Downloaded 943 times

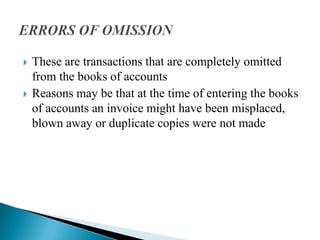

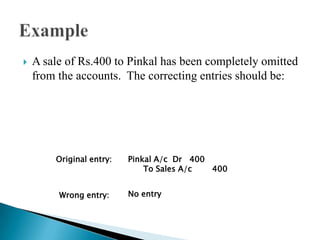

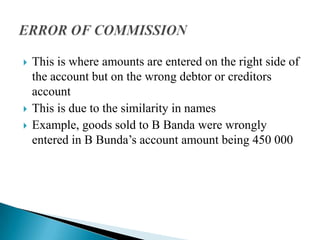

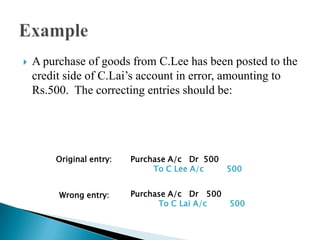

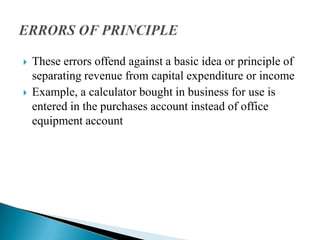

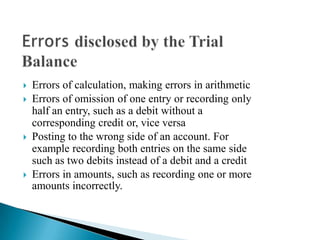

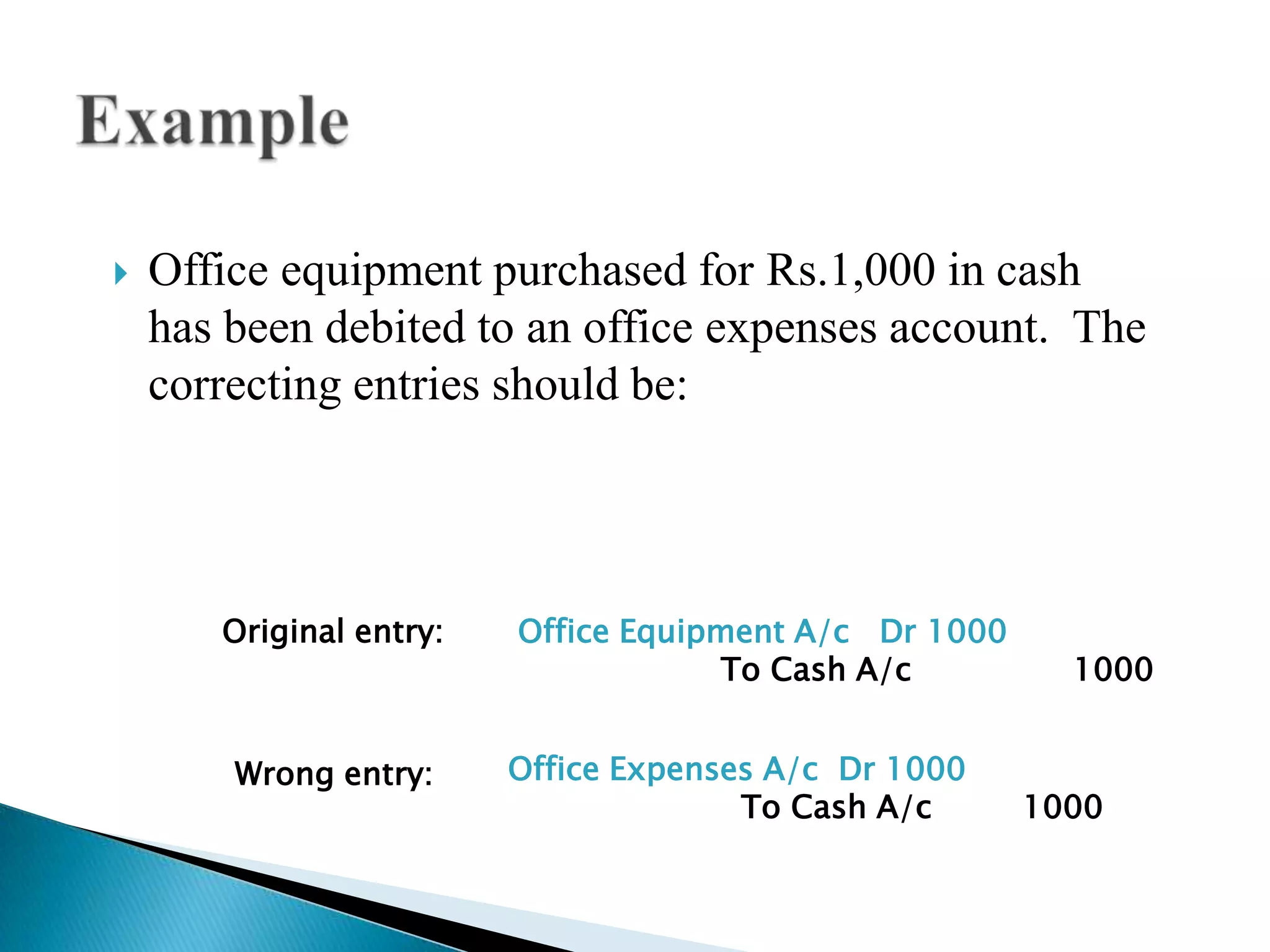

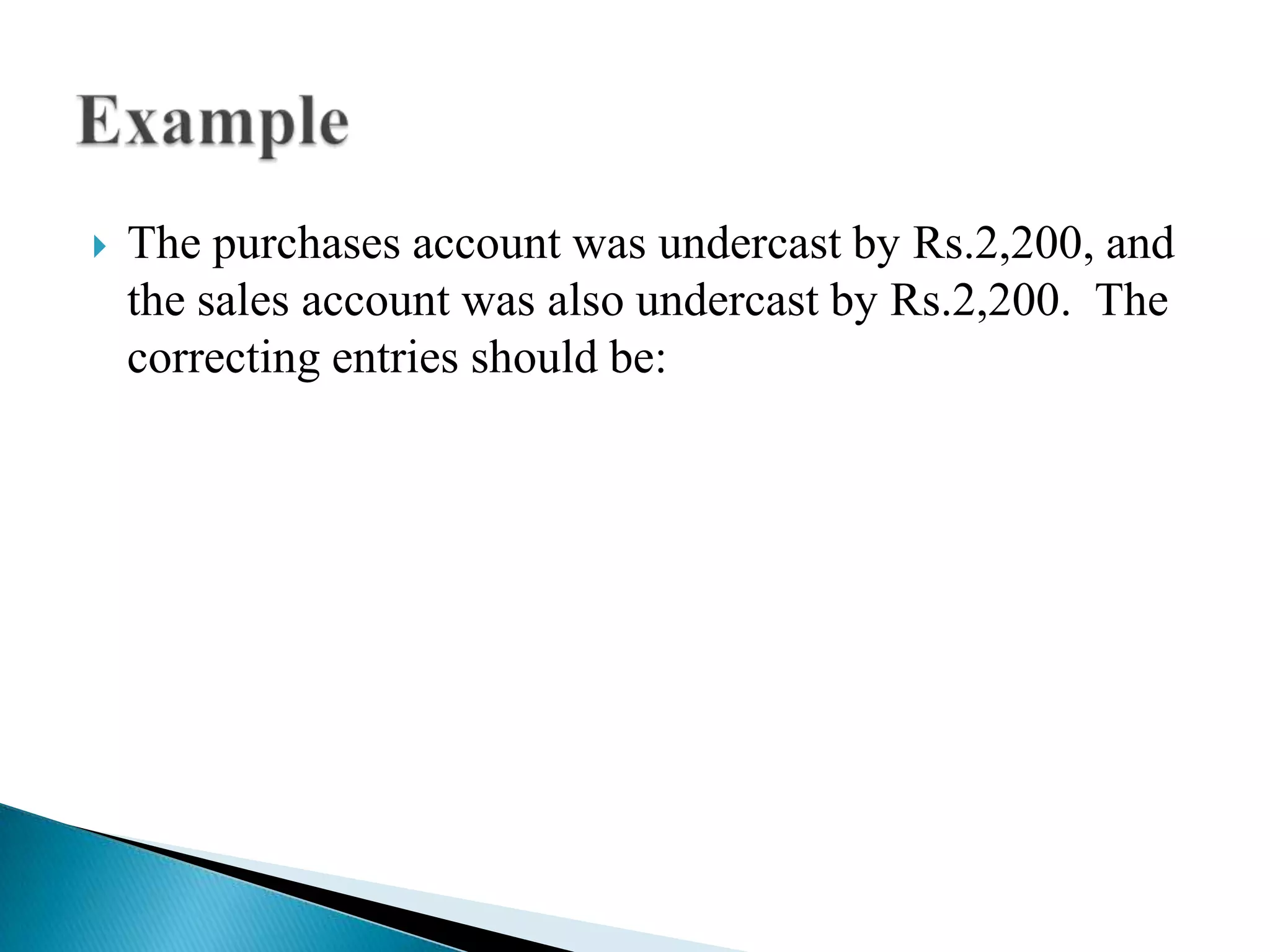

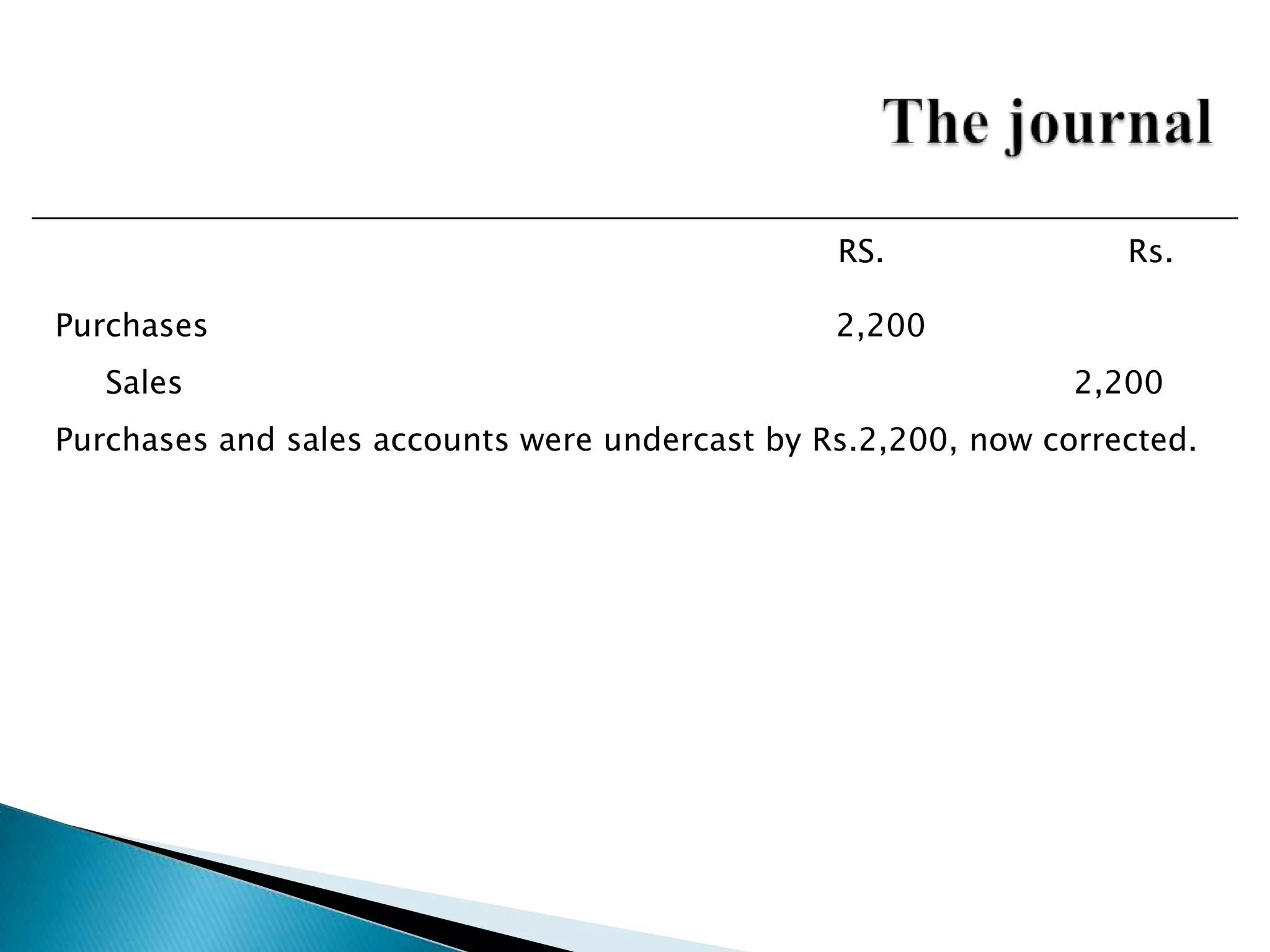

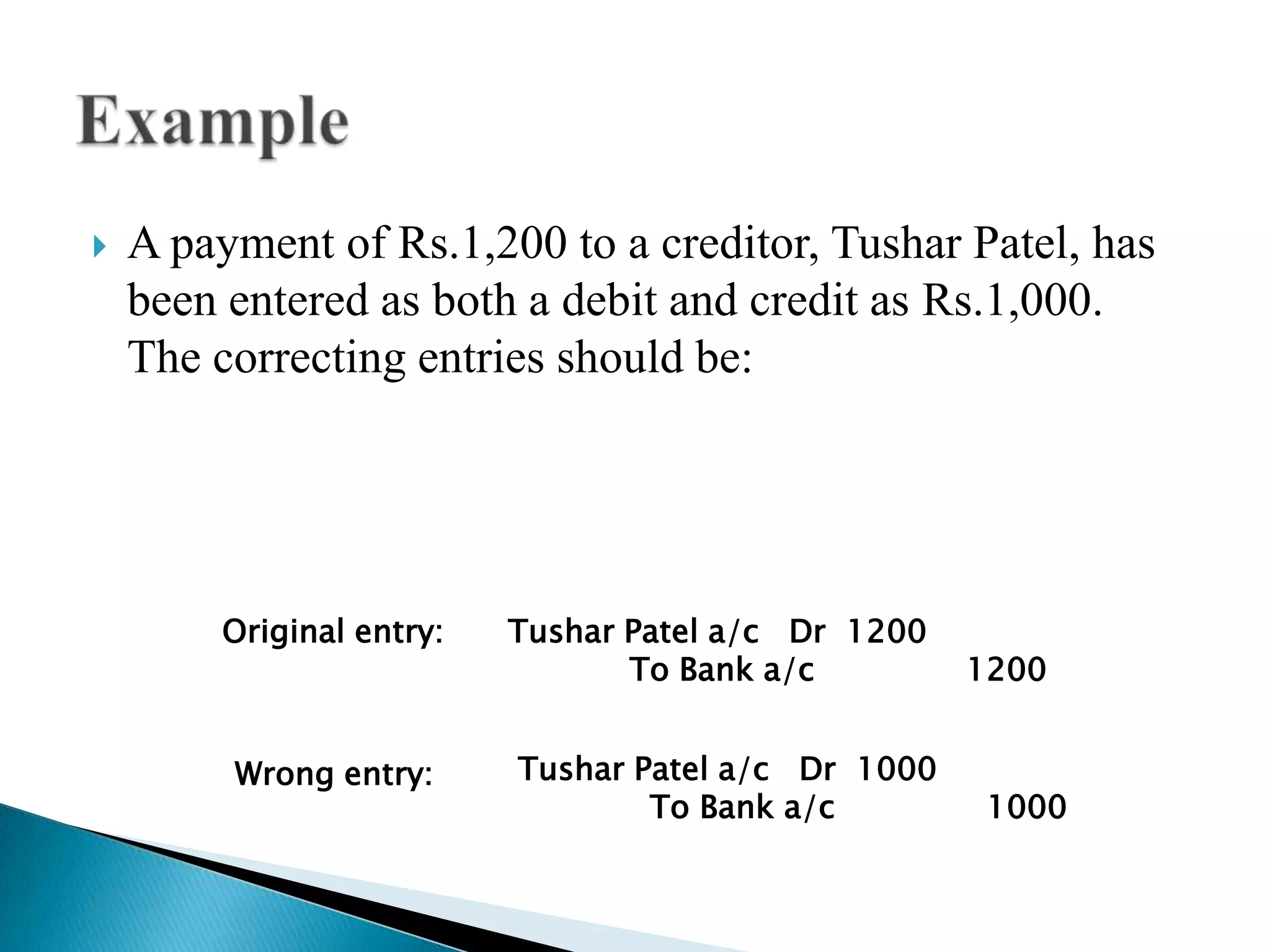

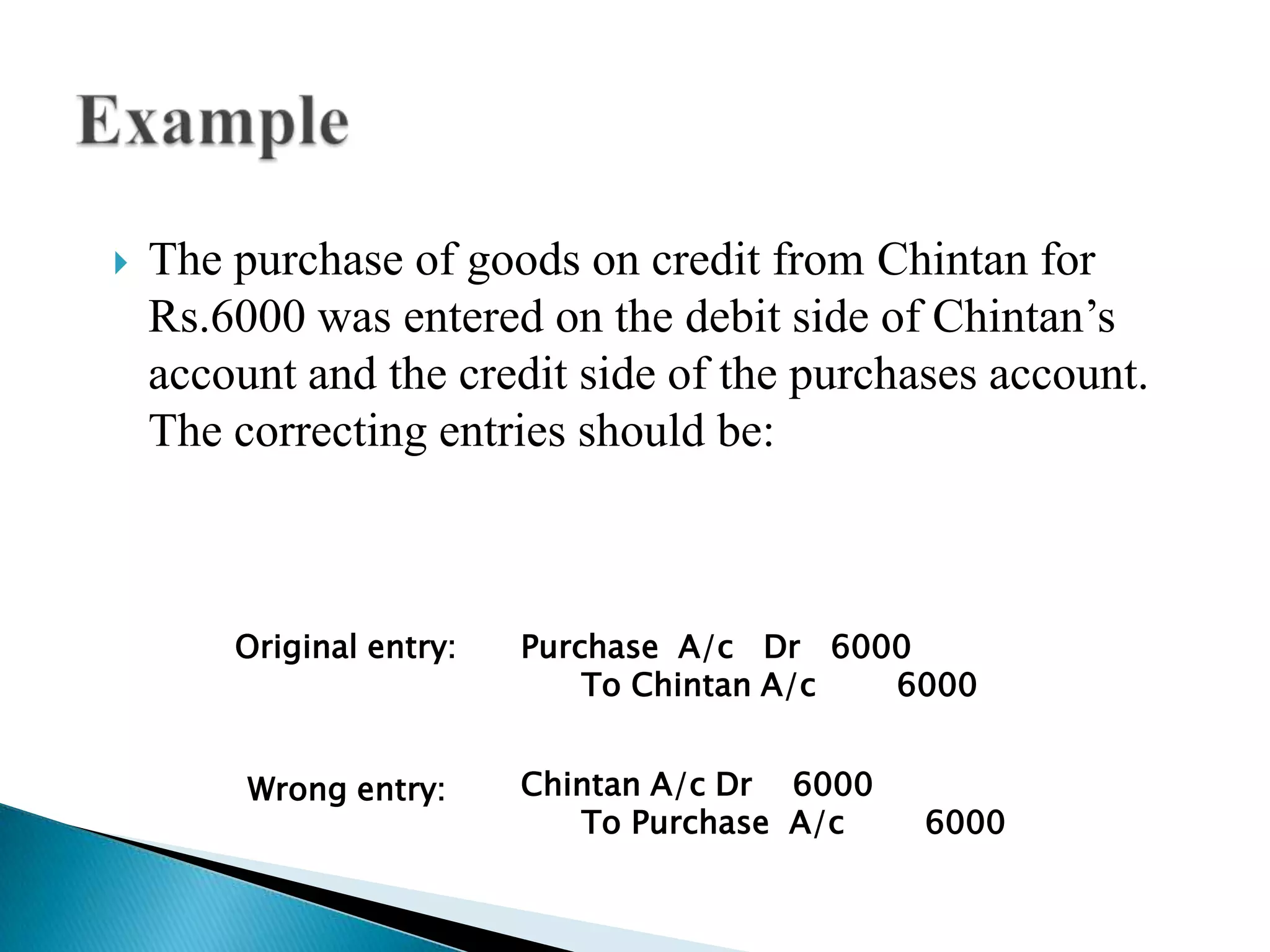

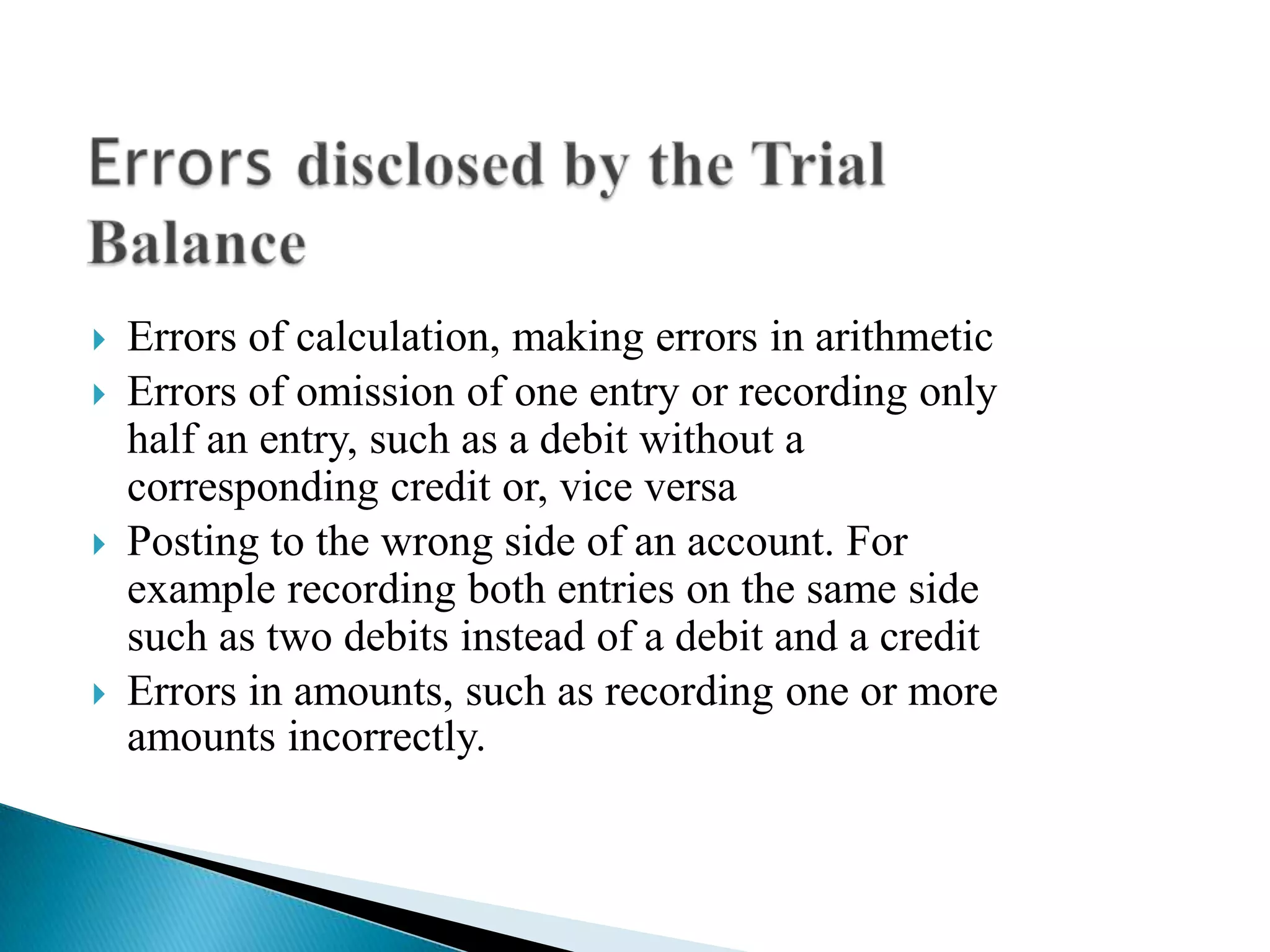

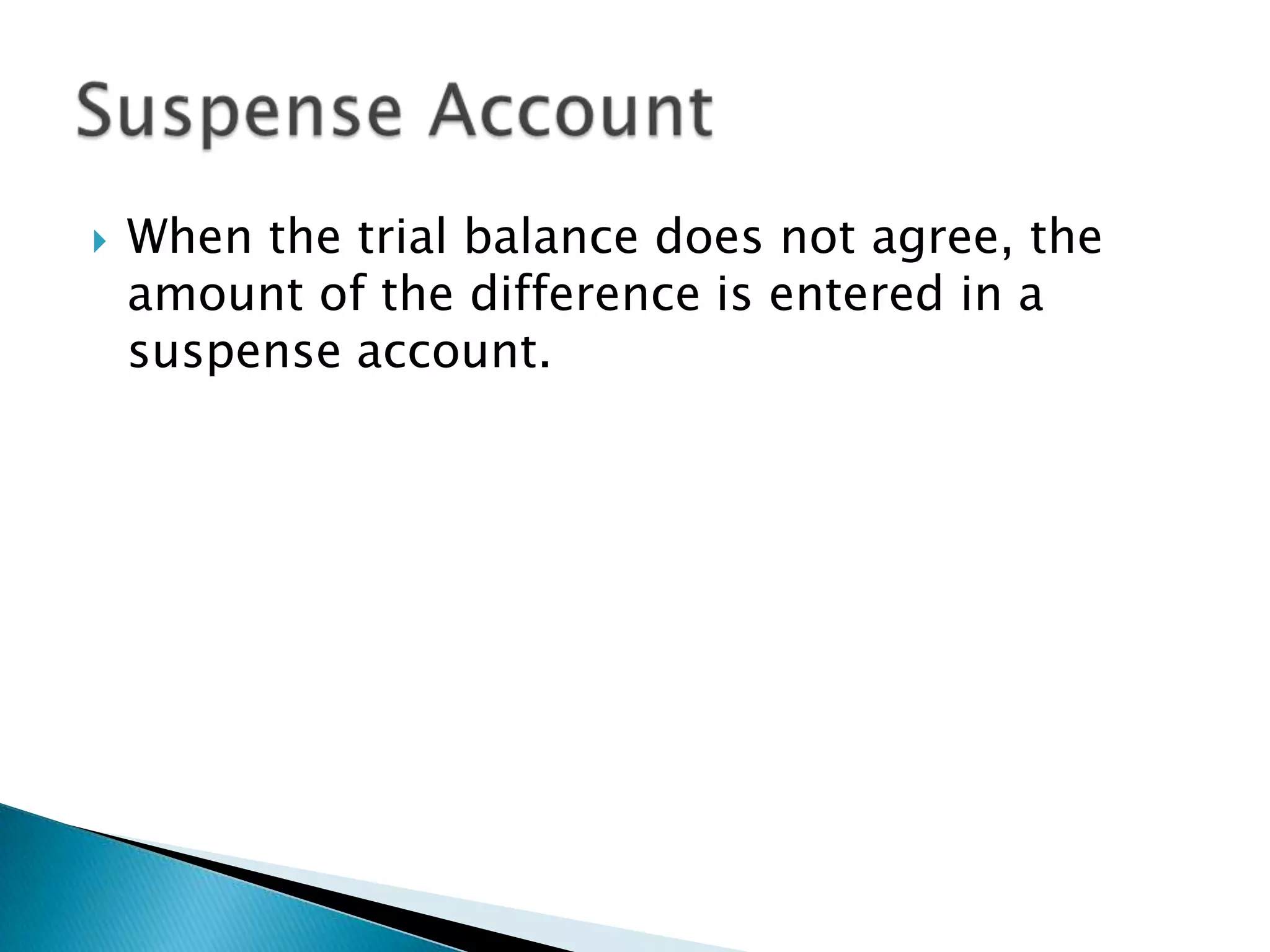

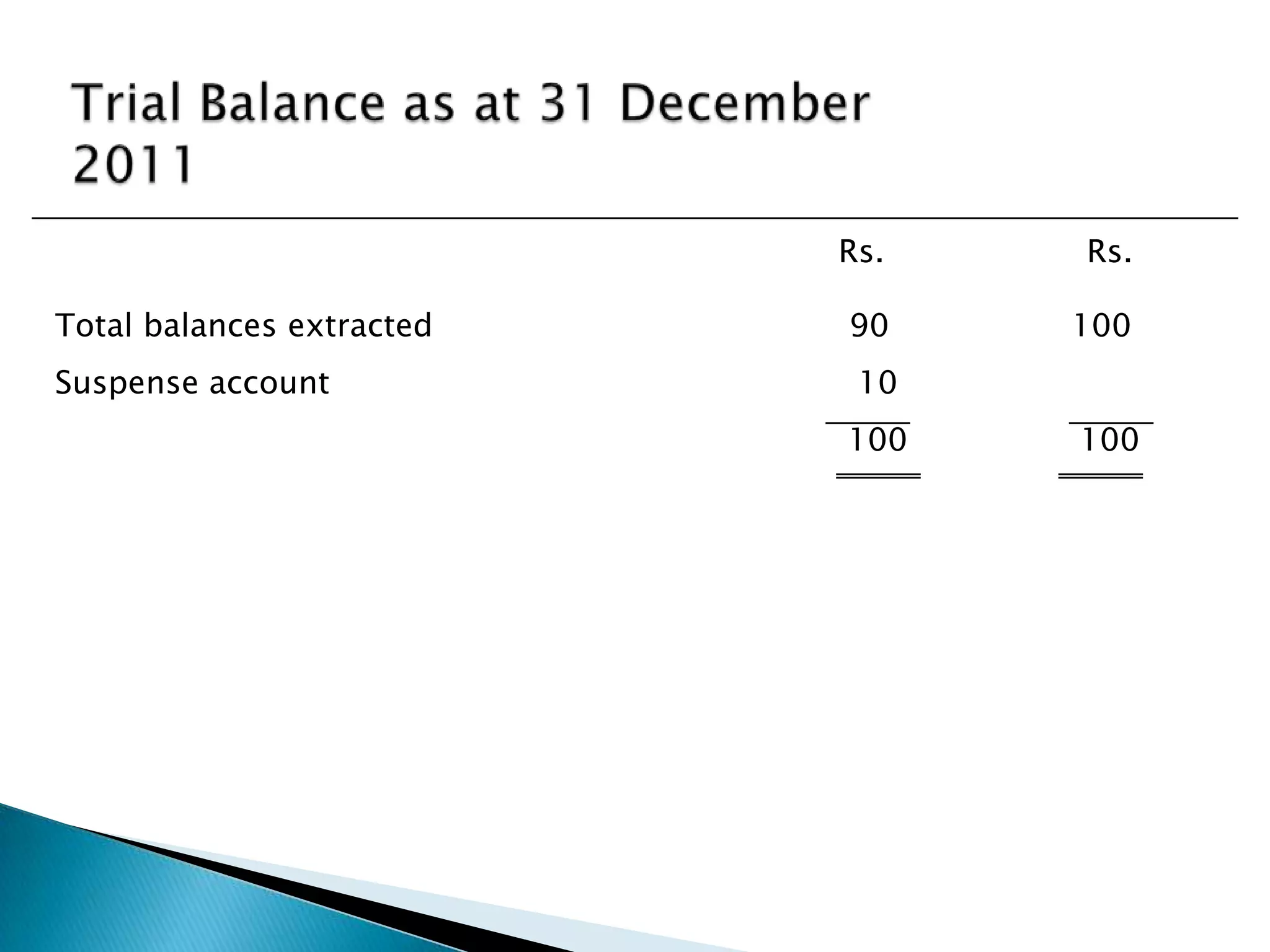

The document discusses types of errors that can occur in accounting records and trial balances. It explains that a trial balance checks the arithmetic accuracy of accounts but not necessarily their accuracy. Errors can be of omission, commission, principle, compensation, original entry, or complete reversal. Specific examples are provided of different error types and the correcting journal entries.

Explains trial balance definitions, discrepancies, error types, and corrections in accounting entries.