LEARNING

OBJECTIVES

Identify the broadobjectives of transaction cycles.

Recognize the types of transactions processed by each of

the three transaction cycles.

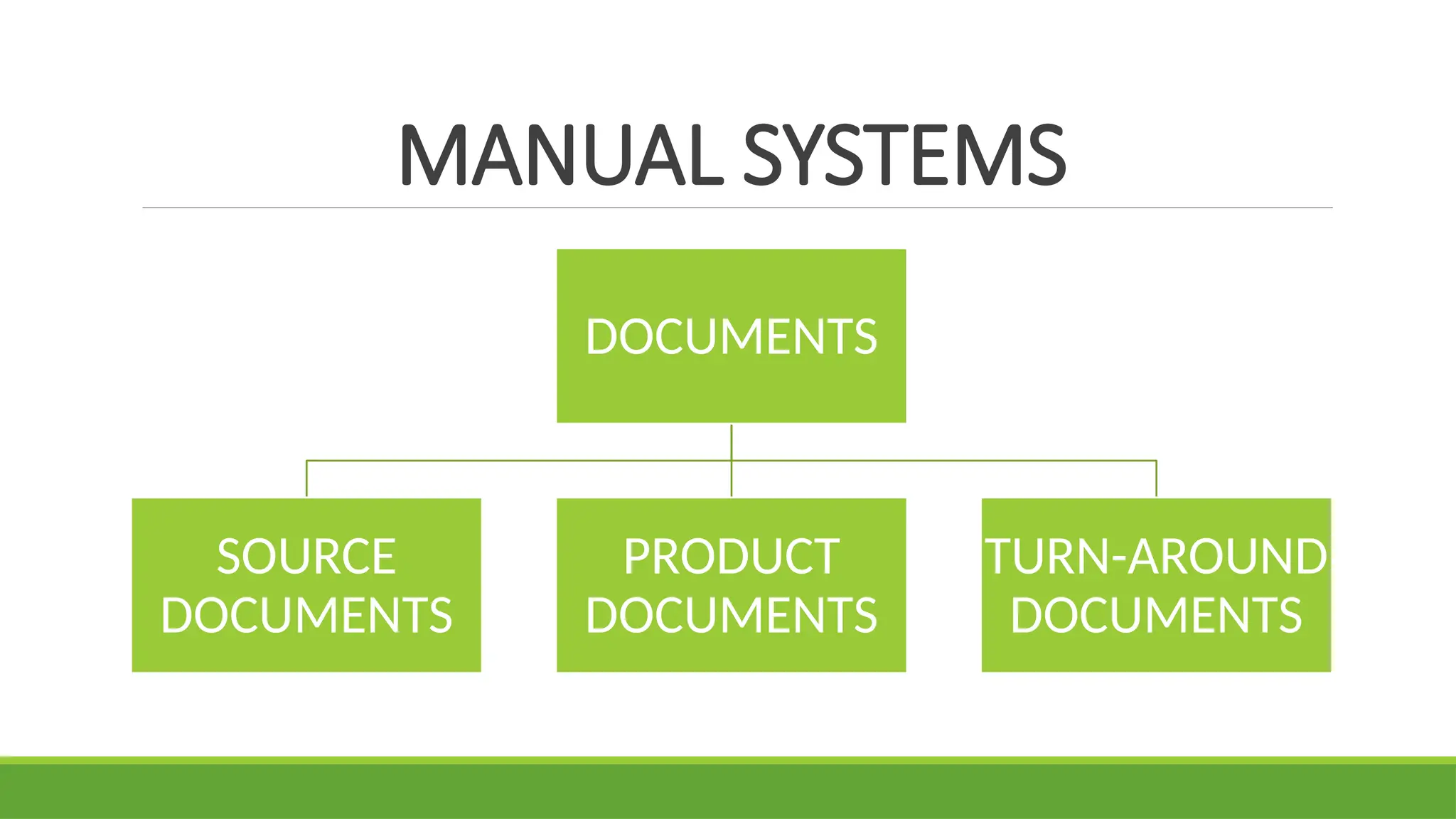

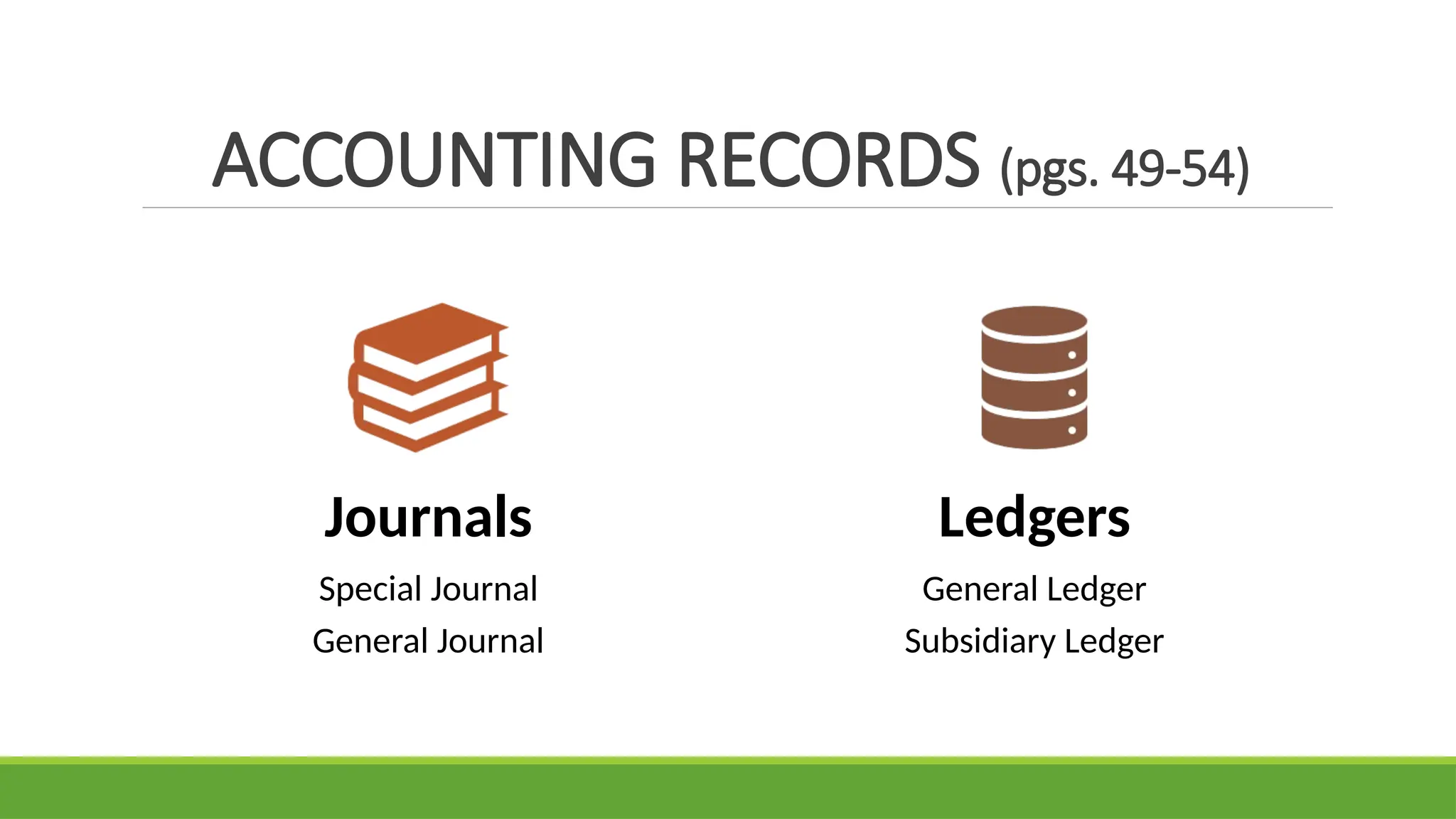

Identify the basic accounting records used in TPS.

Distinguish the relationship between the traditional

accounting records and their magnetic equivalents.

Enumerate the documentation techniques.

Distinguish the differences between batch and real-time

processing and the impact of these technologies on

transaction processing.

Enumerate data coding schemes used in AIS.

GOAL OF TRANSACTIONPROCESSING SYSTEM (TPS)

process financial transactions.

What does financial transactions mean? (previous lecture)

Financial transactions are common business events that occur

regularly.

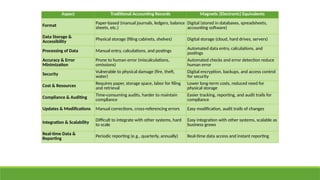

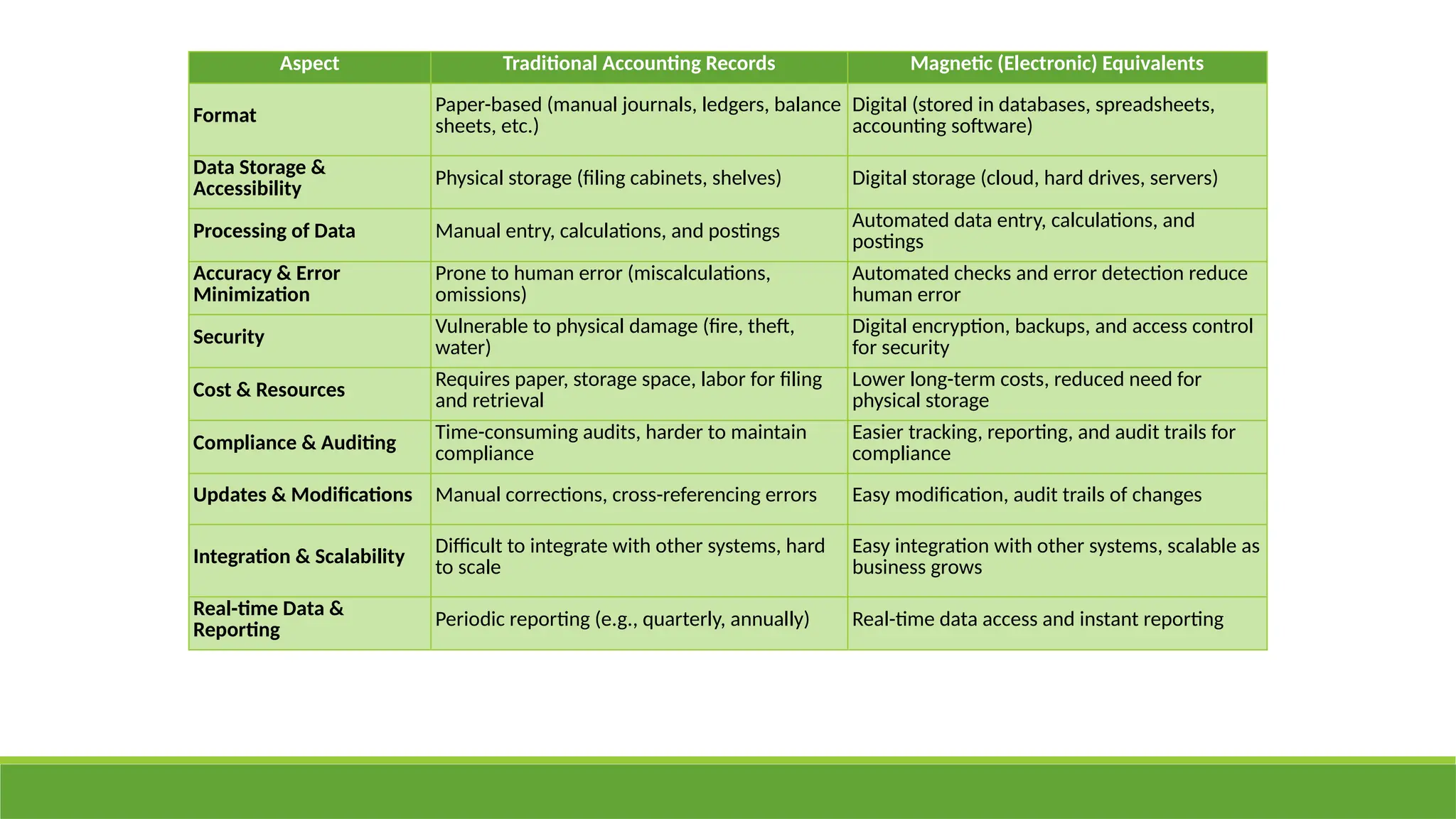

Aspect Traditional AccountingRecords Magnetic (Electronic) Equivalents

Format

Paper-based (manual journals, ledgers, balance

sheets, etc.)

Digital (stored in databases, spreadsheets,

accounting software)

Data Storage &

Accessibility

Physical storage (filing cabinets, shelves) Digital storage (cloud, hard drives, servers)

Processing of Data Manual entry, calculations, and postings Automated data entry, calculations, and

postings

Accuracy & Error

Minimization

Prone to human error (miscalculations,

omissions)

Automated checks and error detection reduce

human error

Security

Vulnerable to physical damage (fire, theft,

water)

Digital encryption, backups, and access control

for security

Cost & Resources

Requires paper, storage space, labor for filing

and retrieval

Lower long-term costs, reduced need for

physical storage

Compliance & Auditing

Time-consuming audits, harder to maintain

compliance

Easier tracking, reporting, and audit trails for

compliance

Updates & Modifications Manual corrections, cross-referencing errors Easy modification, audit trails of changes

Integration & Scalability Difficult to integrate with other systems, hard

to scale

Easy integration with other systems, scalable as

business grows

Real-time Data &

Reporting

Periodic reporting (e.g., quarterly, annually) Real-time data access and instant reporting

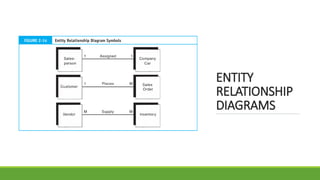

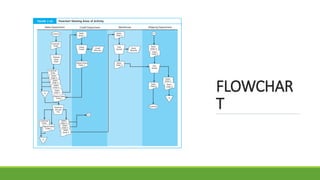

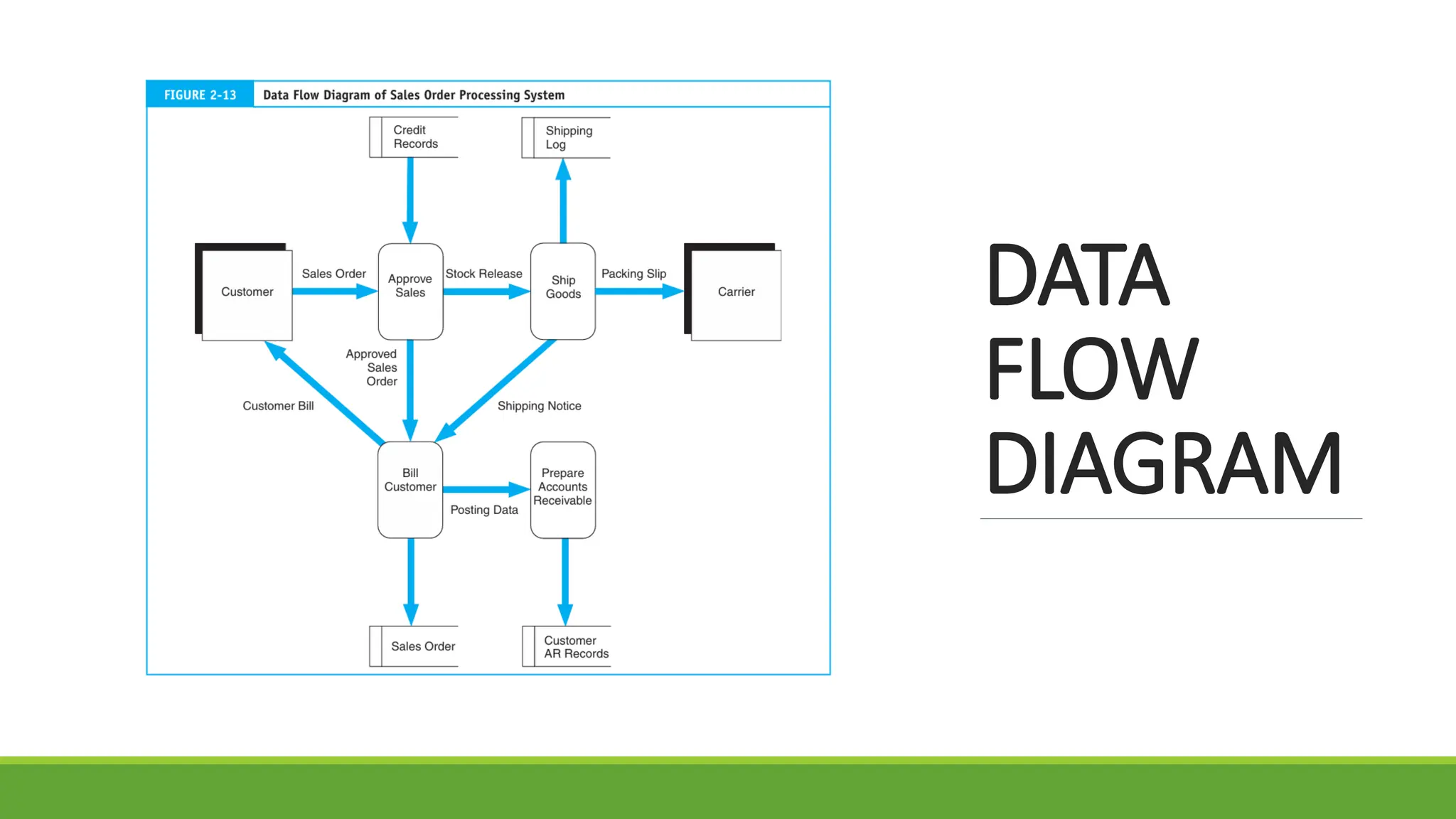

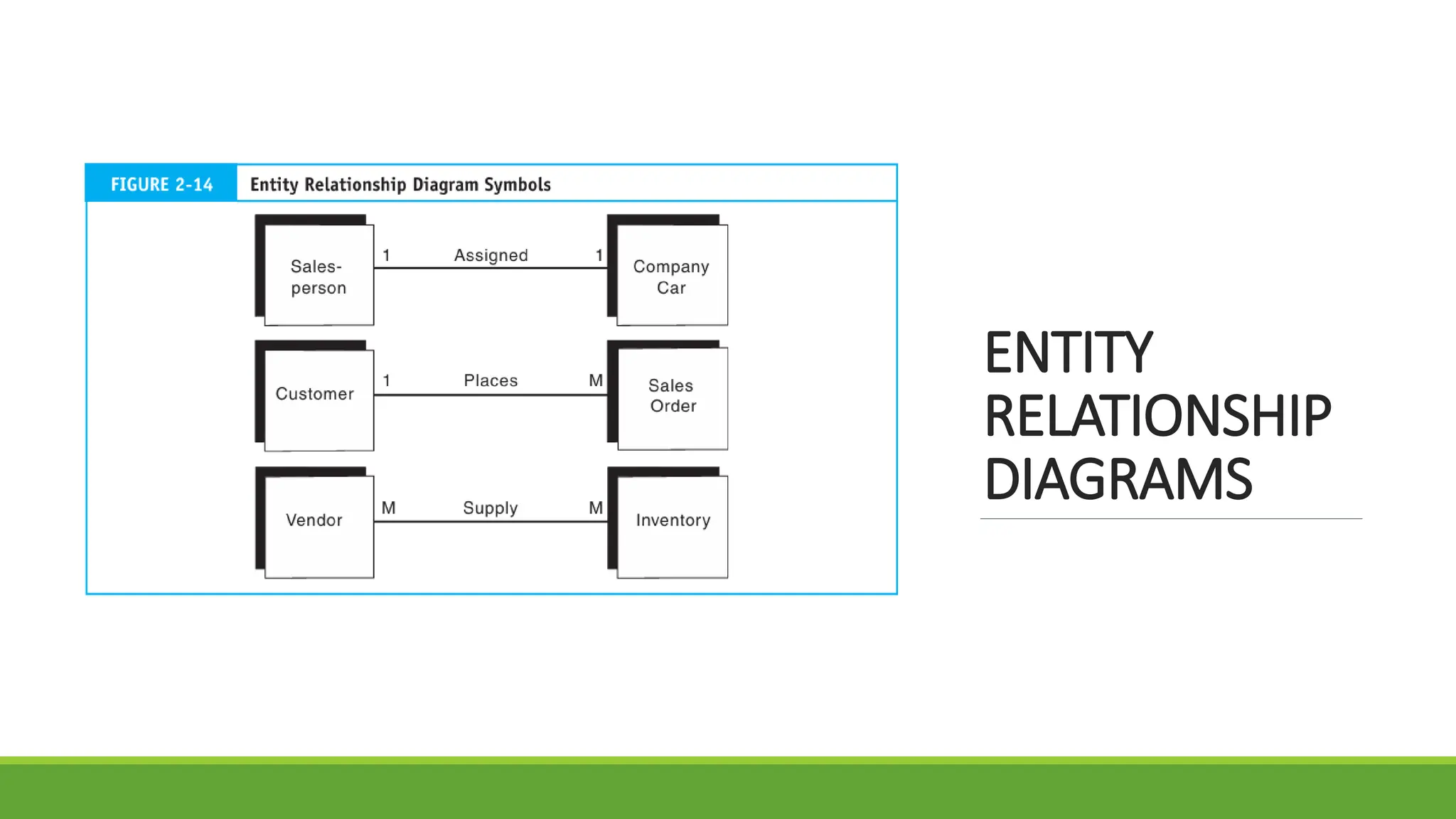

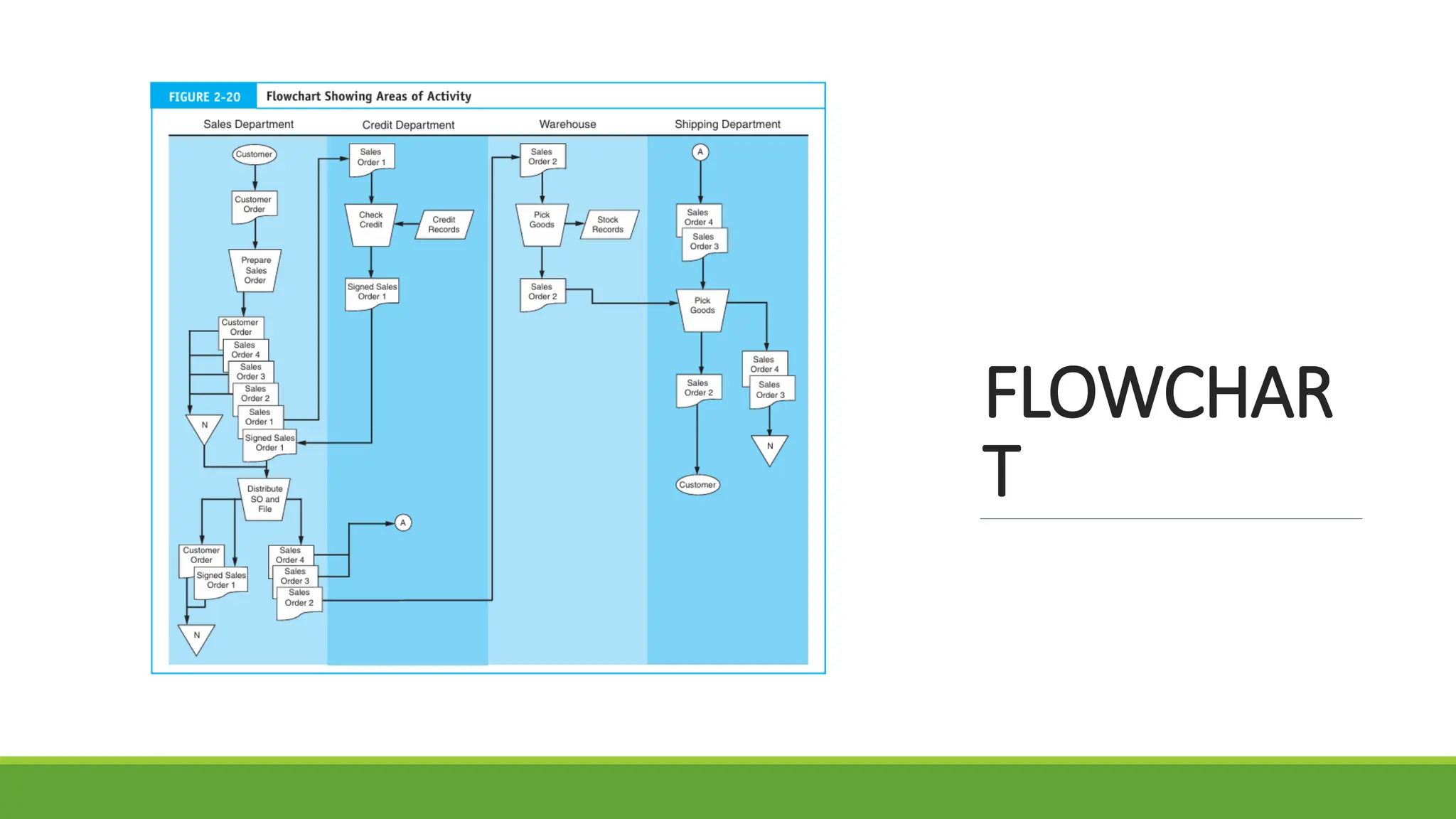

DOCUMENTATION

TECHNIQUES

The old sayingthat a picture is worth a thousand words is

extremely applicable when it comes to documenting systems.

A written description of a system can be wordy and difficult

to follow. Experience has shown that a visual image can

convey vital system information more effectively and

efficiently than words. As both systems designers and

auditors, accountants use system documentation routinely.

The ability to document systems in graphic form is thus an

important skill for accountants to master.

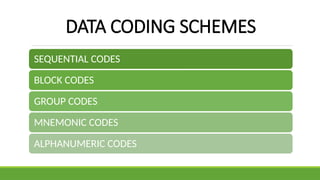

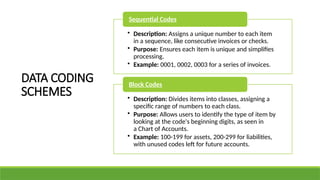

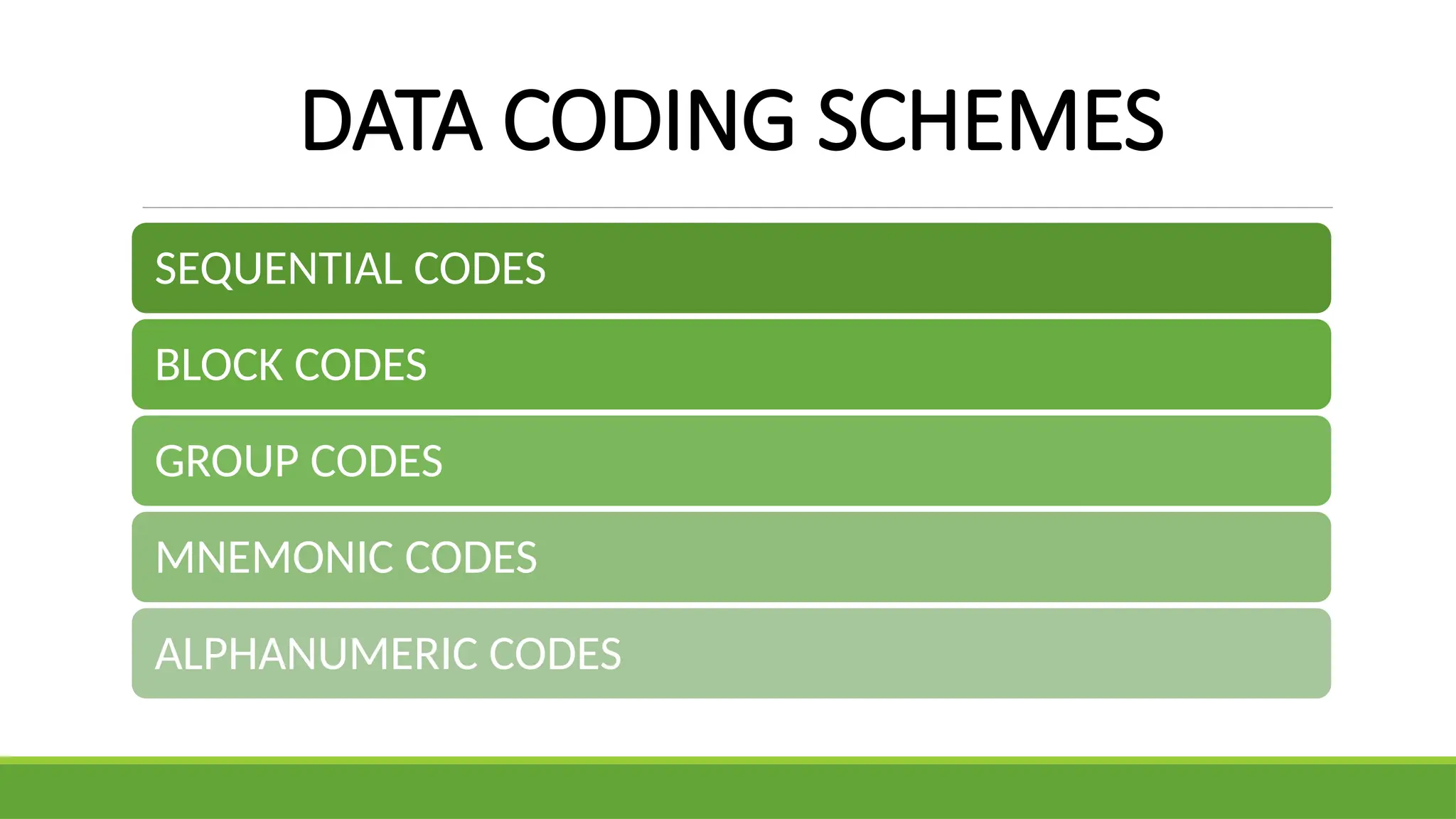

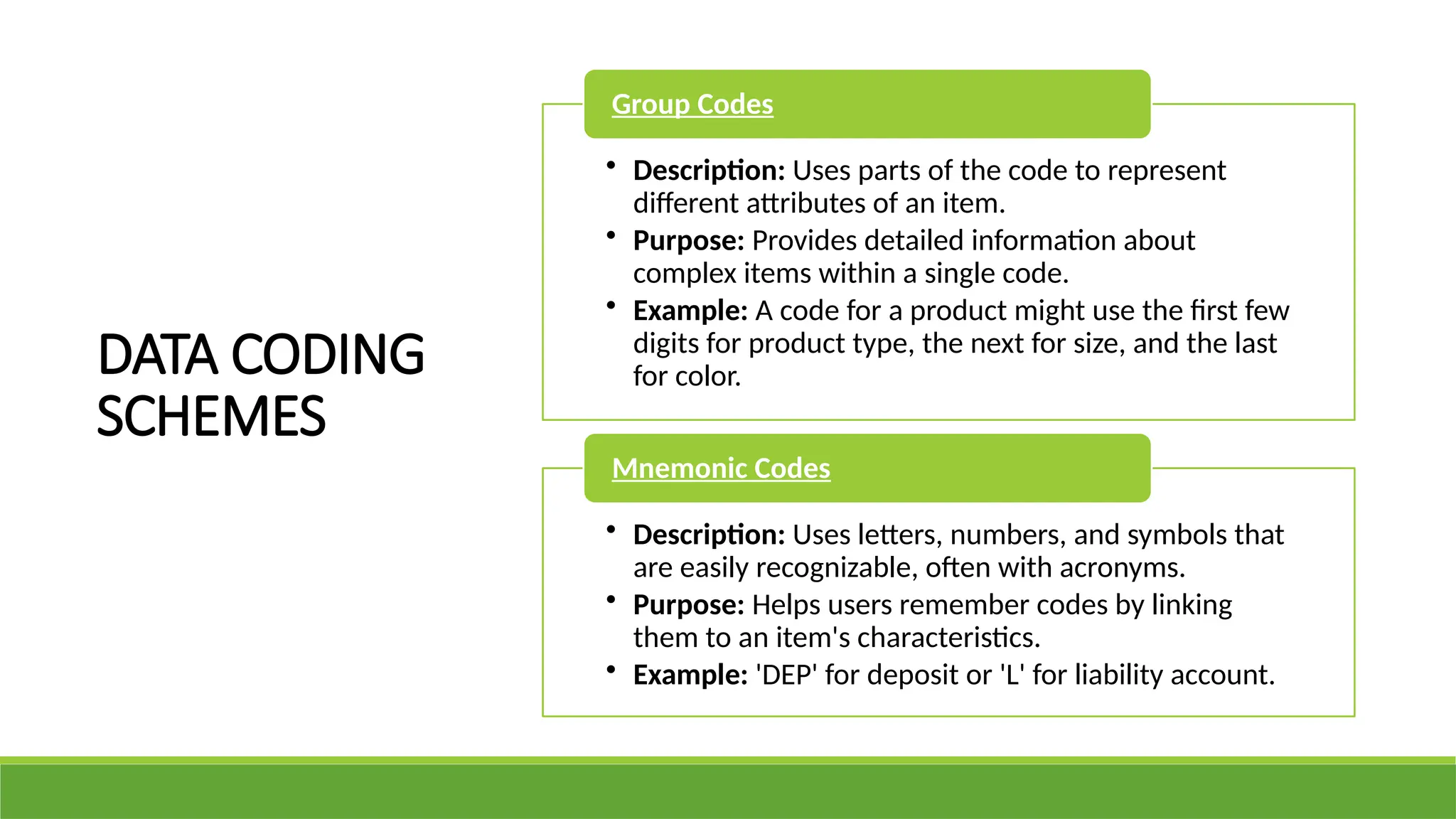

DATA CODING

SCHEMES

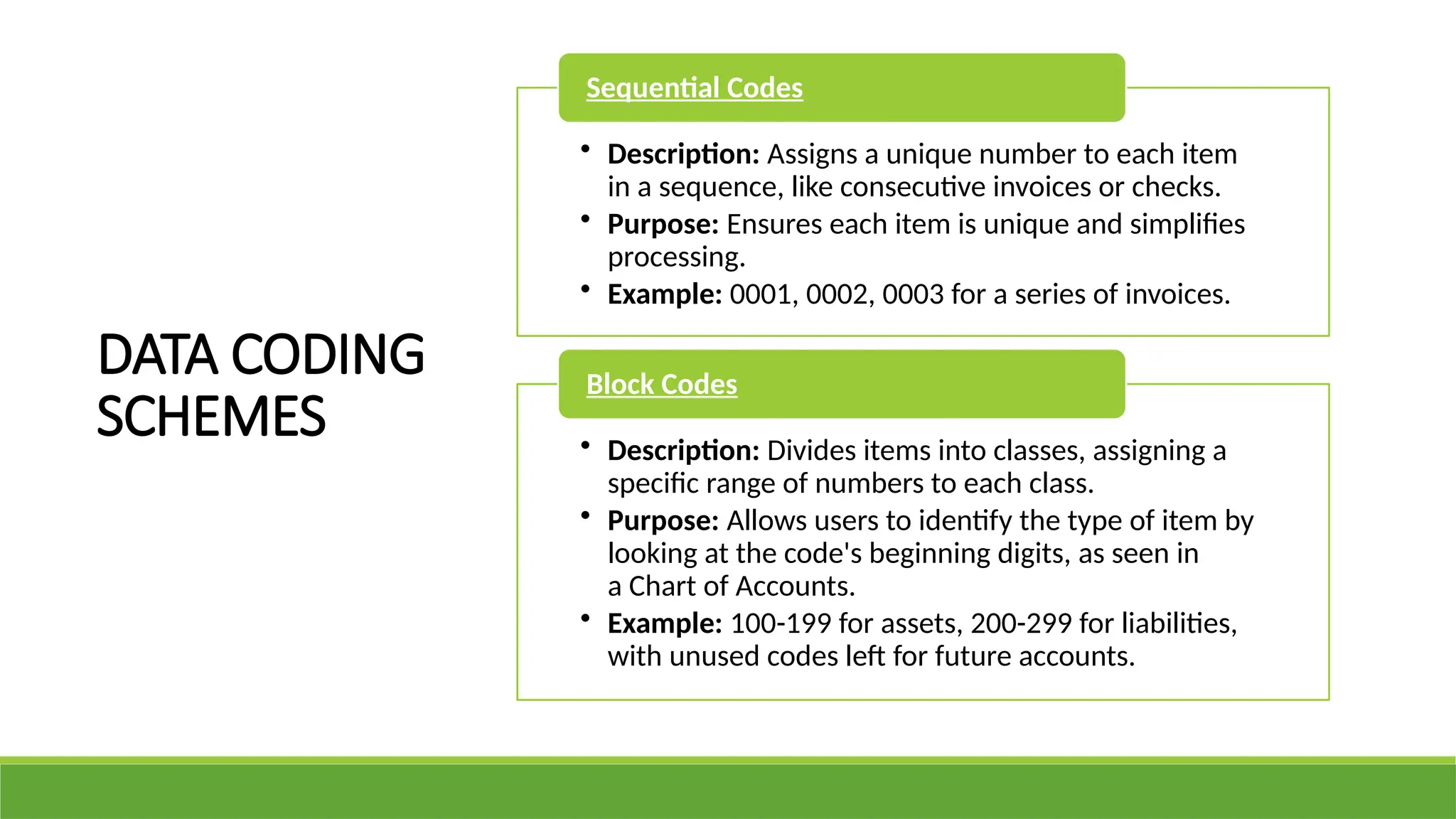

• Description:Assigns a unique number to each item

in a sequence, like consecutive invoices or checks.

• Purpose: Ensures each item is unique and simplifies

processing.

• Example: 0001, 0002, 0003 for a series of invoices.

Sequential Codes

• Description: Divides items into classes, assigning a

specific range of numbers to each class.

• Purpose: Allows users to identify the type of item by

looking at the code's beginning digits, as seen in

a Chart of Accounts.

• Example: 100-199 for assets, 200-299 for liabilities,

with unused codes left for future accounts.

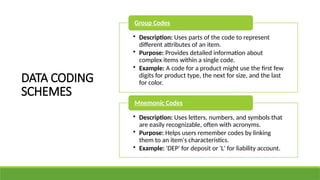

Block Codes

28.

• Description: Usesparts of the code to represent

different attributes of an item.

• Purpose: Provides detailed information about

complex items within a single code.

• Example: A code for a product might use the first few

digits for product type, the next for size, and the last

for color.

Group Codes

• Description: Uses letters, numbers, and symbols that

are easily recognizable, often with acronyms.

• Purpose: Helps users remember codes by linking

them to an item's characteristics.

• Example: 'DEP' for deposit or 'L' for liability account.

Mnemonic Codes

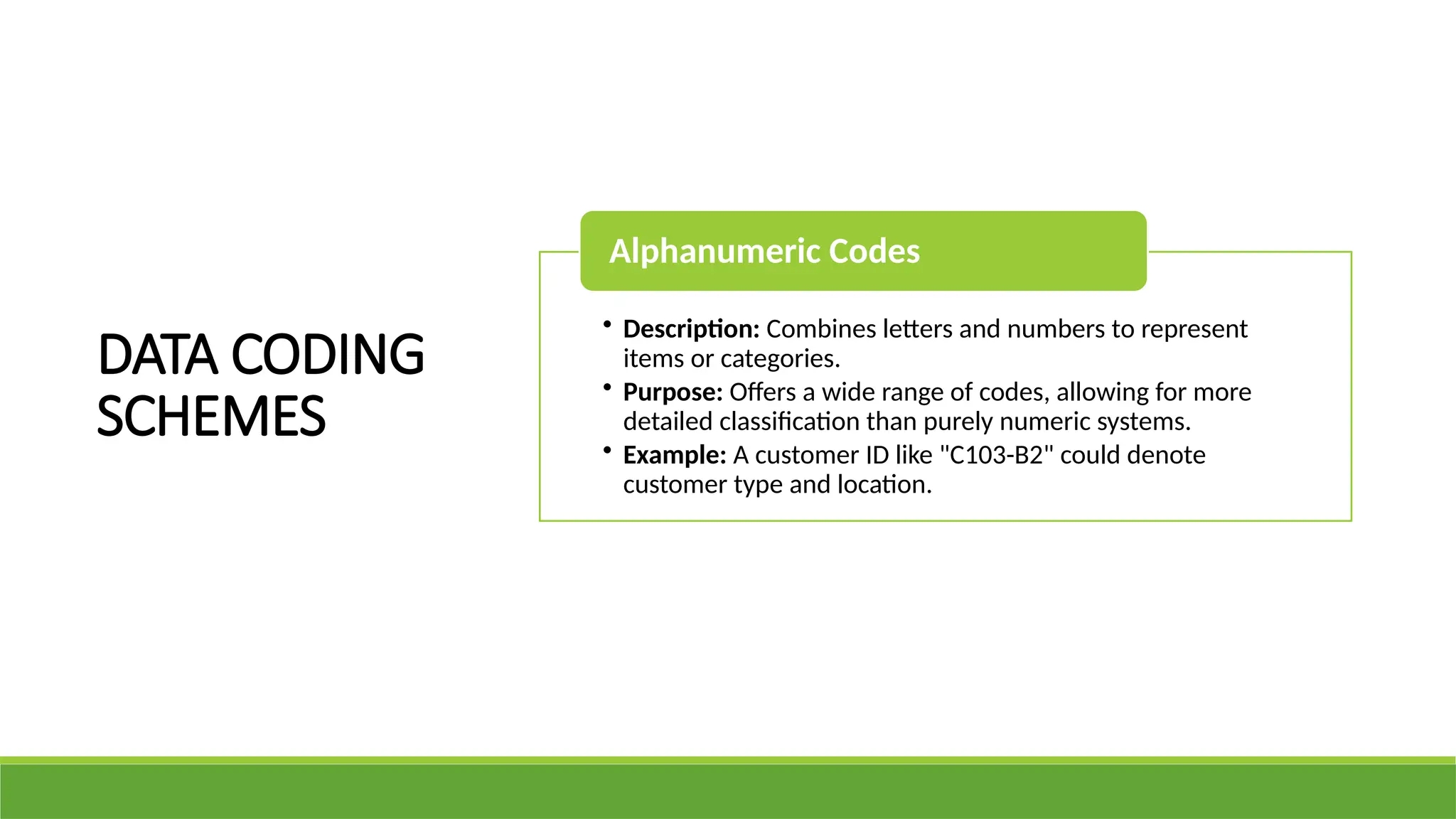

DATA CODING

SCHEMES

29.

DATA CODING

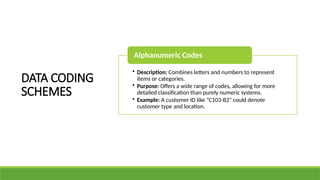

SCHEMES

• Description:Combines letters and numbers to represent

items or categories.

• Purpose: Offers a wide range of codes, allowing for more

detailed classification than purely numeric systems.

• Example: A customer ID like "C103-B2" could denote

customer type and location.

Alphanumeric Codes

DATA CODING

SCHEMES

30.

LEARNING

OBJECTIVES

Identify the broadobjectives of transaction cycles.

Recognize the types of transactions processed by each of

the three transaction cycles.

Identify the basic accounting records used in TPS.

Distinguish the relationship between the traditional

accounting records and their magnetic equivalents.

Enumerate the documentation techniques.

Distinguish the differences between batch and real-time

processing and the impact of these technologies on

transaction processing.

Enumerate data coding schemes used in AIS.

![accounting_information_system[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/accountinginformationsystem1-231215144622-b88f4649-thumbnail.jpg?width=600ounds&width=560&fit=bounds)