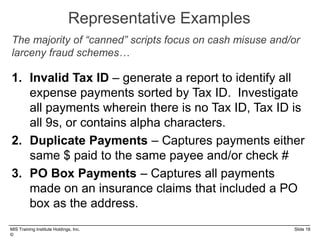

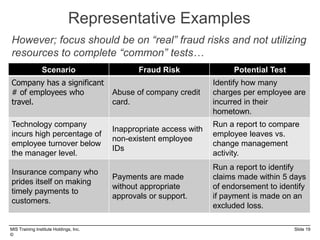

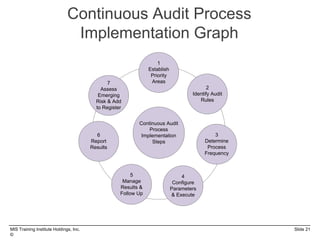

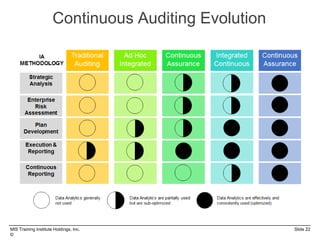

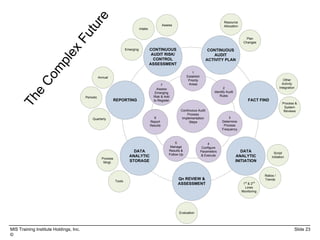

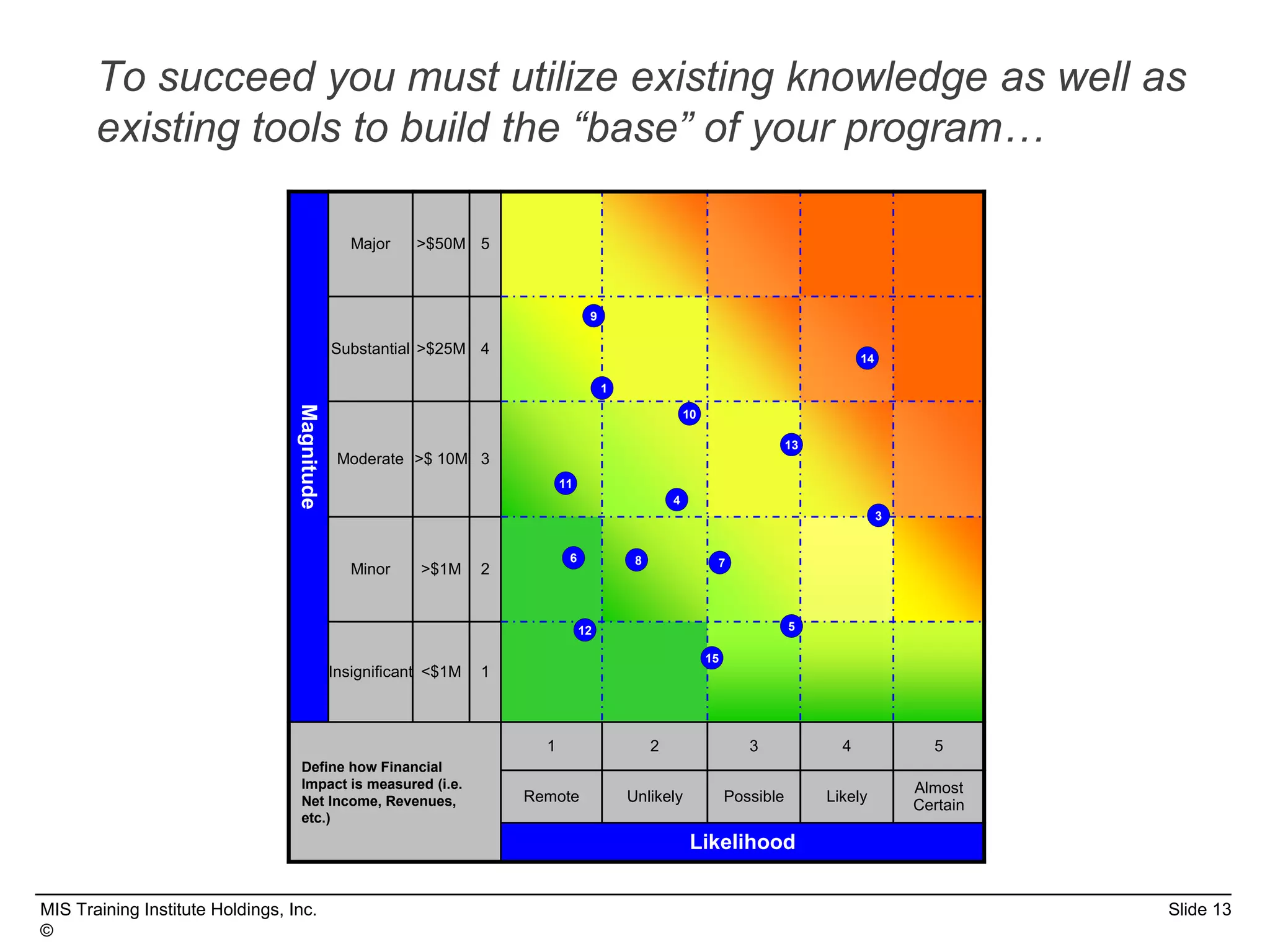

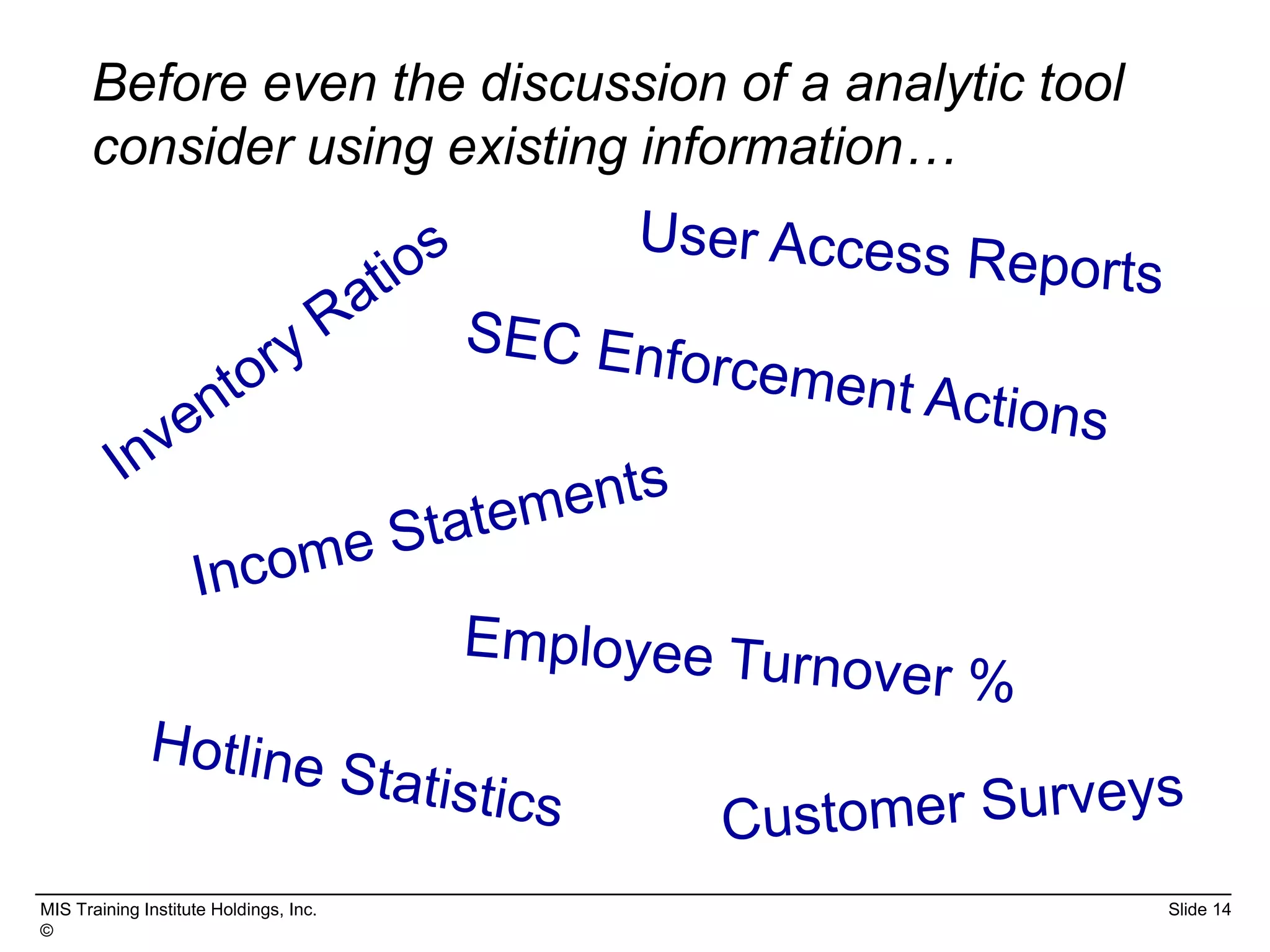

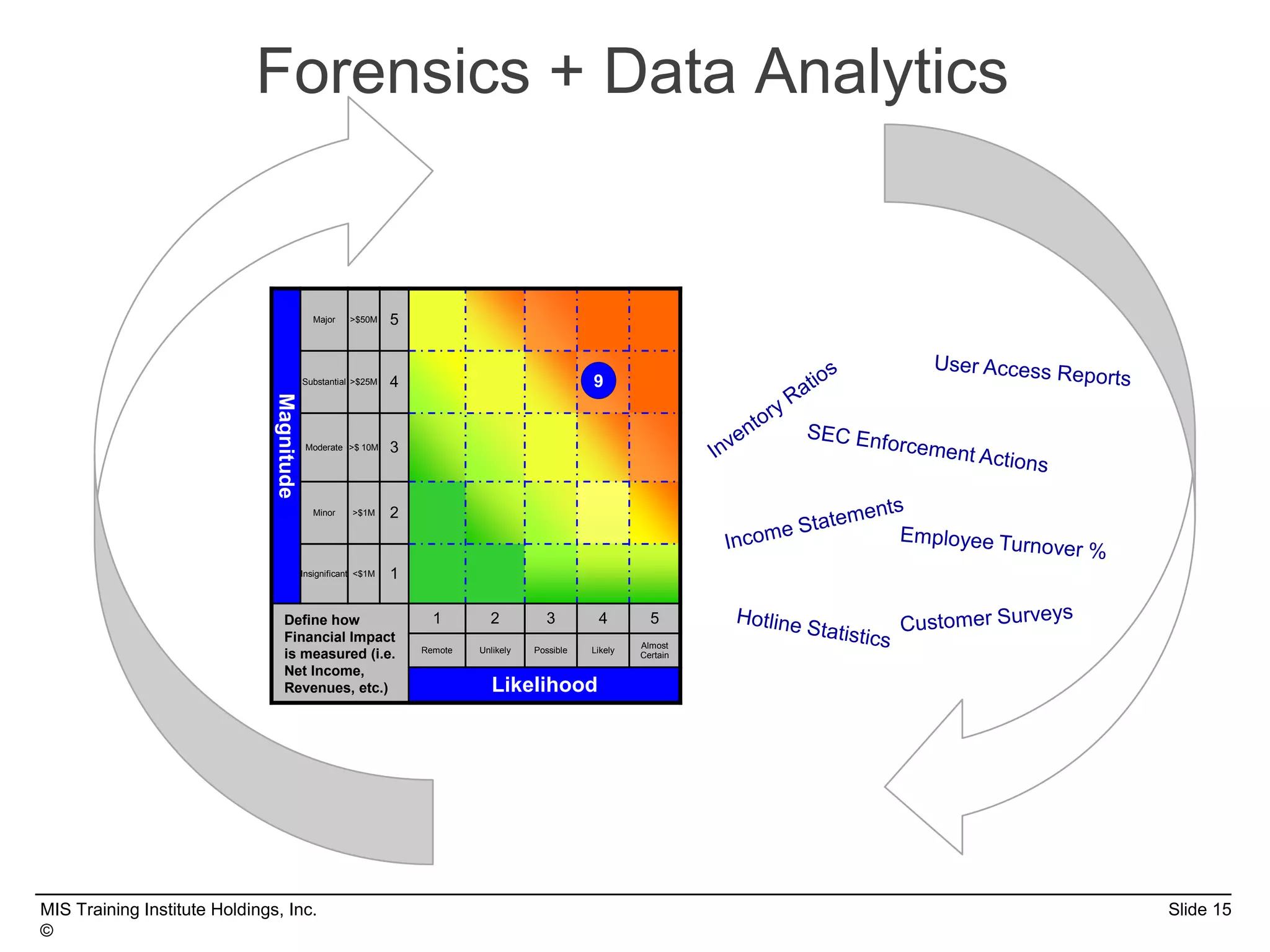

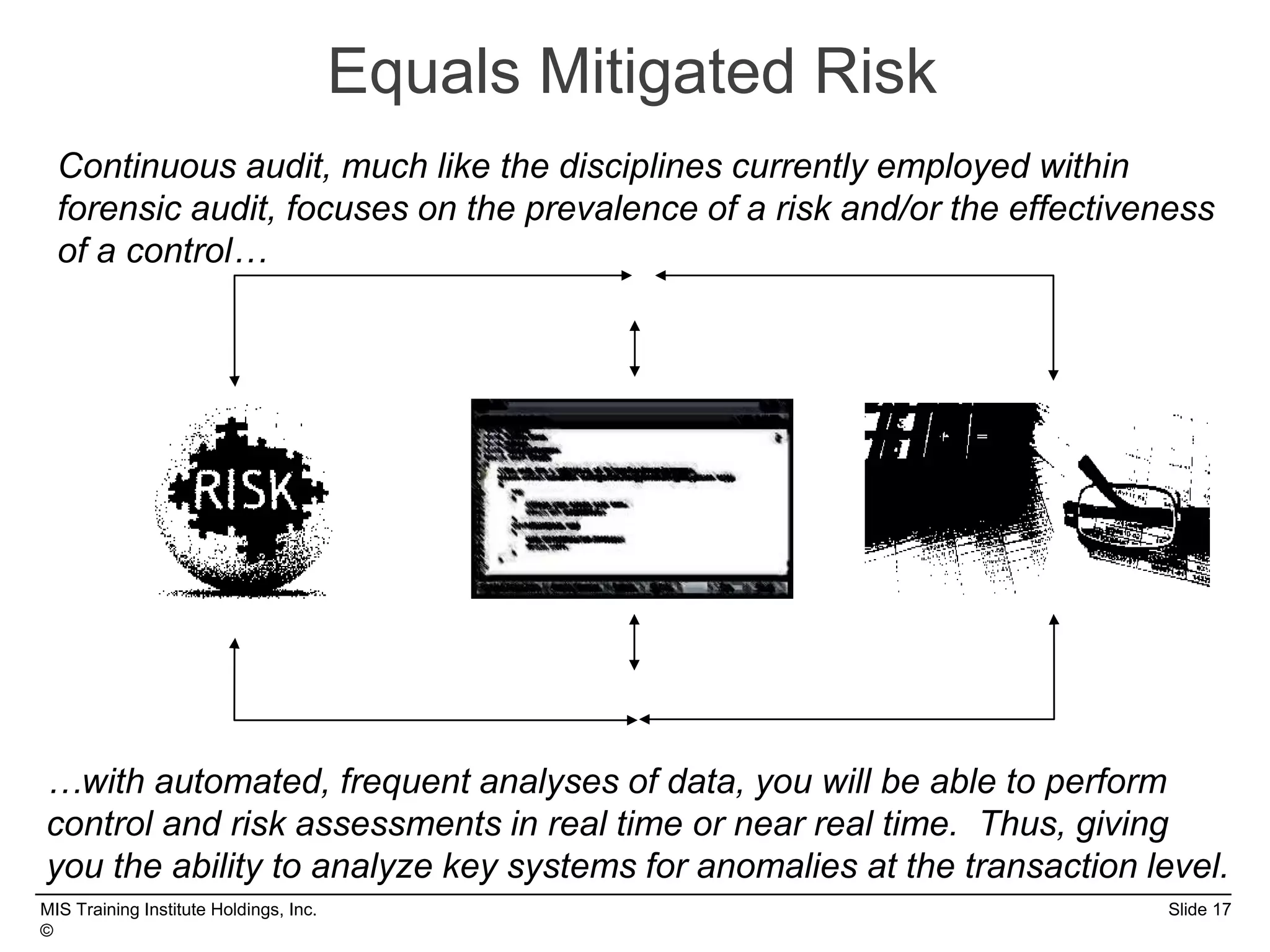

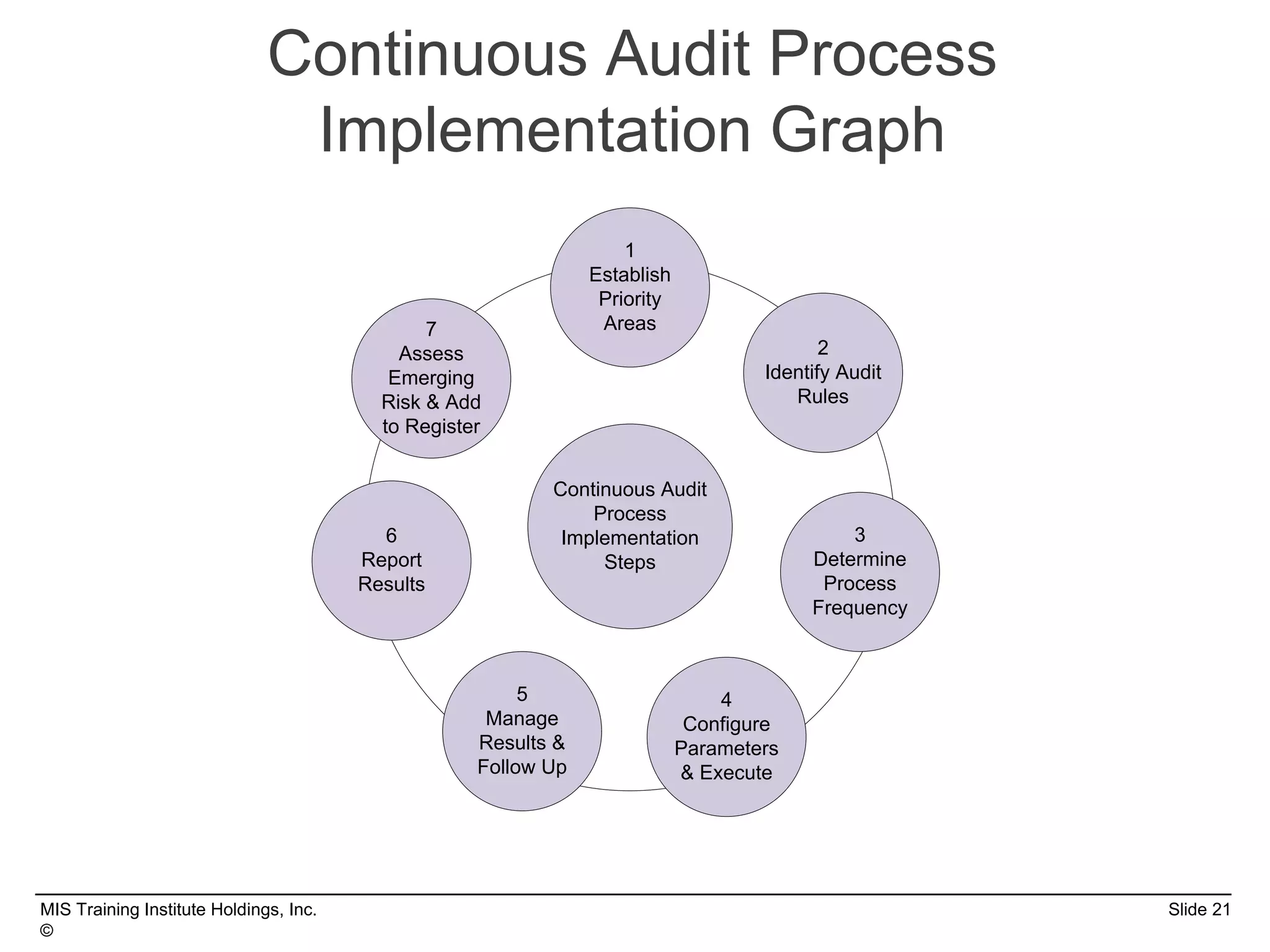

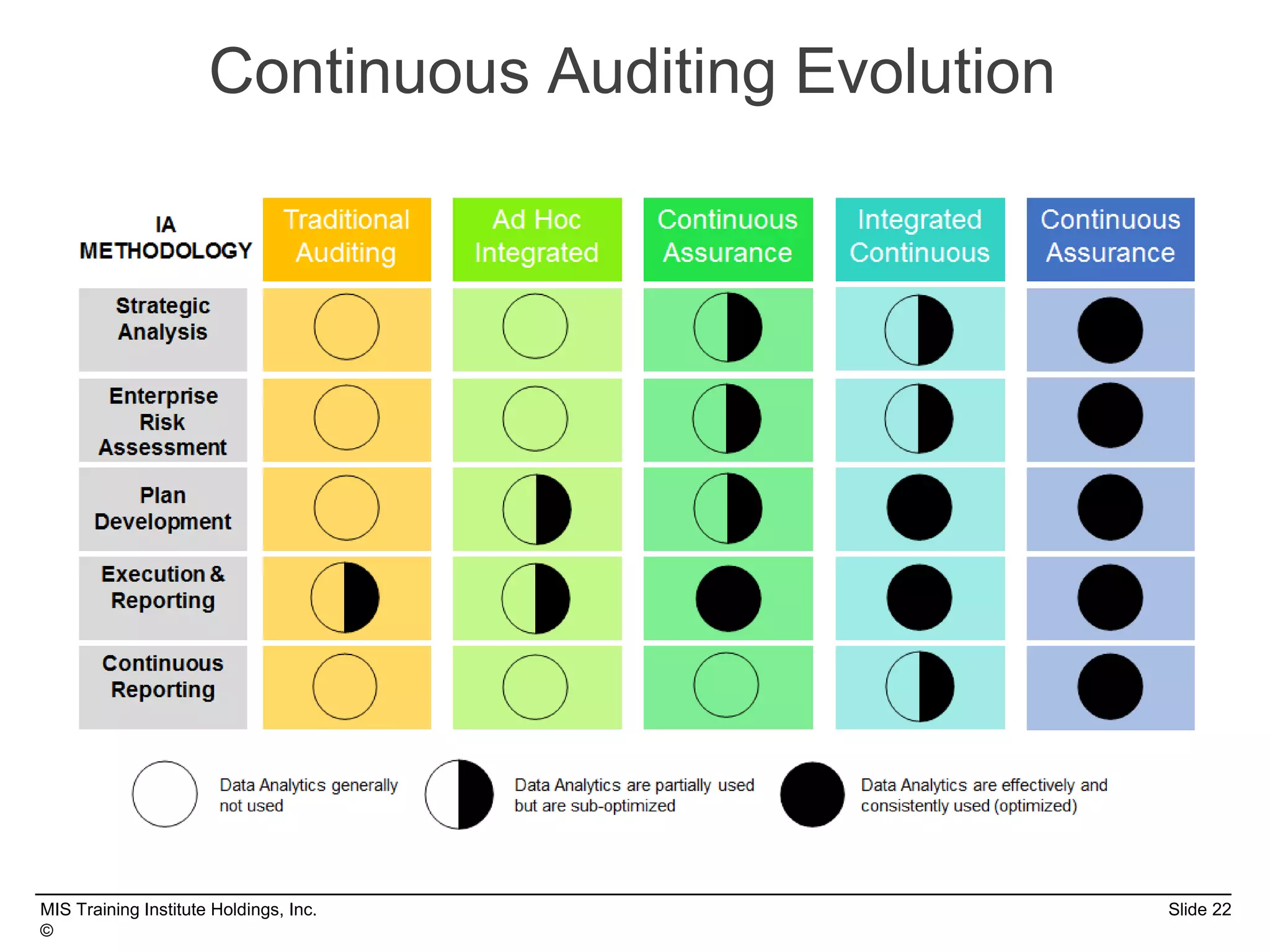

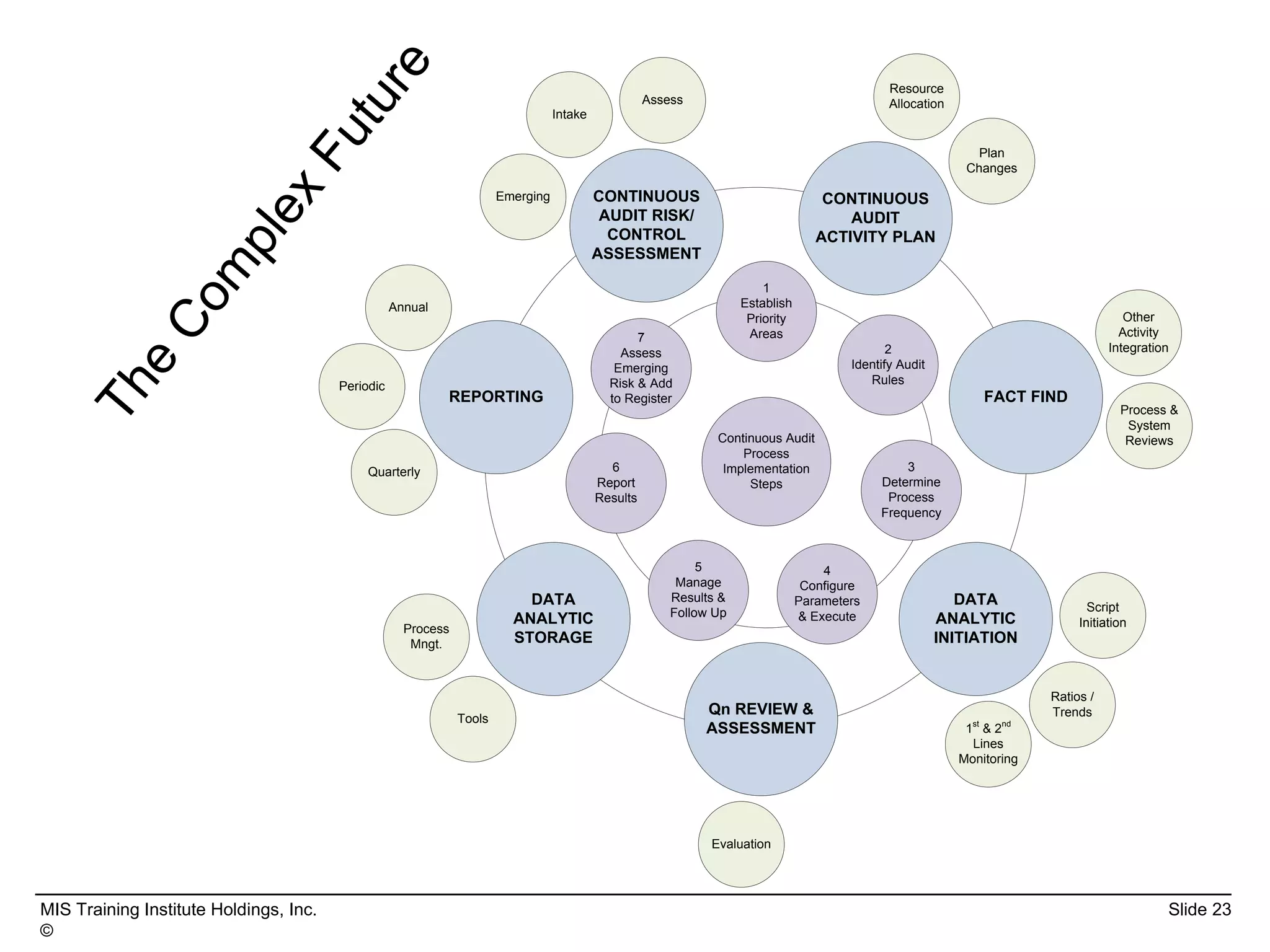

This document summarizes a presentation on merging forensics with data analytics. The presentation discusses how big data is affecting organizations and audit departments, outlines current data analytics programs and tools used, and how forensics can relate to data analytics to help mitigate risks. It also covers the evolution of continuous auditing and how data analytics may impact organizations and audit departments in the future. The key points are that data analytics can build on forensic objectives by allowing professionals to analyze large amounts of data to focus on various risks, and that continuous auditing using data analytics requires establishing priorities, identifying rules, and managing the process over time.

![Matrix and determinant URT [Autosaved].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/matrixanddeterminanturtautosaved-251018190340-9e6a6deb-thumbnail.jpg?width=600ounds&width=560&fit=bounds)

![RTP_AR_Basic_Learners' Workbook_KS2 [FOR REPRODUCTION] (1).pdf](https://cdn.slidesharecdn.com/ss_thumbnails/rtparbasiclearnersworkbookks2forreproduction1-251016024943-e51a16ac-thumbnail.jpg?width=600ounds&width=560&fit=bounds)