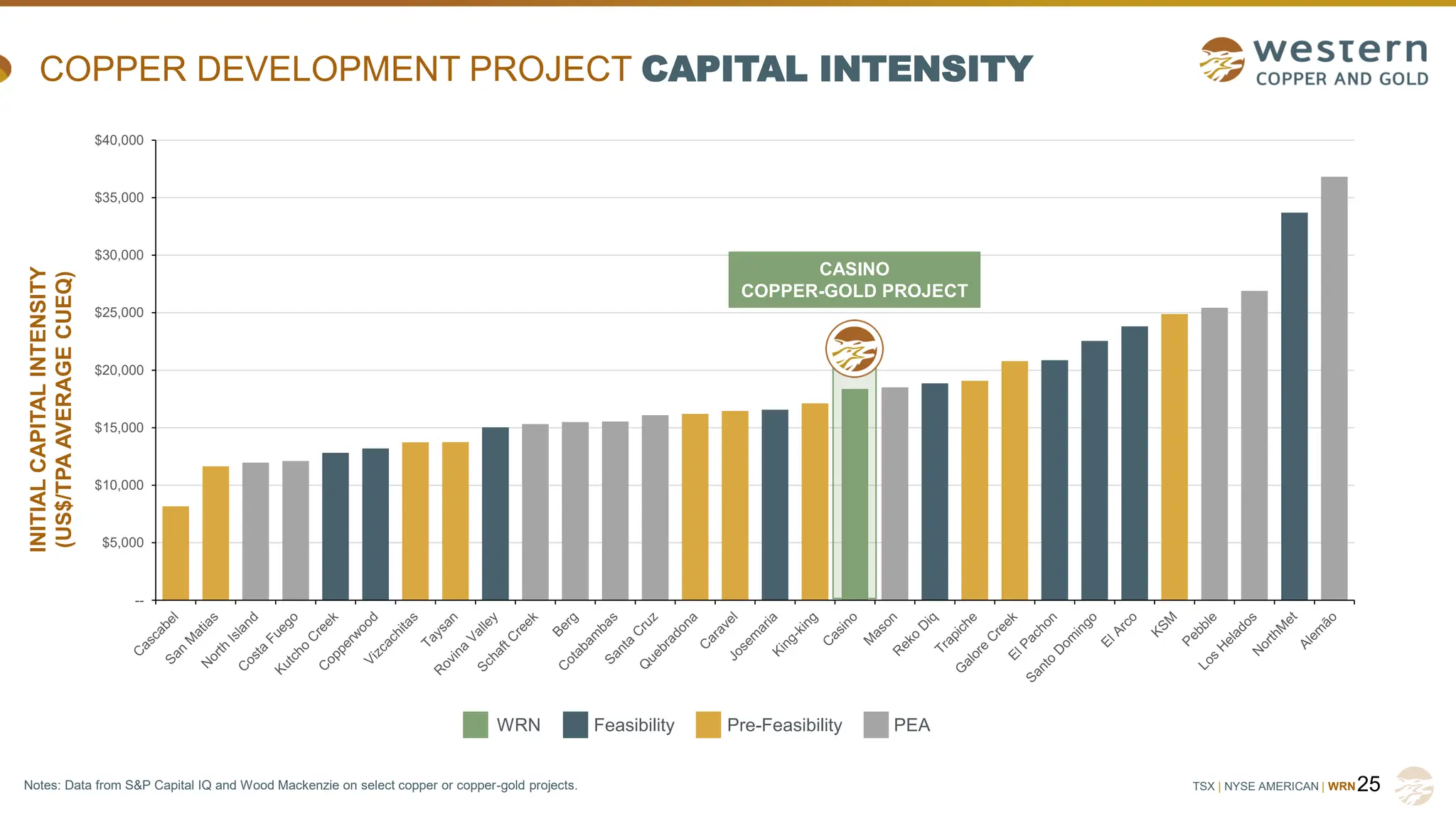

--

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

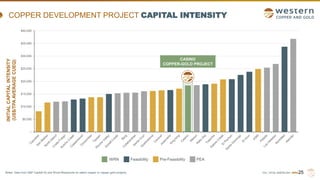

COPPER DEVELOPMENT PROJECT CAPITAL INTENSITY

25

CASINO

COPPER-GOLD PROJECT

INITIAL

CAPITAL

INTENSITY

(US$/TPA

AVERAGE

CUEQ)

WRN Feasibility Pre-Feasibility PEA

Notes: Data from S&P Capital IQ and Wood Mackenzie on select copper or copper-gold projects.

26.

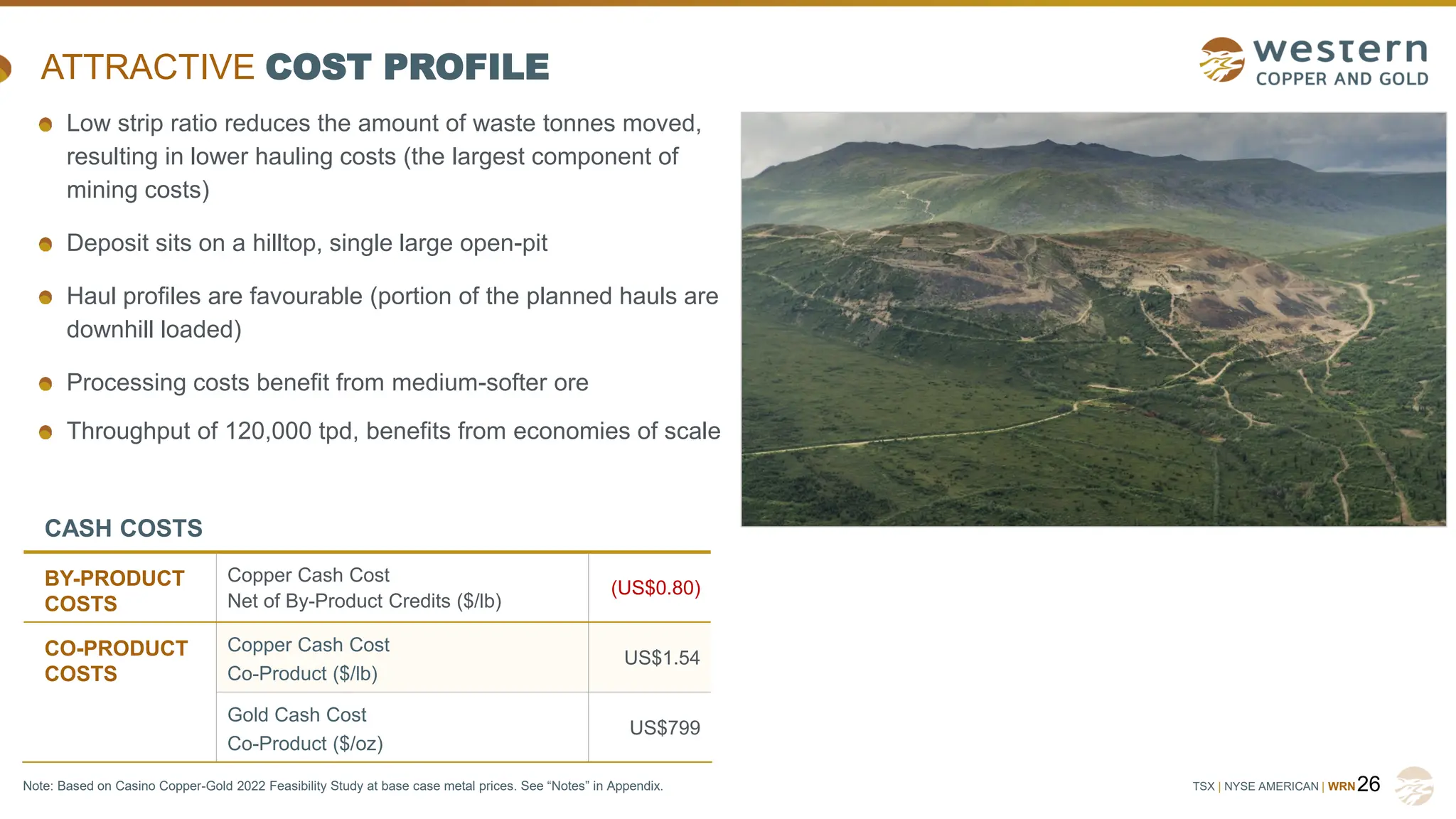

TSX | NYSEAMERICAN | WRN26

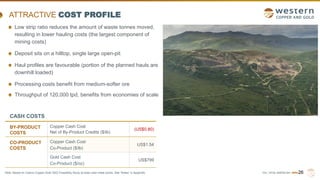

ATTRACTIVE COST PROFILE

CASH COSTS

BY-PRODUCT

COSTS

Copper Cash Cost

Net of By-Product Credits ($/lb)

(US$0.80)

CO-PRODUCT

COSTS

Copper Cash Cost

Co-Product ($/lb)

US$1.54

Gold Cash Cost

Co-Product ($/oz)

US$799

Low strip ratio reduces the amount of waste tonnes moved,

resulting in lower hauling costs (the largest component of

mining costs)

Deposit sits on a hilltop, single large open-pit

Haul profiles are favourable (portion of the planned hauls are

downhill loaded)

Processing costs benefit from medium-softer ore

Throughput of 120,000 tpd, benefits from economies of scale

Note: Based on Casino Copper-Gold 2022 Feasibility Study at base case metal prices. See “Notes” in Appendix.

27.

TSX | NYSEAMERICAN | WRN

FEASIBILITY STUDY OPERATING COST

27

Note: Based on Casino Copper-Gold 2022 Feasibility Study. See “Notes” in Appendix.

UNIT COSTS LIFE-OF-MINE

MILLING

OPERATION

Milling ($/t ore milled) C$6.42

Mining ($/t ore milled) C$4.28

General &

Administrative

($/t ore milled) C$0.46

Total ($/t ore milled) C$11.16

HEAP LEACH

OPERATION

Heap Leach Operation ($/t leached) C$1.93

ADR/SART ($/t leached) C$4.80

Total ($/t leached) C$6.73

28.

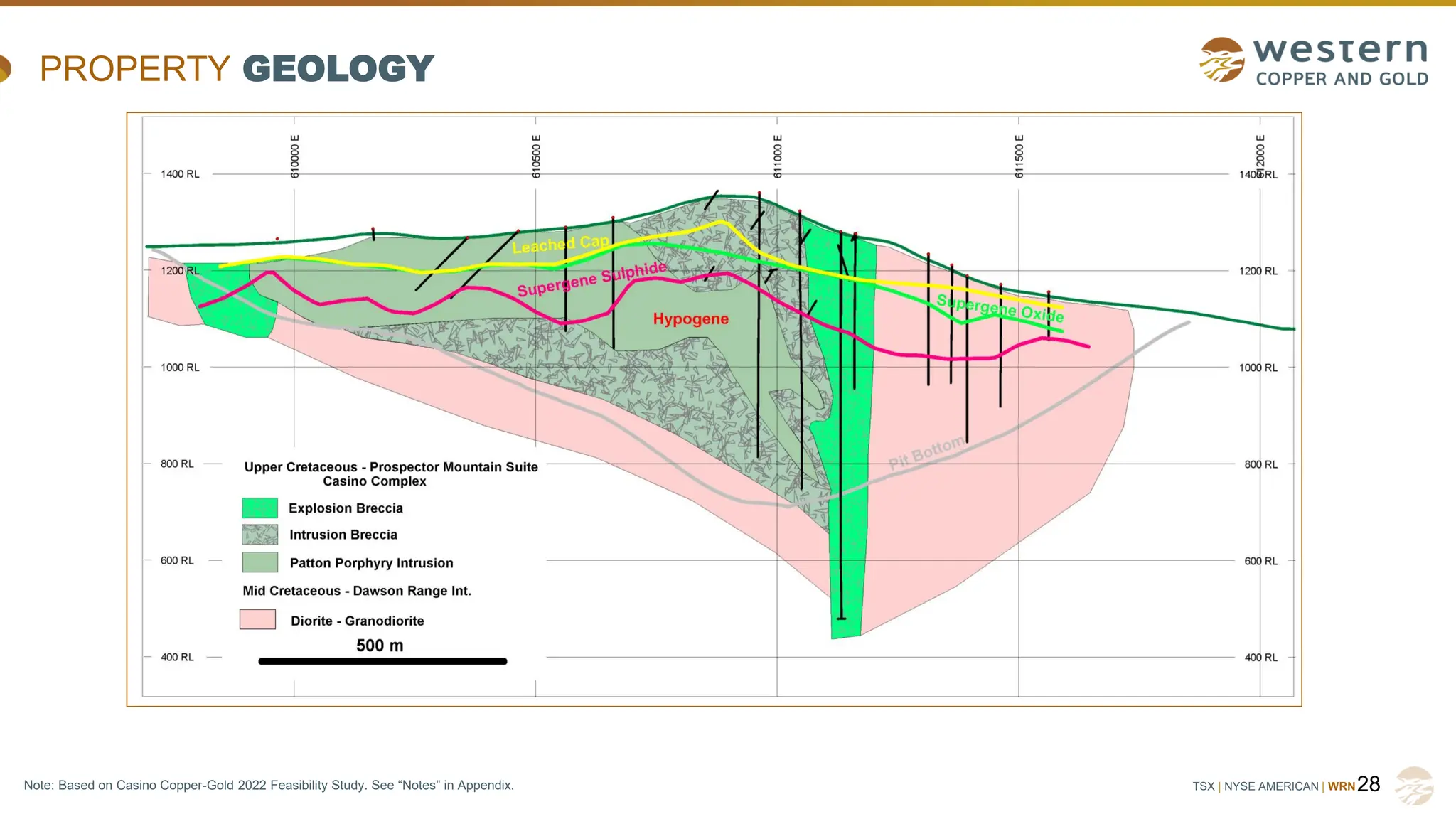

TSX | NYSEAMERICAN | WRN

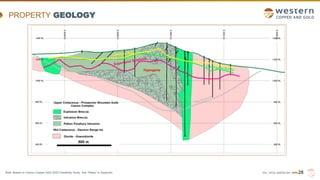

PROPERTY GEOLOGY

28

Note: Based on Casino Copper-Gold 2022 Feasibility Study. See “Notes” in Appendix.

29.

TSX | NYSEAMERICAN | WRN

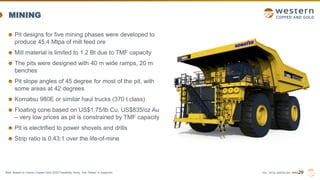

MINING

Pit designs for five mining phases were developed to

produce 45.4 Mtpa of mill feed ore

Mill material is limited to 1.2 Bt due to TMF capacity

The pits were designed with 40 m wide ramps, 20 m

benches

Pit slope angles of 45 degree for most of the pit, with

some areas at 42 degrees

Komatsu 980E or similar haul trucks (370 t class)

Floating cone based on US$1.75/lb Cu, US$835/oz Au

– very low prices as pit is constrained by TMF capacity

Pit is electrified to power shovels and drills

Strip ratio is 0.43:1 over the life-of-mine

29

Note: Based on Casino Copper-Gold 2022 Feasibility Study. See “Notes” in Appendix.

30.

TSX | NYSEAMERICAN | WRN

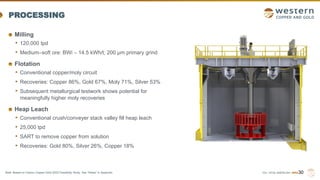

PROCESSING

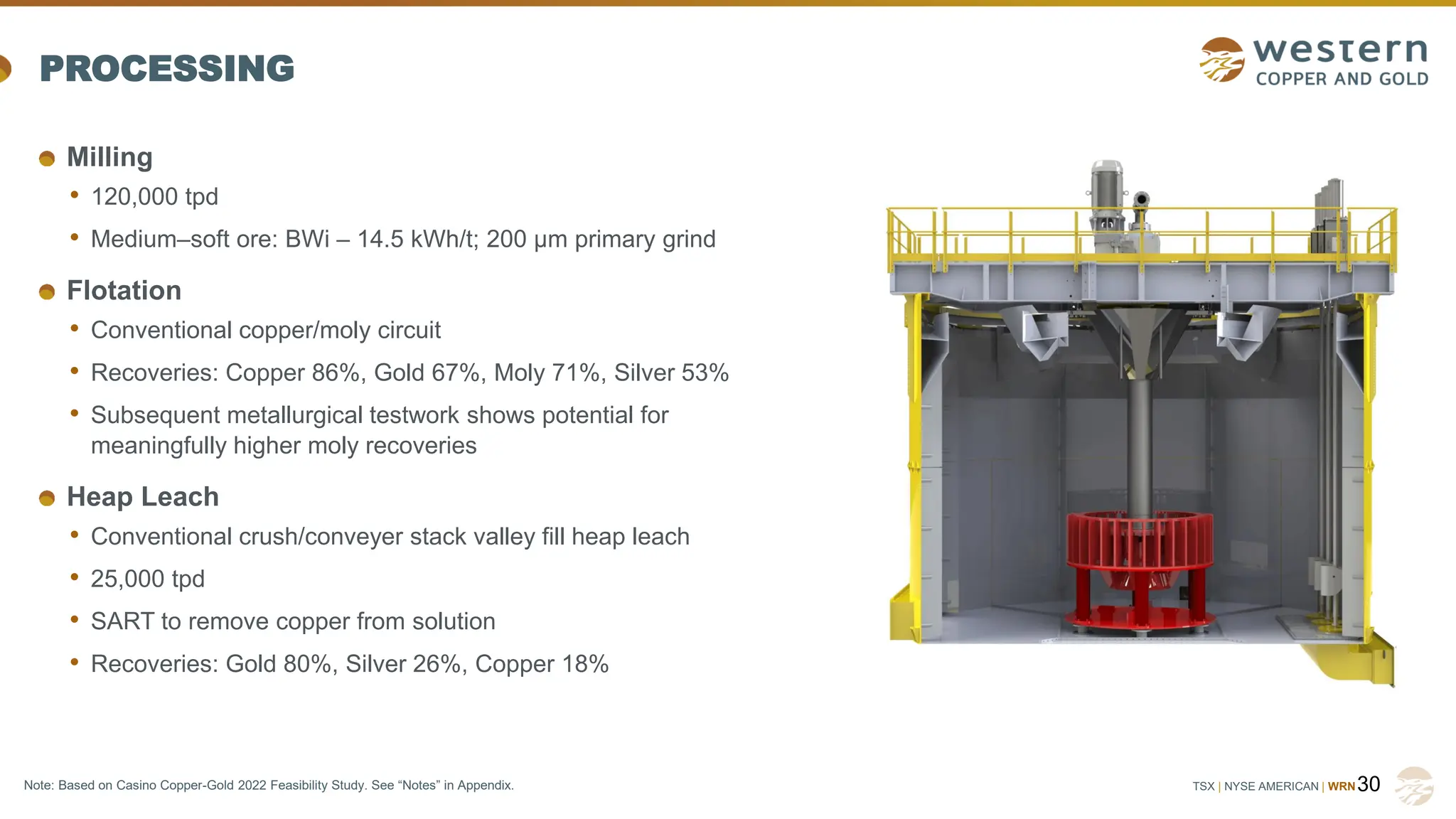

Milling

• 120,000 tpd

• Medium–soft ore: BWi – 14.5 kWh/t; 200 µm primary grind

Flotation

• Conventional copper/moly circuit

• Recoveries: Copper 86%, Gold 67%, Moly 71%, Silver 53%

• Subsequent metallurgical testwork shows potential for

meaningfully higher moly recoveries

Heap Leach

• Conventional crush/conveyer stack valley fill heap leach

• 25,000 tpd

• SART to remove copper from solution

• Recoveries: Gold 80%, Silver 26%, Copper 18%

30

Note: Based on Casino Copper-Gold 2022 Feasibility Study. See “Notes” in Appendix.

TSX | NYSEAMERICAN | WRN

NOTES

Technical report entitled “Casino Copper-Gold Project, Form 43-101 F1

Technical Report Feasibility Study” dated June 13, 2022, a copy of which is

available on the Company's website at www.westerncopperandgold.com.

Prepared by: Daniel Roth, P.Eng.; Laurie Tahija, MMSA-QP; Patrick Dugan,

P.E.; Mike Hester, F Aus IMM; John M. Marek, P.Eng.; Carl Schulze, P.Geo.;

Daniel Friedman, P.Eng; Scott Weston, P.Geo; each of whom is a qualified

person pursuant to National Instrument 43-101 ("Qualified Person")

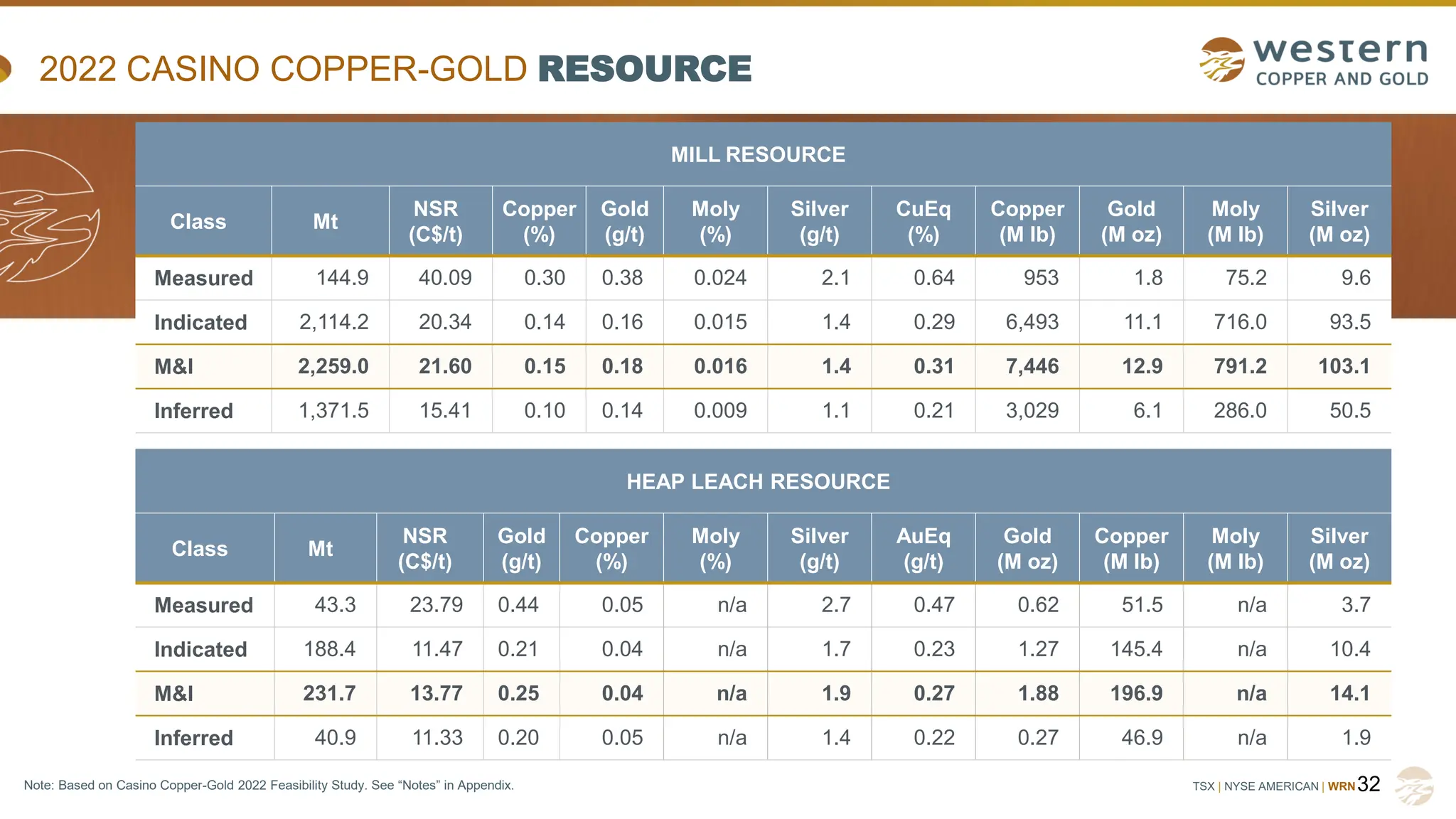

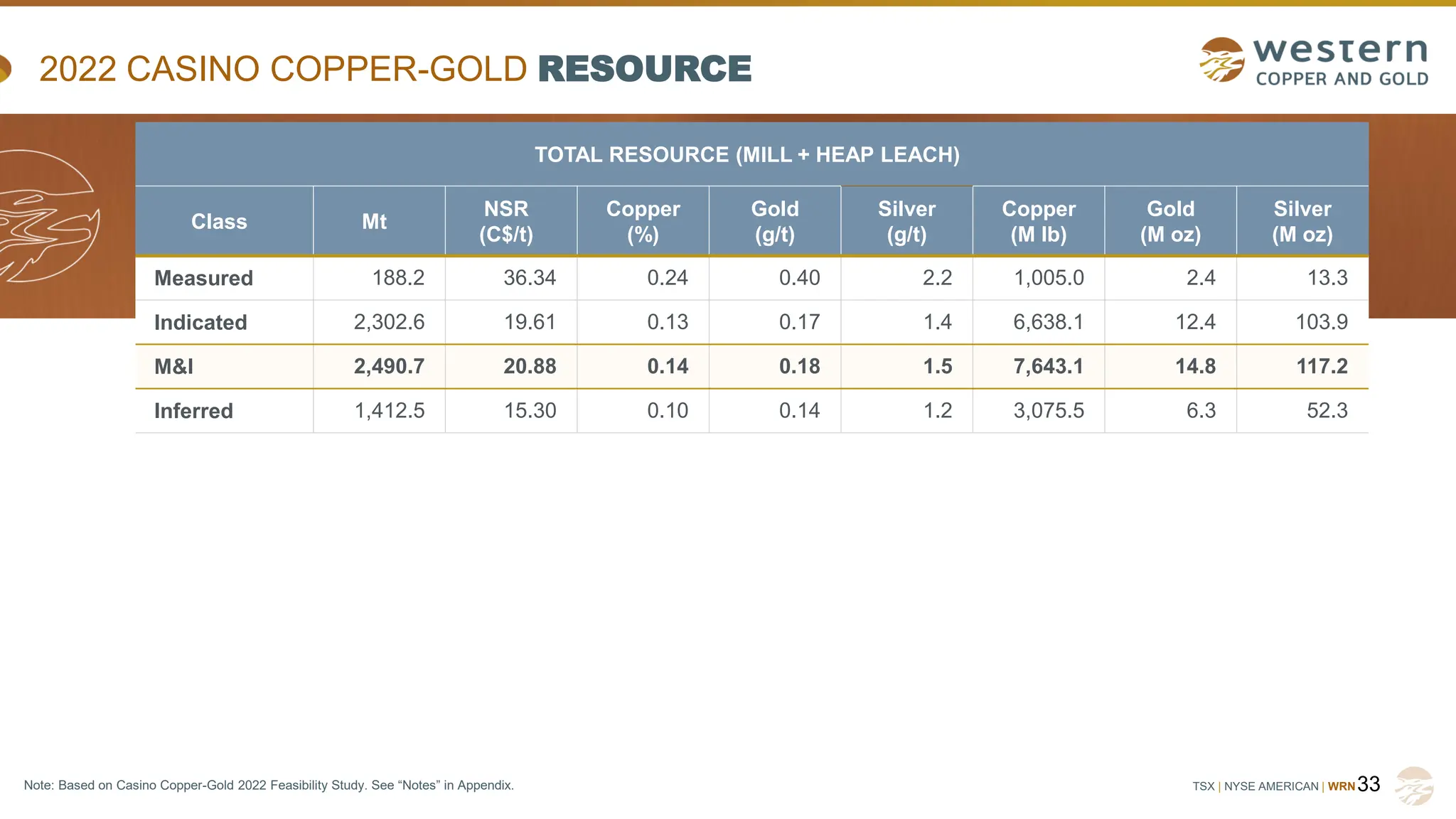

Mineral Resources

• The Mineral Resources have an effective date of 29 April 2022 and

the estimate was prepared using the definitions in CIM Definition Standards

(10 May 2014).

• All figures are rounded to reflect the relative accuracy of the estimate and

therefore numbers may not appear to add precisely.

• Mineral Resources that are not Mineral Reserves do not have demonstrated

economic viability.

• Mineral Resources for leach material are based on prices of US$3.50/lb

copper, US$1,650/oz gold and US$22/oz silver

• Mineral Resources for mill material are based on prices of US$3.50/lb

copper, US$1,650/oz gold, US$22/oz silver, and US$12.00/lb moly.

• Mineral Resources are based on NSR cut-off of C$6.61/t for leach material

and C$6.11/t for mill material.

• NSR value for leach material is as follows:

- NSR (C$/t) = $15.21 x copper (%) + $50.51 x gold (g/t) + $0.210 x silver (g/t), based

on copper recovery of 18%, gold recovery of 80% and silver recovery of 26%.

34

“Casino Copper-Gold Feasibility Study” • NSR value for hypogene sulphide mill material is:

- NSR (C$/t) = $73.81 x copper (%) + $41.16 x gold (g/t) + $213.78 x moly (%) +

0.386 x silver (g/t), based on recoveries of 92.2% copper, 66% gold, 50% silver

and 78.6% moly.

• NSR value for supergene mill material is:

- NSR (C$/t) = $80.06 x recoverable copper (%) + $43.03 x gold (g/t) + $142.11 x

moly (%) + 0.464 x silver (g/t), based on recoveries of 69% gold, 60% silver and

52.3% moly. Recoverable copper = 0.94 x (total copper – soluble copper).

• Mineral Resources are reported in relation to a conceptual constraining

pit shell in order to demonstrate reasonable prospects for eventual

economic extraction, as required by the definition of Mineral Resource in

NI 43-101; mineralization lying outside of the pit shell is excluded from

the Mineral Resource.

• AuEq and CuEq values are based on prices of US$3.50/lb copper,

US$1,650/oz gold, US$22/oz silver, and US$12.00/lb moly, and account

for all metal recoveries and smelting/refining charges.

• The NSR calculations also account for smelting and refining charges and

payables.

35.

TSX | NYSEAMERICAN | WRN

NOTES

Mineral Reserve

• The Mineral Reserve estimate has an effective date of June 13, 2022 and

was prepared using the CIM Definition Standards (10 May 2014).

• Columns may not sum exactly due to rounding.

• Mineral Reserves are based on commodity prices of US$3.25/lb Cu,

US$1,550/oz Au, US$12.00/lb Mo, and US$22.00/oz Ag.

• Mineral Reserves amenable to milling are based on NSR cutoffs that vary by

time period to balance mine and plant production capacities. They range from

a low of $6.11/t to a high of $25.00/t.

• NSR value for supergene (SOX and SUS) mill material is

- NSR (C$/t) = $73.63 x recoverable copper (%) + $40.41 x gold (g/t) + $142.11 x moly (%)

+ 0.464 x silver (g/t), based on recoveries of 69% gold, 52.3% molybdenum and 60%

silver. Recoverable copper = 0.94 x (total copper – soluble copper).

• NSR value for hypogene (HYP) mill material is

- NSR (C$/t) = $67.88 x copper (%) + $38.66 x gold (g/t) + $213.78 x moly (%) + $0.386 x

silver (g/t), based on recoveries of 92.2% copper, 66% gold, 78.6% molybdenum and 50%

silver.

• Mineral Reserves amenable to heap leaching are based on an NSR cutoff of

$6.61/t.

35

“Casino Copper-Gold Feasibility Study”

Other technical information in this presentation:

• NSR value for leach material is

- NSR (C$/t) = $14.05 x copper (%) + $47.44 x gold (g/t) + $0.210 x silver (g/t), based

on recoveries of 18% copper, 80% gold and 26% silver.

• AuEq and CuEq values are based on prices of US$ 3.25/lb Cu,

US$1,550/oz Au, US$12.00/lb Mo, and US$22.00/oz Ag, and account for

all metal recoveries and smelting/refining charges.

• The NSR calculations also account for smelter/refinery treatment charges

and payables.

Technical information regarding the Casino Copper-Gold Project contained

in this presentation is based on the Casino Copper-Gold 2022 FS prepared

by or under the supervision of the Qualified Persons noted previously.

Copper equivalent calculations in this presentation, not associated with the

Casino mineral resource or reserve, are based on: US$3.60/lb copper;

US$1,700/oz gold; US$14/lb molybdenum; and US$22/oz silver with no

accounting for metallurgical recovery.