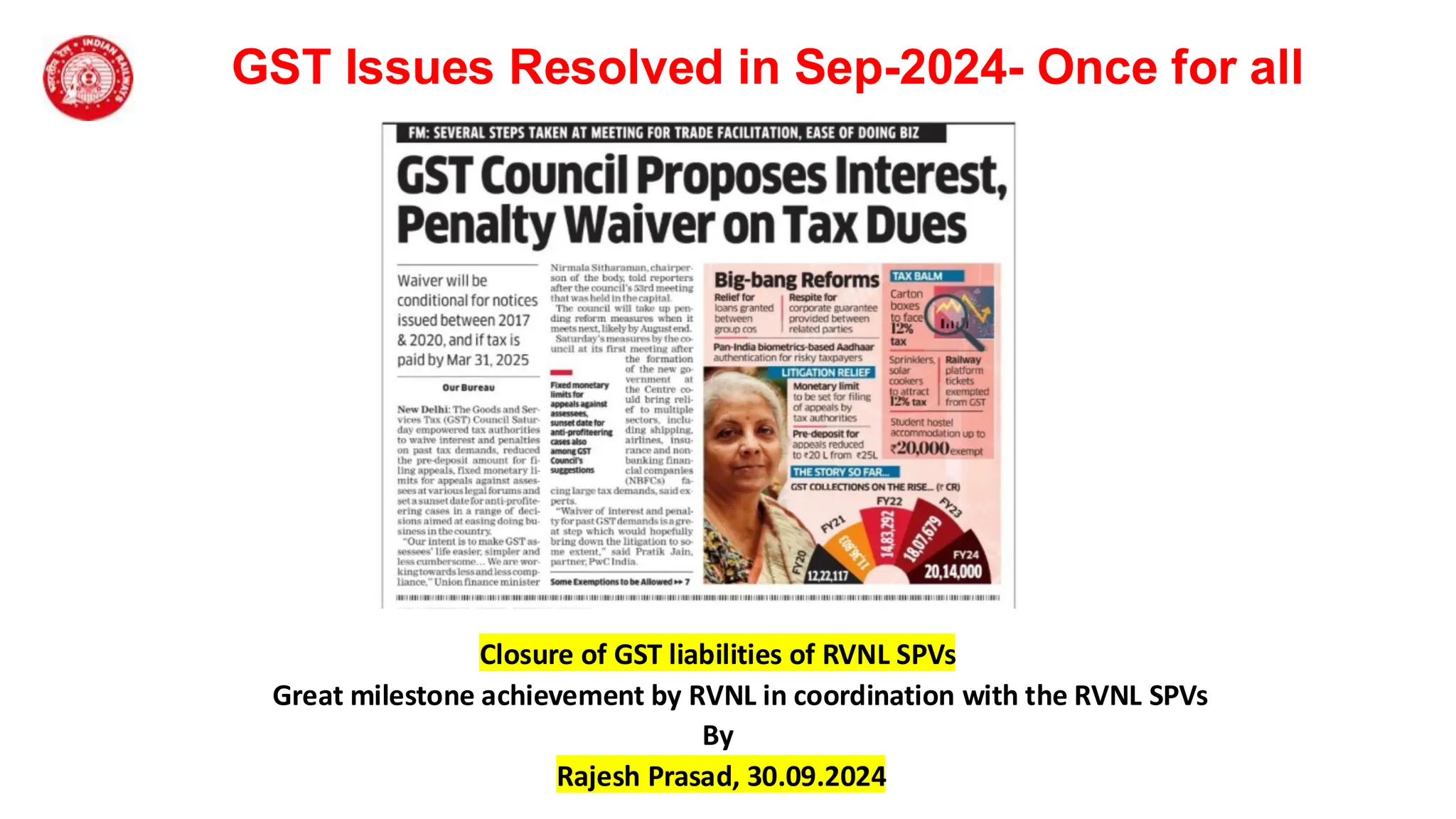

Issues related to GST were big issues and it could have destroyed the PPP model for creation of Railway Infrastructures. This document gives the details about the problem and how it got resolved.

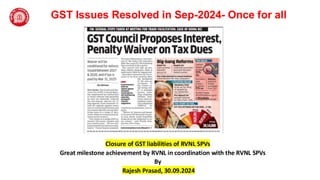

GST Issues Resolvedin Sep-2024- Once for all

Closure of GST liabilities of RVNL SPVs

Great milestone achievement by RVNL in coordination with the RVNL SPVs

By

Rajesh Prasad, 30.09.2024

2.

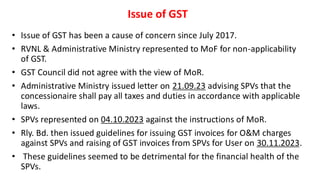

Issue of GST

•Issue of GST has been a cause of concern since July 2017.

• RVNL & Administrative Ministry represented to MoF for non-applicability

of GST.

• GST Council did not agree with the view of MoR.

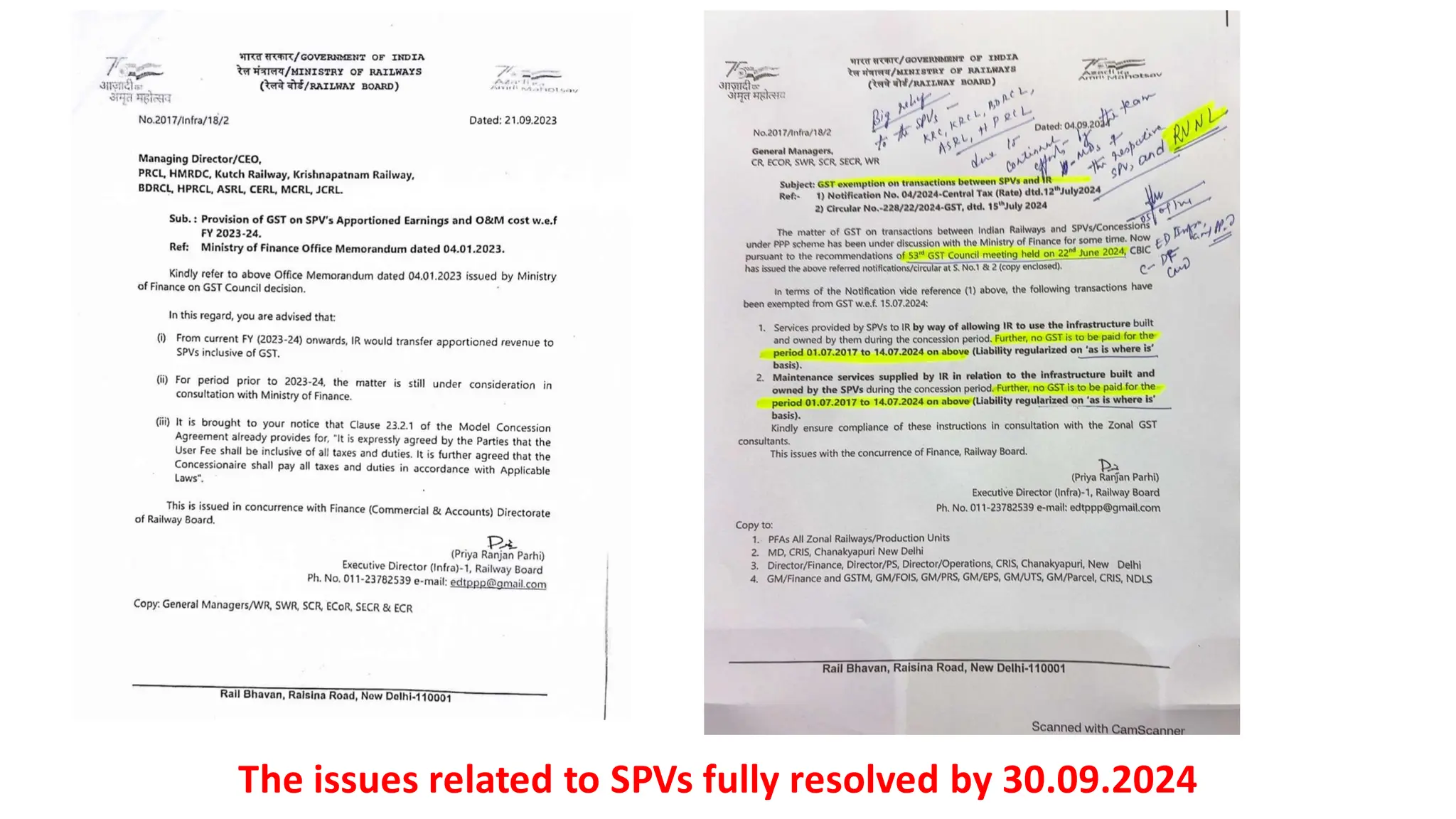

• Administrative Ministry issued letter on 21.09.23 advising SPVs that the

concessionaire shall pay all taxes and duties in accordance with applicable

laws.

• SPVs represented on 04.10.2023 against the instructions of MoR.

• Rly. Bd. then issued guidelines for issuing GST invoices for O&M charges

against SPVs and raising of GST invoices from SPVs for User on 30.11.2023.

• These guidelines seemed to be detrimental for the financial health of the

SPVs.

3.

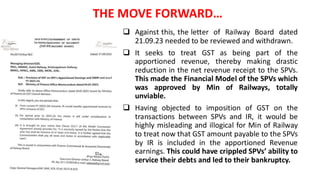

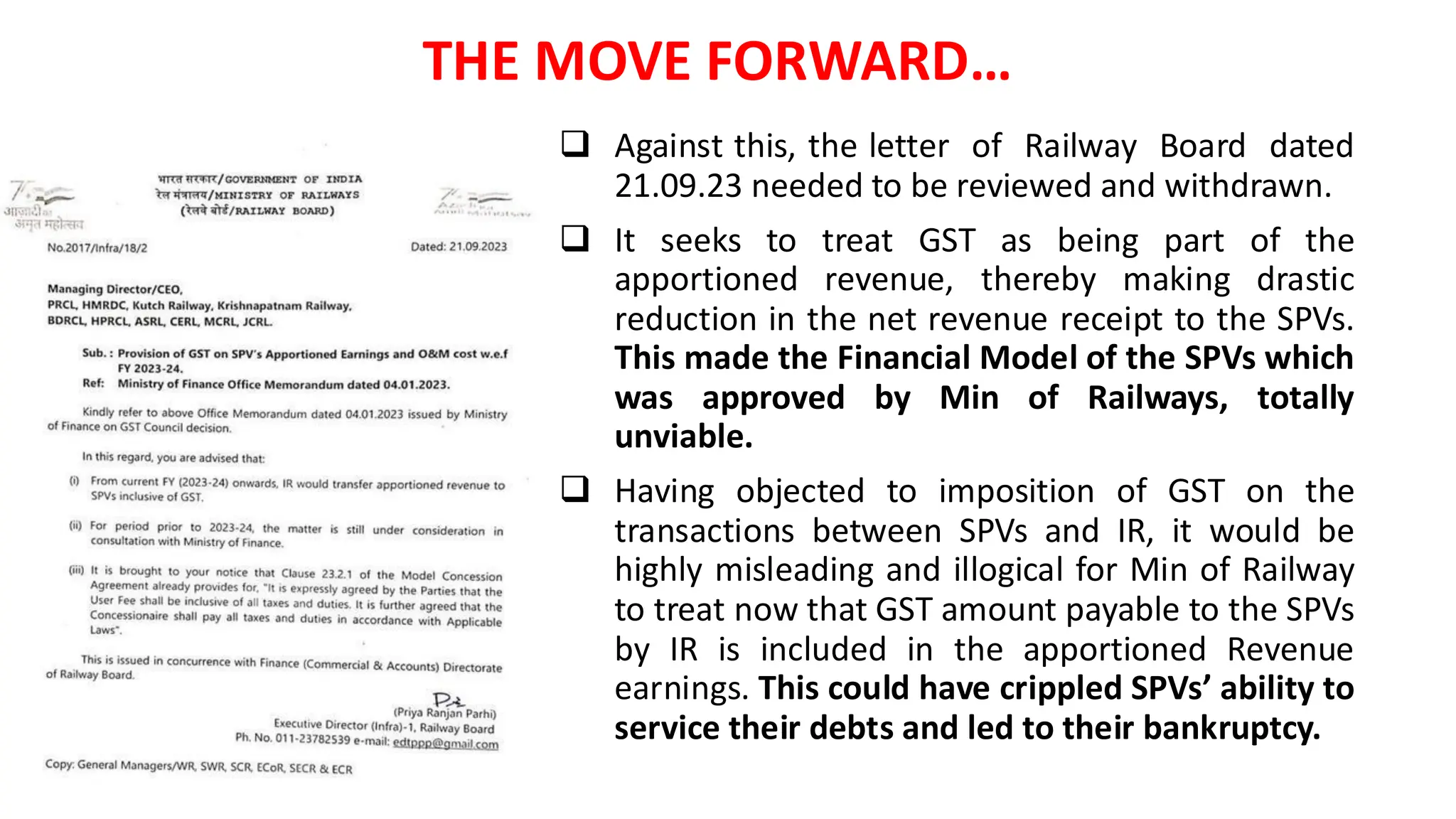

❑ Against this,the letter of Railway Board dated

21.09.23 needed to be reviewed and withdrawn.

❑ It seeks to treat GST as being part of the

apportioned revenue, thereby making drastic

reduction in the net revenue receipt to the SPVs.

This made the Financial Model of the SPVs which

was approved by Min of Railways, totally

unviable.

❑ Having objected to imposition of GST on the

transactions between SPVs and IR, it would be

highly misleading and illogical for Min of Railway

to treat now that GST amount payable to the SPVs

by IR is included in the apportioned Revenue

earnings. This could have crippled SPVs’ ability to

service their debts and led to their bankruptcy.

THE MOVE FORWARD…

4.

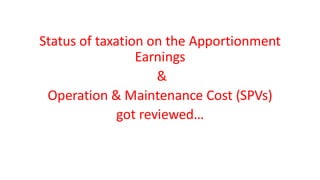

Status of taxationon the Apportionment

Earnings

&

Operation & Maintenance Cost (SPVs)

got reviewed…

5.

Brief background forthe fight..

Concession Agreement:

SPVs have right to receive from MoR- its share in accordance with

the rules of inter-railway apportionment of earnings, of the tariff

collected from the freight traffic originating, terminating and

moving on the Project Railway, including haulage charges collected

from container operations, after deduction of Operations and

maintenance costs, in accordance with the Project Related

Agreements

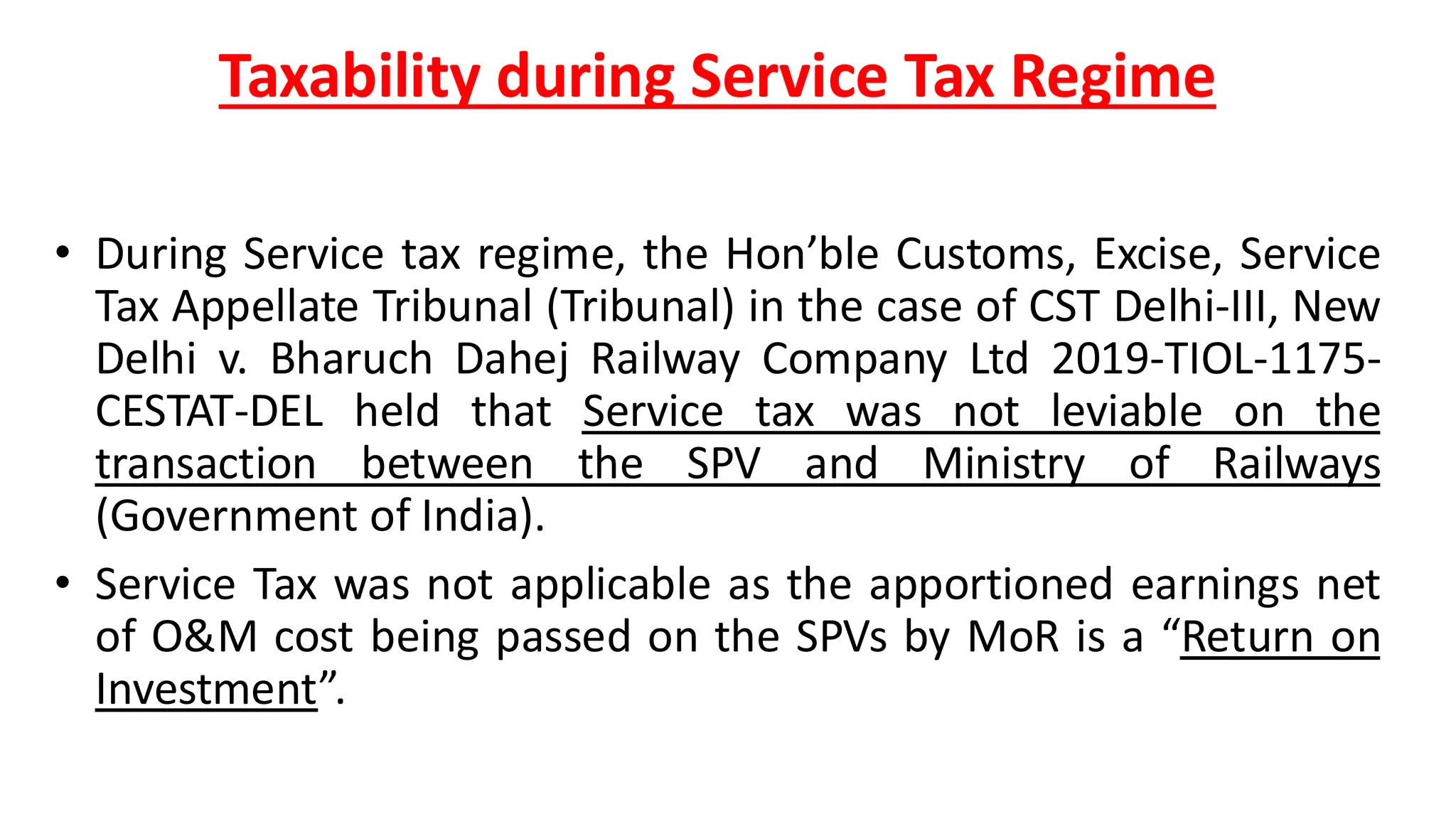

6.

Taxability during ServiceTax Regime

• During Service tax regime, the Hon’ble Customs, Excise, Service

Tax Appellate Tribunal (Tribunal) in the case of CST Delhi-III, New

Delhi v. Bharuch Dahej Railway Company Ltd 2019-TIOL-1175-

CESTAT-DEL held that Service tax was not leviable on the

transaction between the SPV and Ministry of Railways

(Government of India).

• Service Tax was not applicable as the apportioned earnings net

of O&M cost being passed on the SPVs by MoR is a “Return on

Investment”.

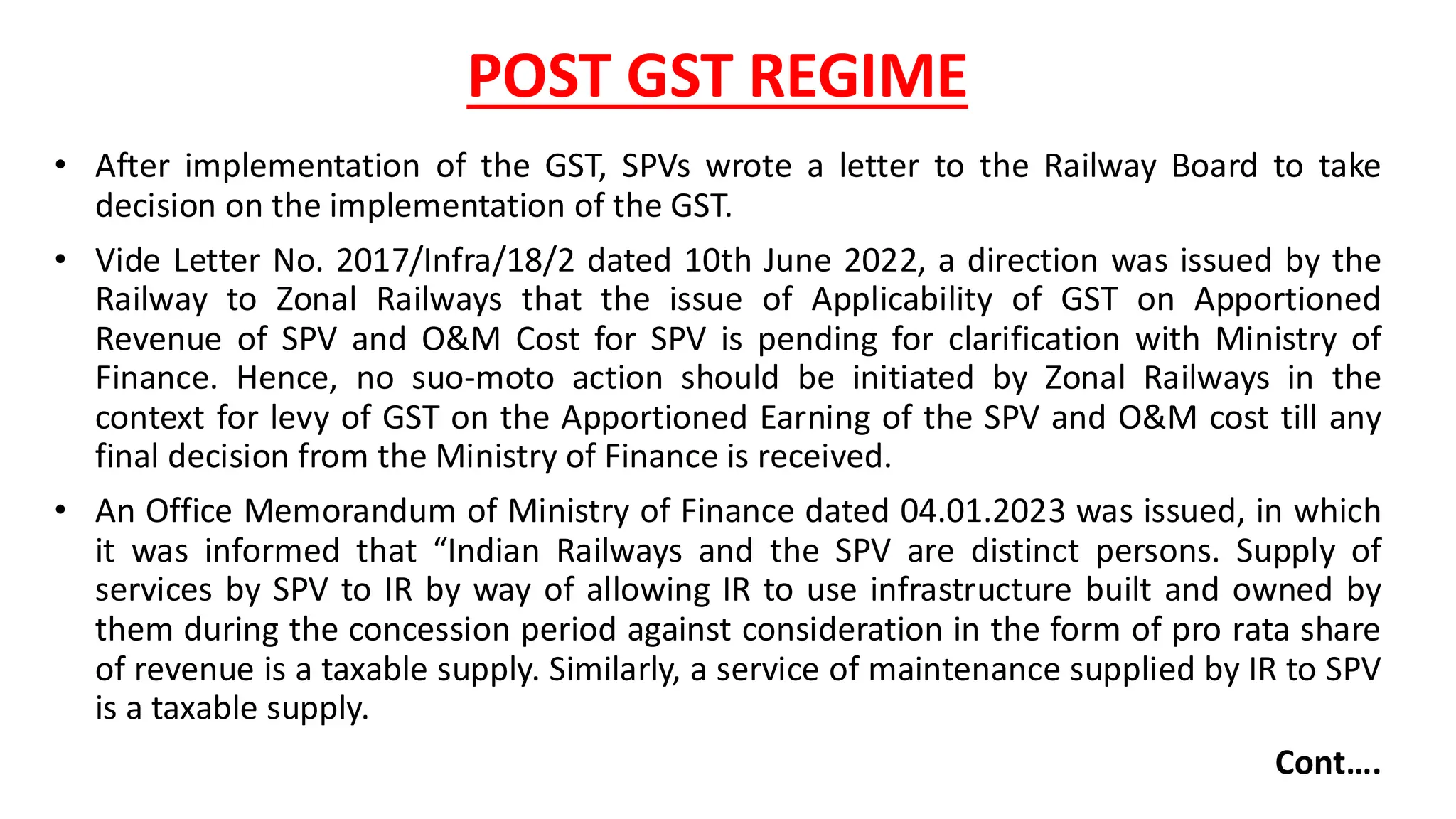

7.

POST GST REGIME

•After implementation of the GST, SPVs wrote a letter to the Railway Board to take

decision on the implementation of the GST.

• Vide Letter No. 2017/Infra/18/2 dated 10th June 2022, a direction was issued by the

Railway to Zonal Railways that the issue of Applicability of GST on Apportioned

Revenue of SPV and O&M Cost for SPV is pending for clarification with Ministry of

Finance. Hence, no suo-moto action should be initiated by Zonal Railways in the

context for levy of GST on the Apportioned Earning of the SPV and O&M cost till any

final decision from the Ministry of Finance is received.

• An Office Memorandum of Ministry of Finance dated 04.01.2023 was issued, in which

it was informed that “Indian Railways and the SPV are distinct persons. Supply of

services by SPV to IR by way of allowing IR to use infrastructure built and owned by

them during the concession period against consideration in the form of pro rata share

of revenue is a taxable supply. Similarly, a service of maintenance supplied by IR to SPV

is a taxable supply.

Cont….

8.

in cont….

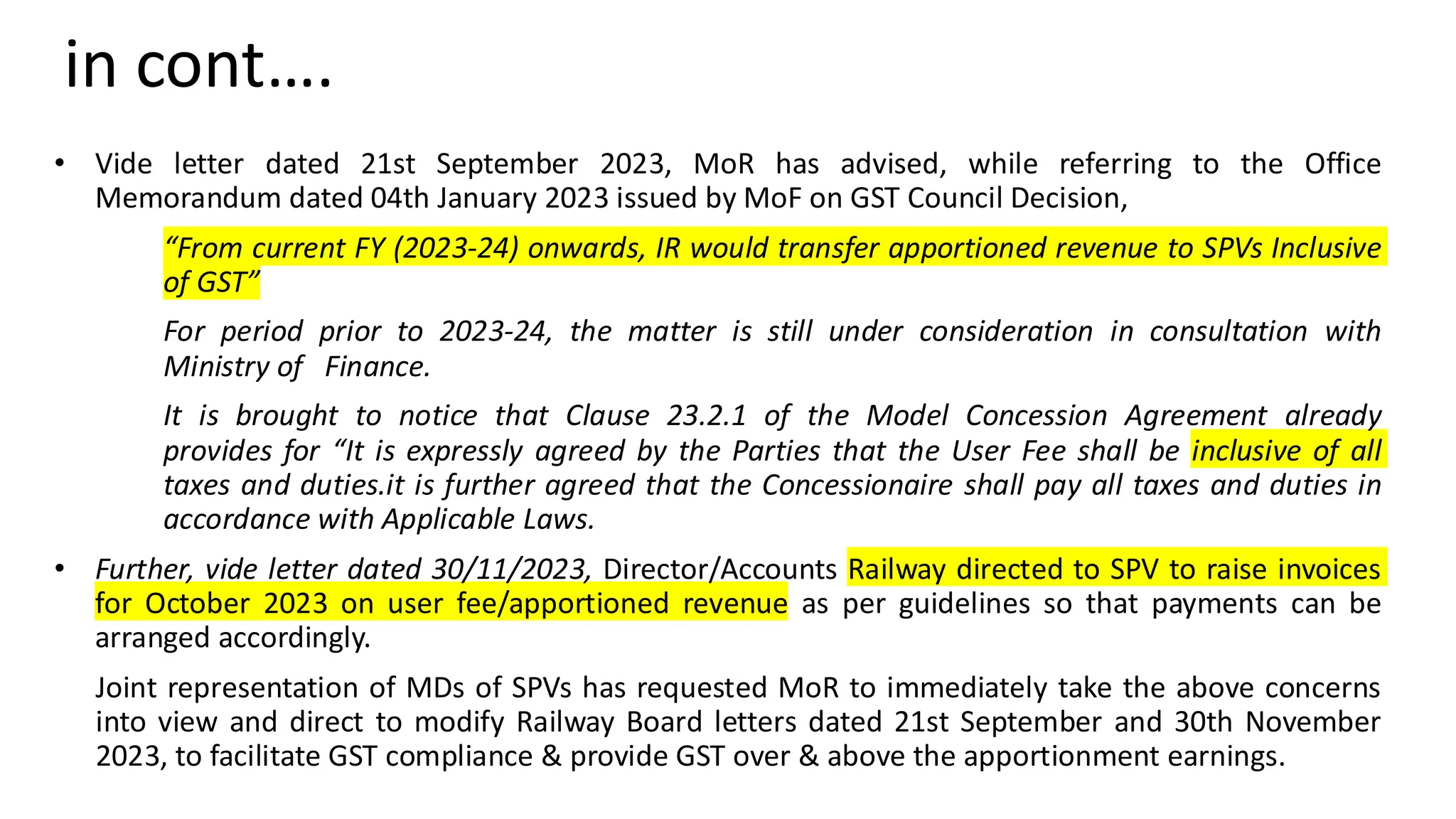

• Videletter dated 21st September 2023, MoR has advised, while referring to the Office

Memorandum dated 04th January 2023 issued by MoF on GST Council Decision,

“From current FY (2023-24) onwards, IR would transfer apportioned revenue to SPVs Inclusive

of GST”

For period prior to 2023-24, the matter is still under consideration in consultation with

Ministry of Finance.

It is brought to notice that Clause 23.2.1 of the Model Concession Agreement already

provides for “It is expressly agreed by the Parties that the User Fee shall be inclusive of all

taxes and duties.it is further agreed that the Concessionaire shall pay all taxes and duties in

accordance with Applicable Laws.

• Further, vide letter dated 30/11/2023, Director/Accounts Railway directed to SPV to raise invoices

for October 2023 on user fee/apportioned revenue as per guidelines so that payments can be

arranged accordingly.

Joint representation of MDs of SPVs has requested MoR to immediately take the above concerns

into view and direct to modify Railway Board letters dated 21st September and 30th November

2023, to facilitate GST compliance & provide GST over & above the apportionment earnings.

11.

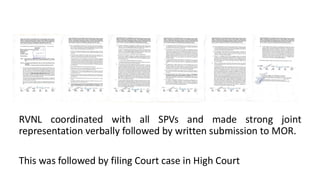

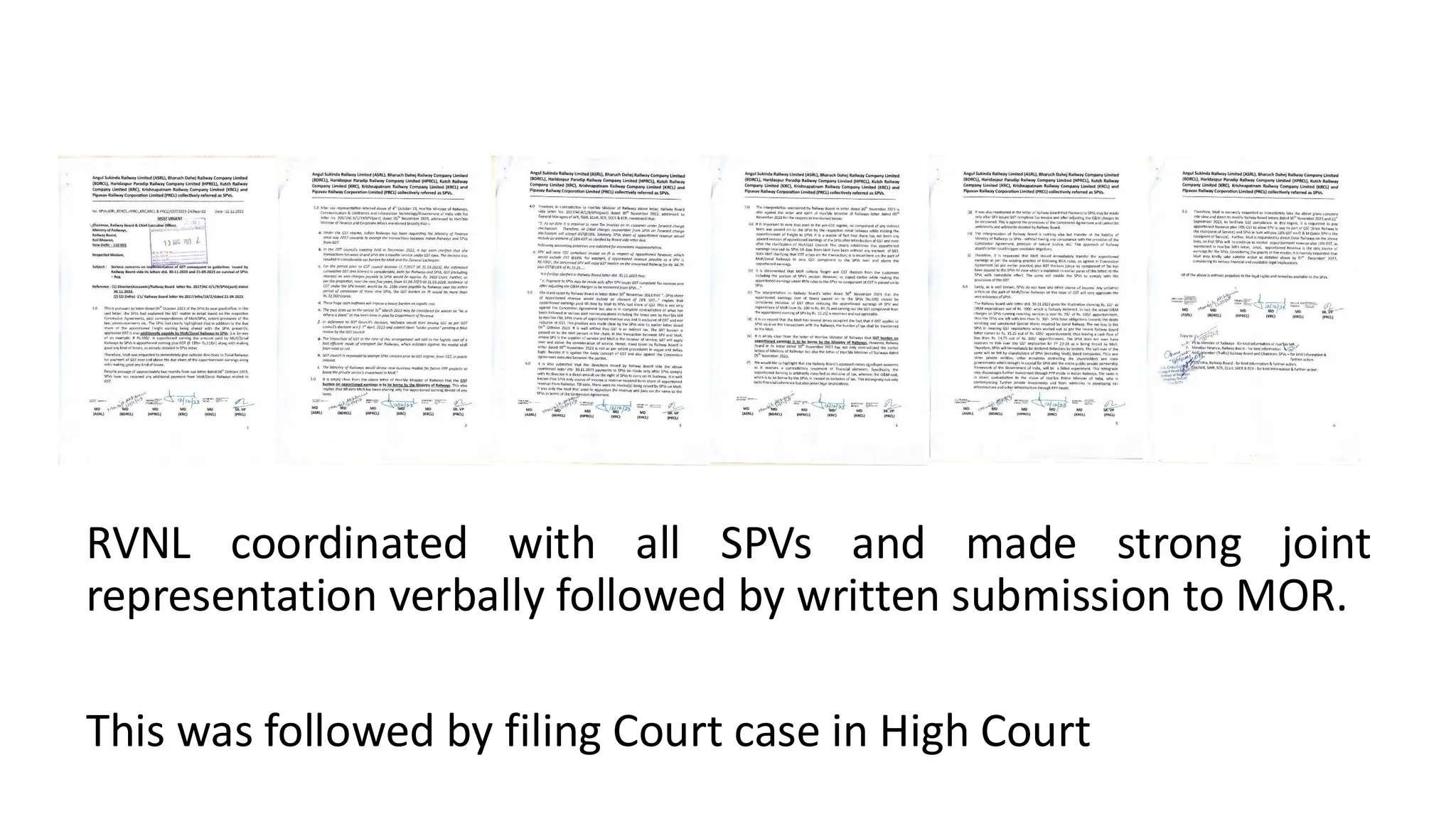

RVNL coordinated withall SPVs and made strong joint

representation verbally followed by written submission to MOR.

This was followed by filing Court case in High Court

12.

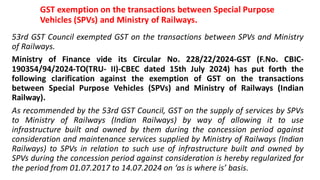

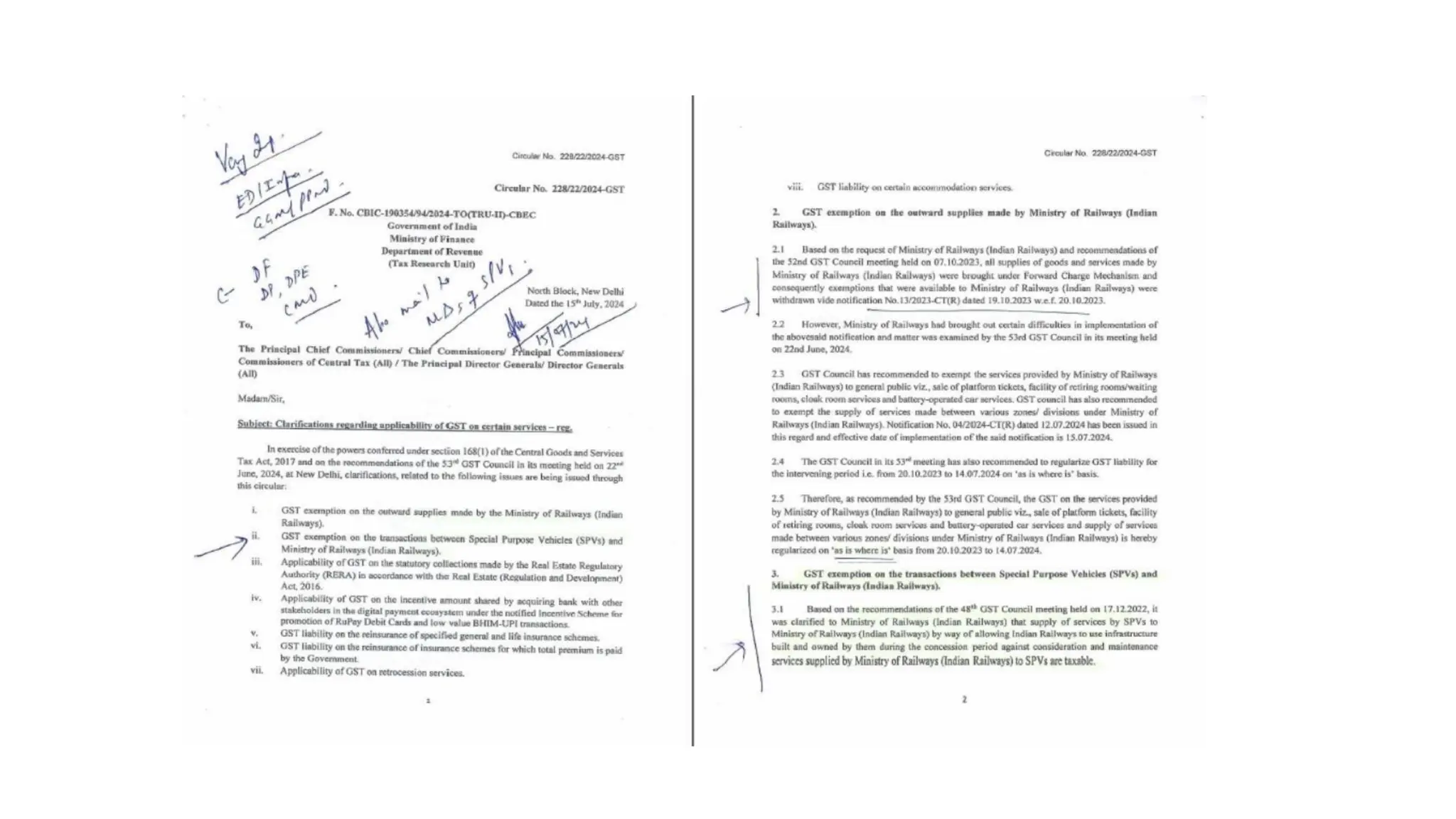

GST exemption onthe transactions between Special Purpose

Vehicles (SPVs) and Ministry of Railways.

53rd GST Council exempted GST on the transactions between SPVs and Ministry

of Railways.

Ministry of Finance vide its Circular No. 228/22/2024-GST (F.No. CBIC-

190354/94/2024-TO(TRU- II)-CBEC dated 15th July 2024) has put forth the

following clarification against the exemption of GST on the transactions

between Special Purpose Vehicles (SPVs) and Ministry of Railways (Indian

Railway).

As recommended by the 53rd GST Council, GST on the supply of services by SPVs

to Ministry of Railways (Indian Railways) by way of allowing it to use

infrastructure built and owned by them during the concession period against

consideration and maintenance services supplied by Ministry of Railways (Indian

Railways) to SPVs in relation to such use of infrastructure built and owned by

SPVs during the concession period against consideration is hereby regularized for

the period from 01.07.2017 to 14.07.2024 on ‘as is where is’ basis.

13.

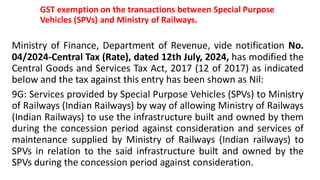

GST exemption onthe transactions between Special Purpose

Vehicles (SPVs) and Ministry of Railways.

Ministry of Finance, Department of Revenue, vide notification No.

04/2024-Central Tax (Rate), dated 12th July, 2024, has modified the

Central Goods and Services Tax Act, 2017 (12 of 2017) as indicated

below and the tax against this entry has been shown as Nil:

9G: Services provided by Special Purpose Vehicles (SPVs) to Ministry

of Railways (Indian Railways) by way of allowing Ministry of Railways

(Indian Railways) to use the infrastructure built and owned by them

during the concession period against consideration and services of

maintenance supplied by Ministry of Railways (Indian railways) to

SPVs in relation to the said infrastructure built and owned by the

SPVs during the concession period against consideration.