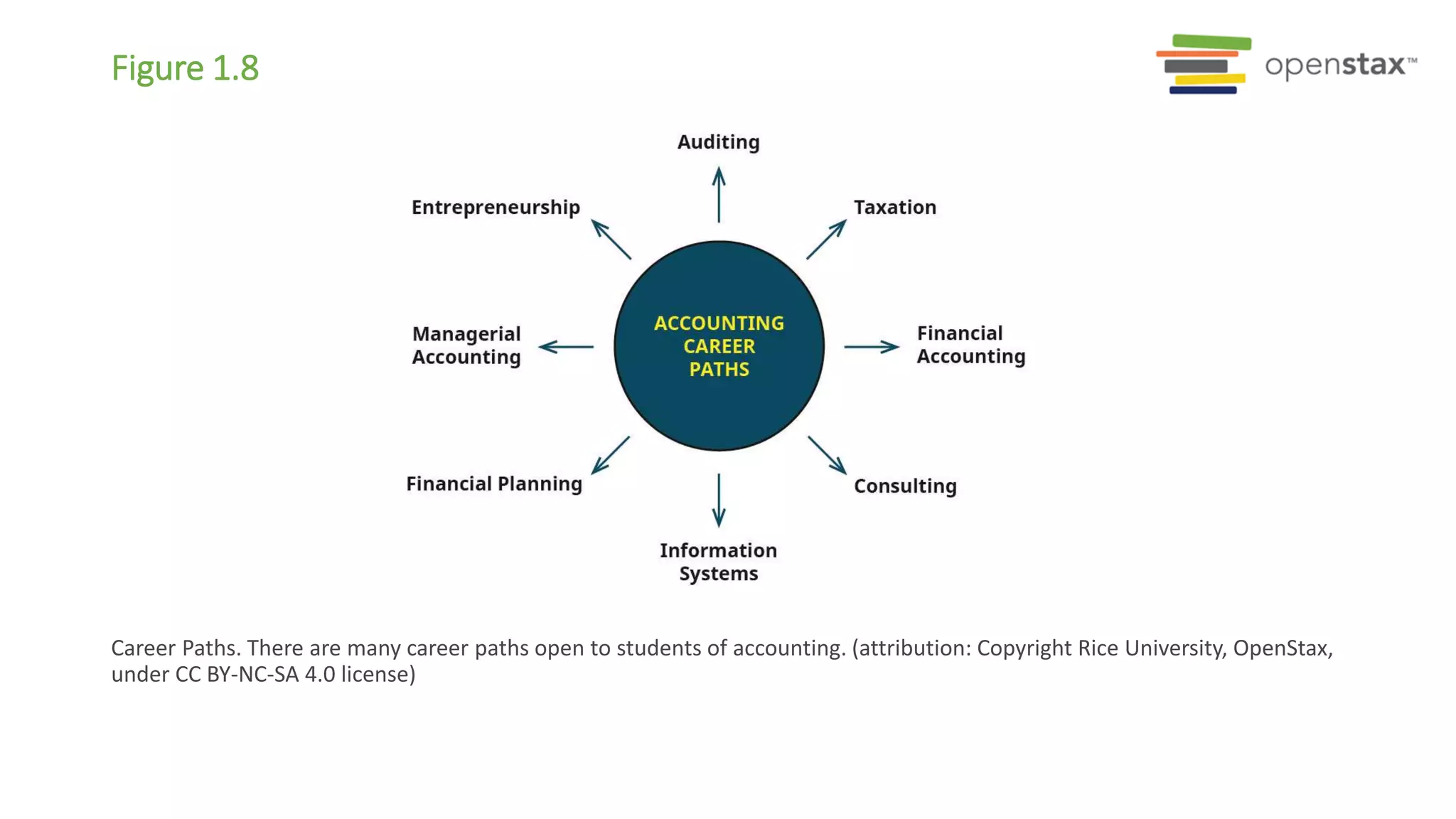

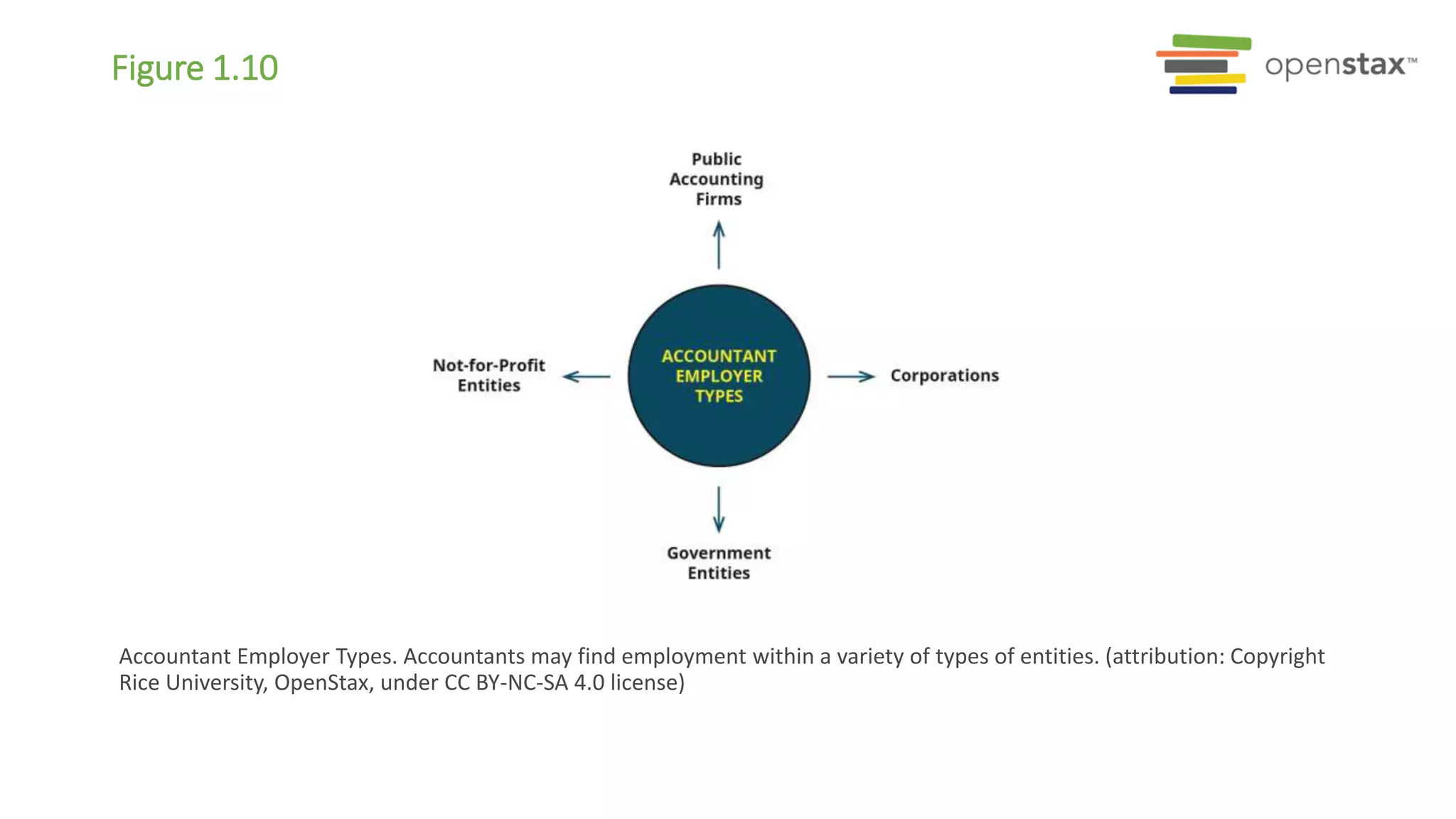

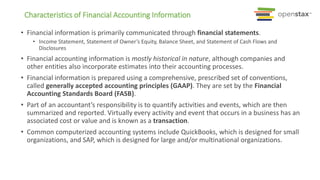

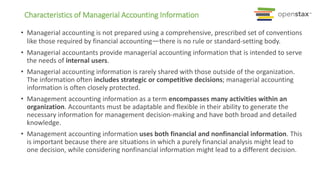

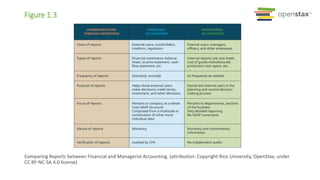

The document provides an overview of accounting, including distinguishing between financial and managerial accounting. It describes typical accounting activities such as identifying, recording, and reporting financial transactions. It explains that accounting provides important information to various stakeholders, including owners, lenders, managers, and government agencies. It also outlines different career paths for accountants in fields like auditing, taxation, and financial planning.

![Your Turn: Daily Decisions

Many academic studies have been conducted on the topic of consumer

behavior and decision-making. It is a fascinating topic of study that attempts

to learn what type of advertising works best, the best place to locate a

business, and many other business-related activities.

One such study, conducted by researchers at Cornell University, concluded

that people make more than 200 food-related decisions per day (Wansink,

B., & Sobal, J. [2007]. Mindless Eating: The 200 Daily Food Decisions We

Overlook. Environment & Behavior, 39[1], 106–123.).

This is astonishing considering the number of decisions found in this

particular study related only to decisions involving food. Imagine how many

day-to-day decisions involve other issues that are important to us, such as

what to wear and how to get from point A to point B. For this exercise,

provide and discuss some of the food-related decisions that you recently

made.](https://image.slidesharecdn.com/acct5x10module1slidedeck-190715161938/85/Role-of-Accounting-15-320.jpg)

![Your Turn: Daily Decisions

Many academic studies have been conducted on the topic of consumer

behavior and decision-making. It is a fascinating topic of study that attempts

to learn what type of advertising works best, the best place to locate a

business, and many other business-related activities.

One such study, conducted by researchers at Cornell University, concluded

that people make more than 200 food-related decisions per day (Wansink,

B., & Sobal, J. [2007]. Mindless Eating: The 200 Daily Food Decisions We

Overlook. Environment & Behavior, 39[1], 106–123.).

This is astonishing considering the number of decisions found in this

particular study related only to decisions involving food. Imagine how many

day-to-day decisions involve other issues that are important to us, such as

what to wear and how to get from point A to point B. For this exercise,

provide and discuss some of the food-related decisions that you recently

made.](https://image.slidesharecdn.com/acct5x10module1slidedeck-190715161938/75/Role-of-Accounting-15-2048.jpg)