Downloaded 103 times

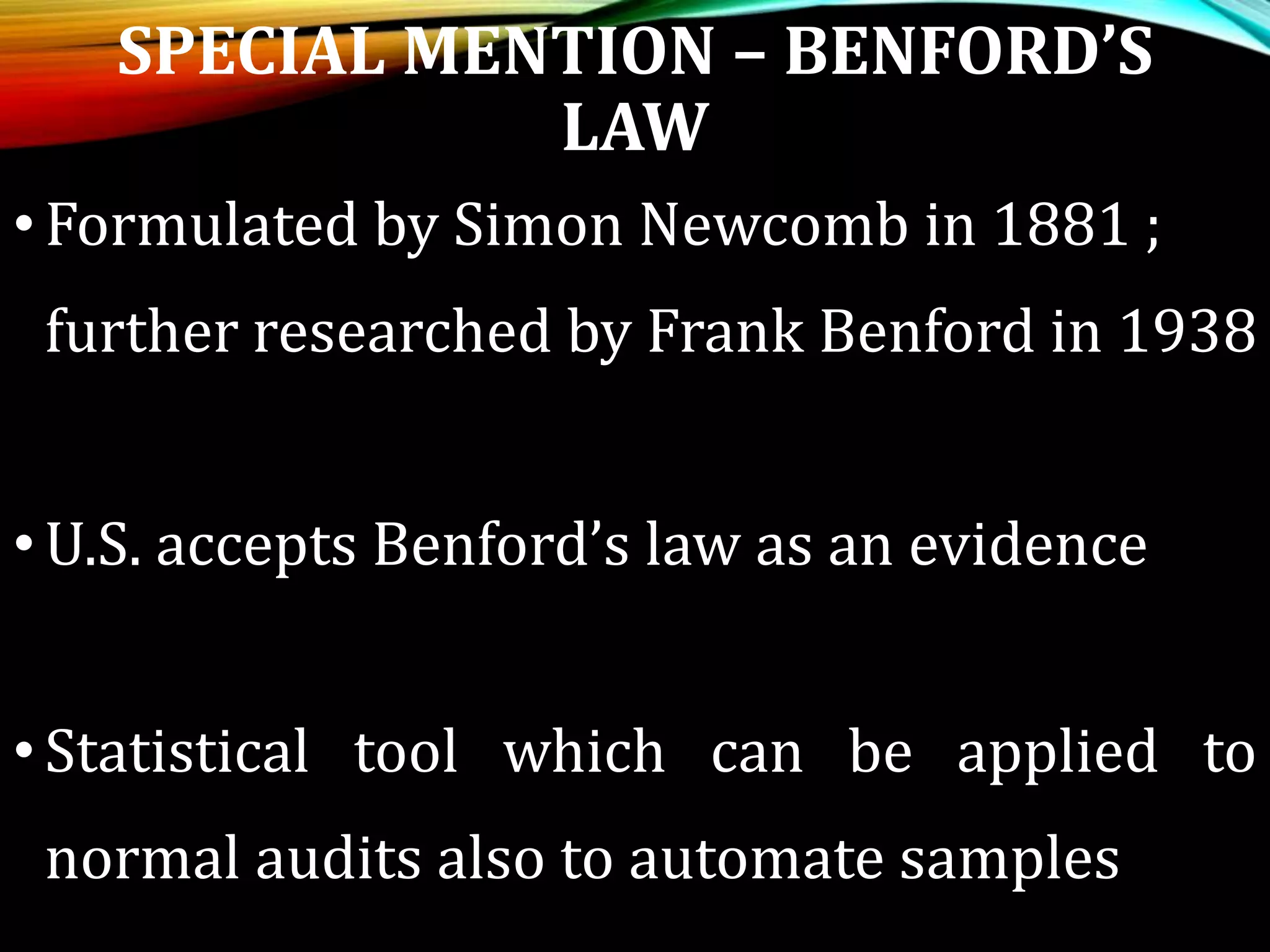

This document discusses data mining and forensic auditing. It defines data mining as using computer techniques to analyze large amounts of data to identify patterns and relationships. Data mining can help auditors identify suspicious transactions by analyzing patterns in areas like computer usage, purchases, and employee data. Forensic auditing investigates potential fraud and uses accounting skills and tools to analyze financial information for legal cases. The document outlines different types of fraud, profiles of potential fraudsters, and specialized tools and techniques auditors can use to detect fraud, such as Benford's Law and other Excel functions.

Overview of data mining and forensic audit concepts by Dhruv Seth.

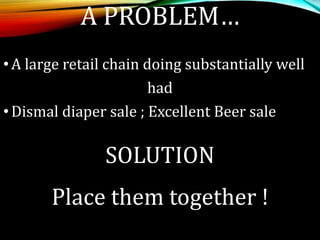

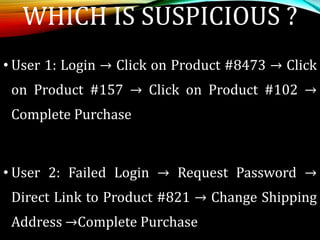

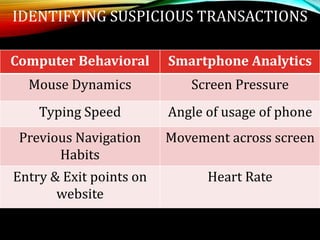

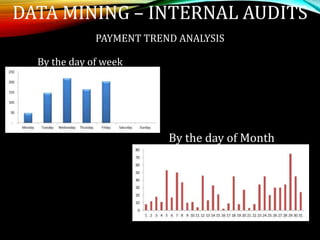

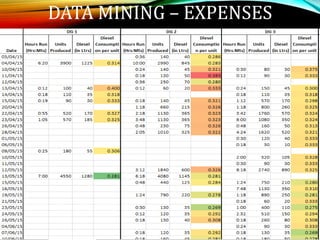

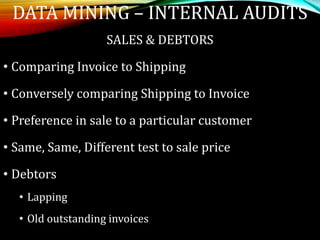

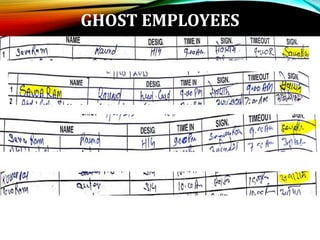

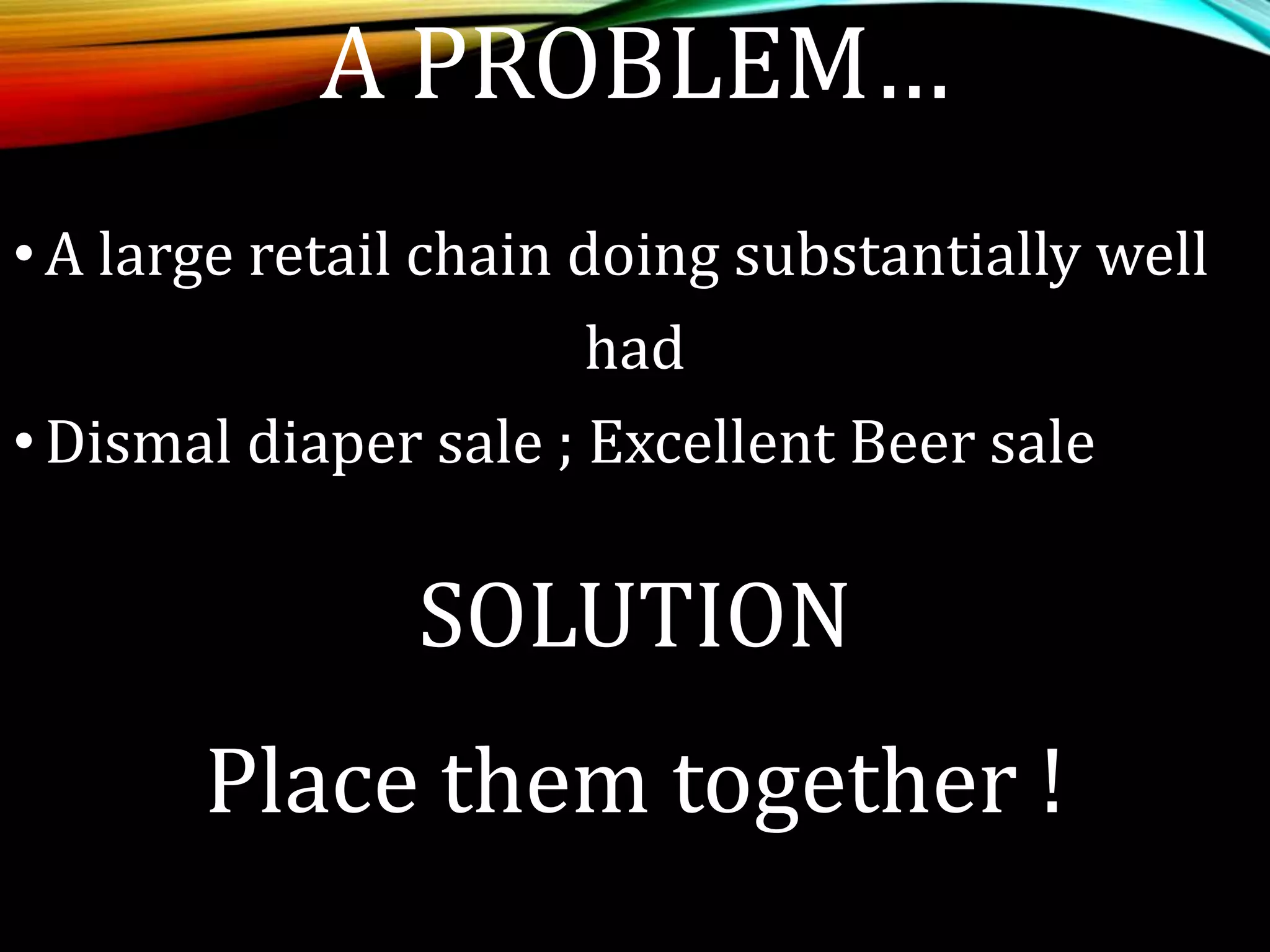

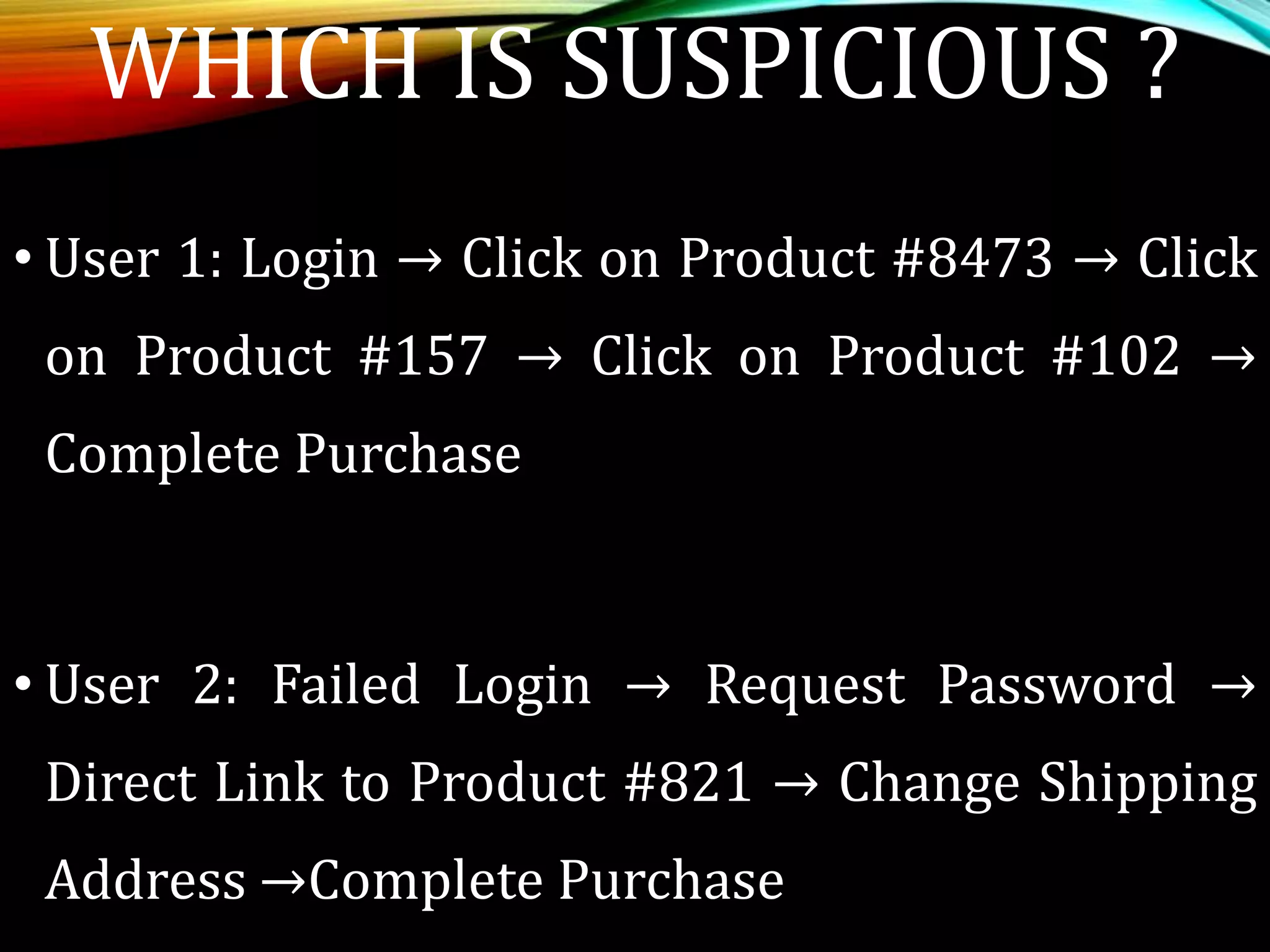

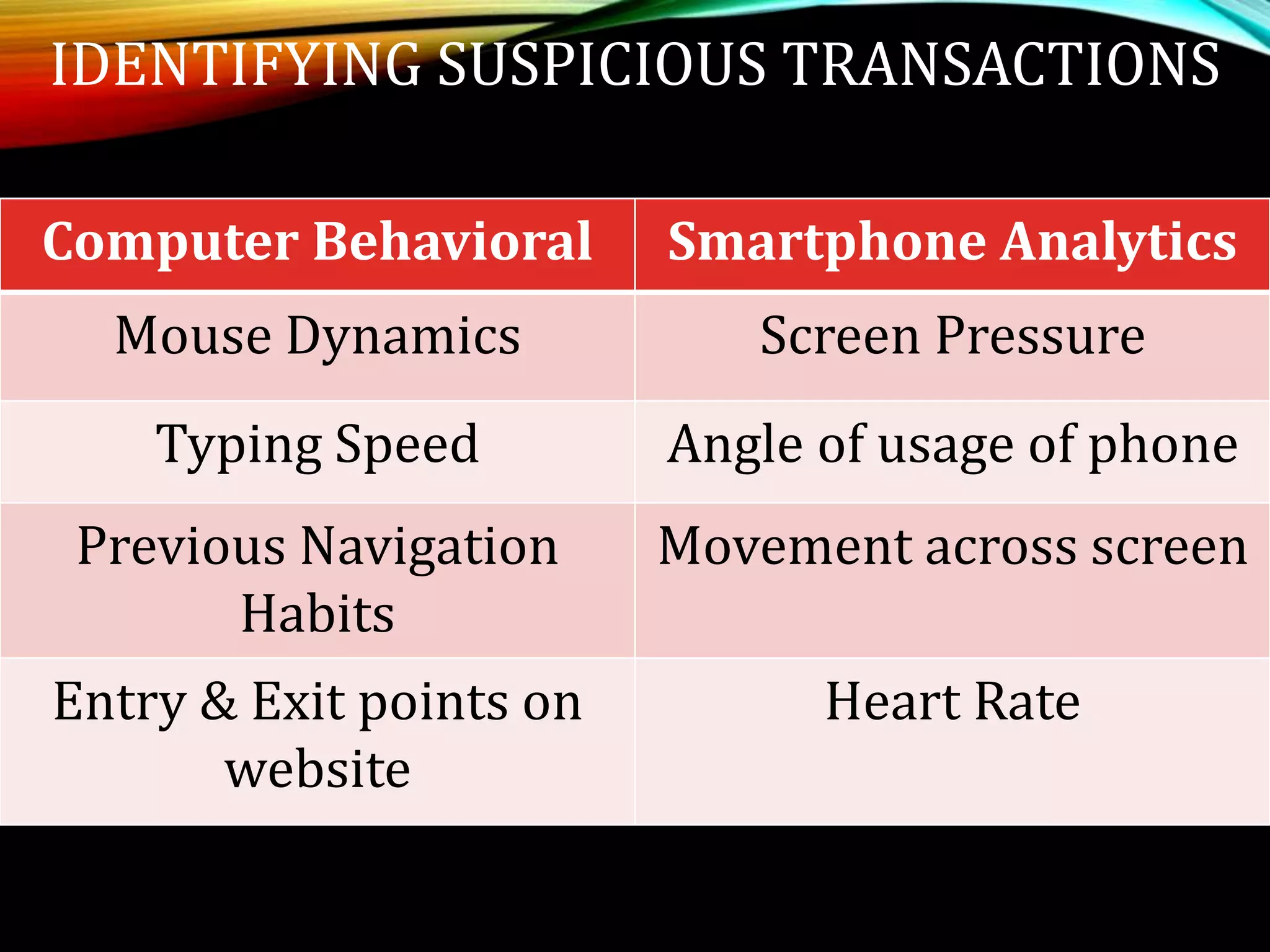

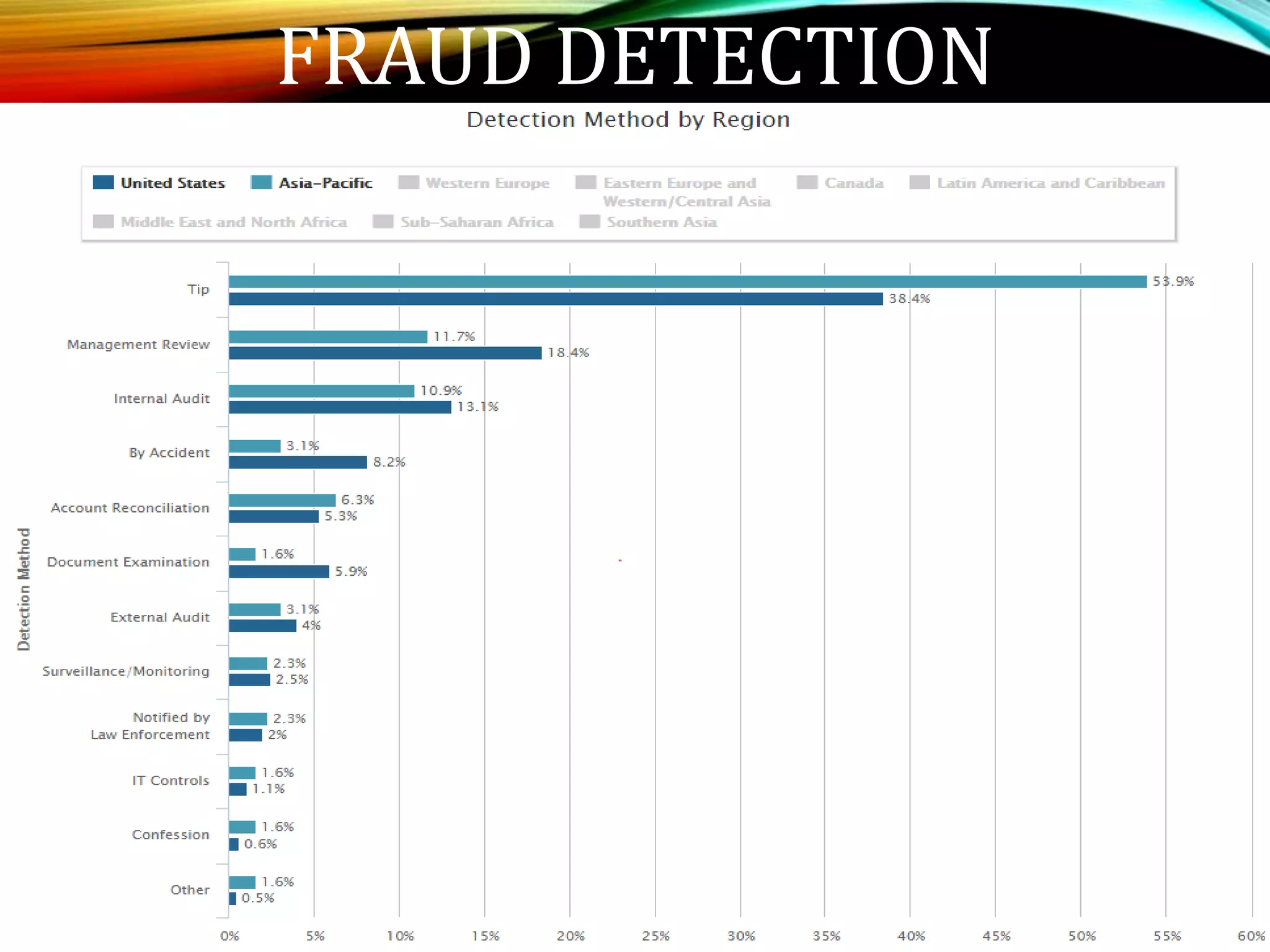

Discusses unusual data sales patterns and user behavior that may indicate suspicious transactions.

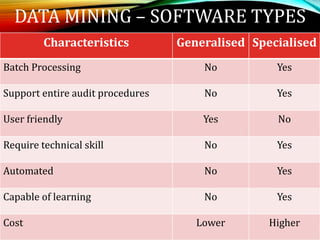

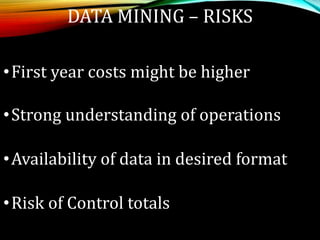

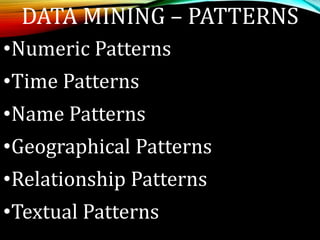

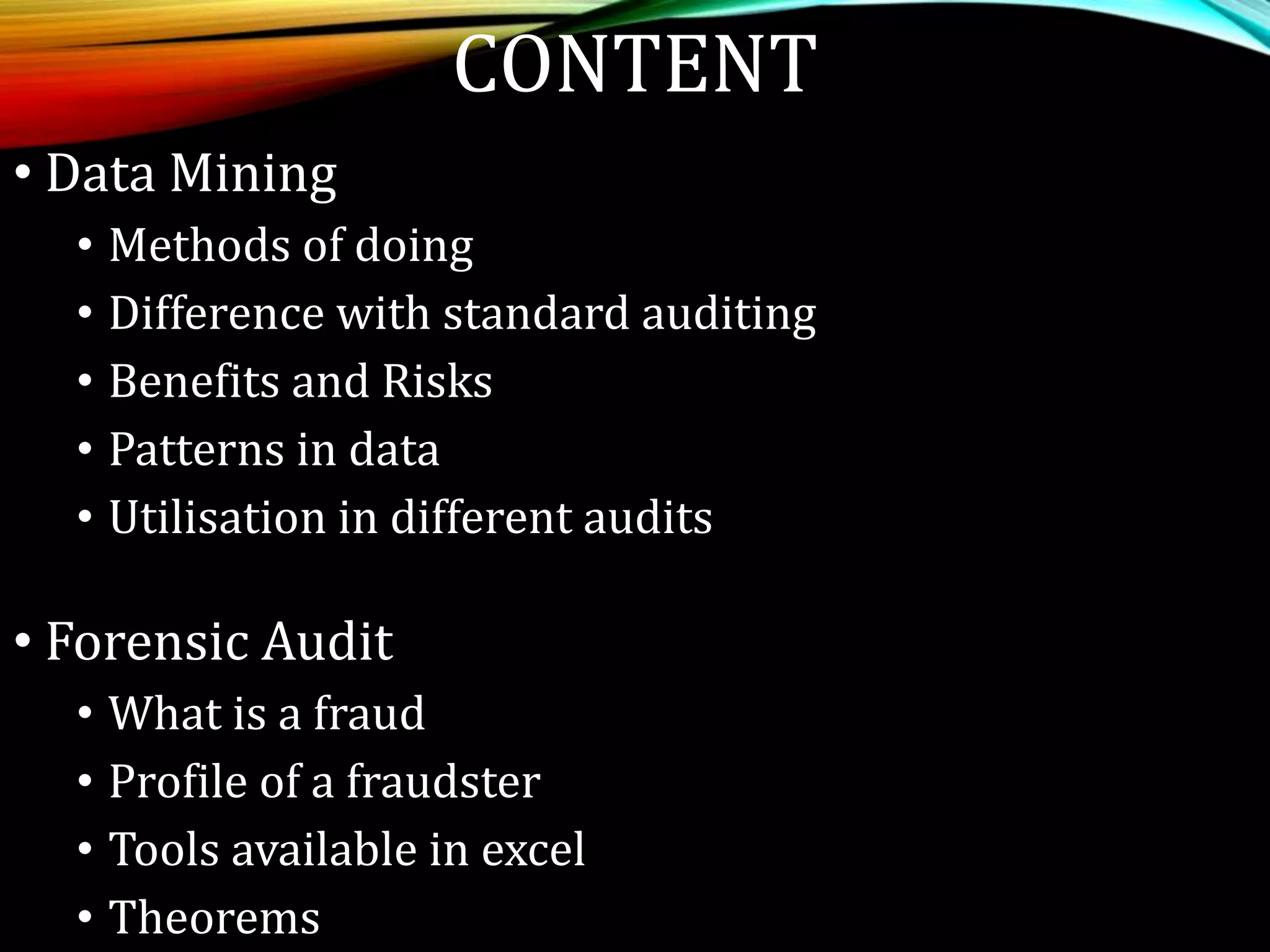

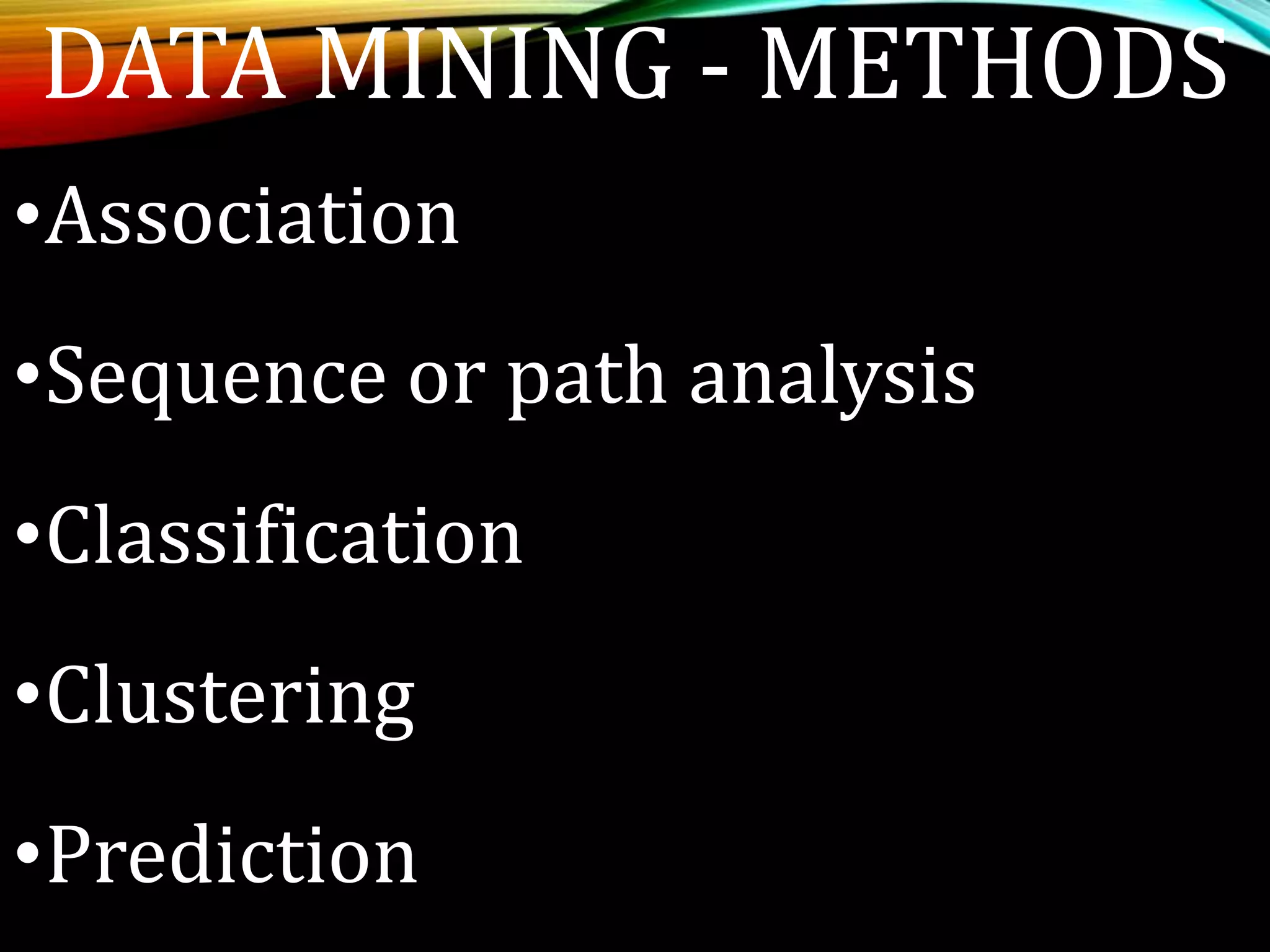

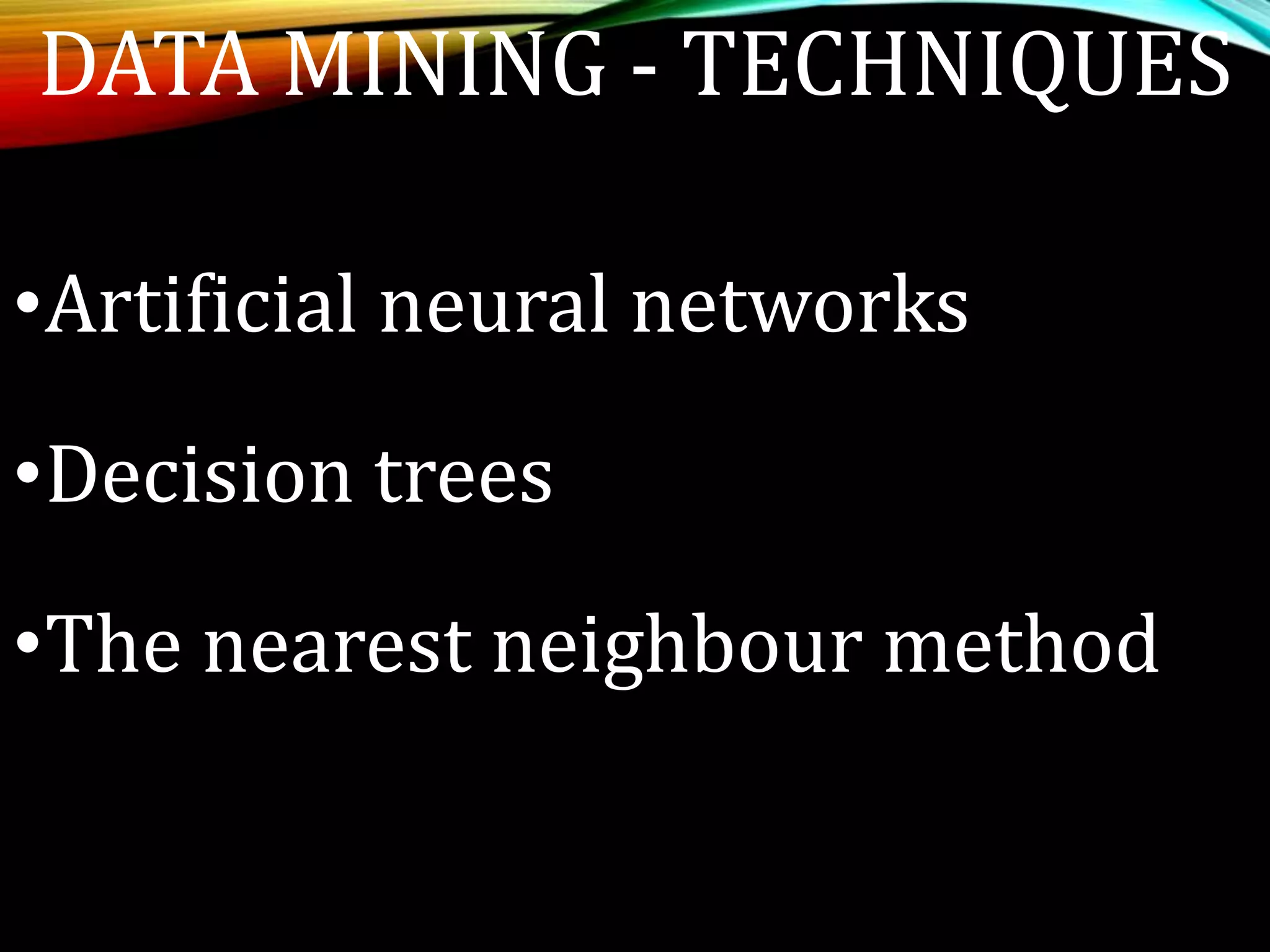

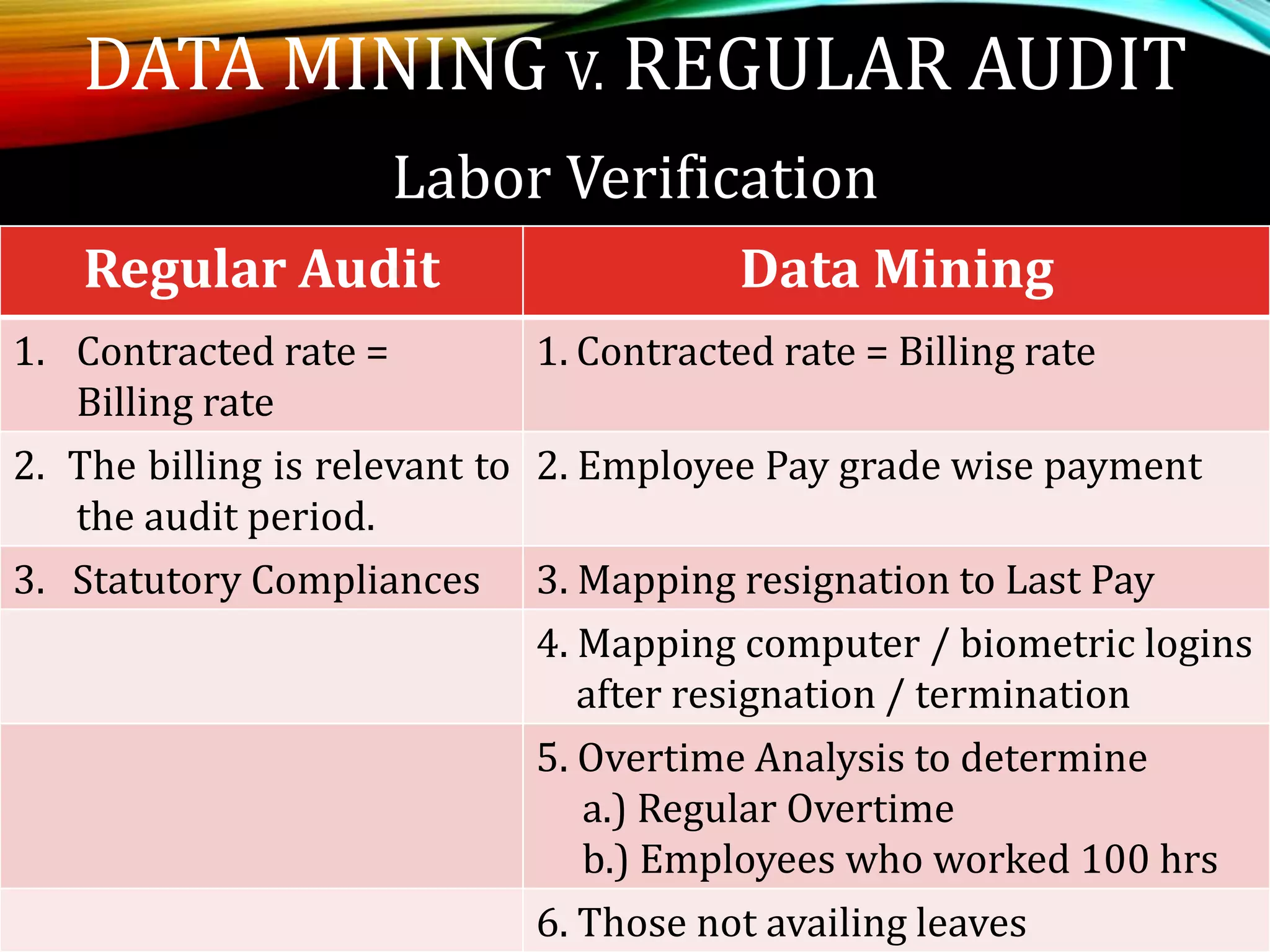

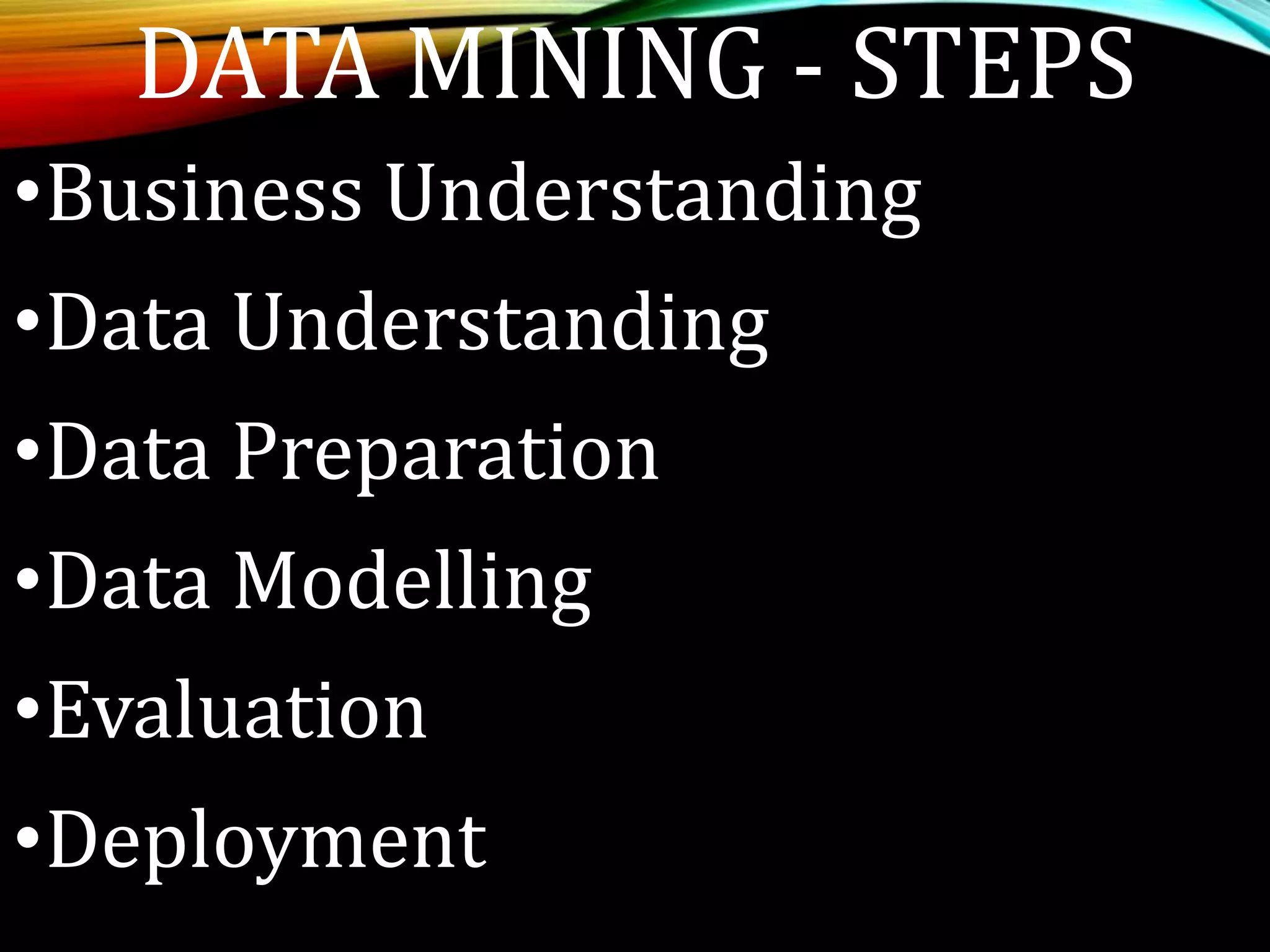

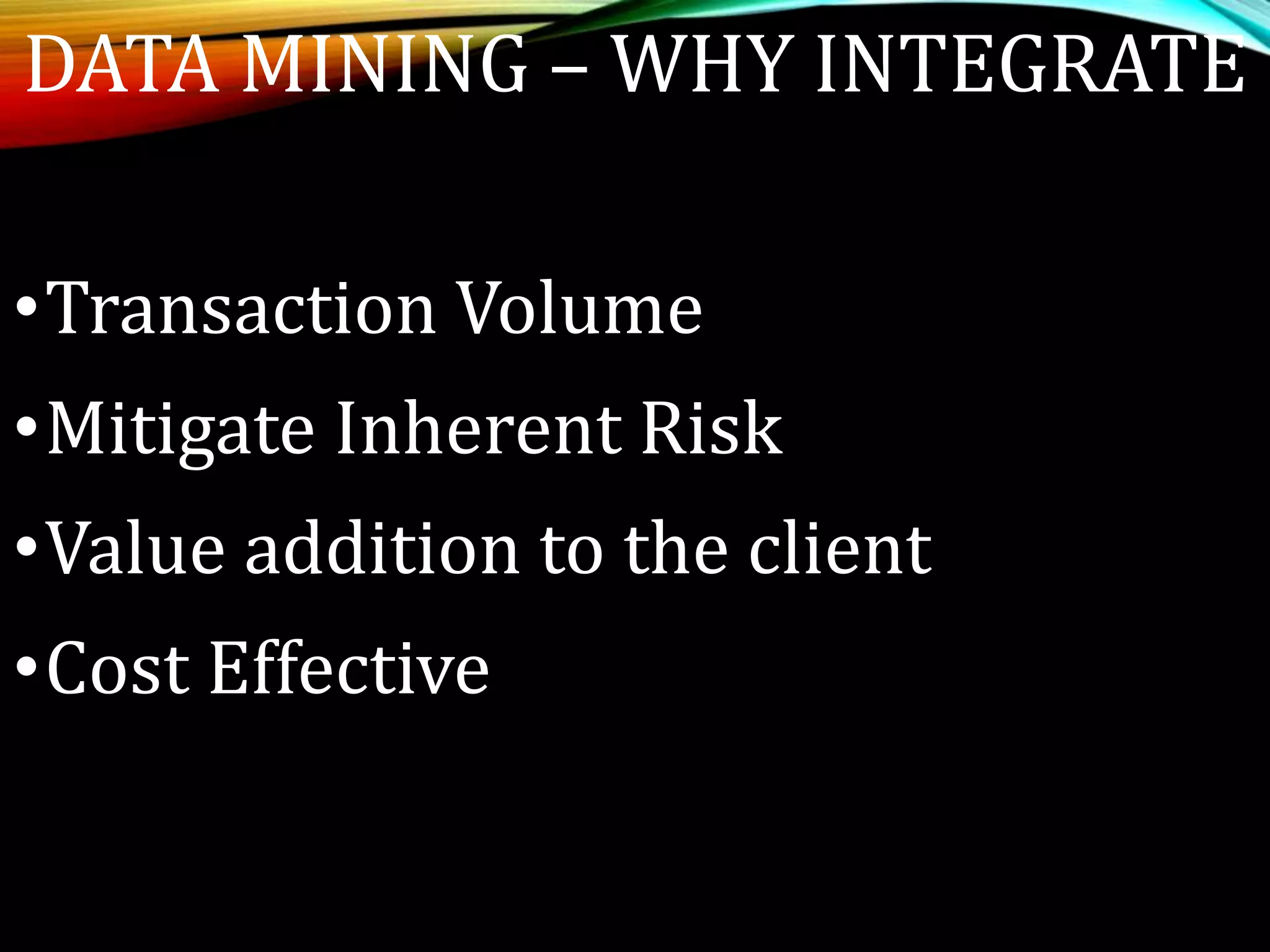

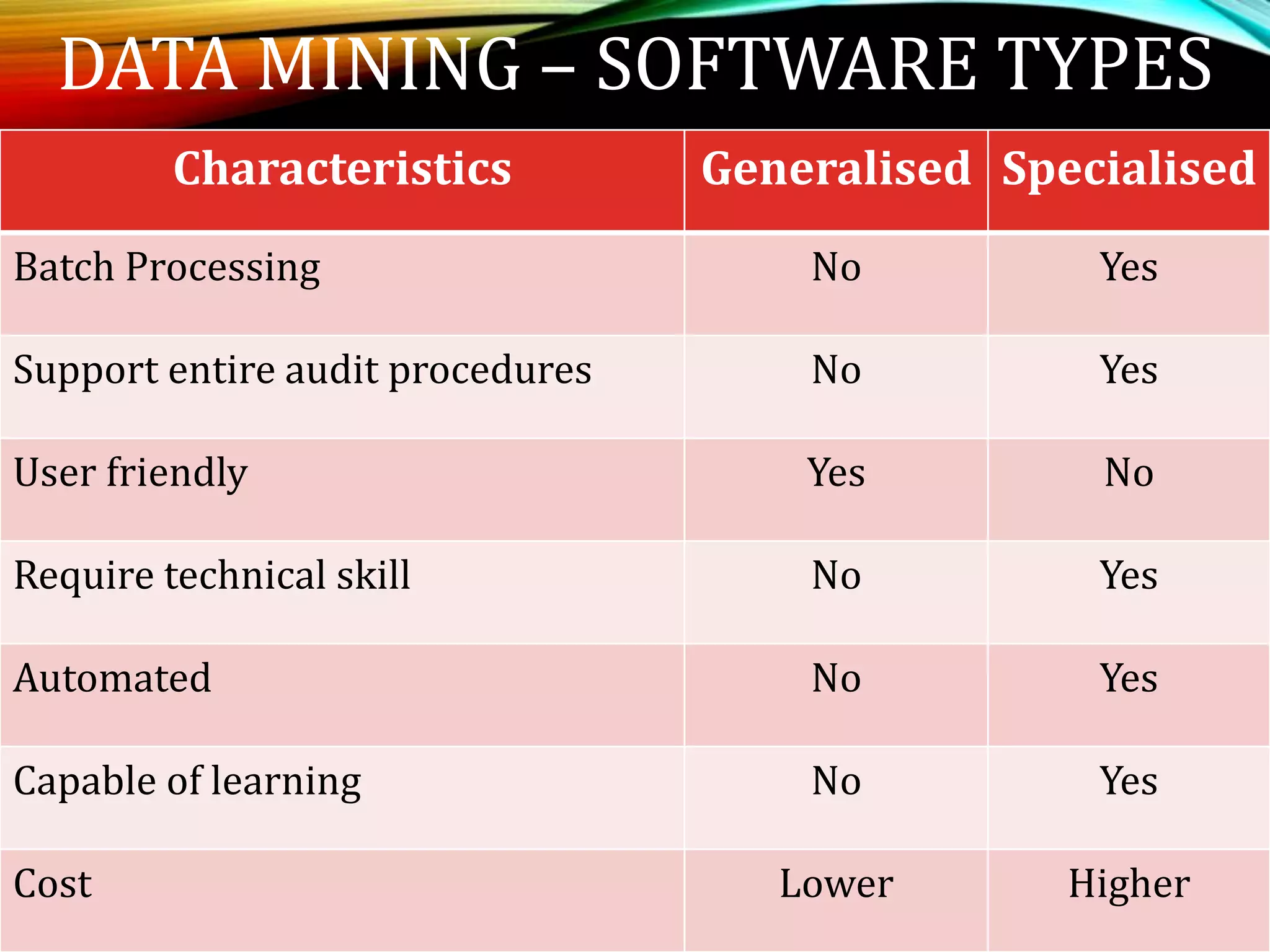

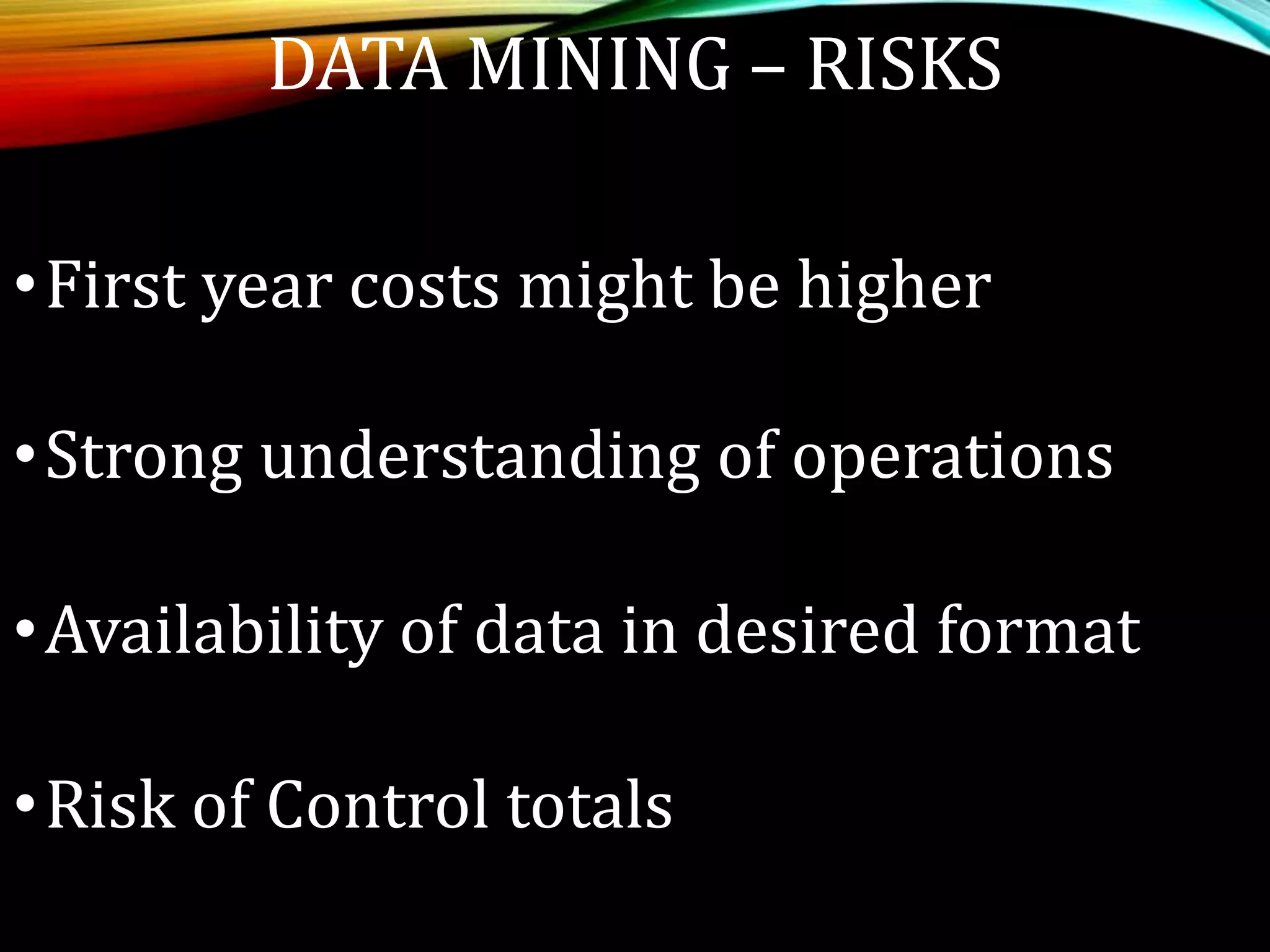

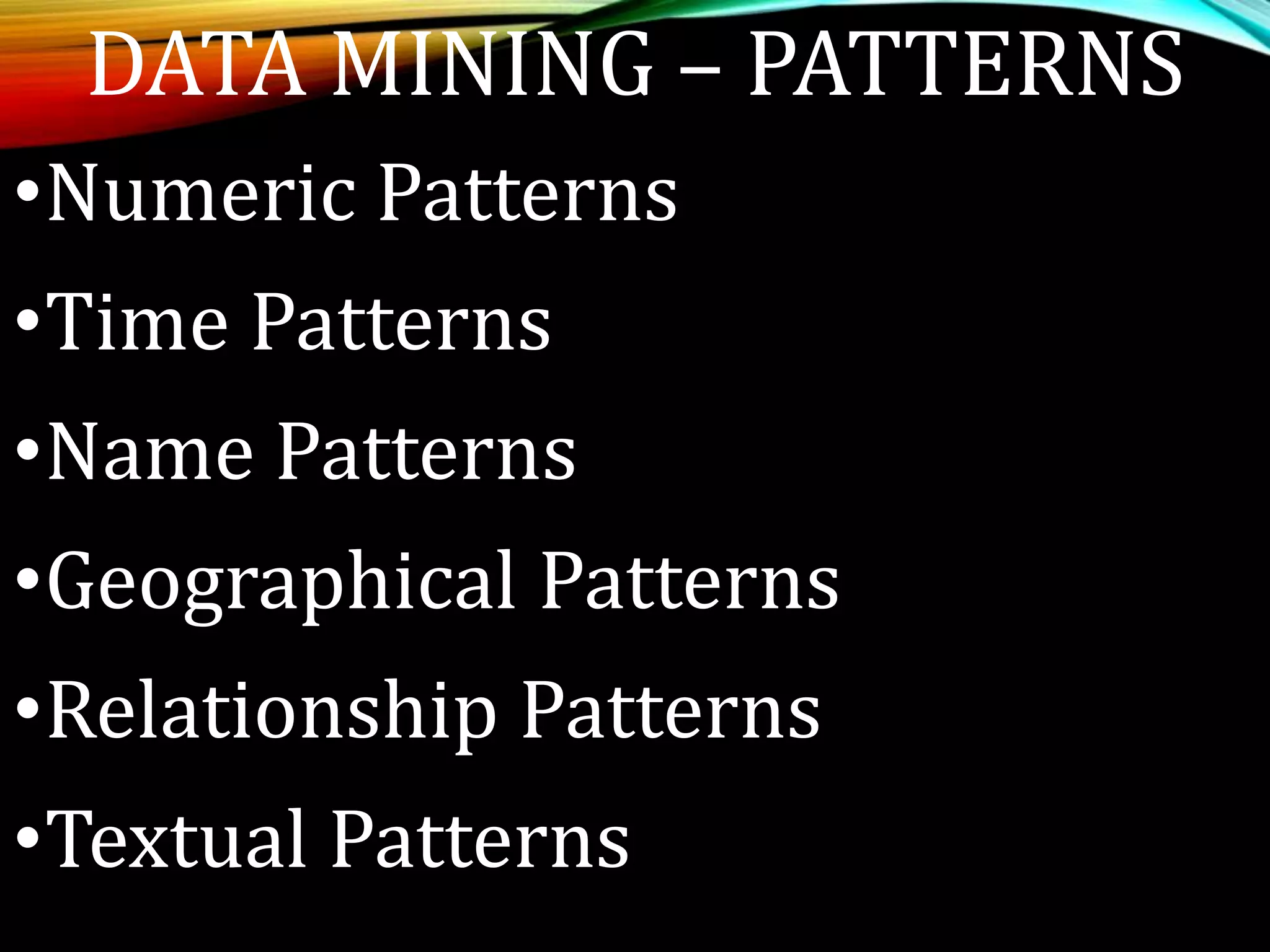

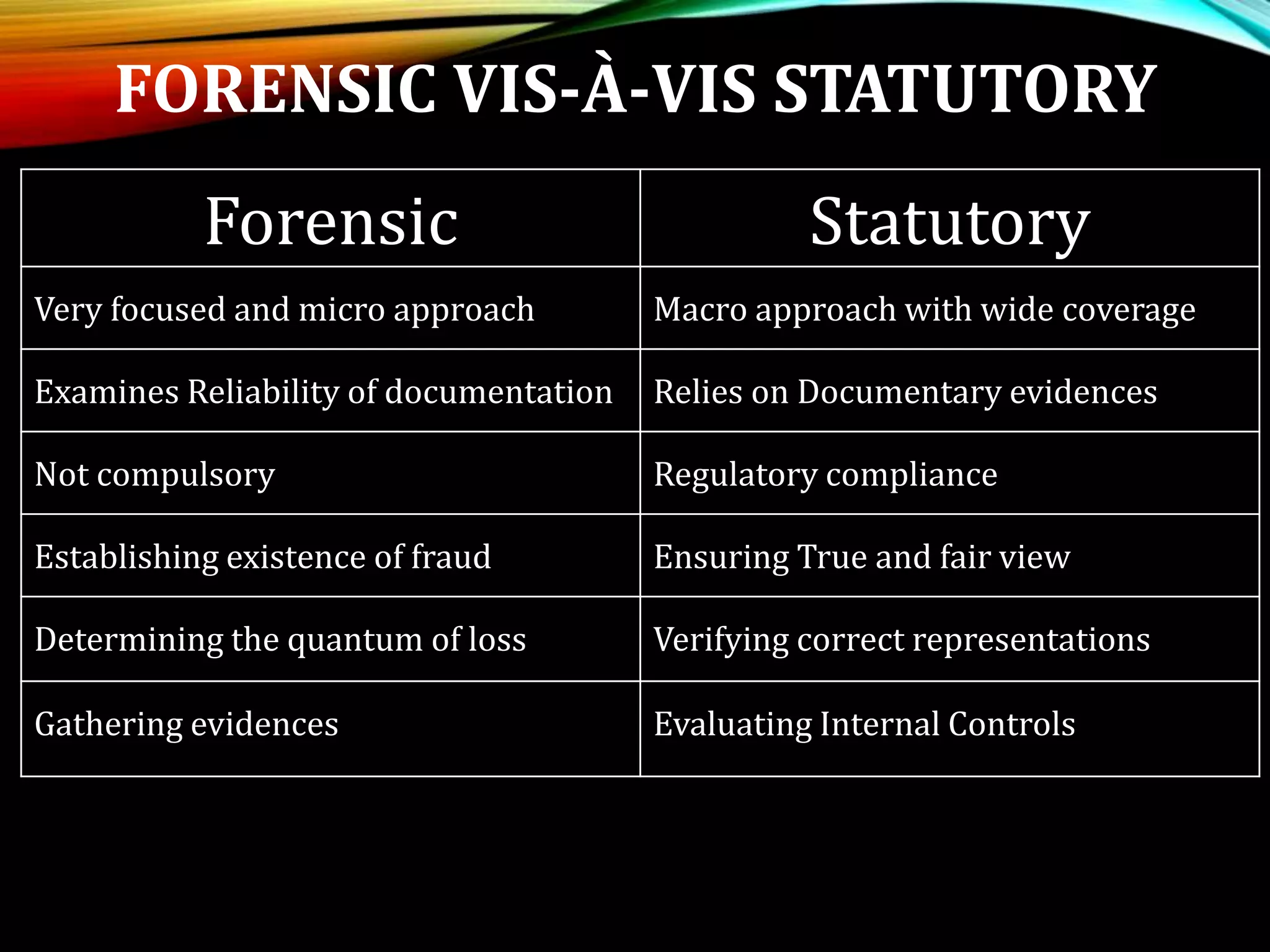

Defines data mining, its steps, classification methods, benefits, risks, and comparison with regular audits.

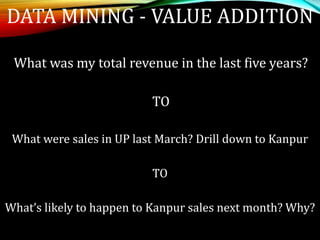

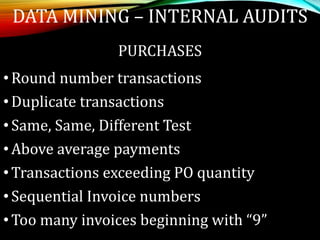

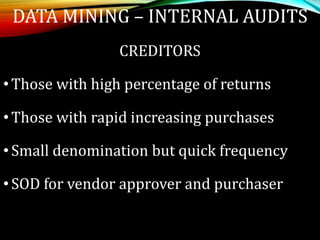

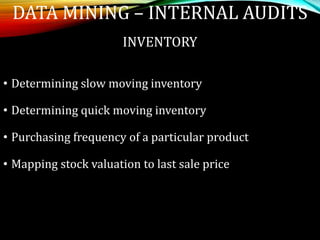

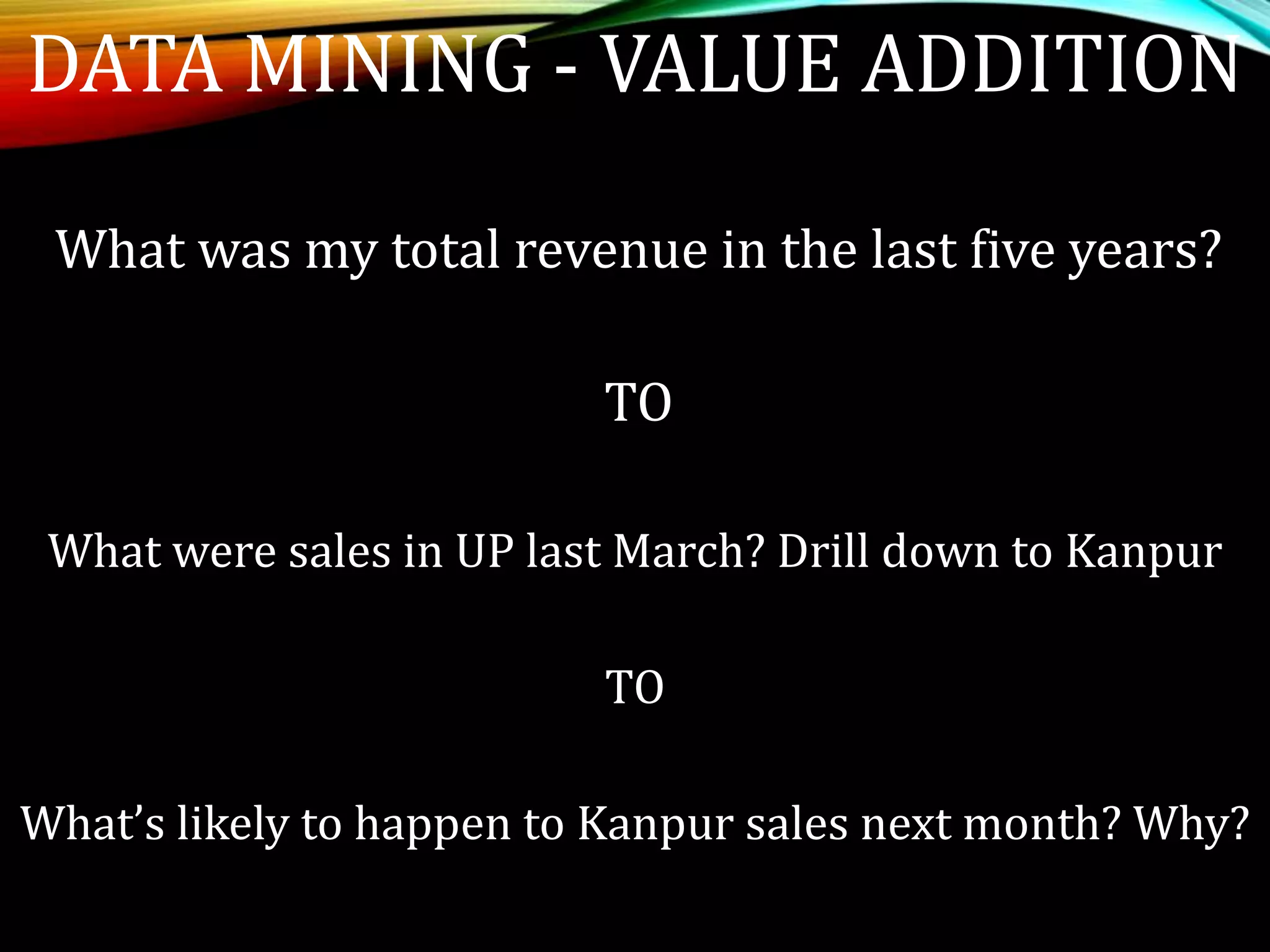

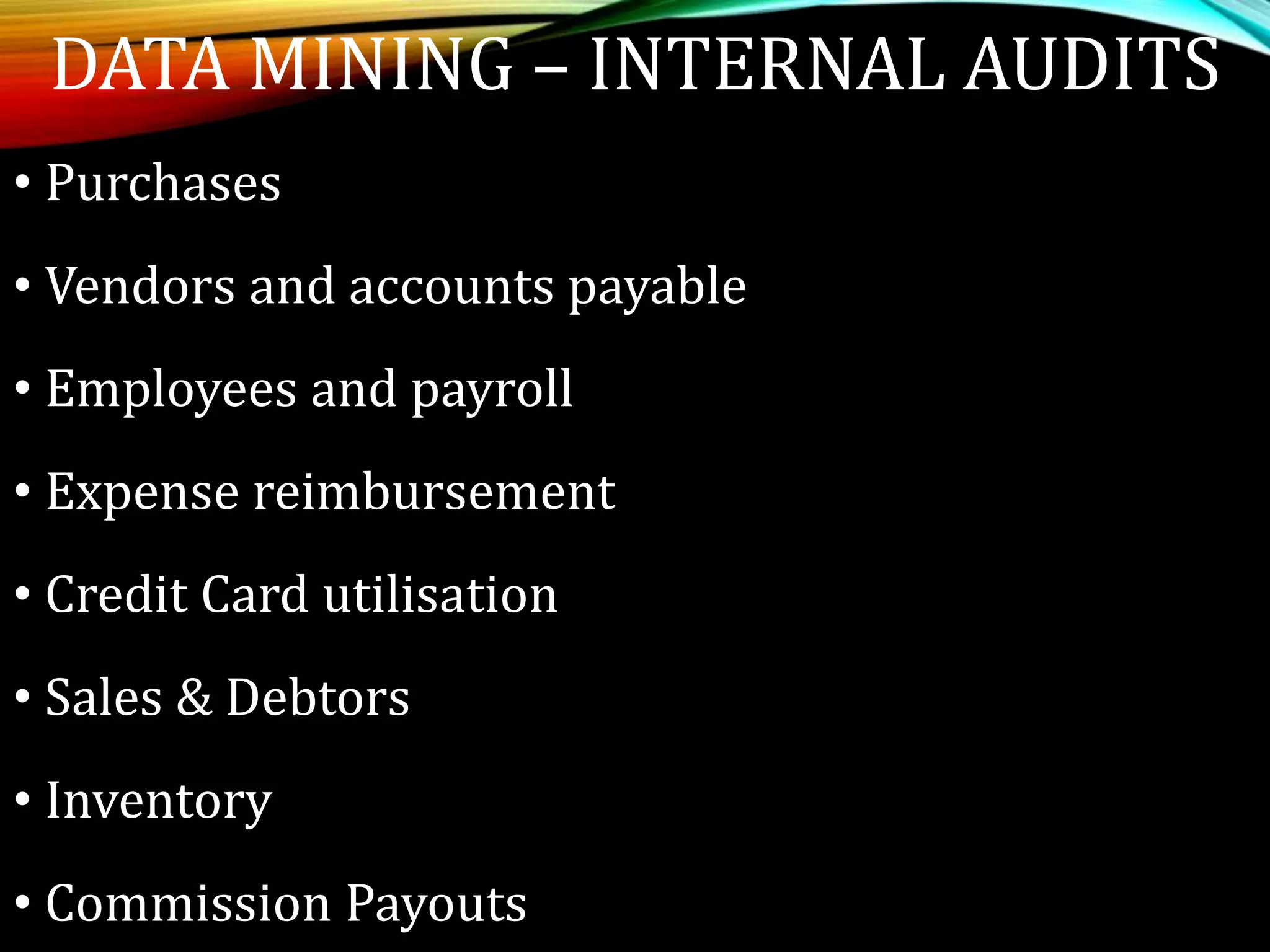

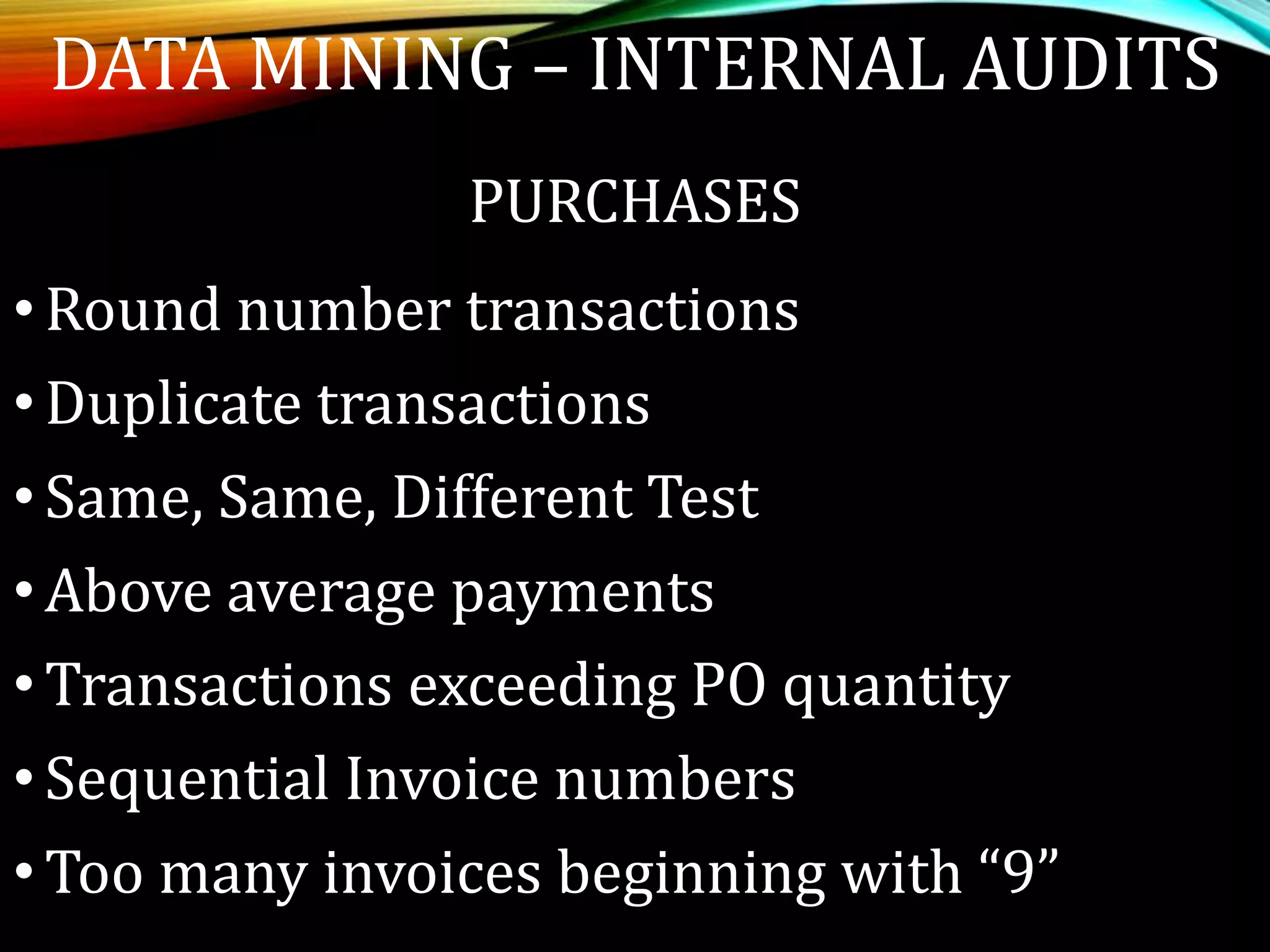

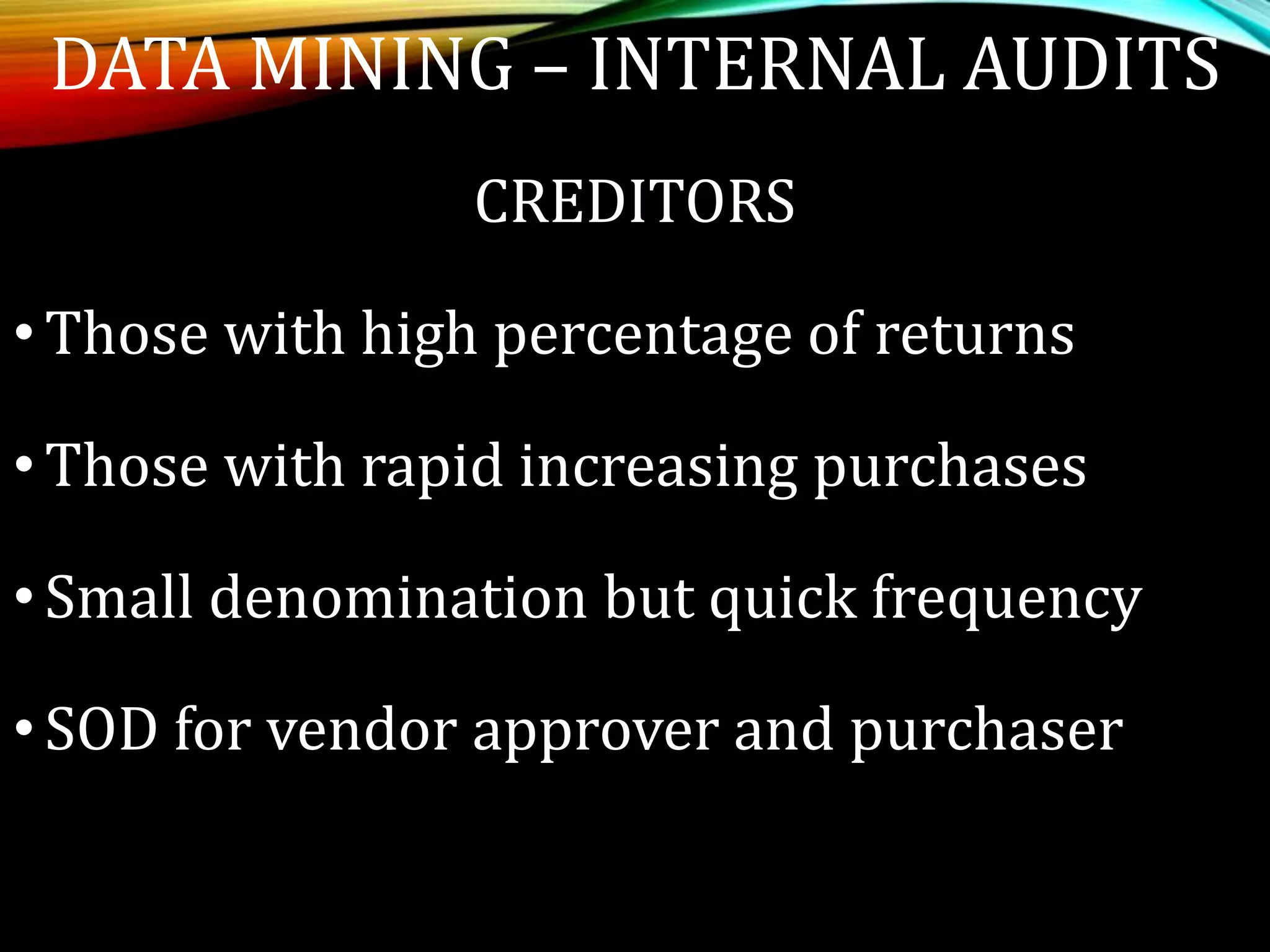

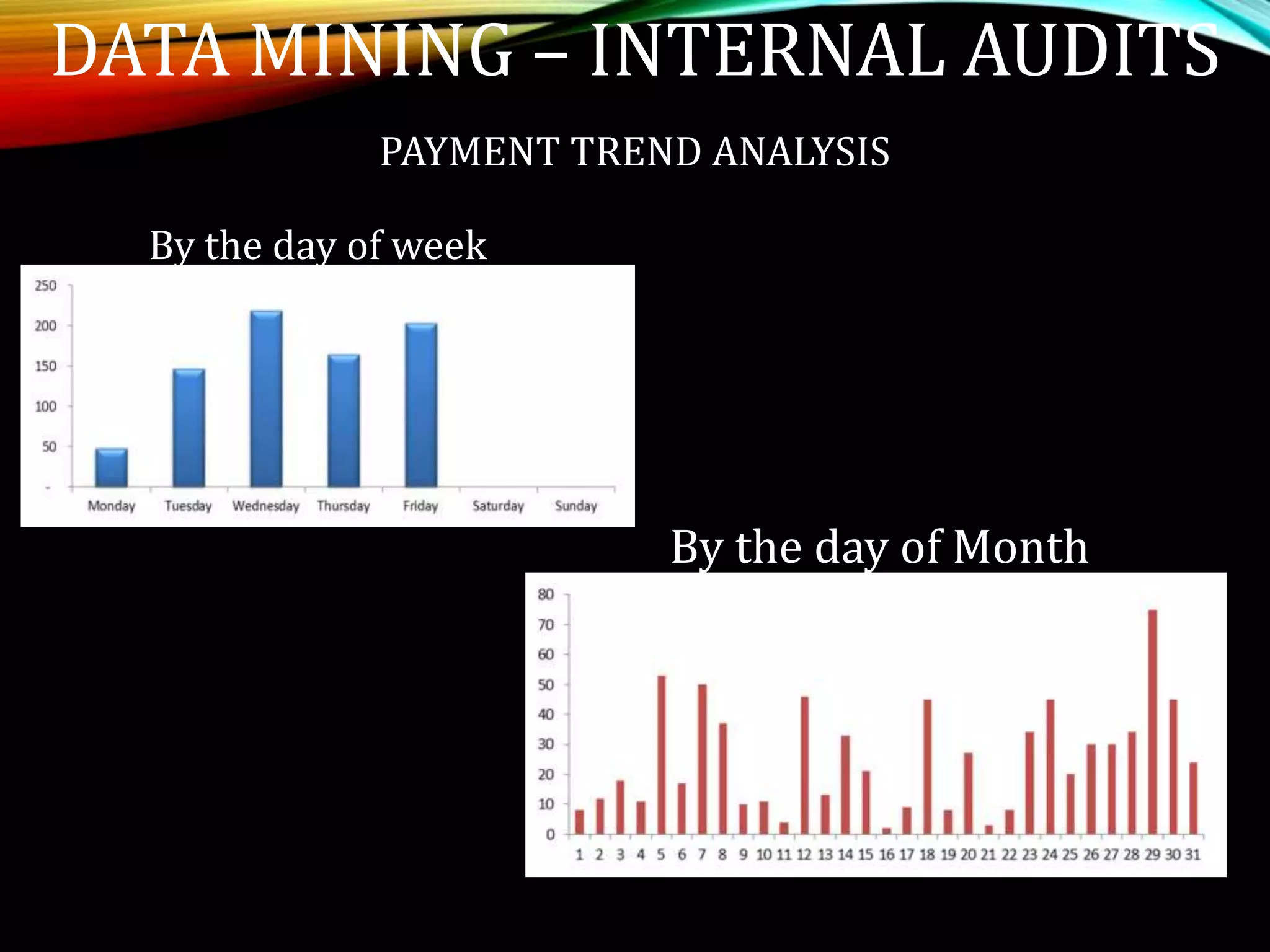

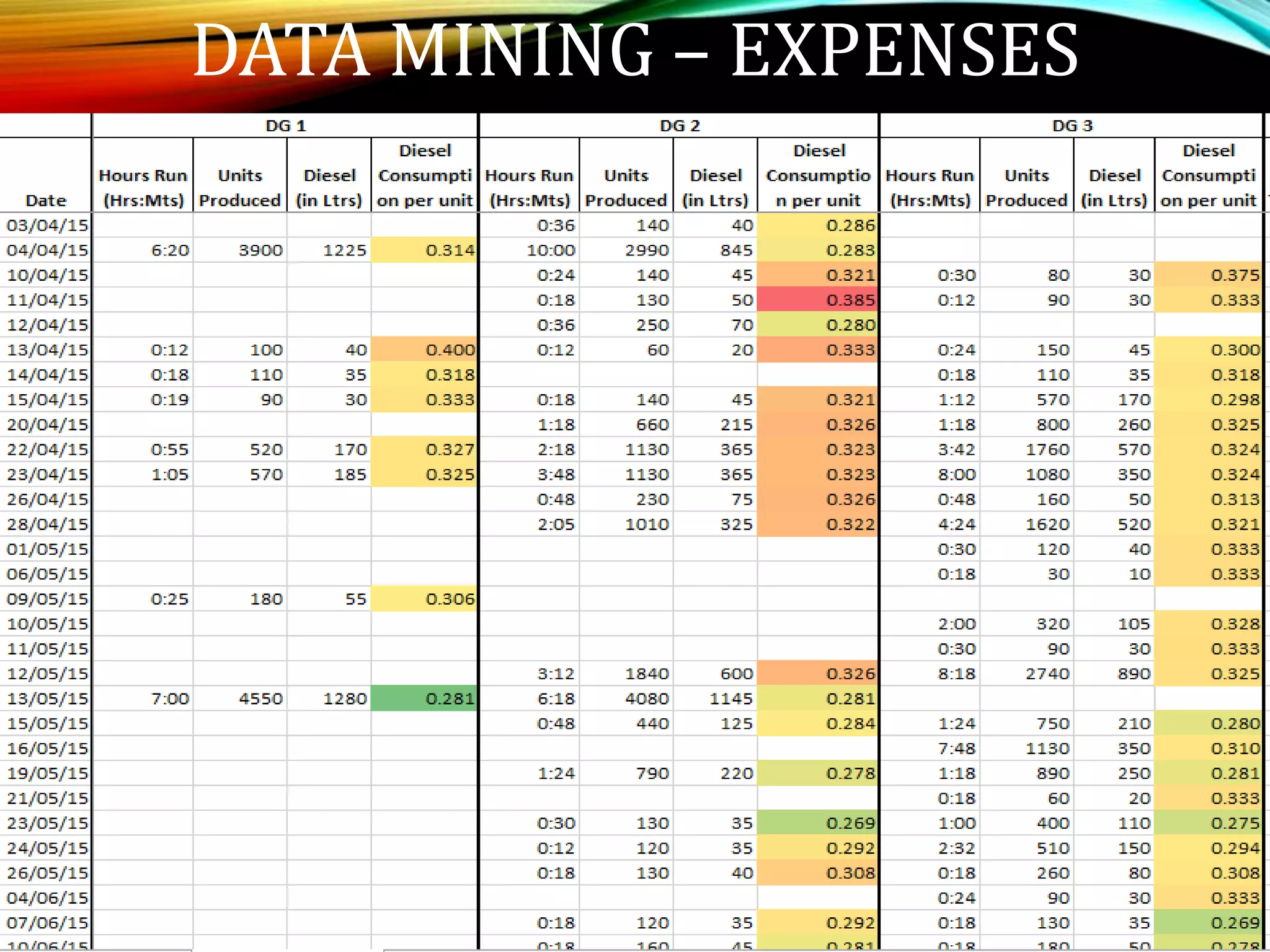

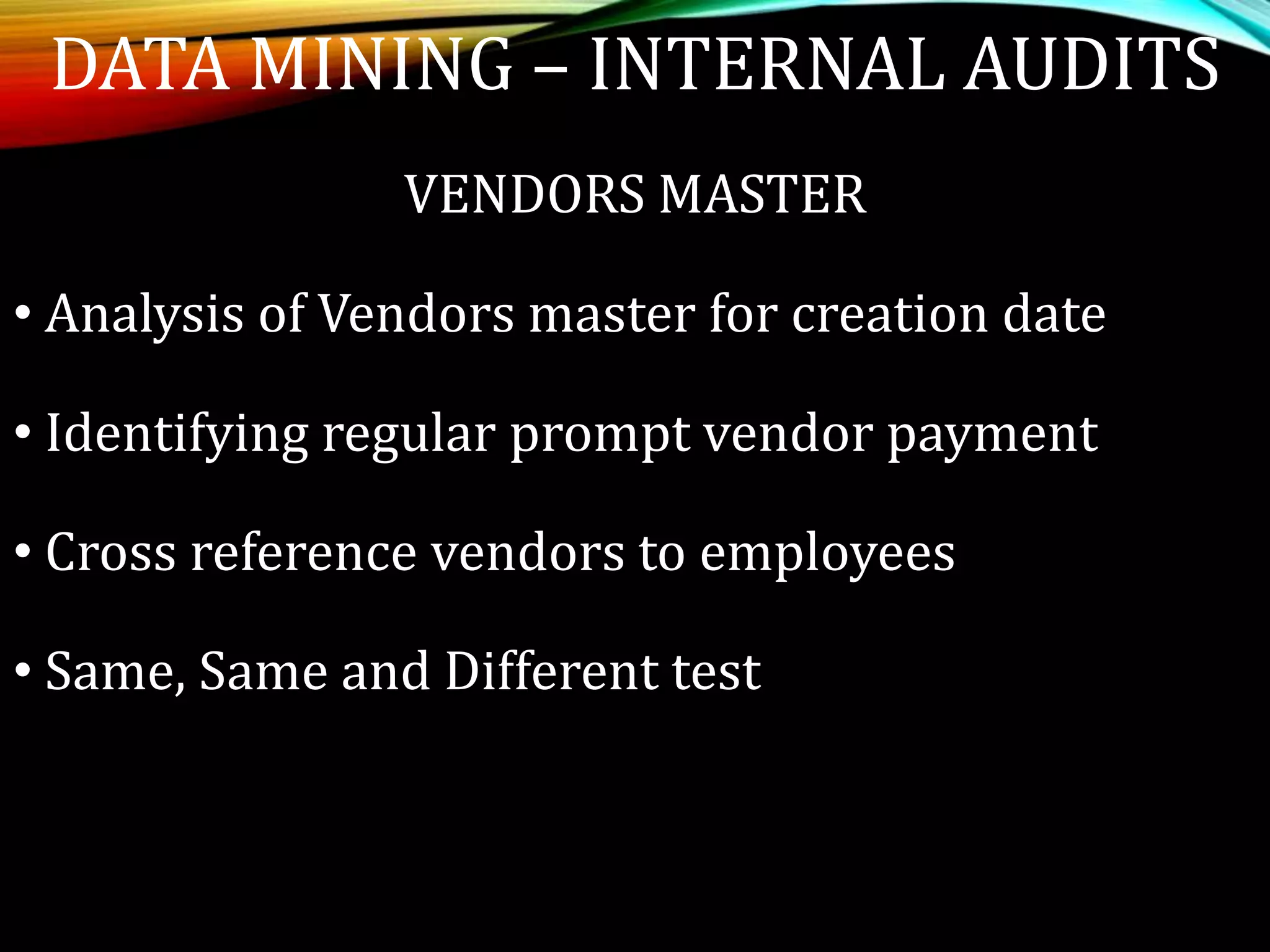

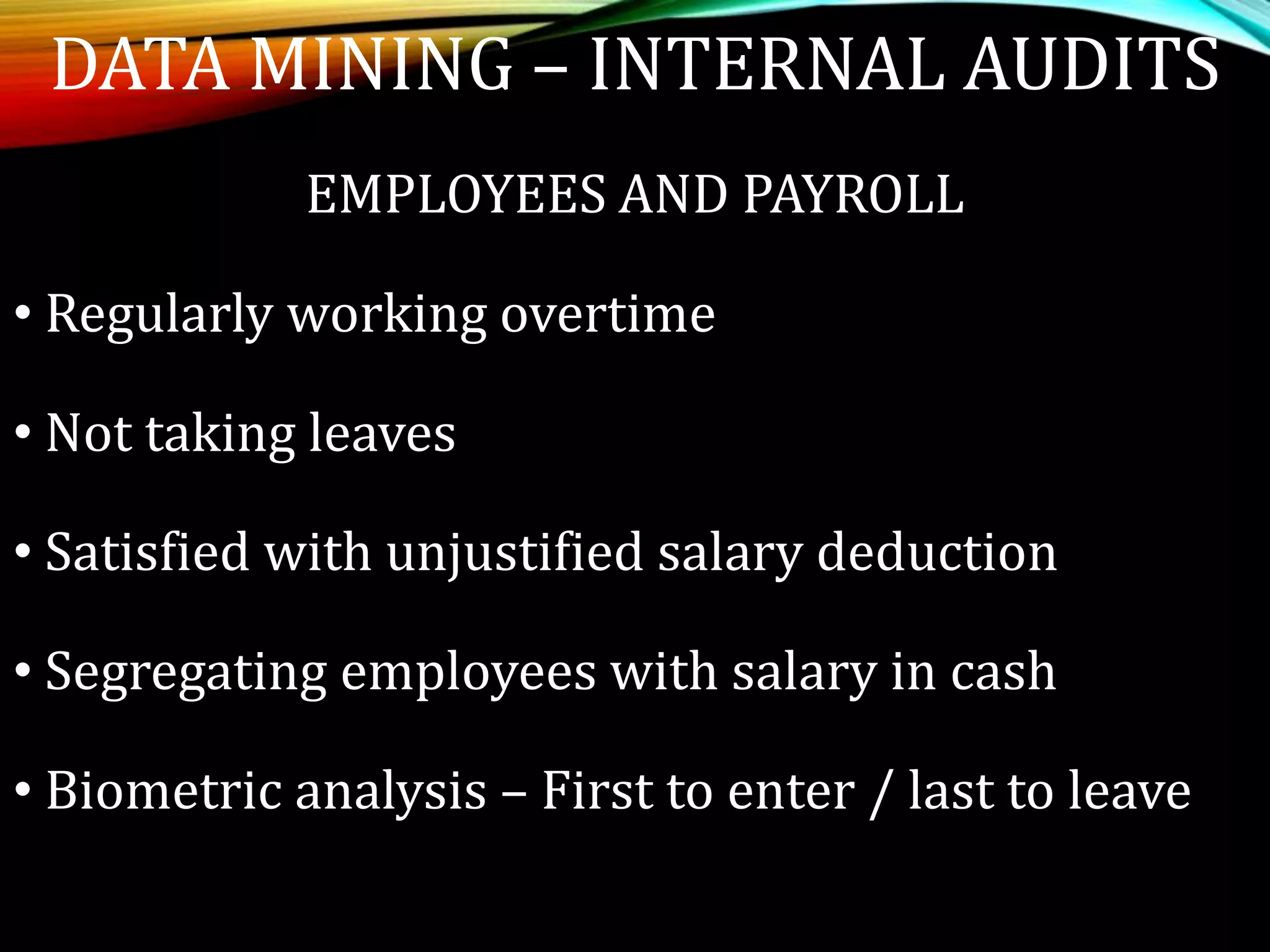

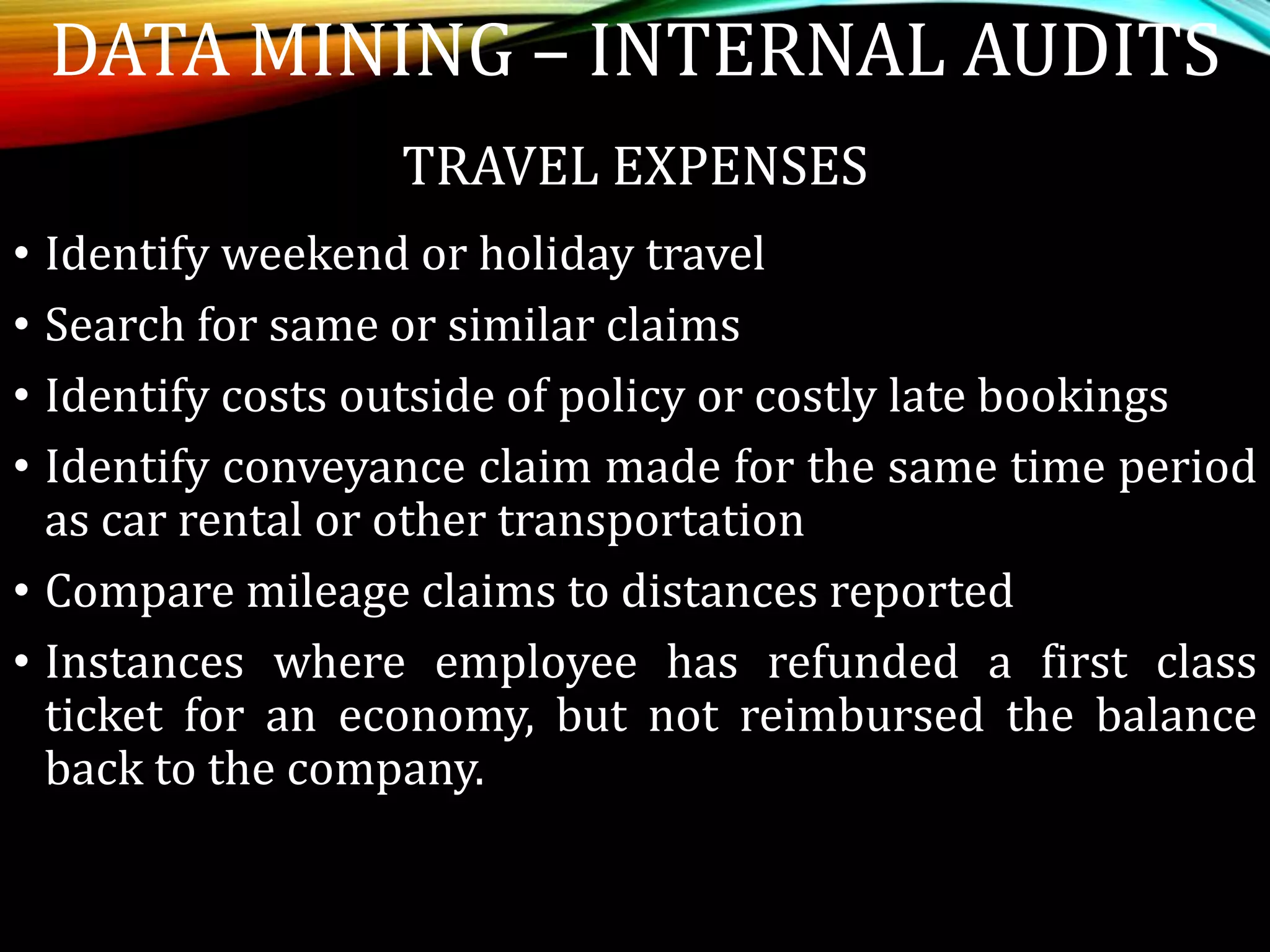

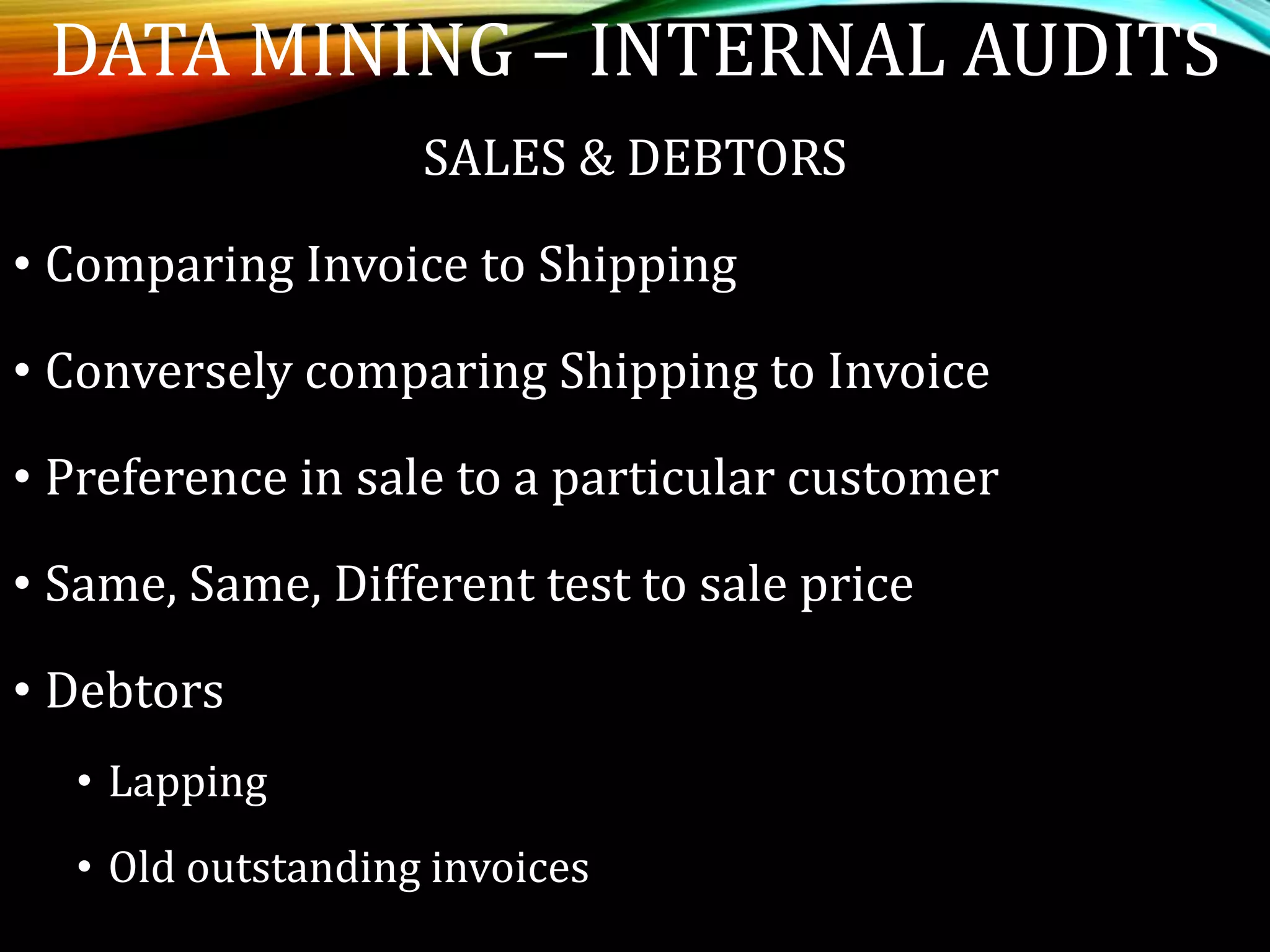

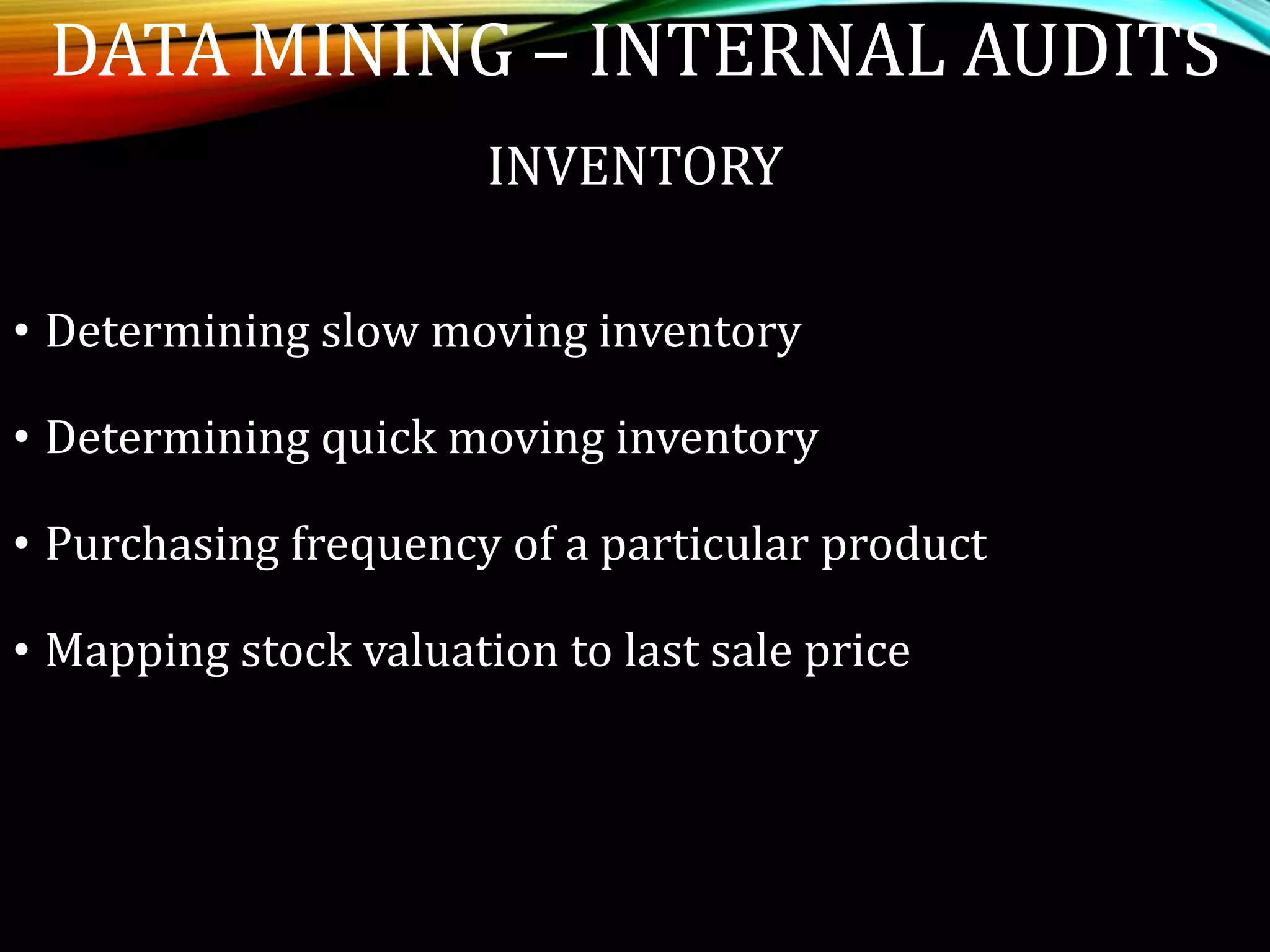

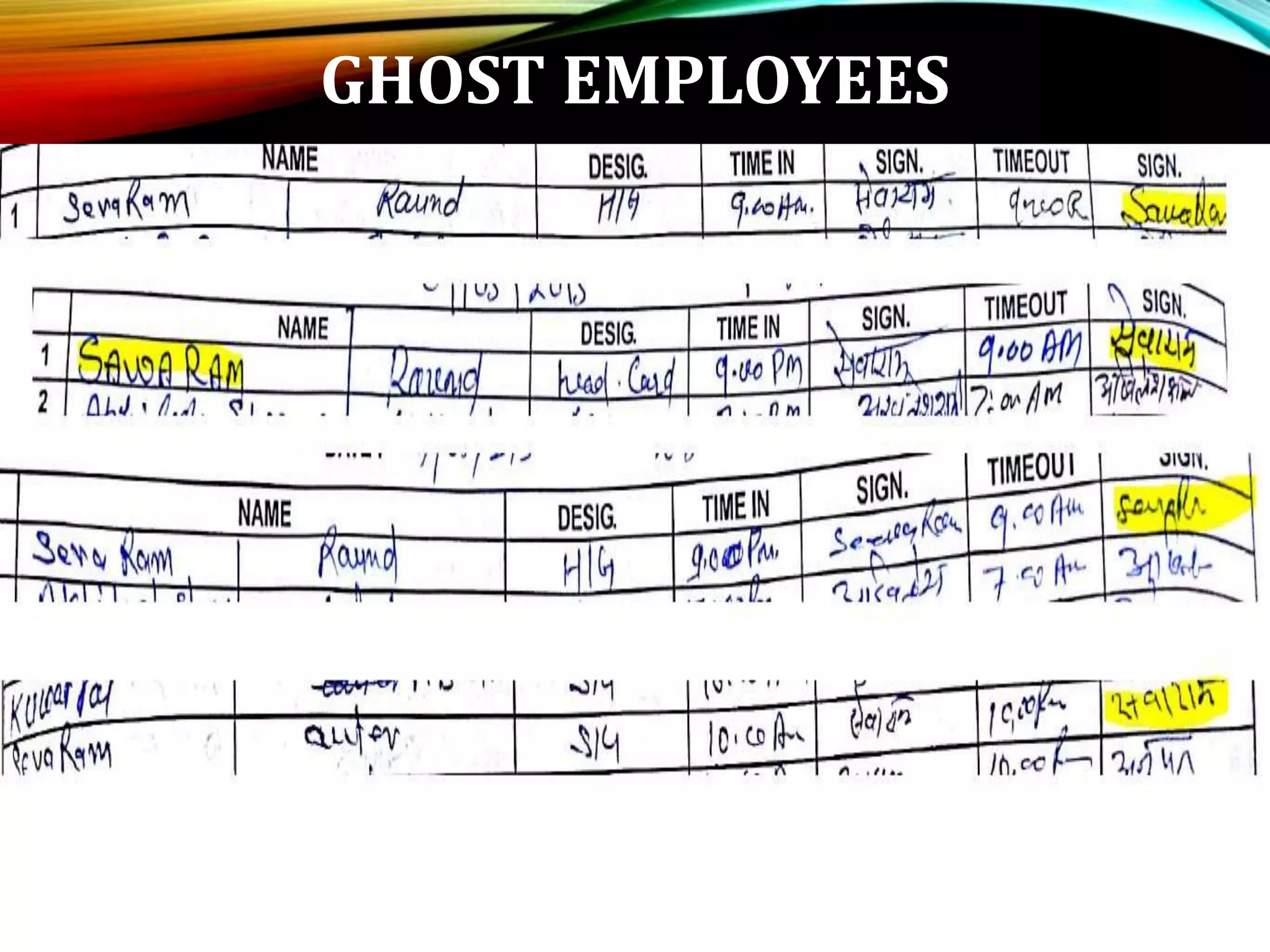

Focuses on applying data mining in internal audits to analyze revenue trends, vendor payments, and employee payroll.

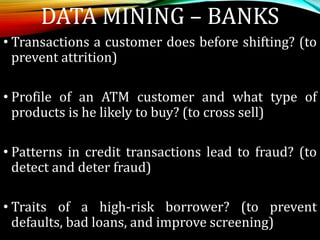

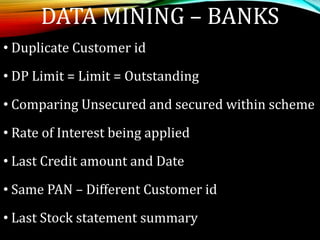

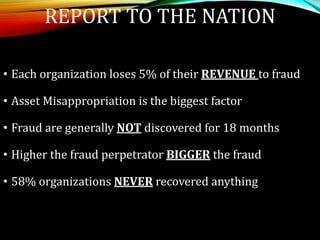

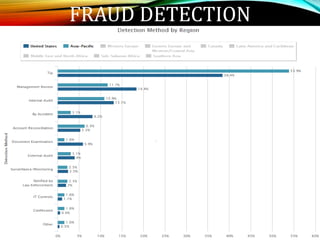

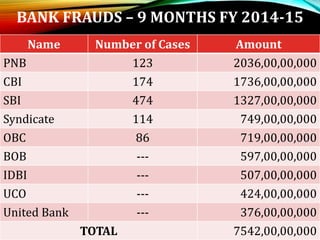

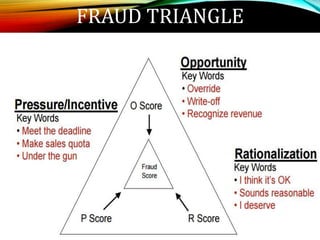

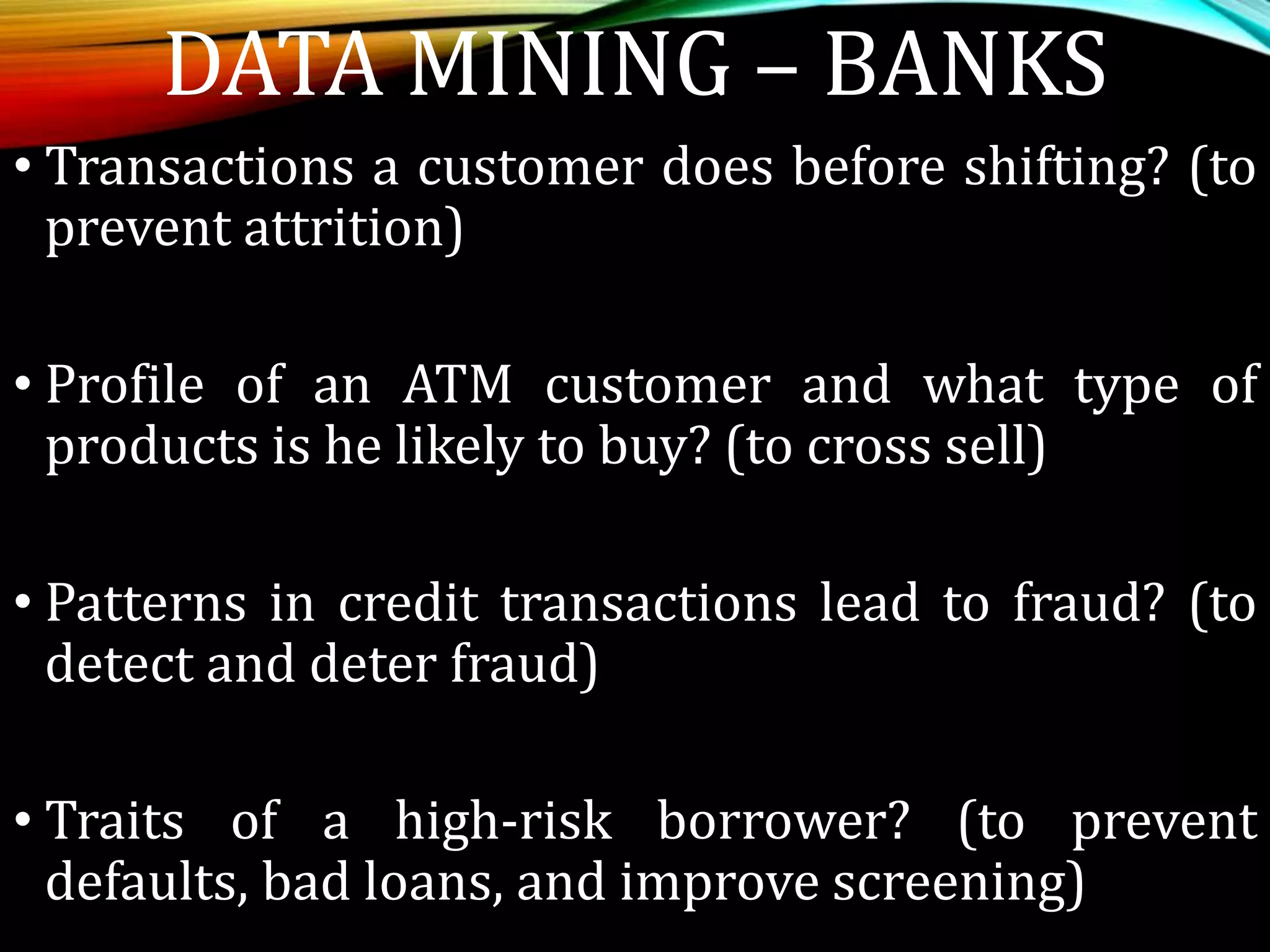

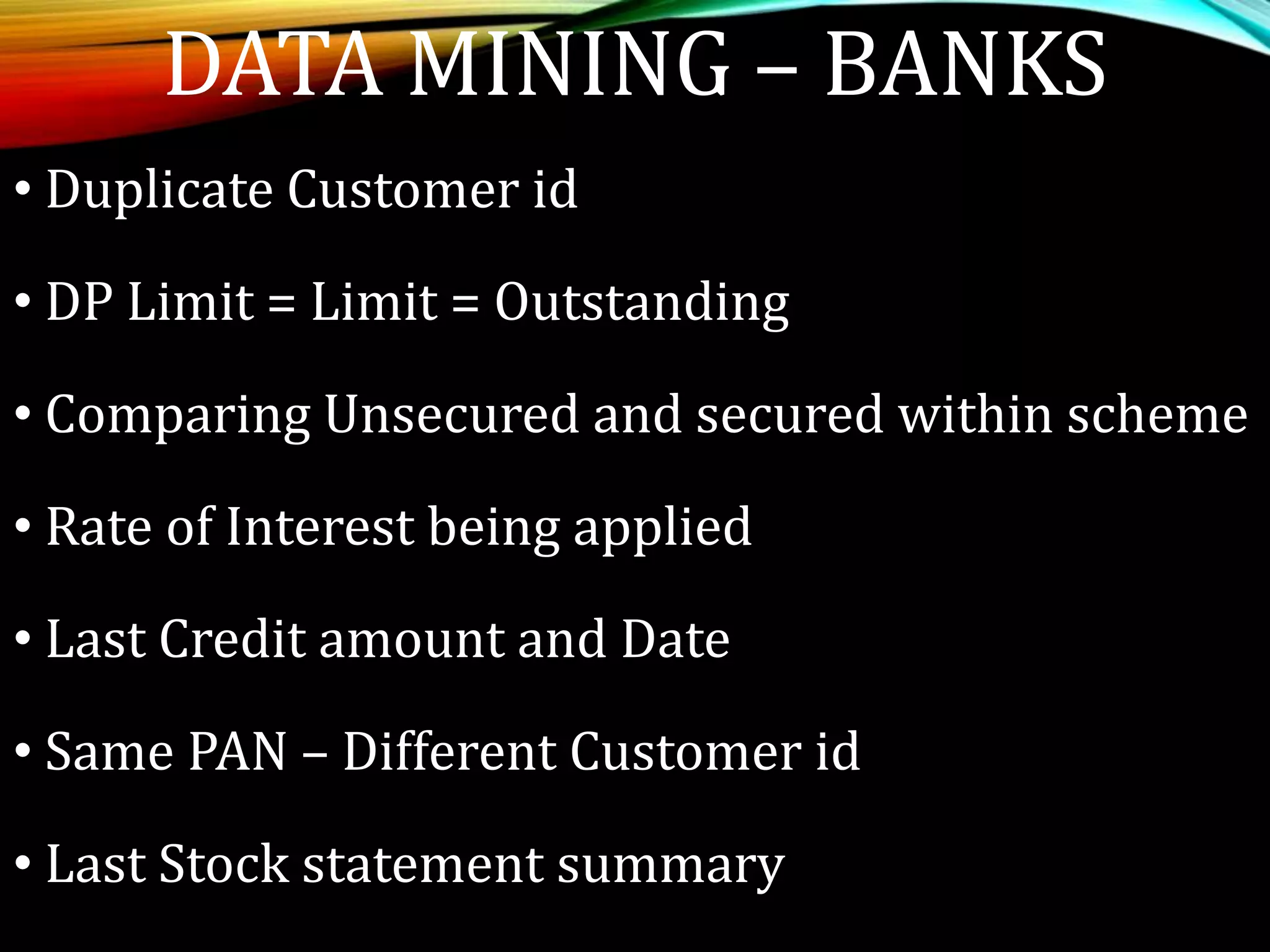

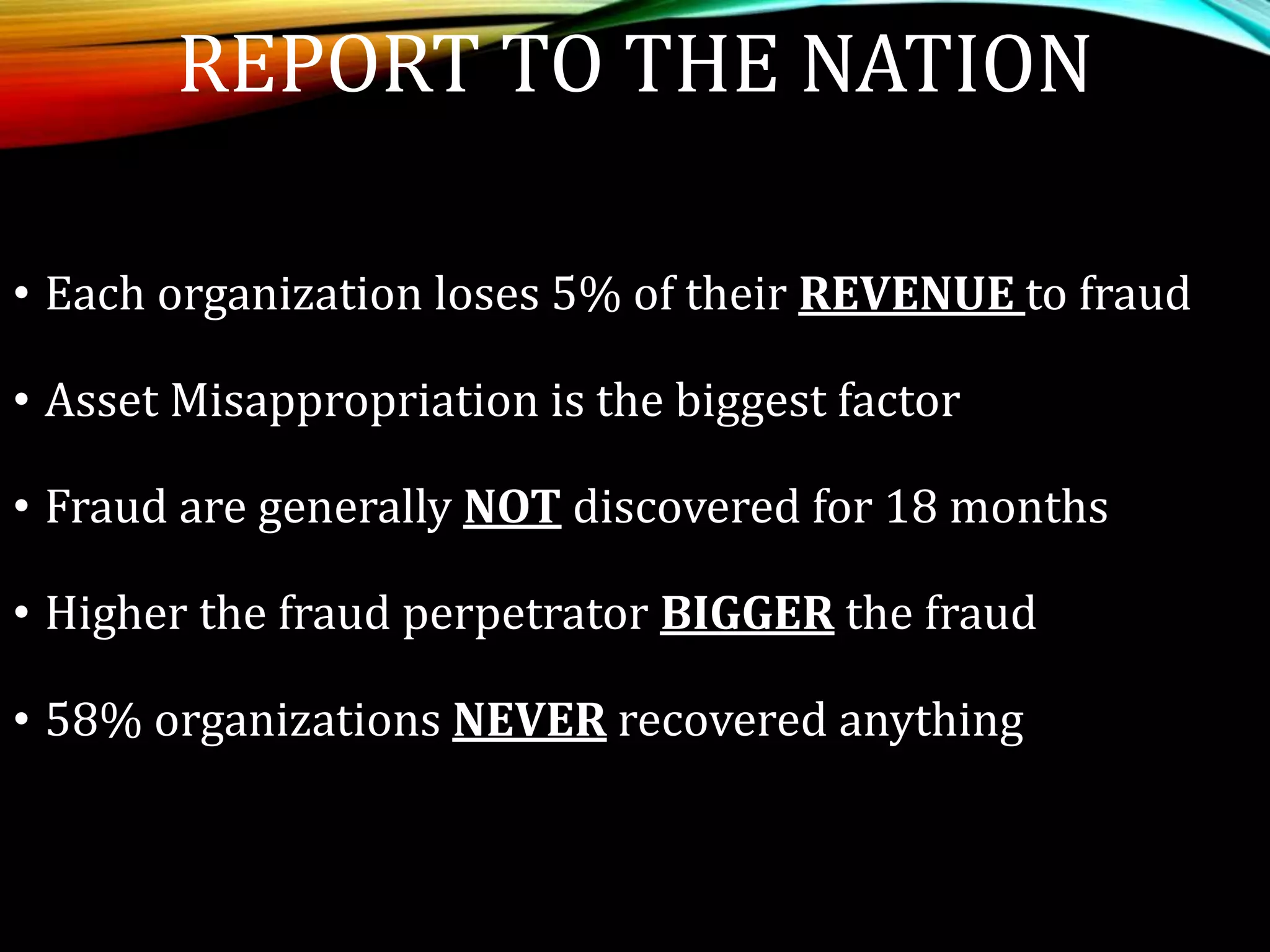

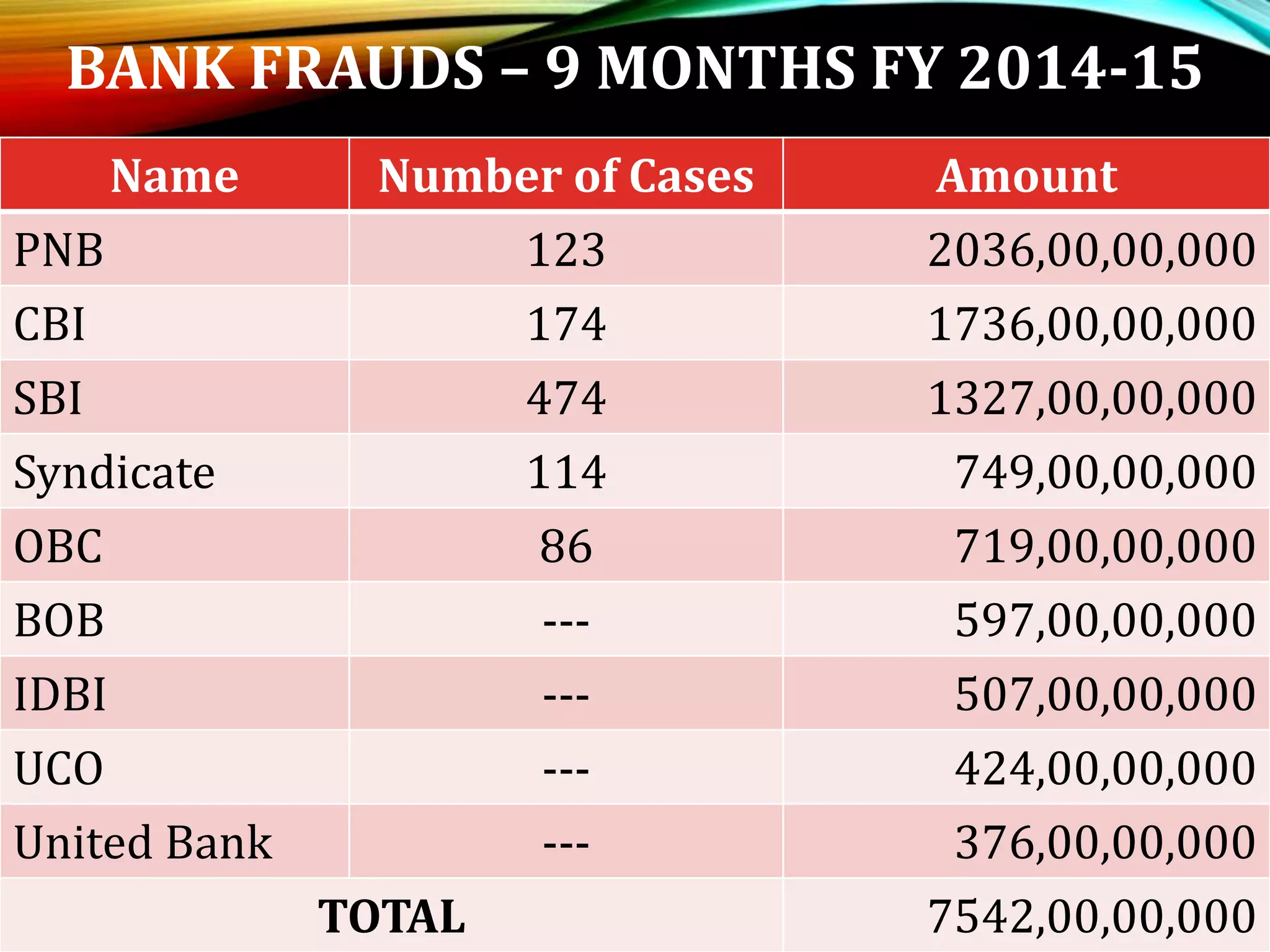

Discusses bank fraud patterns, the nature of fraud, and its impacts on organizations.

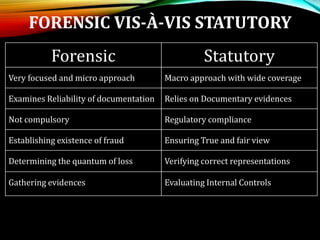

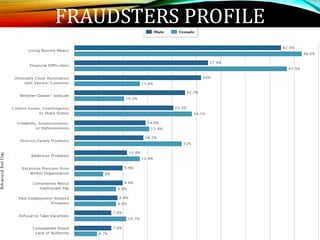

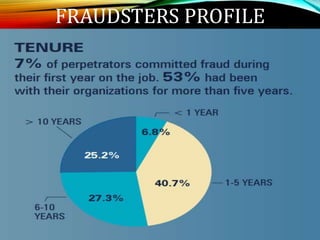

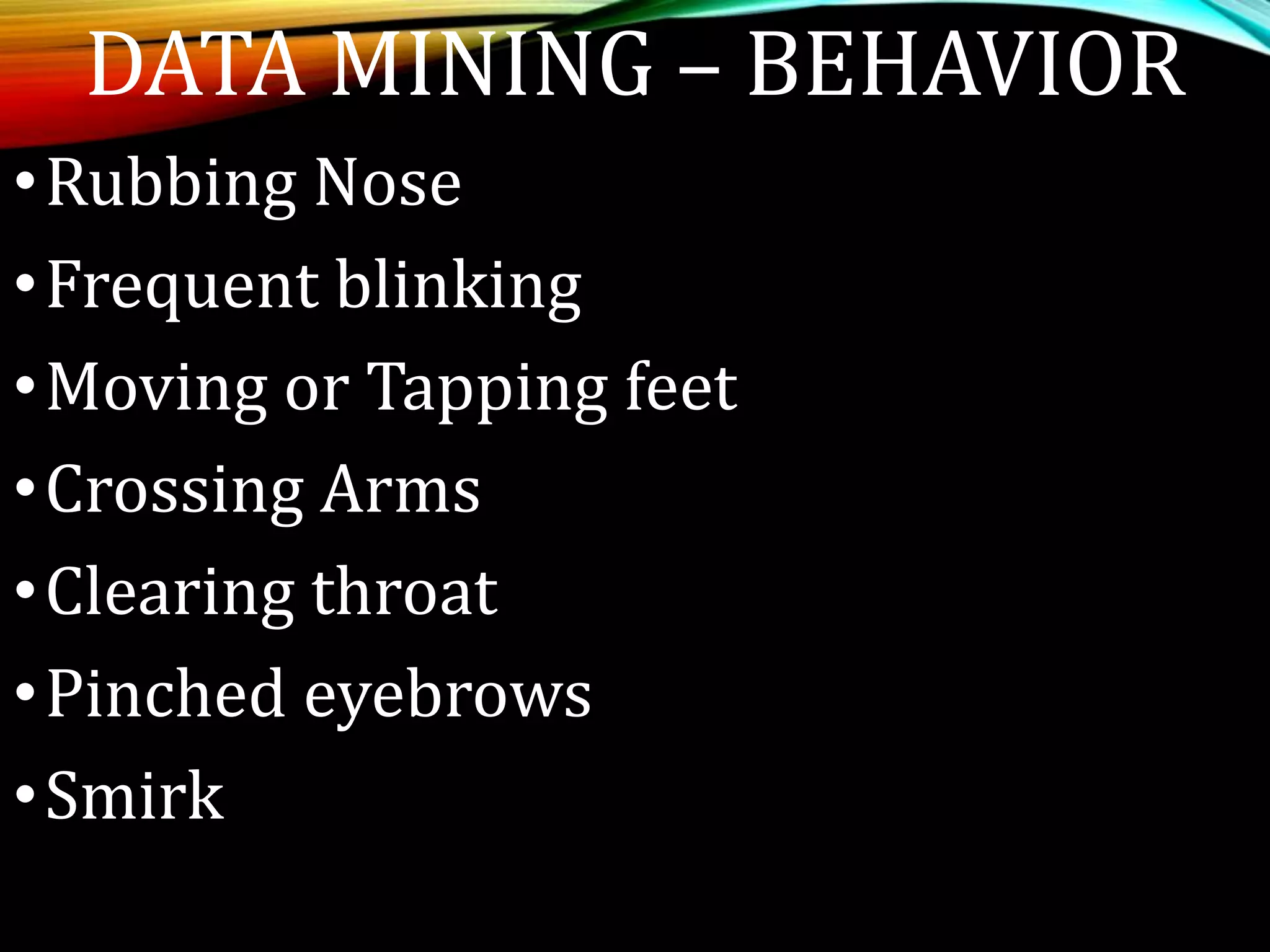

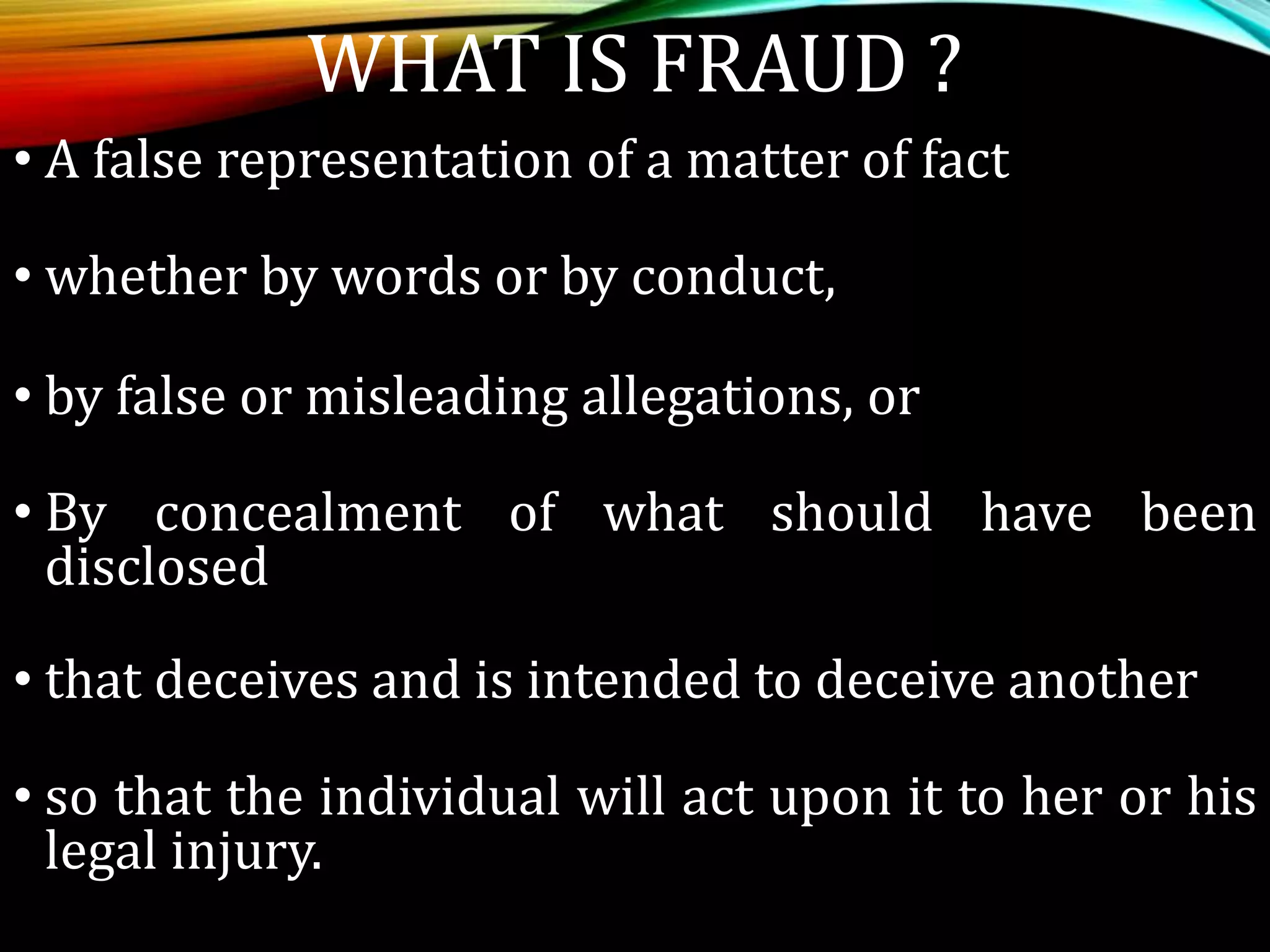

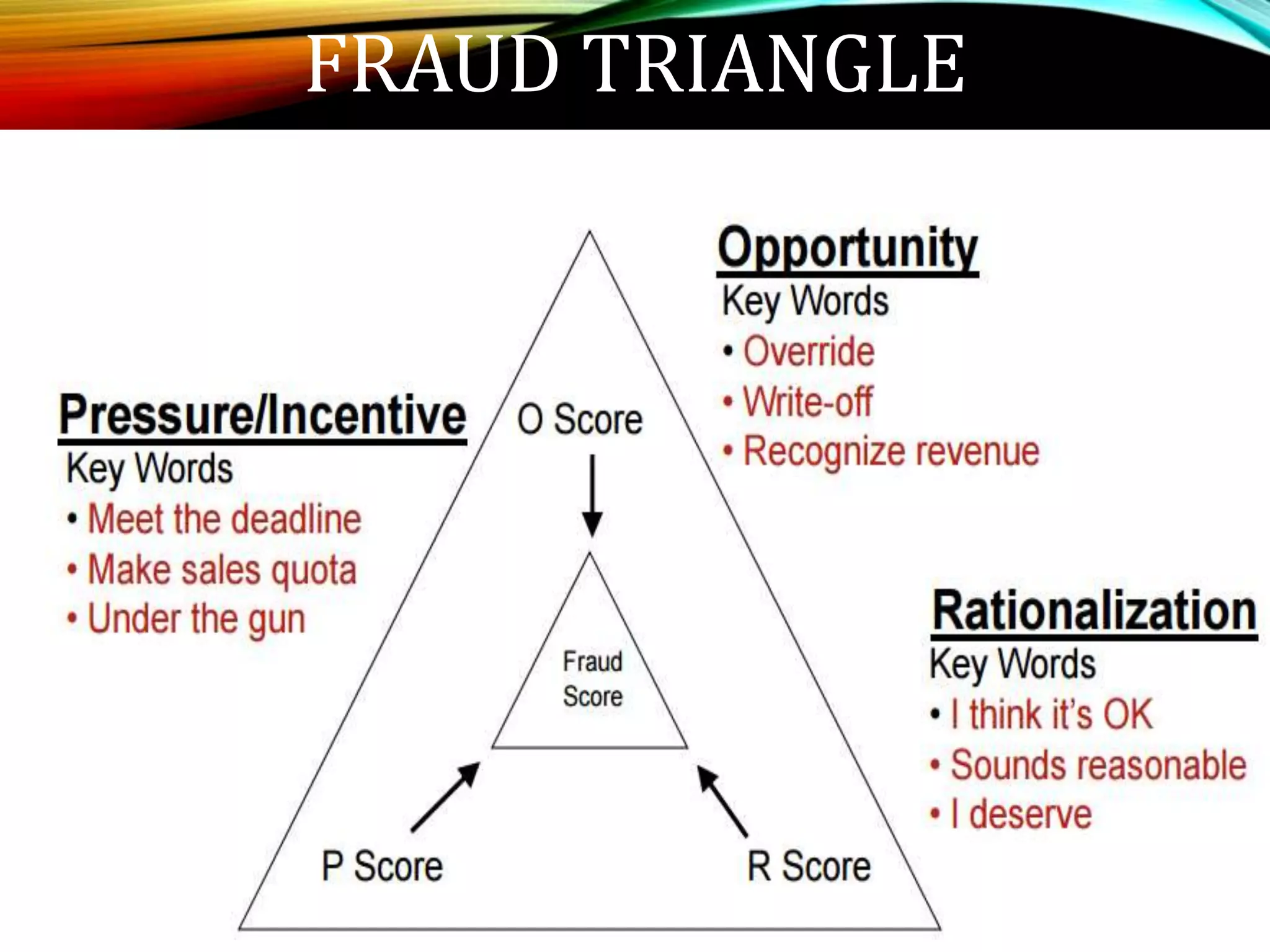

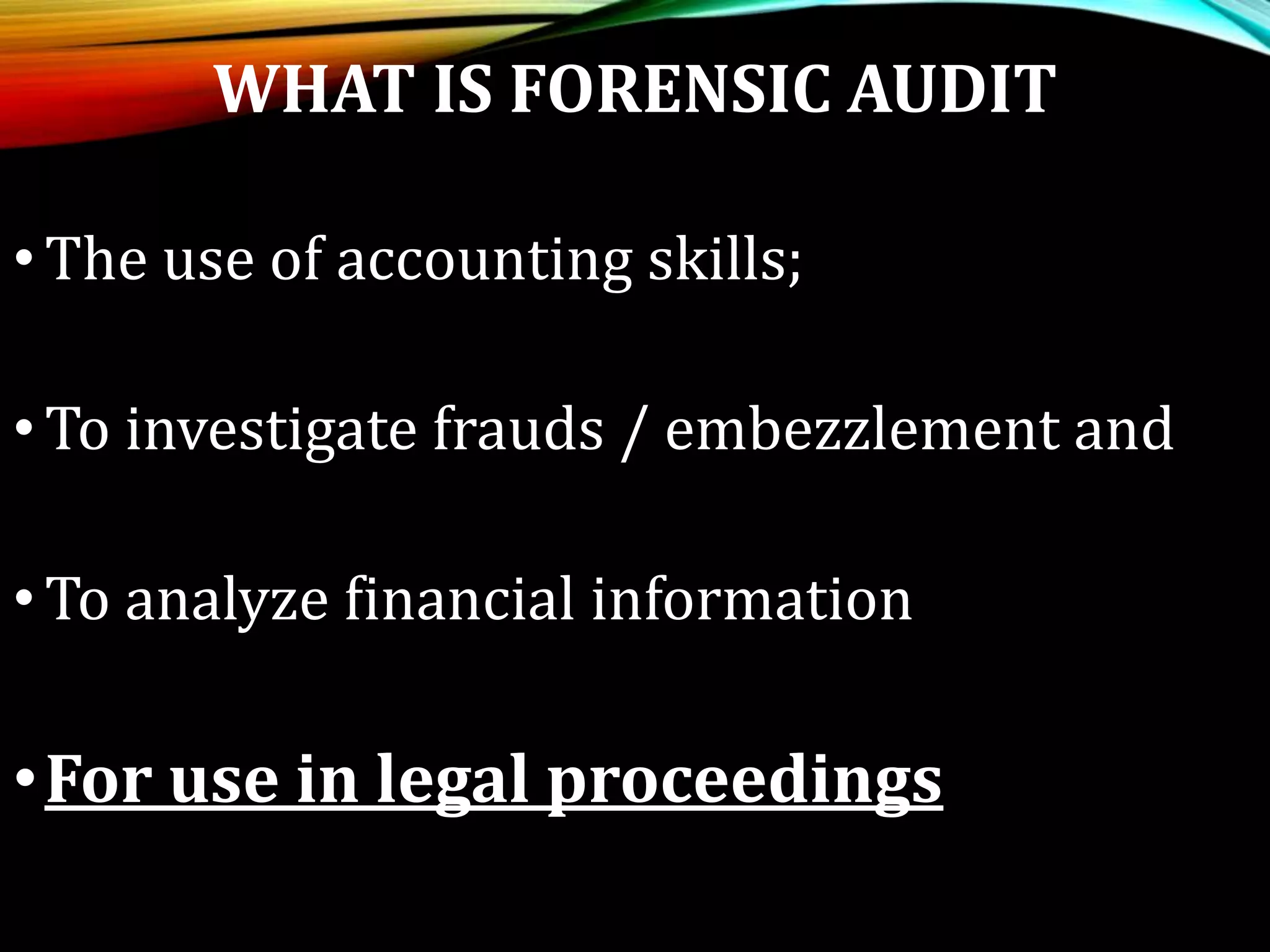

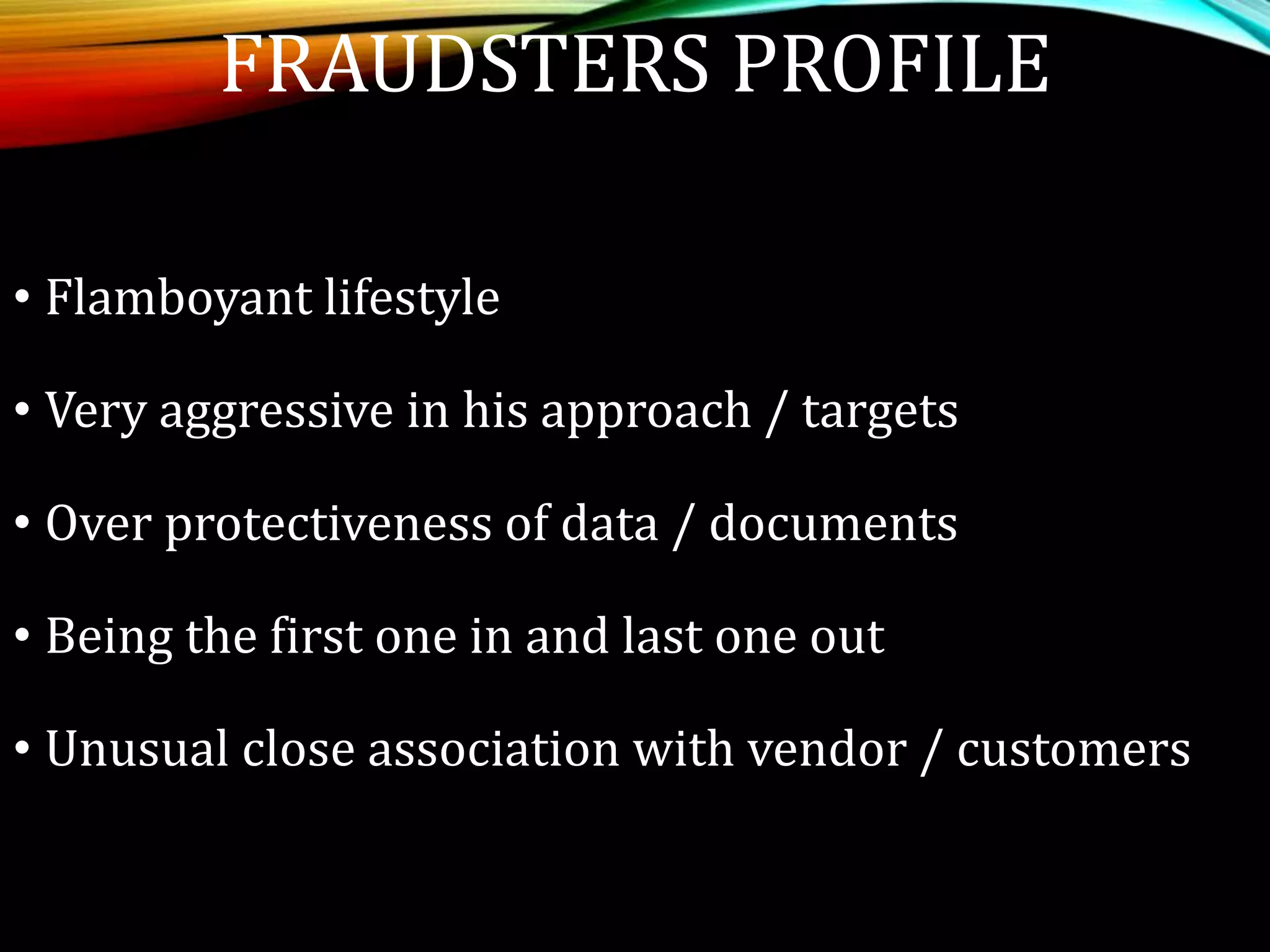

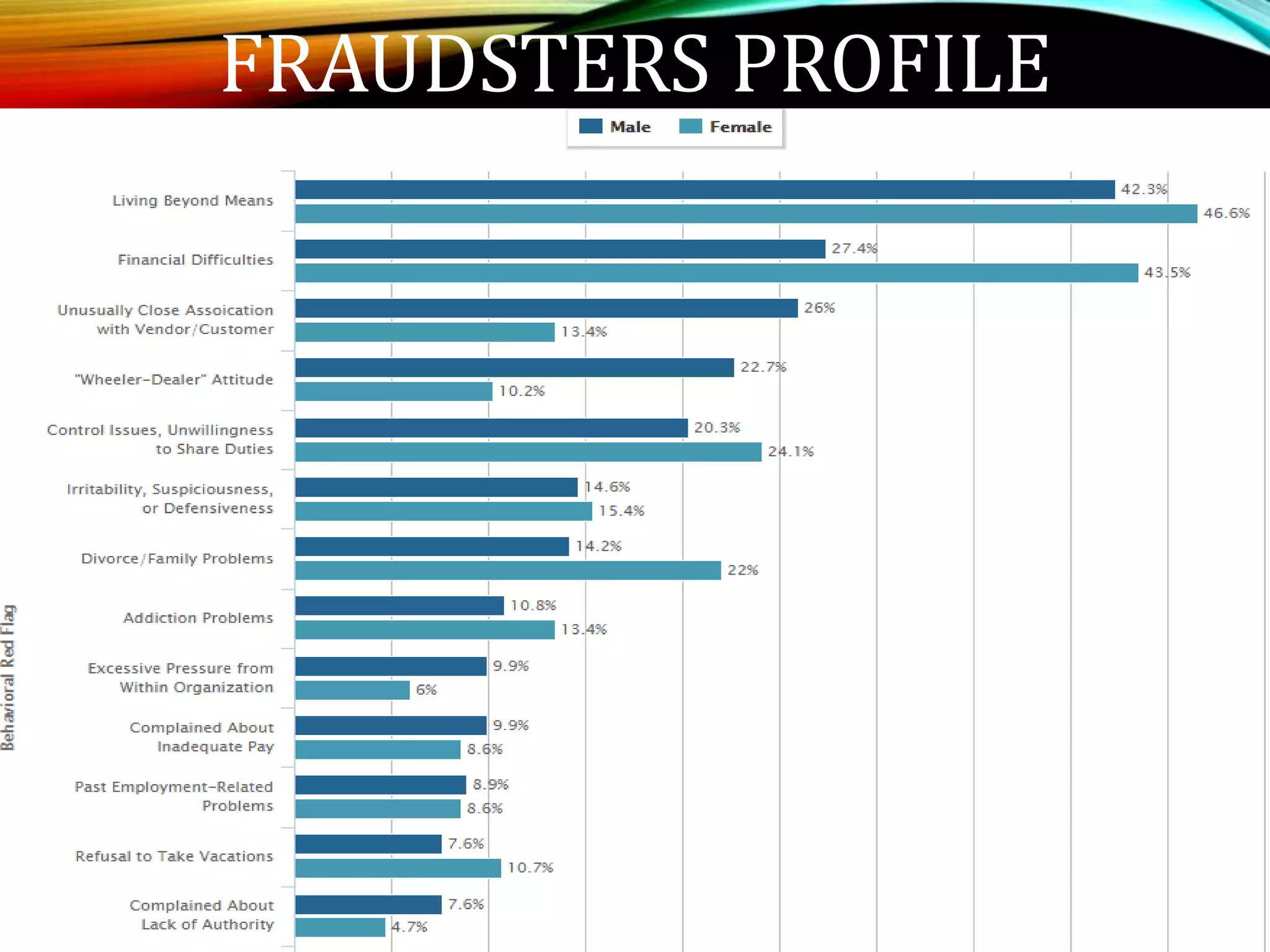

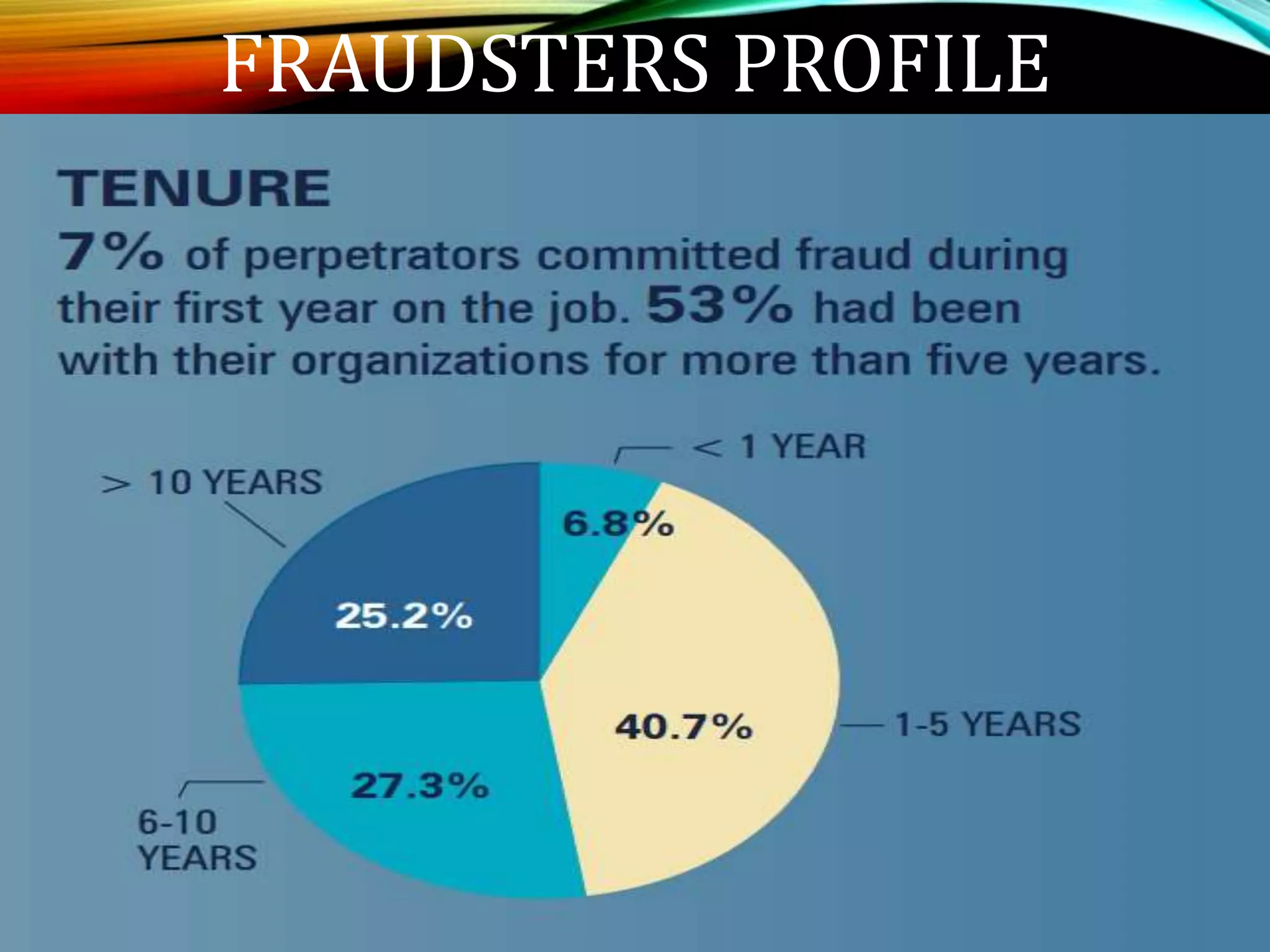

Defines fraud and forensic audit, details characteristics of fraudsters, and the necessity for careful auditing.

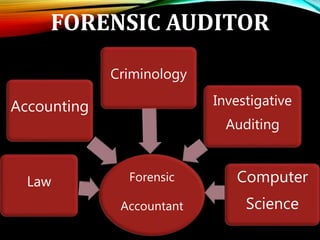

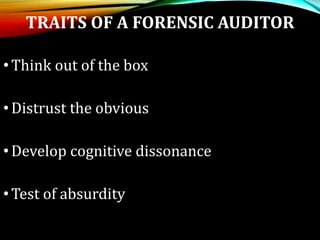

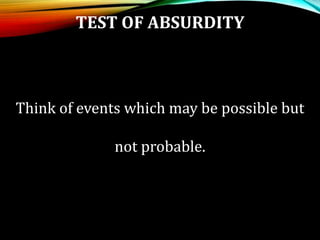

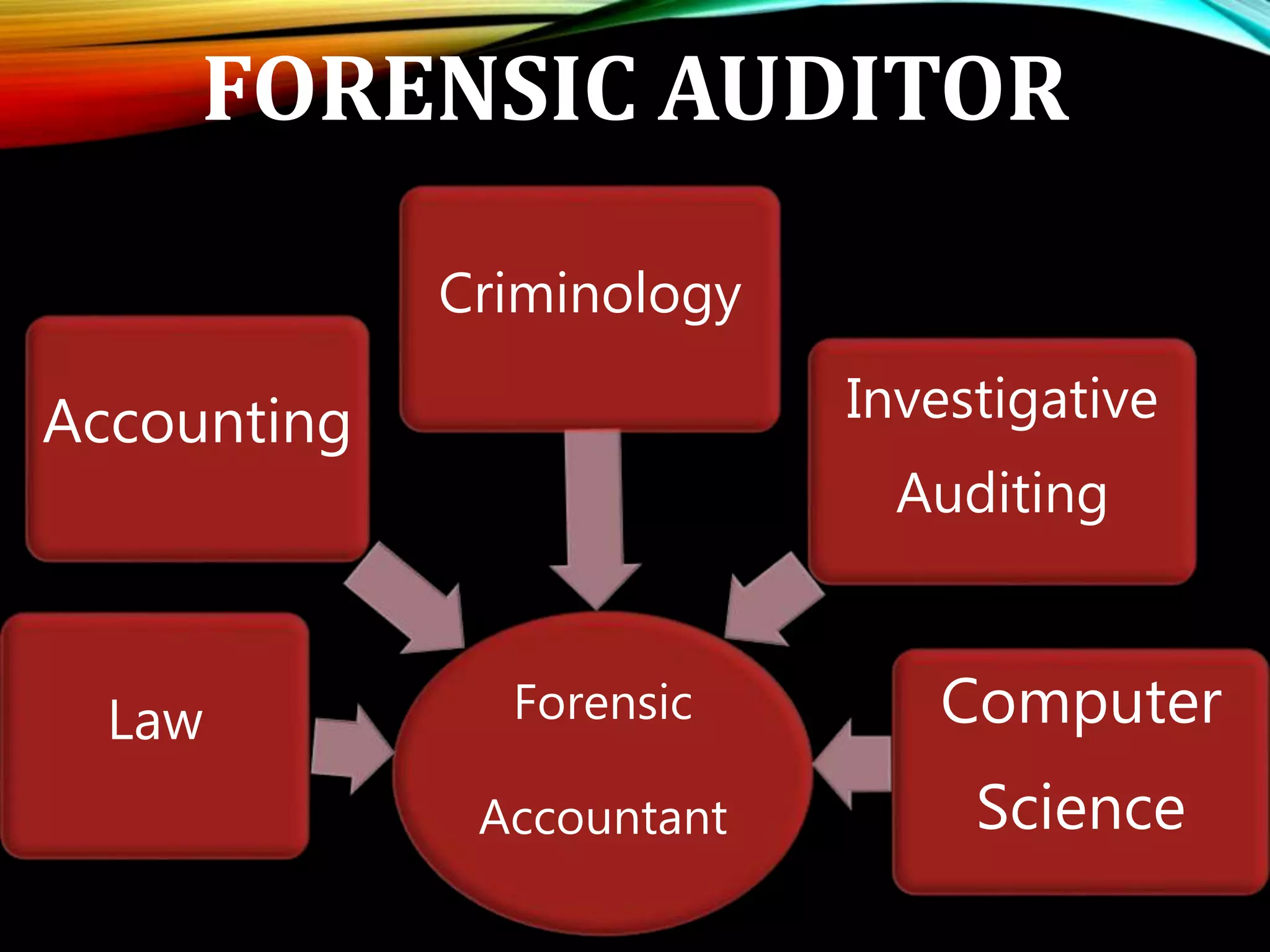

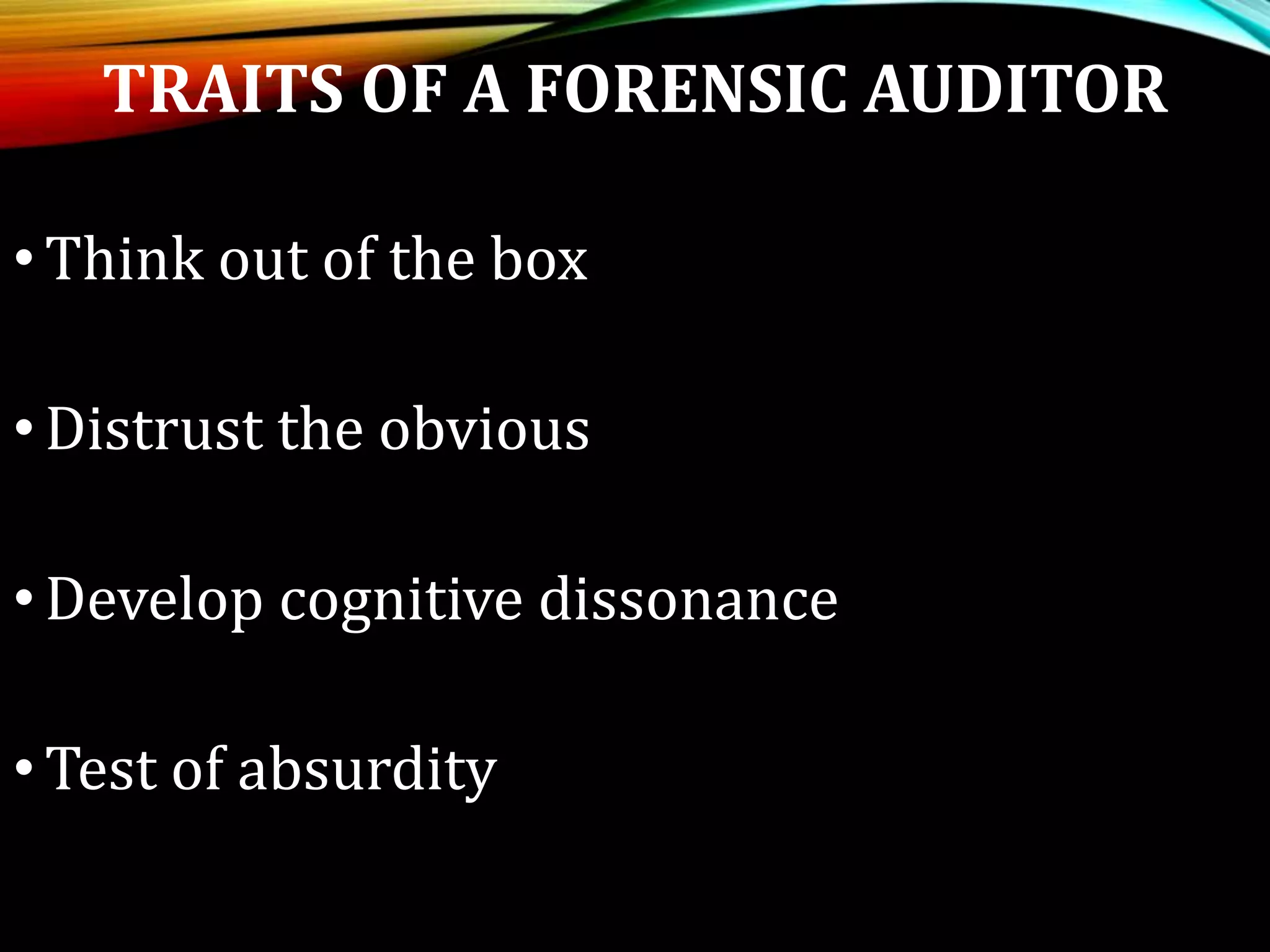

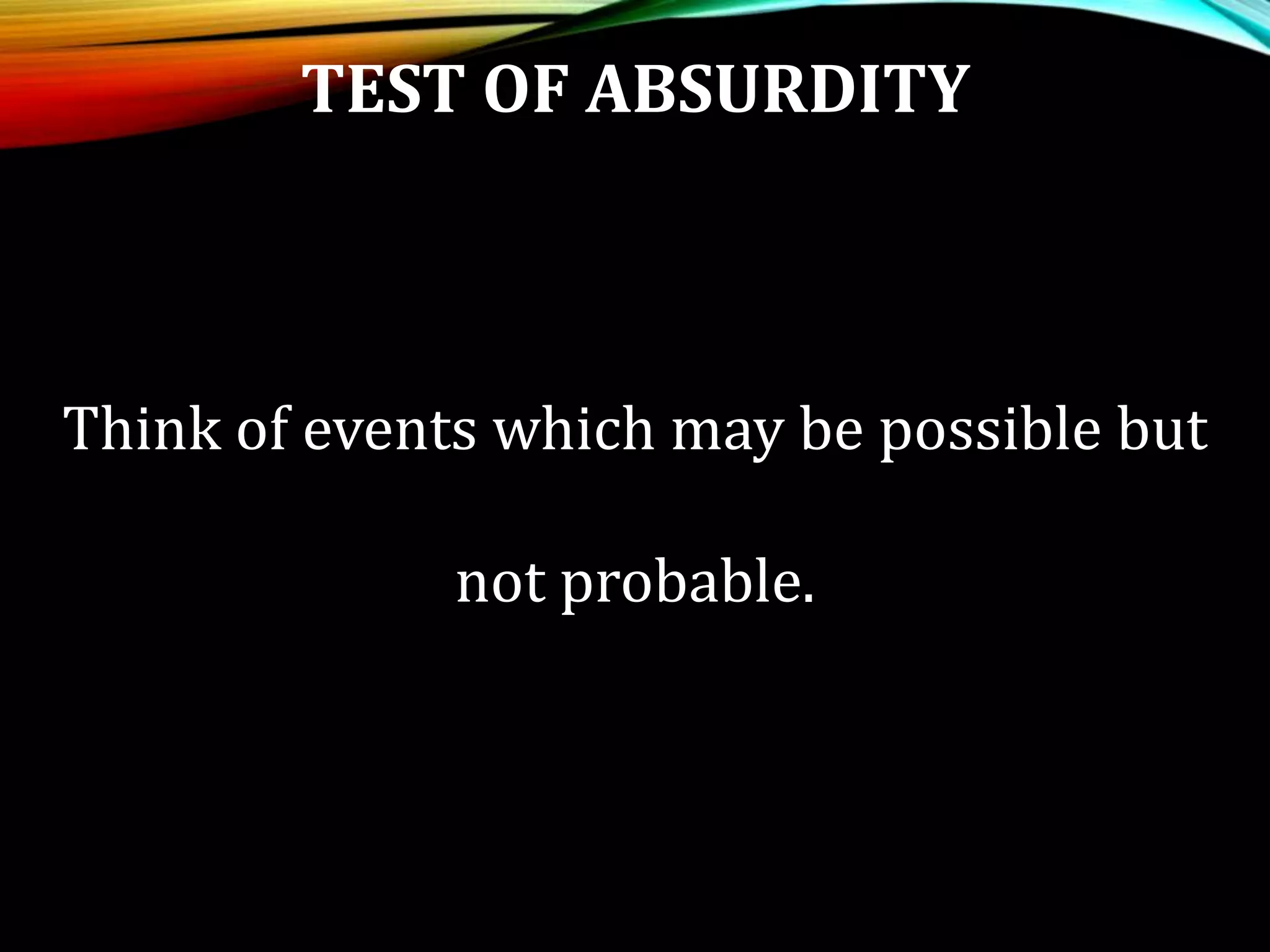

Explores essential skills and traits needed for forensic auditors to effectively detect and investigate fraud.

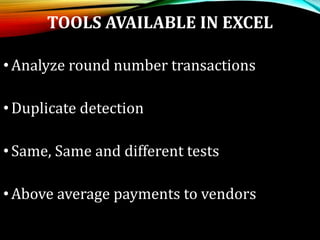

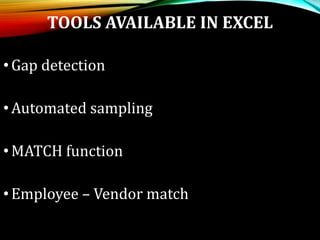

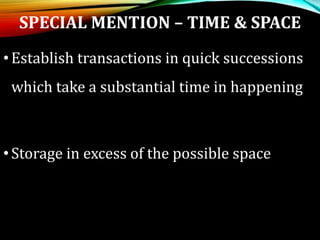

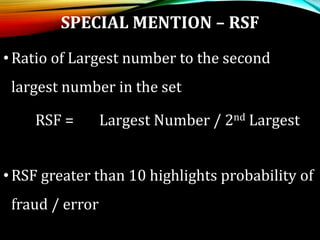

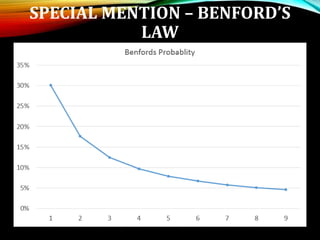

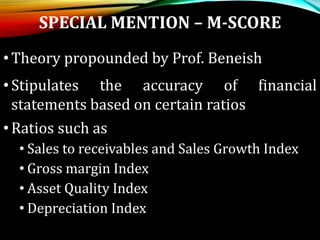

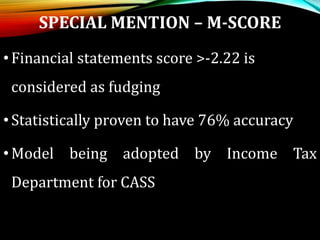

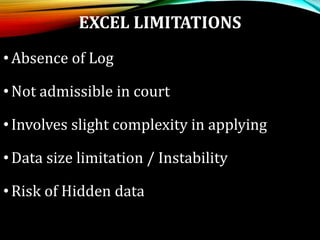

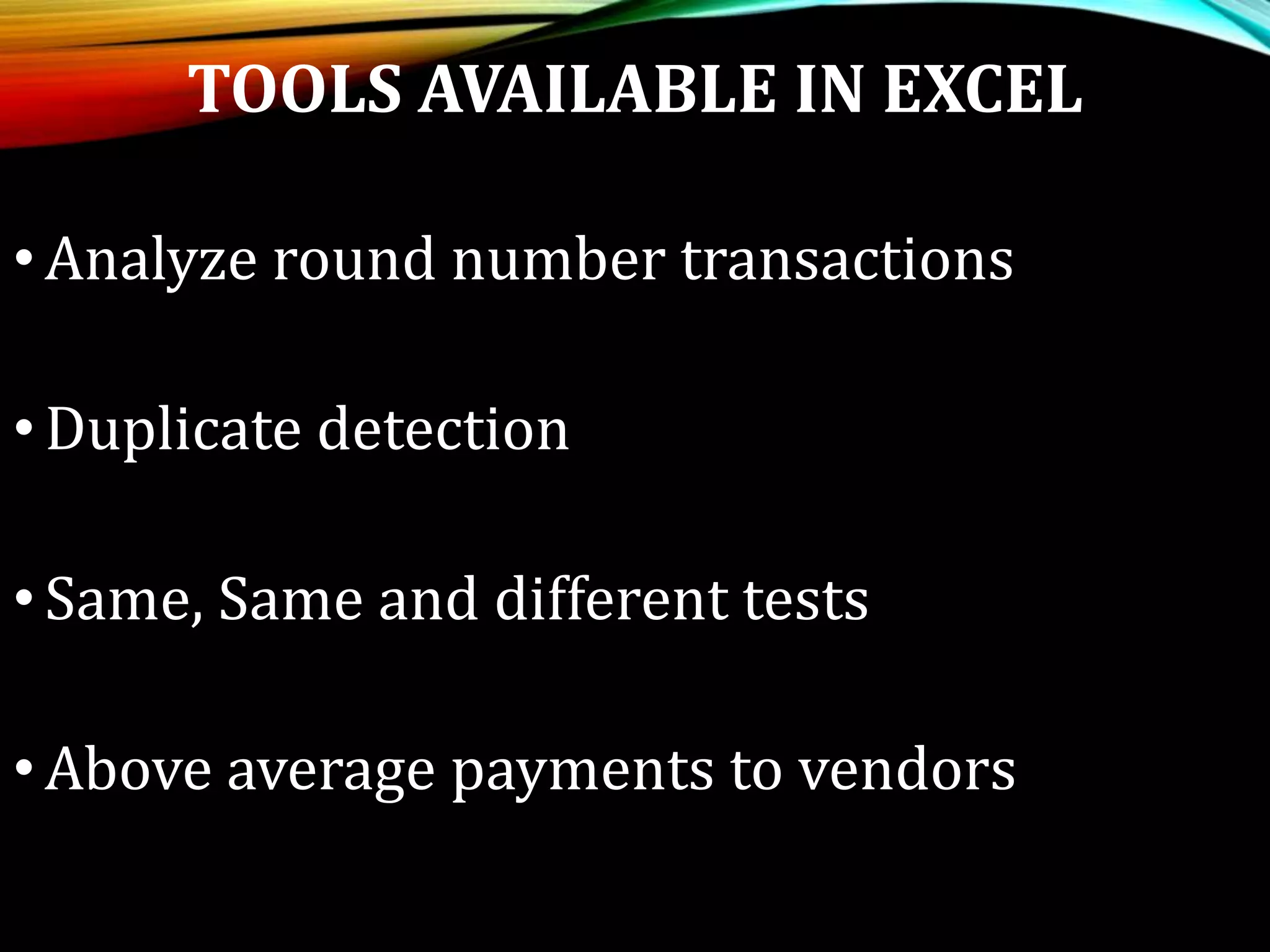

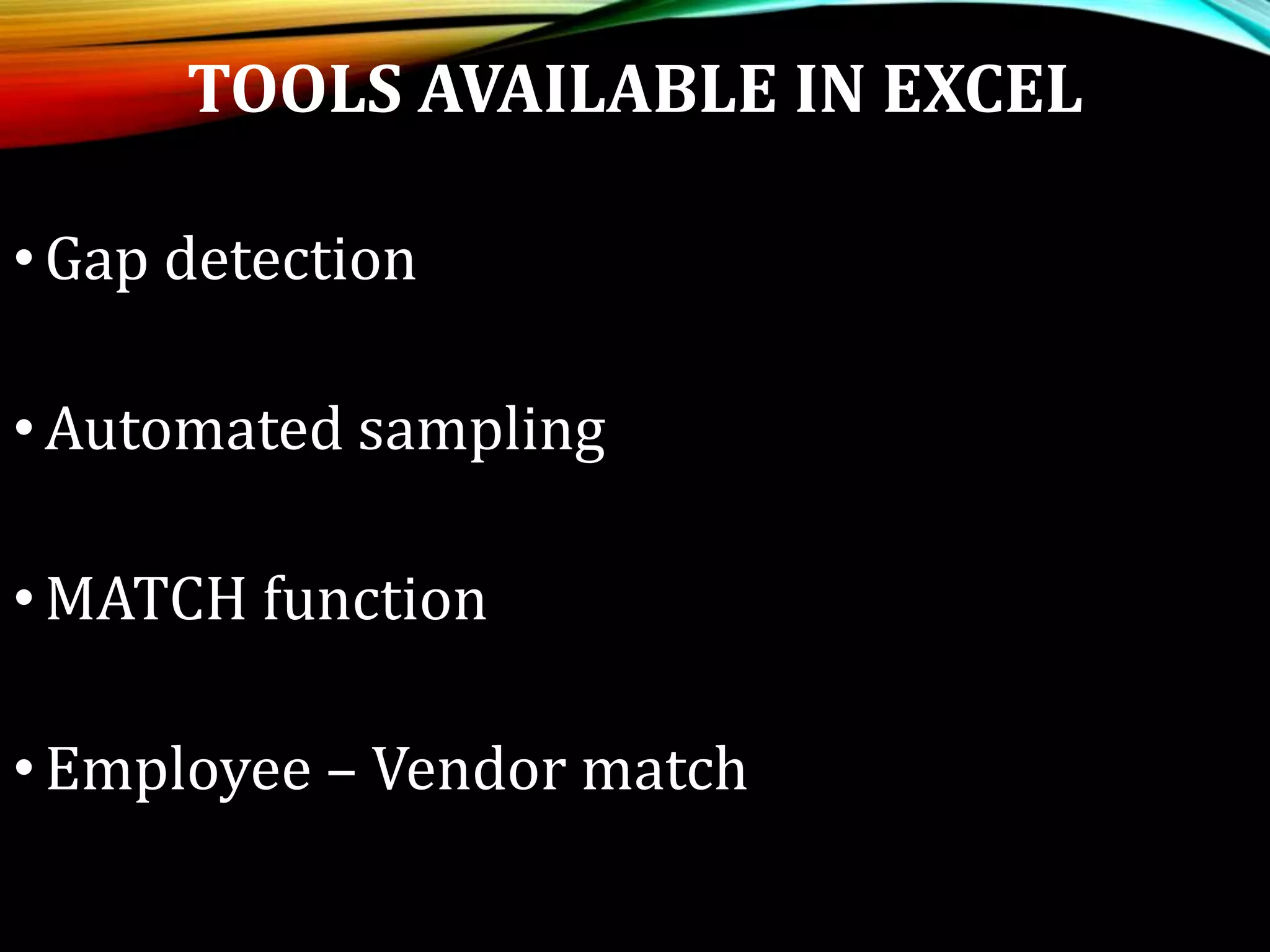

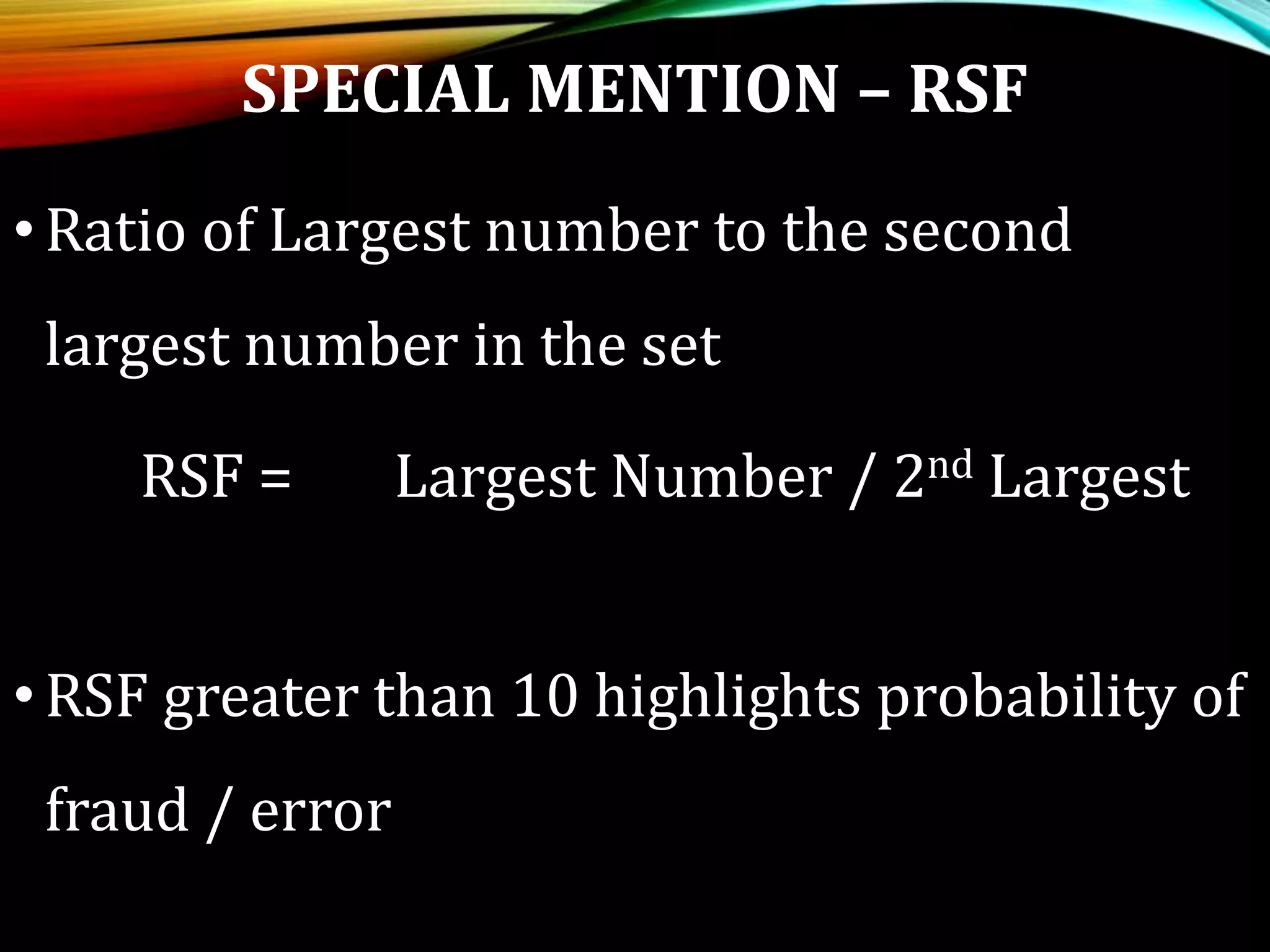

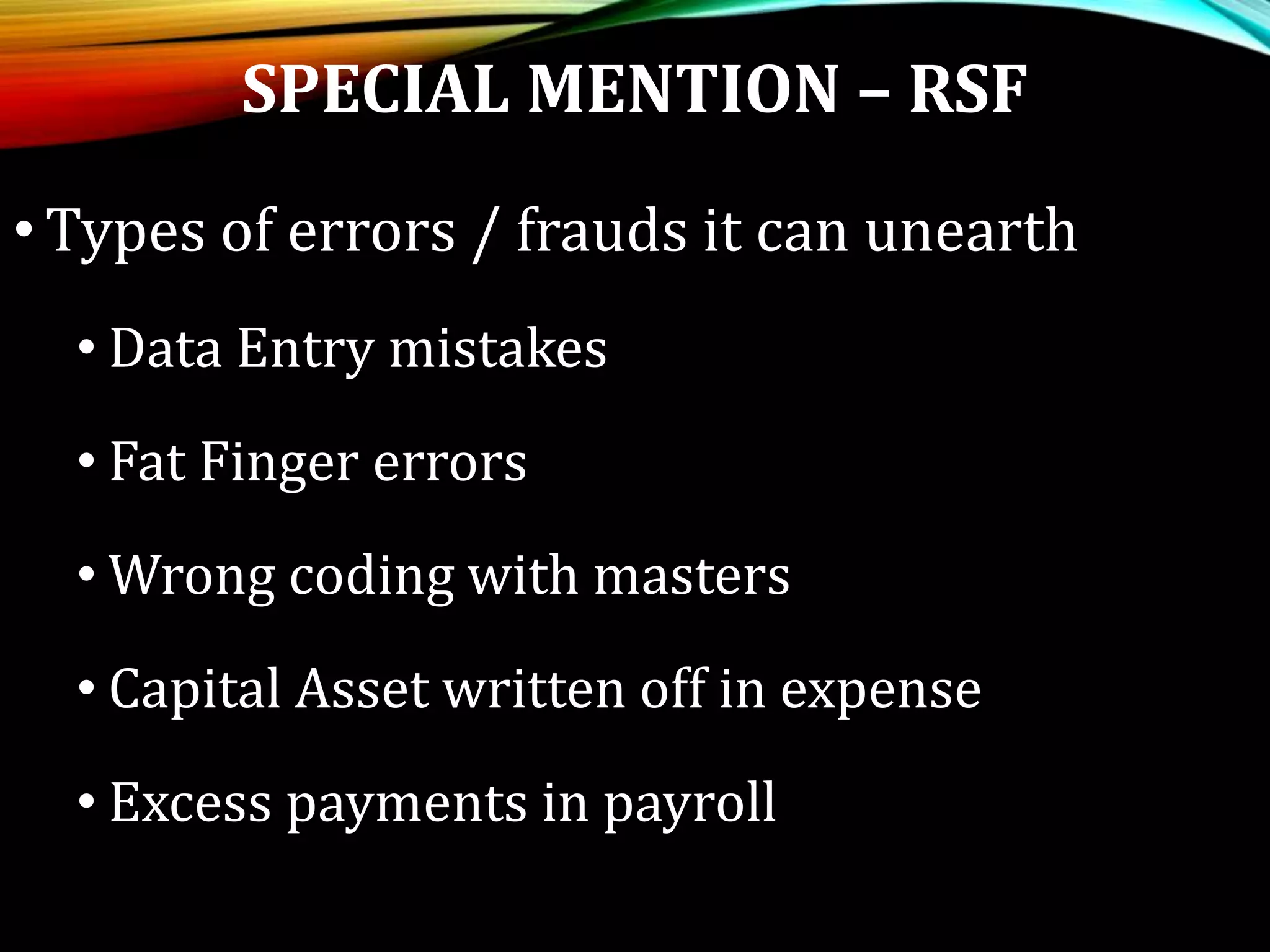

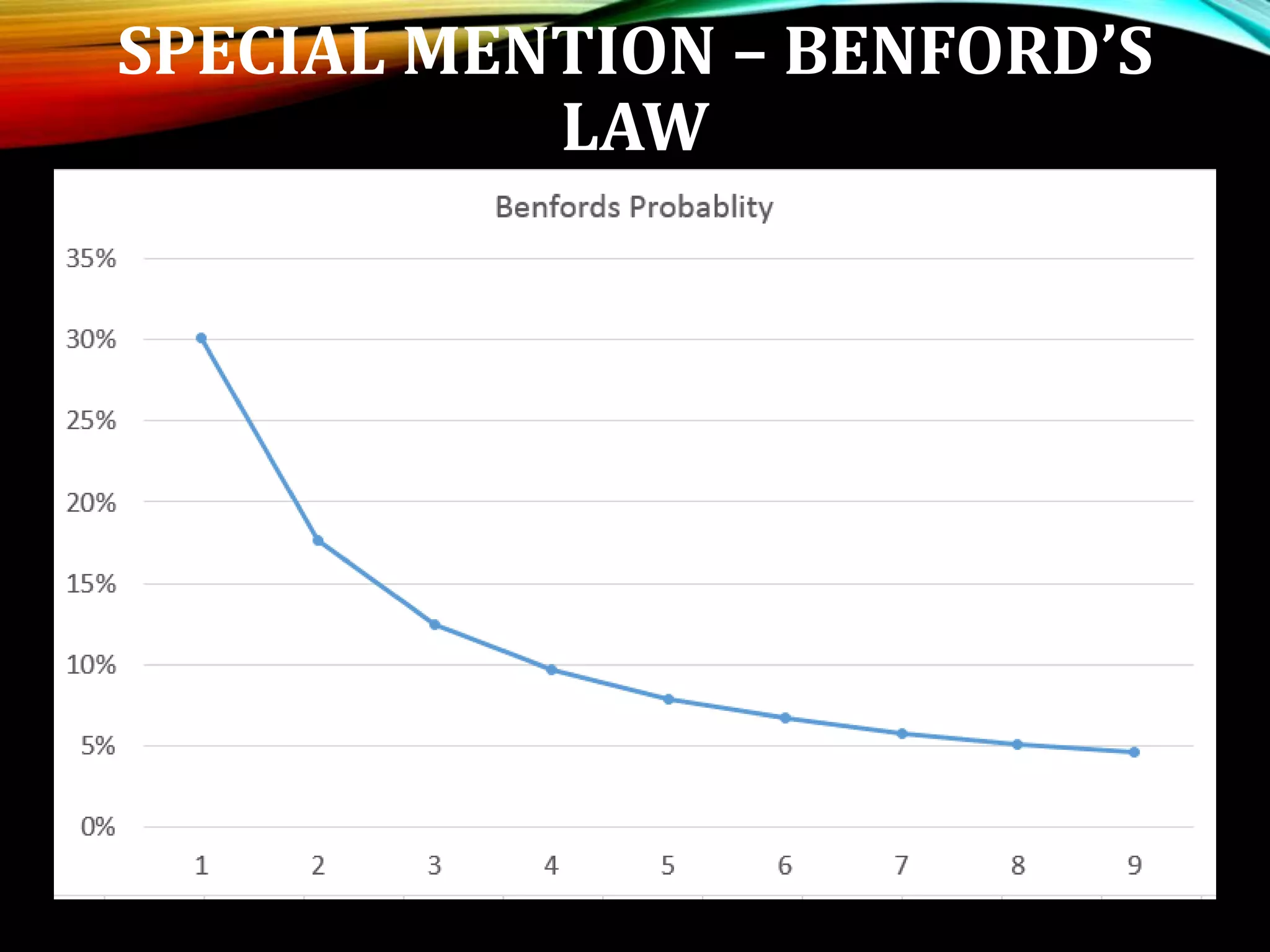

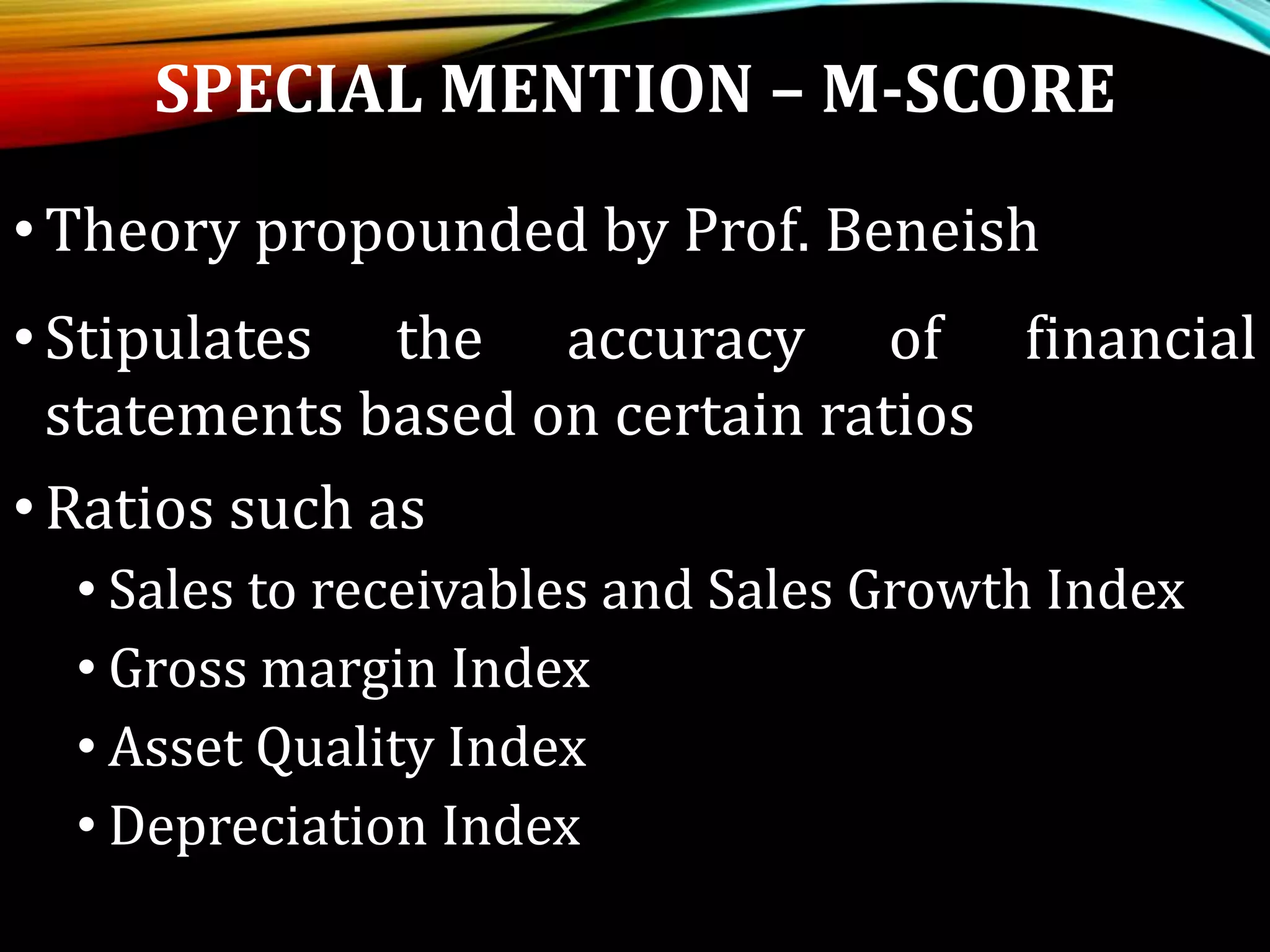

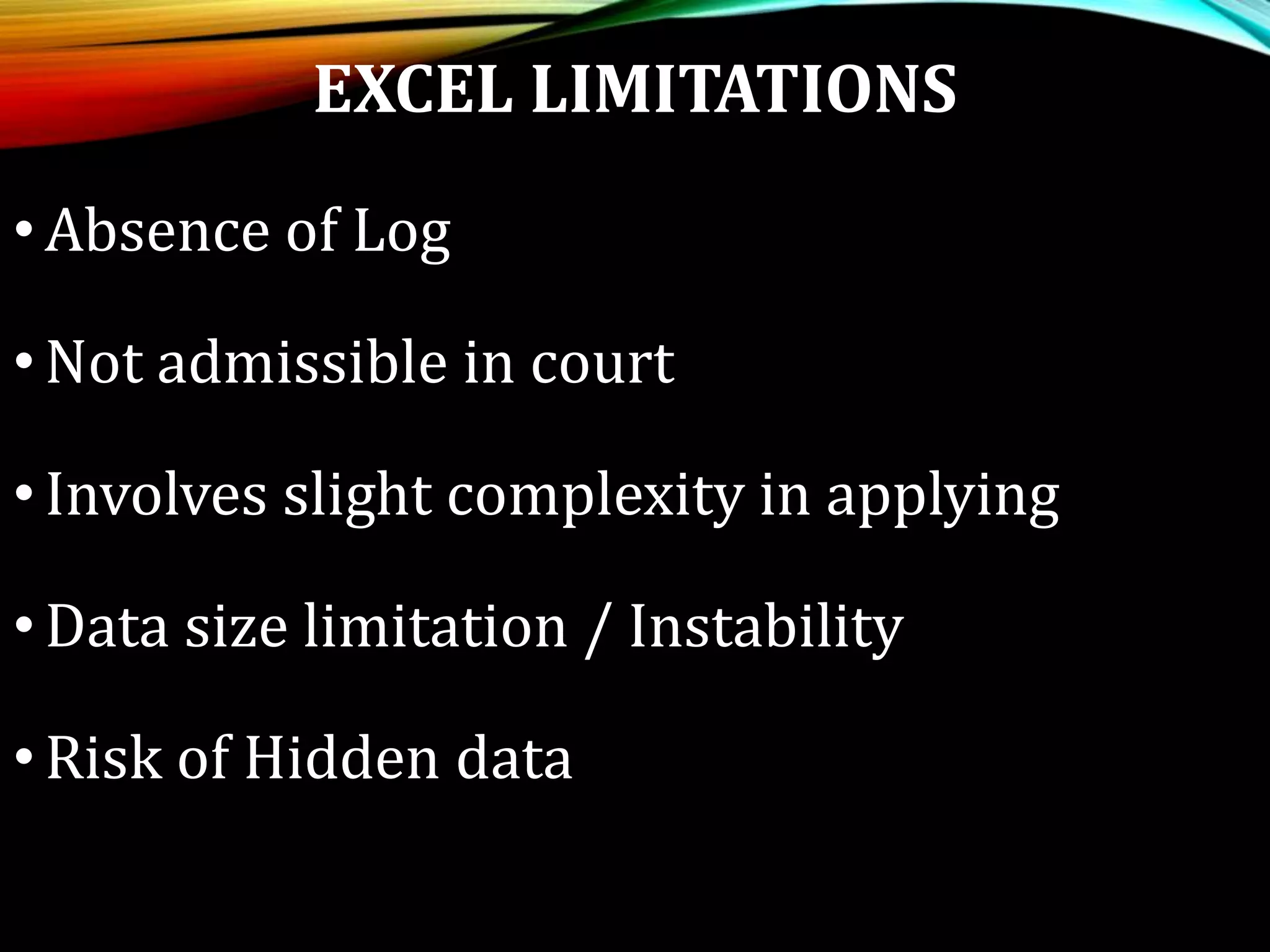

Presents tools and formulas available in Excel, such as RSF and M-Score, to assist in fraud detection.

Wrap up of the presentation with thank you note and contact information.

![Agentic Systems and Compliance - A brief intro [1.2]](https://cdn.slidesharecdn.com/ss_thumbnails/agenticsystemsandcompliace-1-251018025303-958a42ec-thumbnail.jpg?width=600ounds&width=560&fit=bounds)