The document explains the differences between single-entry and double-entry bookkeeping systems. Single-entry bookkeeping is a simple method tracking cash transactions with a cash book, suitable for small enterprises, while double-entry bookkeeping records transactions in at least two accounts, emphasizing a more comprehensive financial overview. The double-entry system is preferred for larger businesses due to its error detection, balanced approach, and the ability to prepare detailed financial statements.

Single entry andDouble entry System

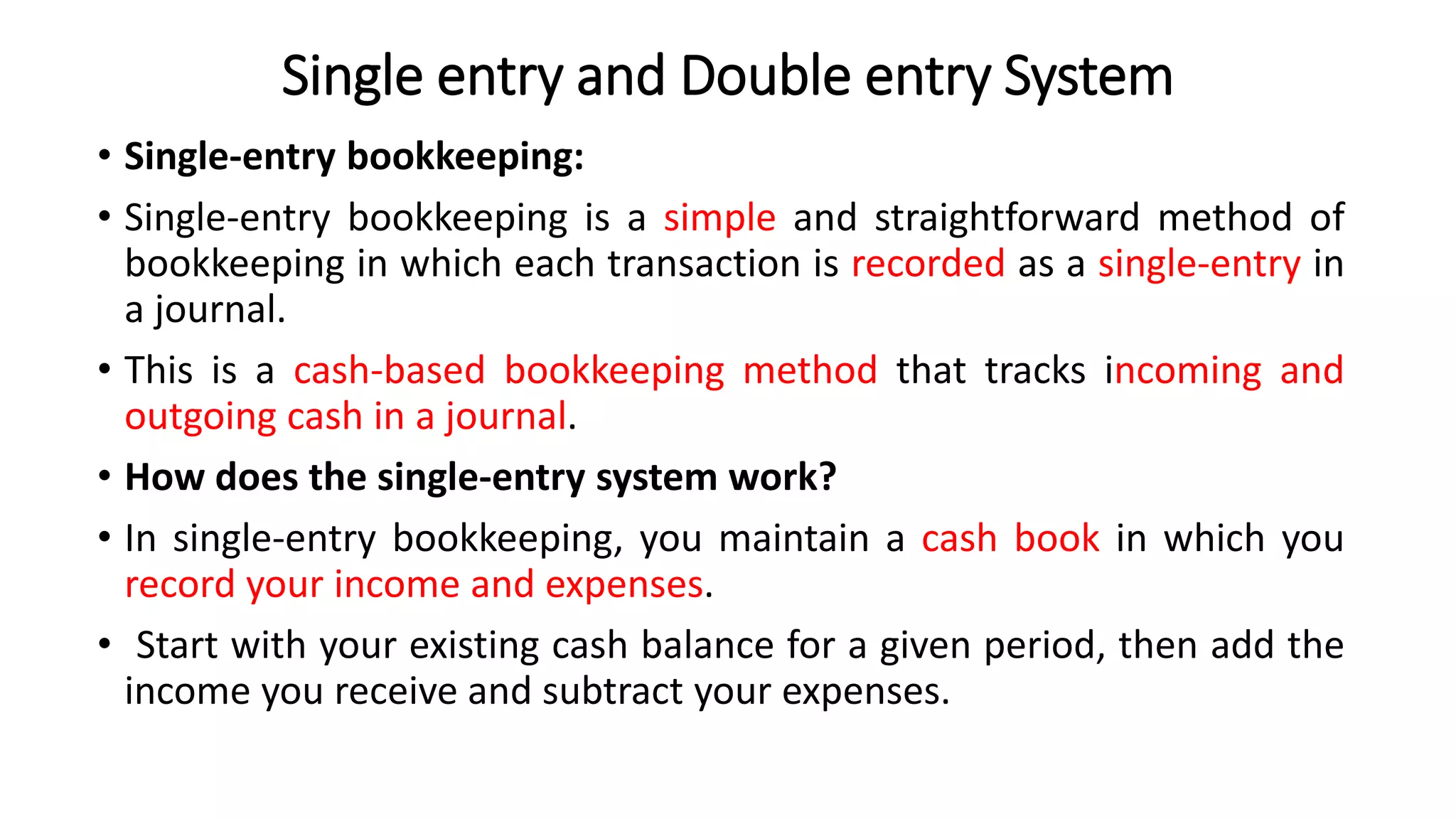

• Single-entry bookkeeping:

• Single-entry bookkeeping is a simple and straightforward method of

bookkeeping in which each transaction is recorded as a single-entry in

a journal.

• This is a cash-based bookkeeping method that tracks incoming and

outgoing cash in a journal.

• How does the single-entry system work?

• In single-entry bookkeeping, you maintain a cash book in which you

record your income and expenses.

• Start with your existing cash balance for a given period, then add the

income you receive and subtract your expenses.

2.

Single entry andDouble entry System

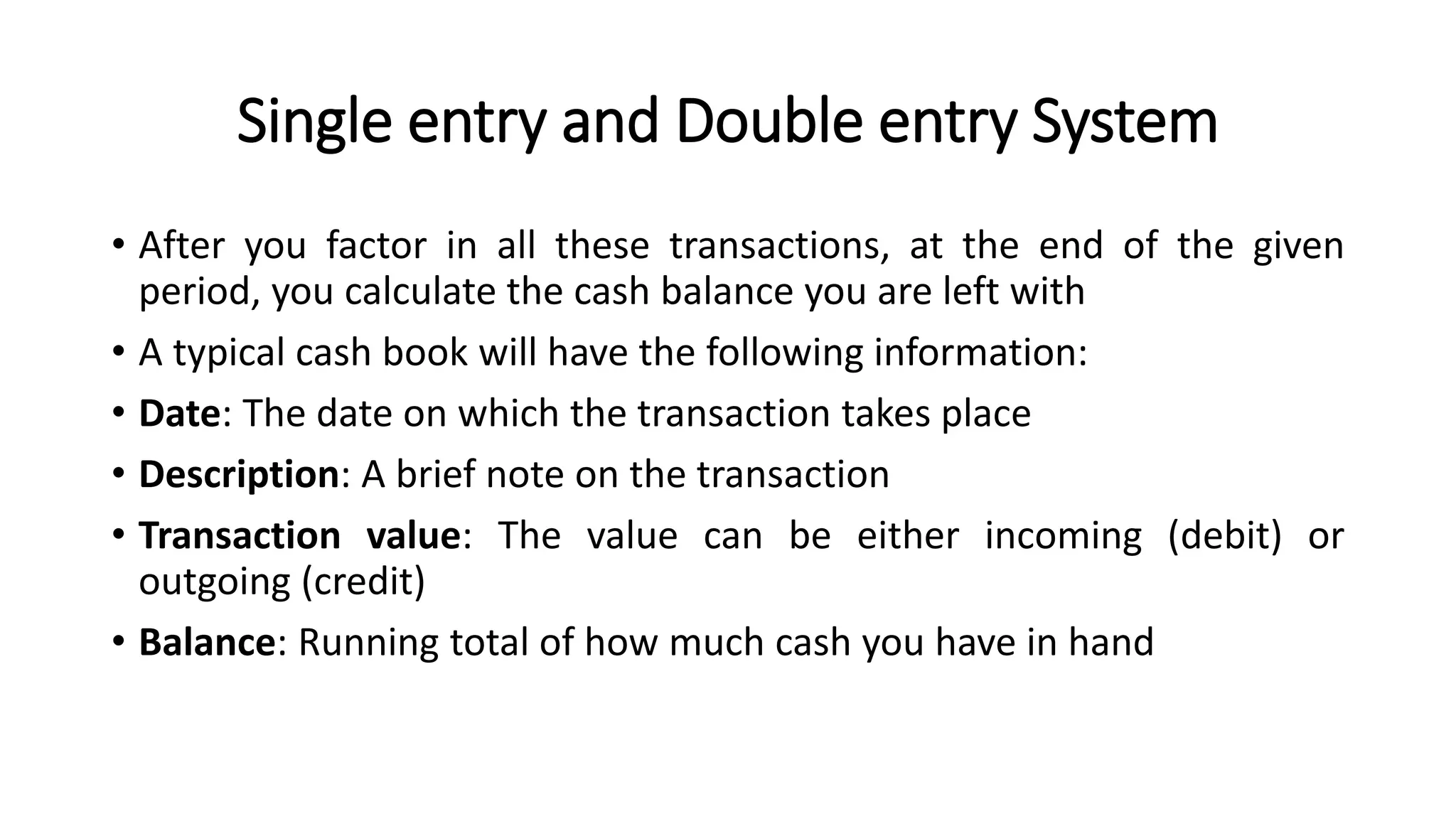

• After you factor in all these transactions, at the end of the given

period, you calculate the cash balance you are left with

• A typical cash book will have the following information:

• Date: The date on which the transaction takes place

• Description: A brief note on the transaction

• Transaction value: The value can be either incoming (debit) or

outgoing (credit)

• Balance: Running total of how much cash you have in hand

3.

Single entry andDouble entry System

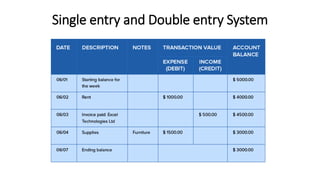

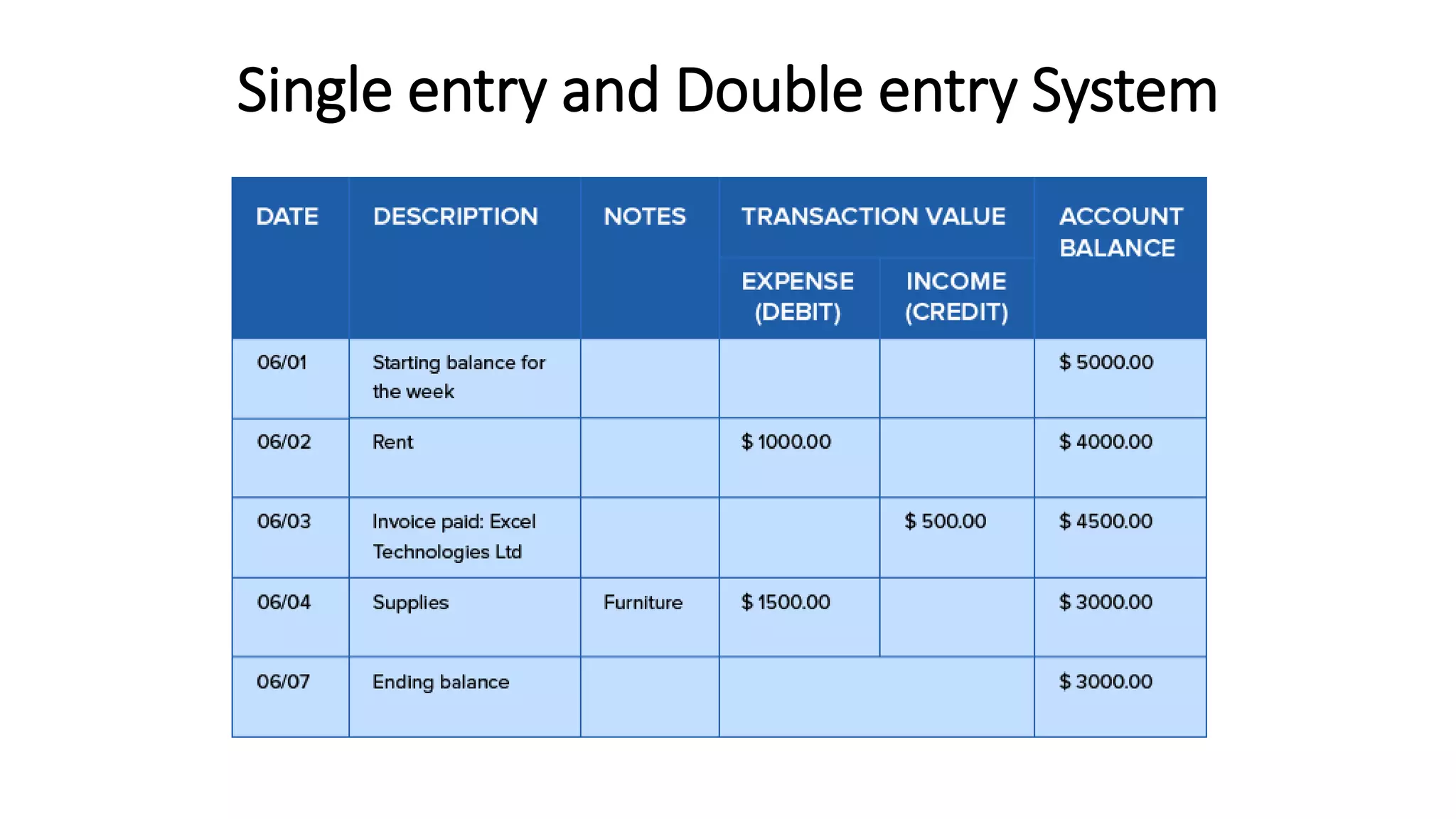

In the following example, suppose you’re a business owner recording the

debit and credit entries for all of the transactions that take place in a week.

1. Let’s assume you have a $5000 cash balance at the beginning of the first

week in June. So this will be your first entry.

2. On the second day of the week you pay your rent, which is $1000. Since

this is an expense, you subtract this amount from your cash balance. This

leaves you with $4000.

3. Your customer pays an invoice for $500, which is income. So this amount is

debited to your account and raises the account balance to $4500.

4. You buy office furniture for $1500. So you subtract this amount from the

existing balance.

5. At the end of the week, you are left with $3000 in cash.

Single entry andDouble entry System

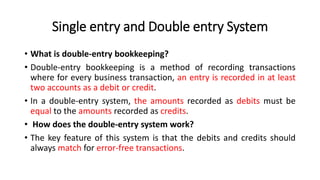

• What is double-entry bookkeeping?

• Double-entry bookkeeping is a method of recording transactions

where for every business transaction, an entry is recorded in at least

two accounts as a debit or credit.

• In a double-entry system, the amounts recorded as debits must be

equal to the amounts recorded as credits.

• How does the double-entry system work?

• The key feature of this system is that the debits and credits should

always match for error-free transactions.

6.

Single entry andDouble entry System

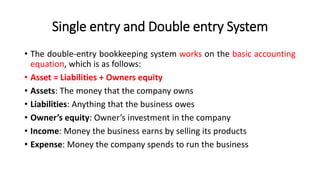

• The double-entry bookkeeping system works on the basic accounting

equation, which is as follows:

• Asset = Liabilities + Owners equity

• Assets: The money that the company owns

• Liabilities: Anything that the business owes

• Owner’s equity: Owner’s investment in the company

• Income: Money the business earns by selling its products

• Expense: Money the company spends to run the business

7.

Single entry andDouble entry System

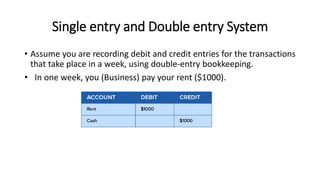

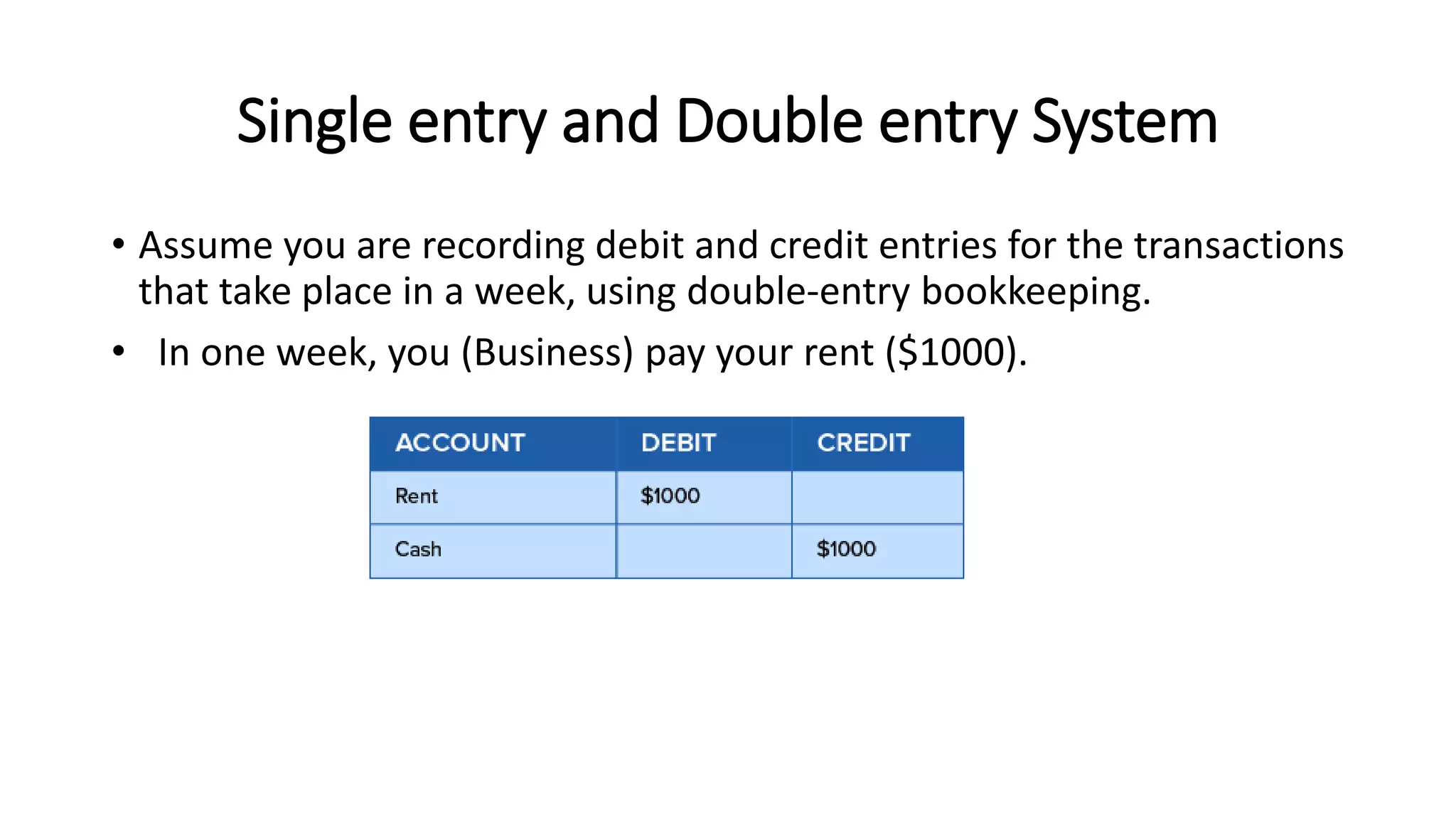

• Assume you are recording debit and credit entries for the transactions

that take place in a week, using double-entry bookkeeping.

• In one week, you (Business) pay your rent ($1000).

8.

Single entry andDouble entry System

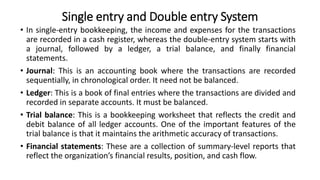

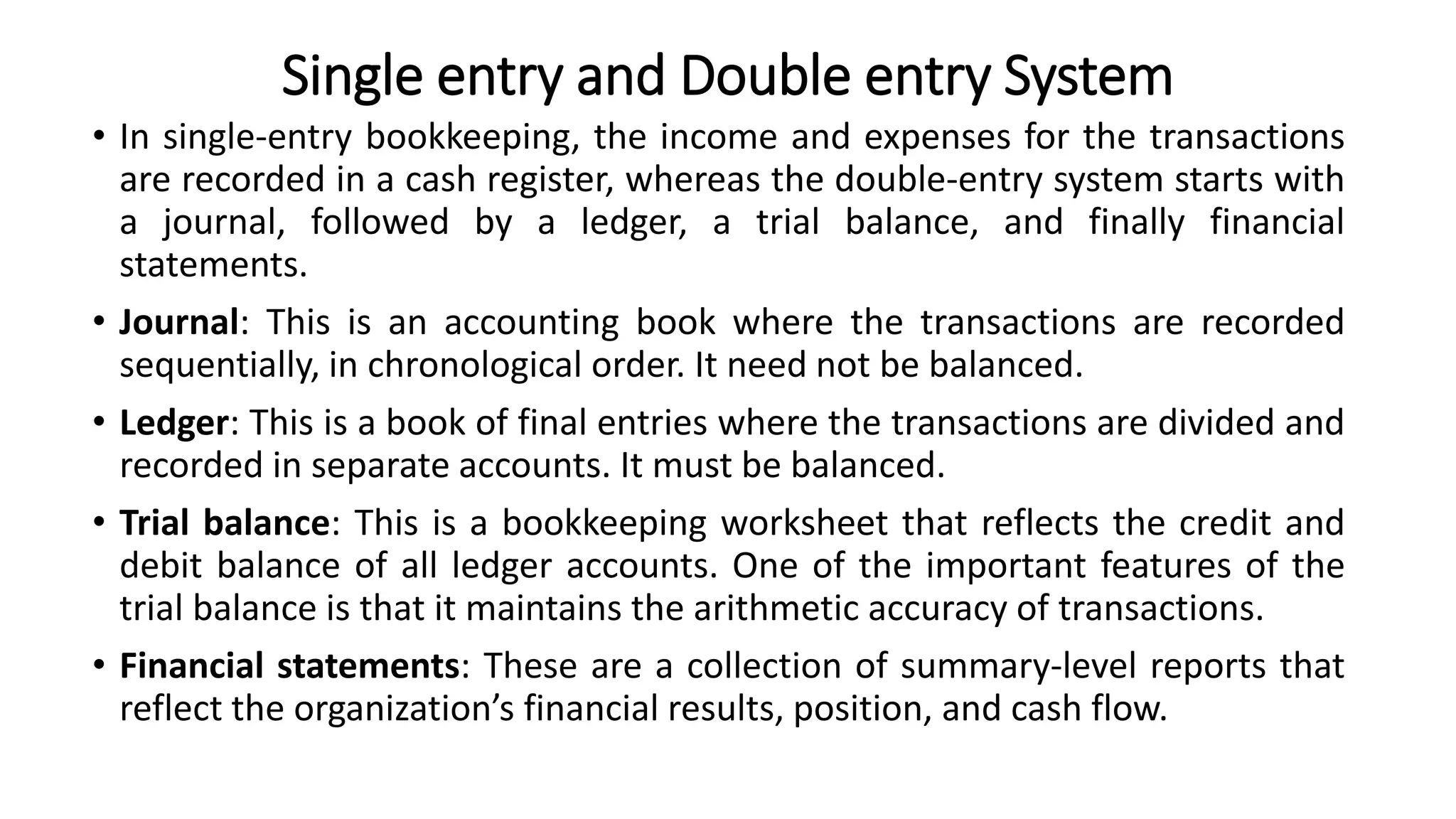

• In single-entry bookkeeping, the income and expenses for the transactions

are recorded in a cash register, whereas the double-entry system starts with

a journal, followed by a ledger, a trial balance, and finally financial

statements.

• Journal: This is an accounting book where the transactions are recorded

sequentially, in chronological order. It need not be balanced.

• Ledger: This is a book of final entries where the transactions are divided and

recorded in separate accounts. It must be balanced.

• Trial balance: This is a bookkeeping worksheet that reflects the credit and

debit balance of all ledger accounts. One of the important features of the

trial balance is that it maintains the arithmetic accuracy of transactions.

• Financial statements: These are a collection of summary-level reports that

reflect the organization’s financial results, position, and cash flow.

9.

Single entry andDouble entry System

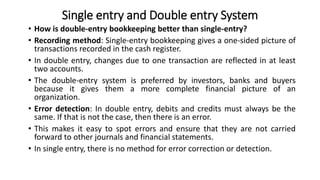

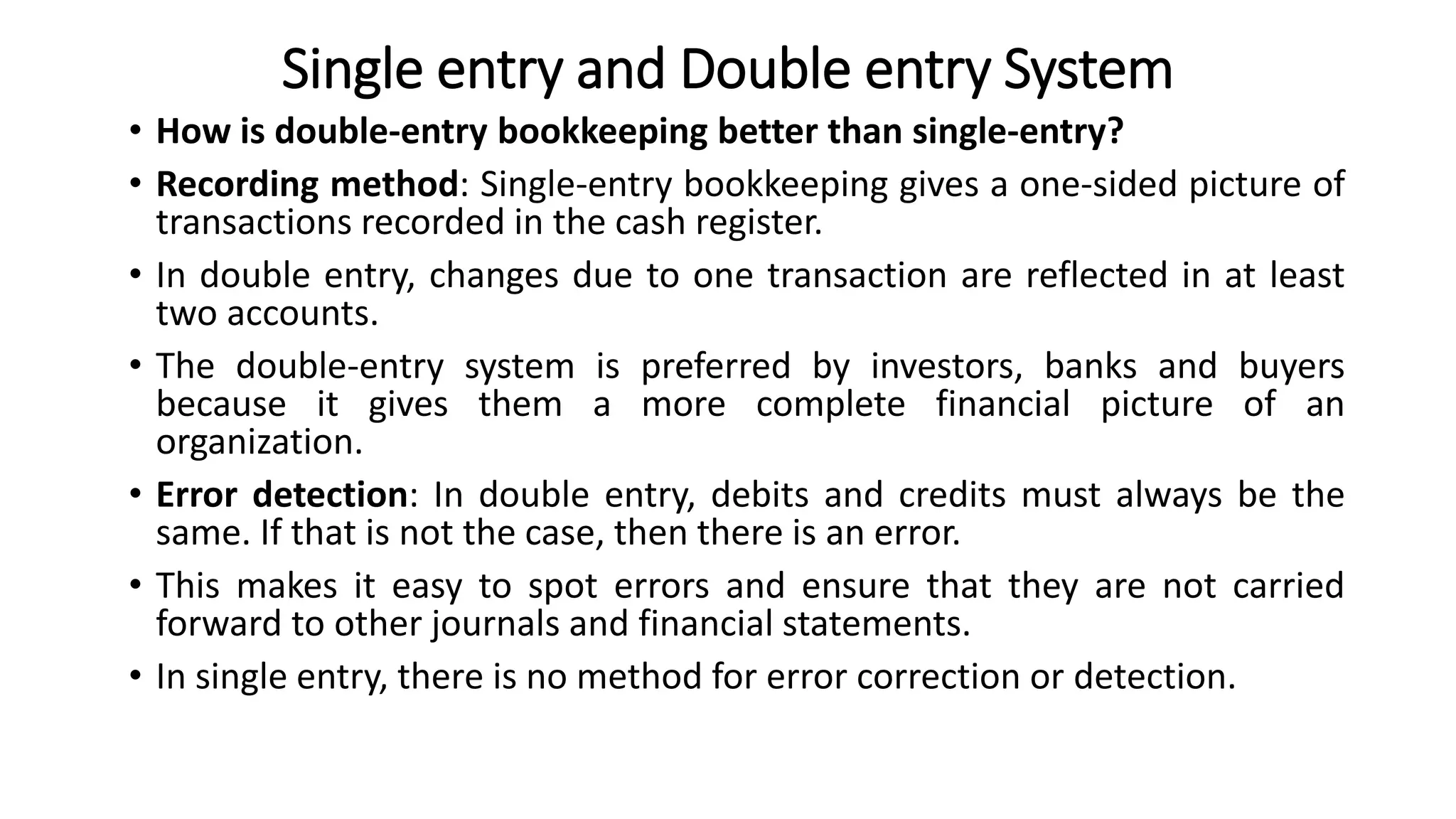

• How is double-entry bookkeeping better than single-entry?

• Recording method: Single-entry bookkeeping gives a one-sided picture of

transactions recorded in the cash register.

• In double entry, changes due to one transaction are reflected in at least

two accounts.

• The double-entry system is preferred by investors, banks and buyers

because it gives them a more complete financial picture of an

organization.

• Error detection: In double entry, debits and credits must always be the

same. If that is not the case, then there is an error.

• This makes it easy to spot errors and ensure that they are not carried

forward to other journals and financial statements.

• In single entry, there is no method for error correction or detection.

10.

Single entry andDouble entry System

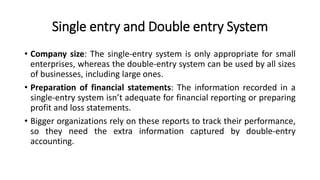

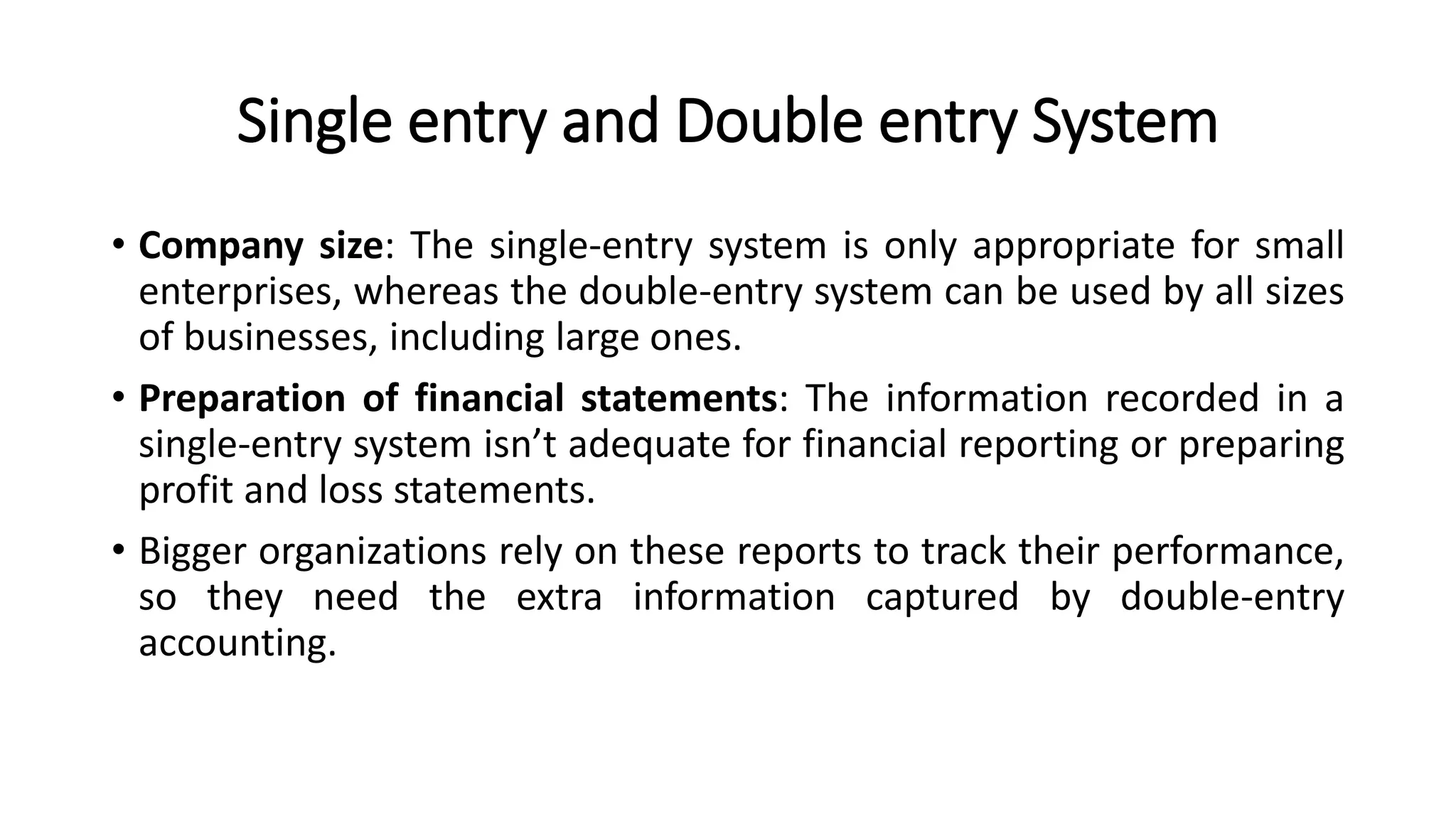

• Company size: The single-entry system is only appropriate for small

enterprises, whereas the double-entry system can be used by all sizes

of businesses, including large ones.

• Preparation of financial statements: The information recorded in a

single-entry system isn’t adequate for financial reporting or preparing

profit and loss statements.

• Bigger organizations rely on these reports to track their performance,

so they need the extra information captured by double-entry

accounting.