Downloaded 498 times

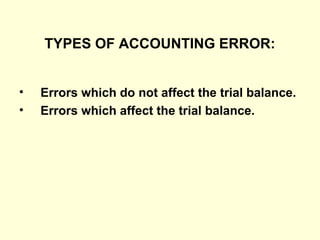

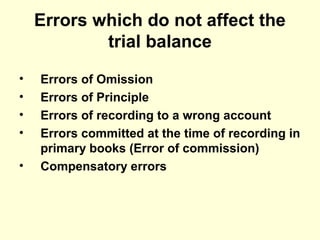

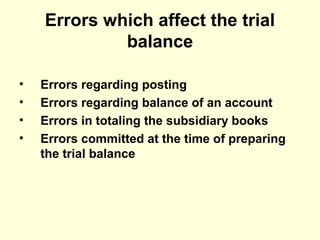

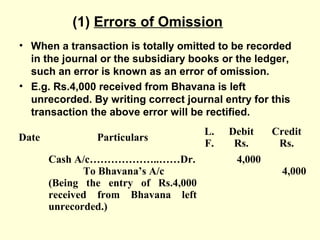

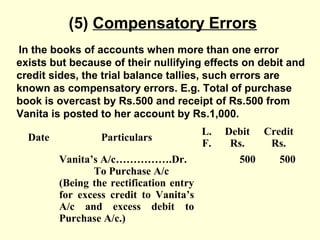

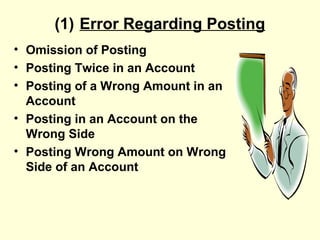

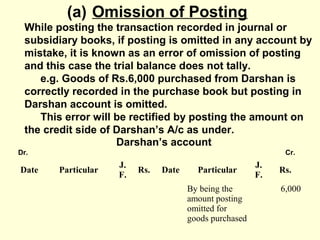

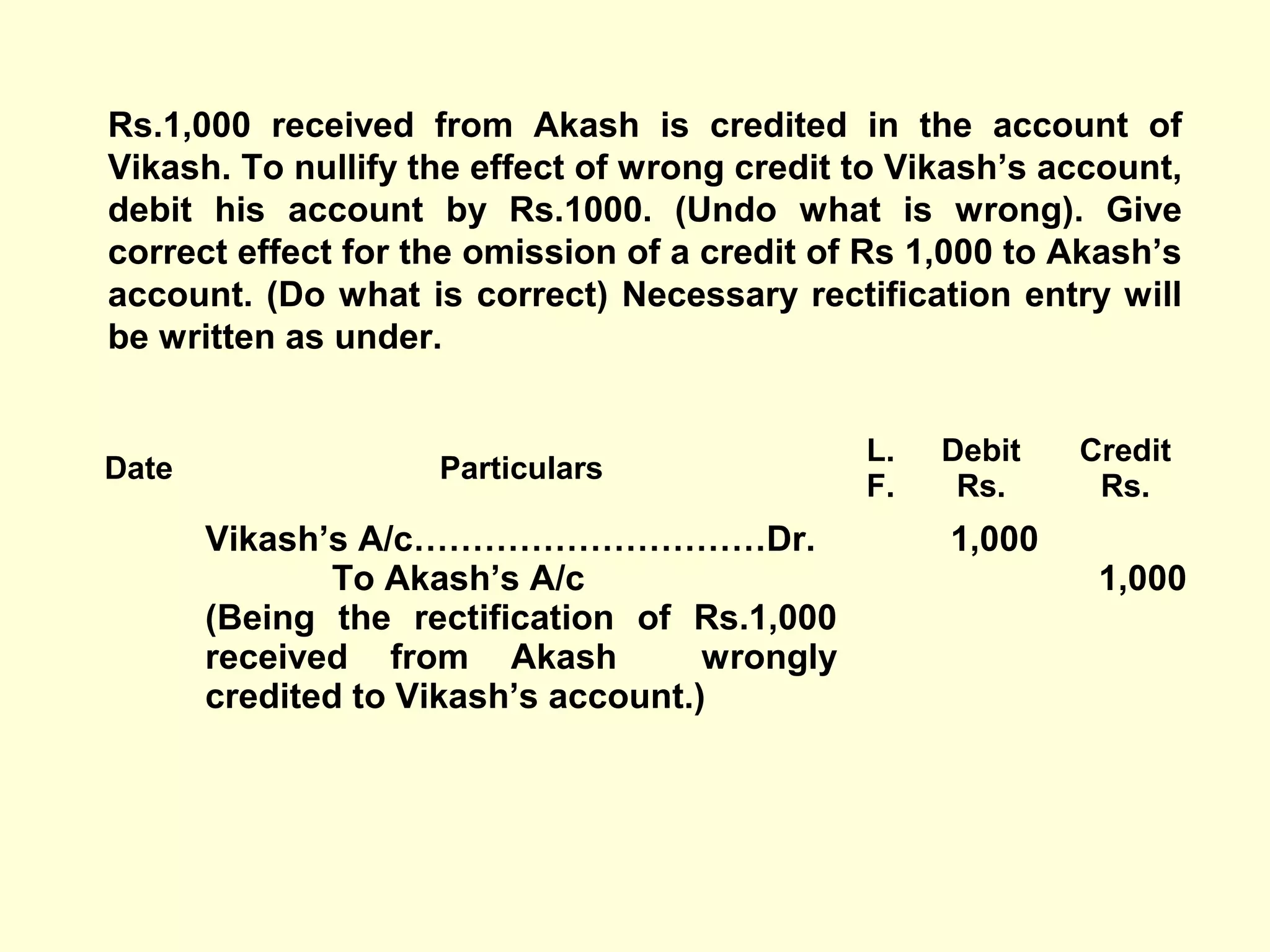

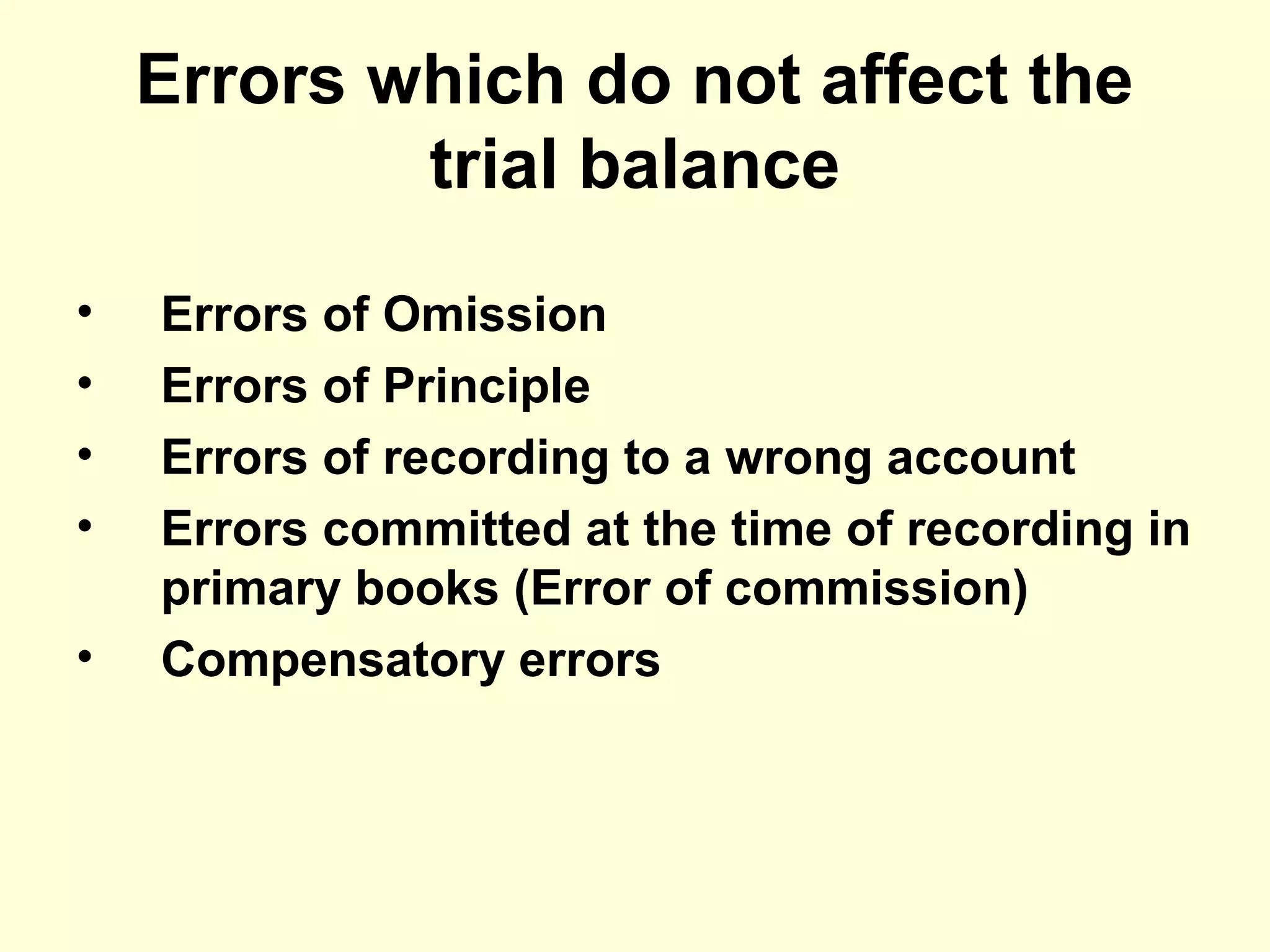

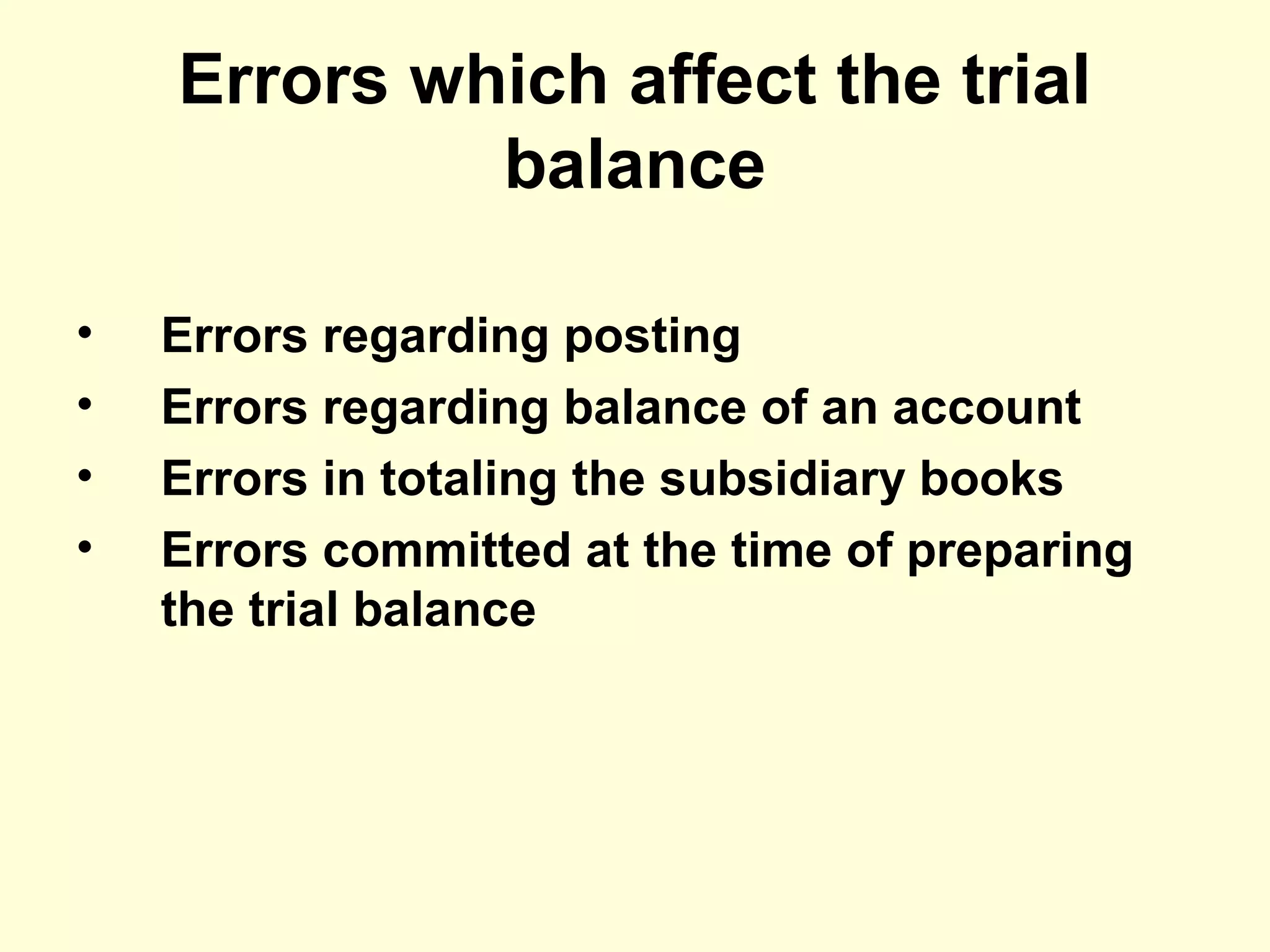

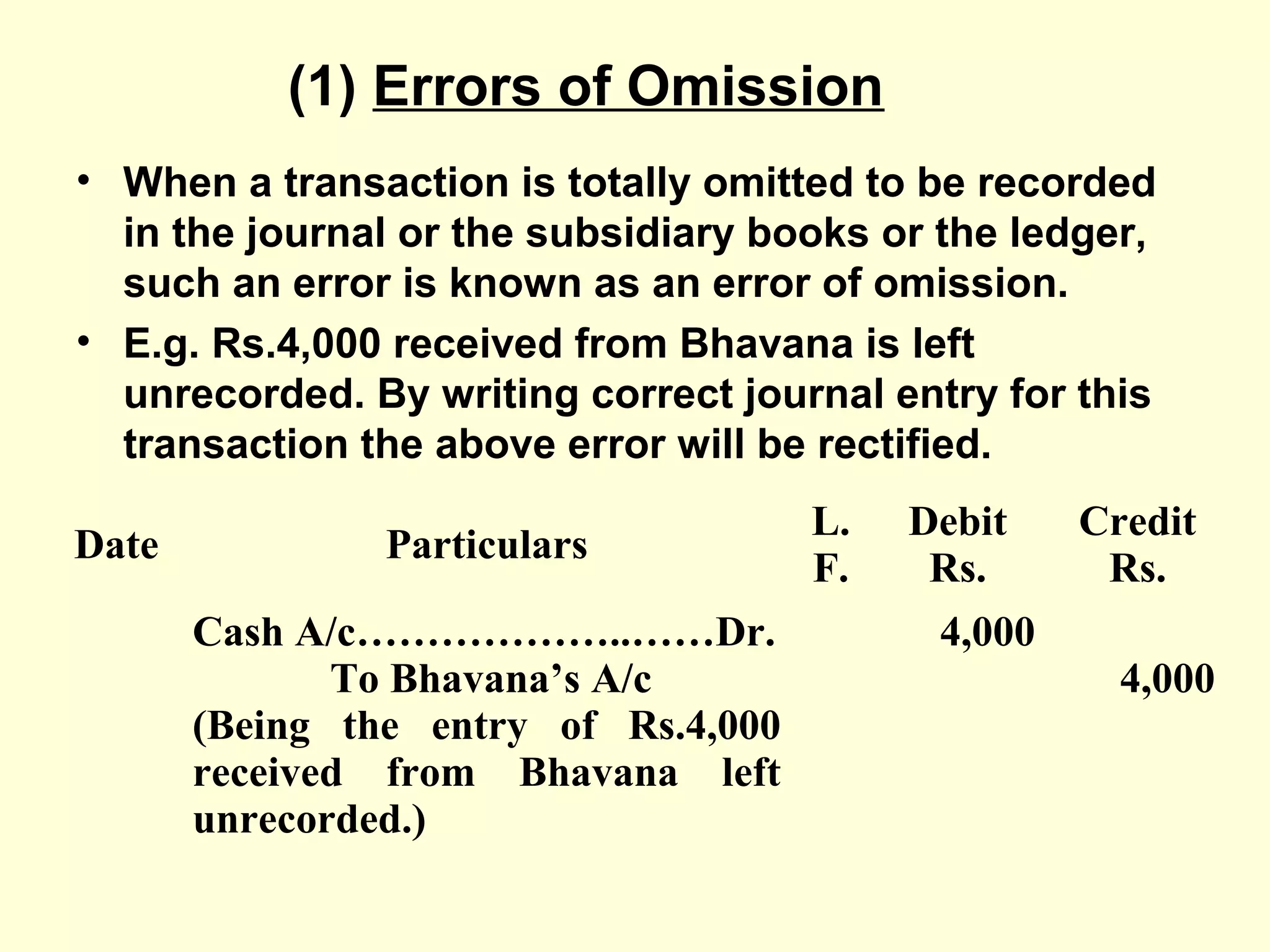

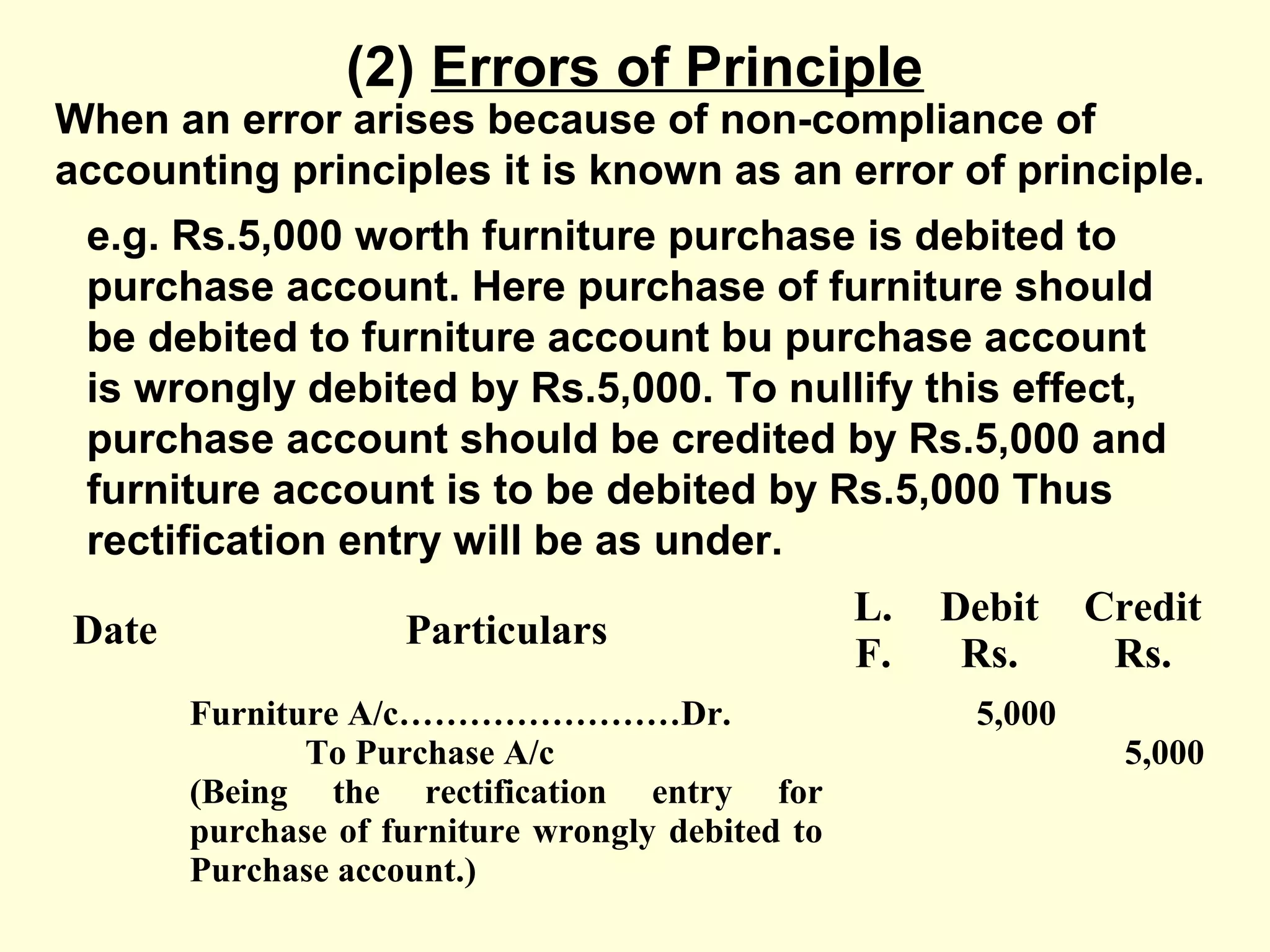

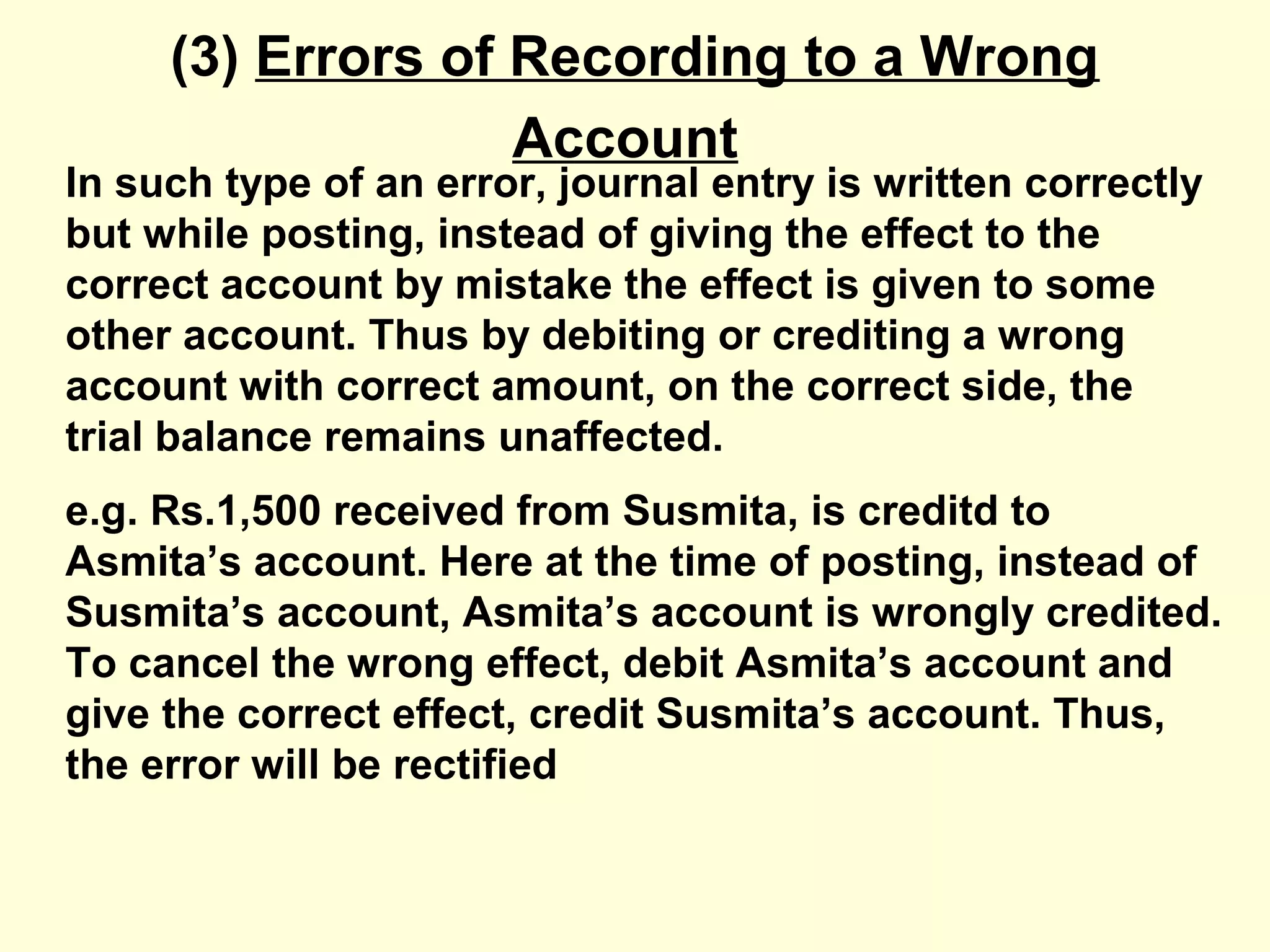

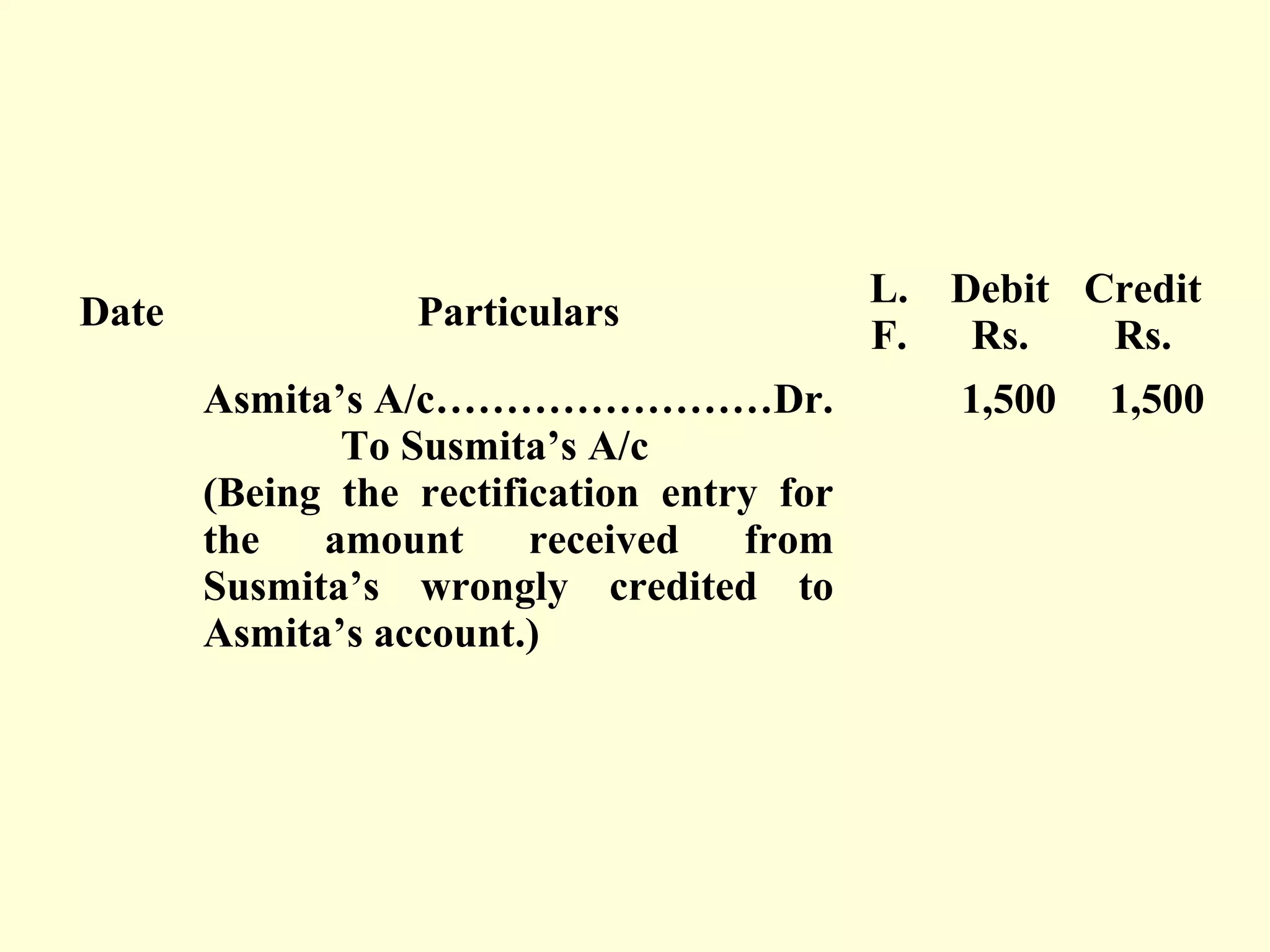

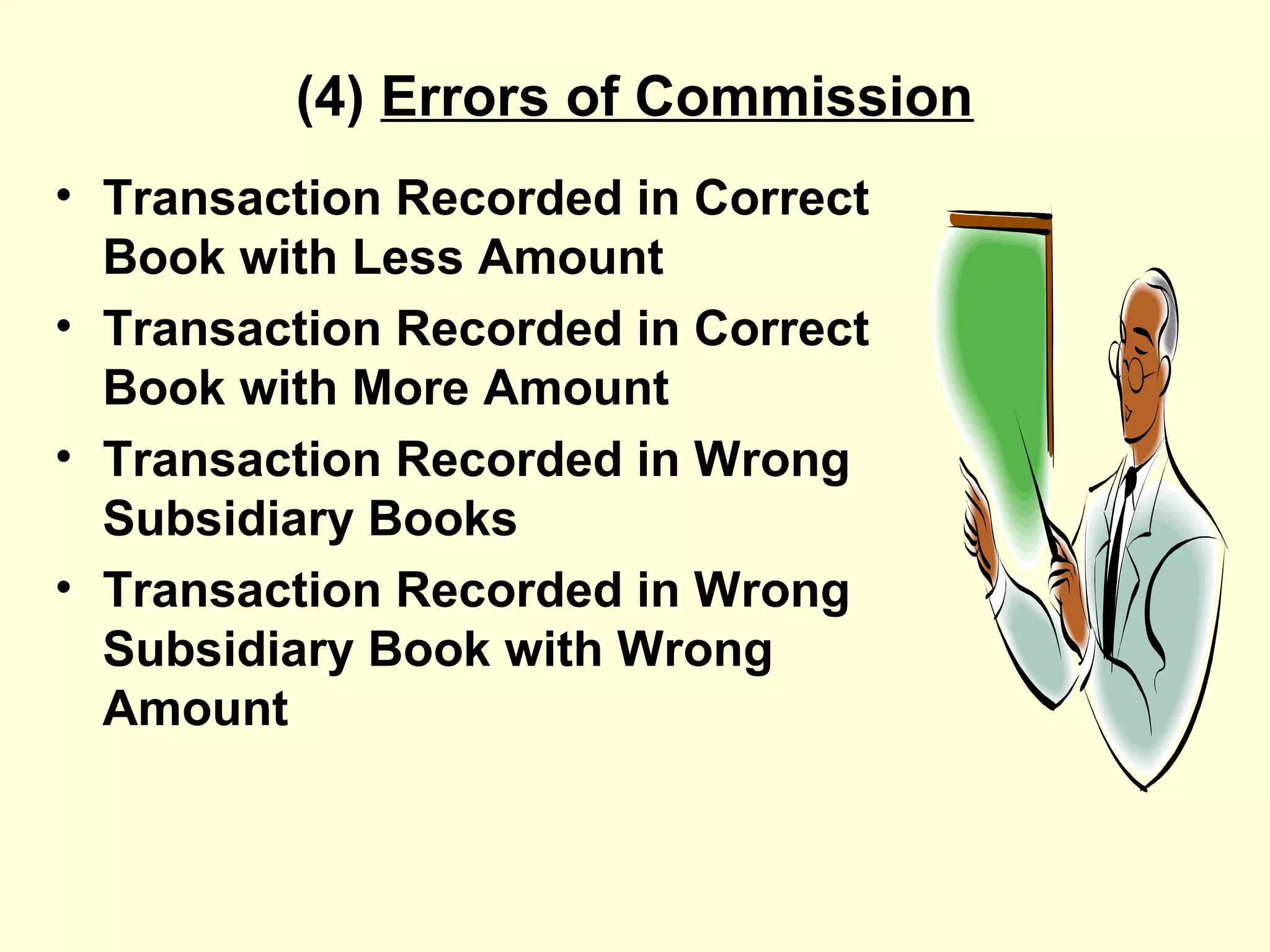

This document discusses various types of accounting errors and how to rectify them. It begins by explaining the need to rectify errors, whether innocent or intentional, by passing rectification journal entries. It then categorizes errors into those that do not affect the trial balance, such as errors of omission, principle, or recording to the wrong account, and those that do affect the trial balance, such as errors in posting, account balances, or preparing the trial balance. For each type of error, examples are provided and the rectifying journal entry is shown. The document emphasizes the principles of "undoing what is wrong" and "doing what is correct" to rectify accounting errors.