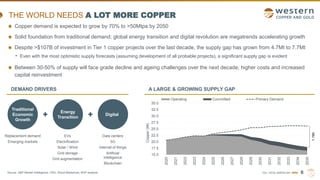

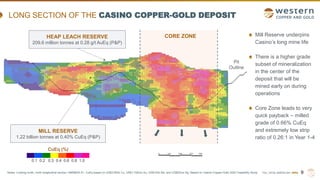

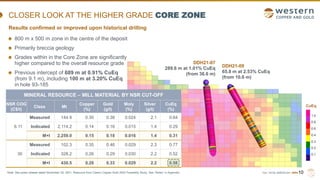

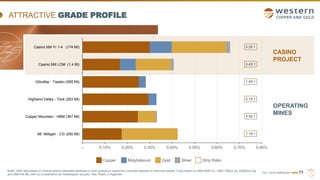

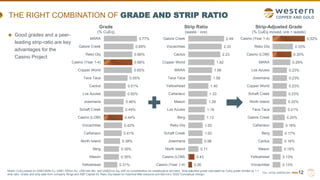

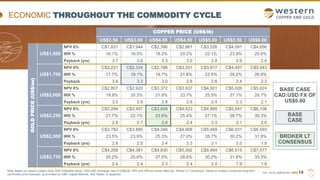

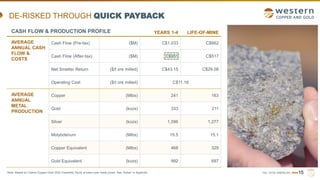

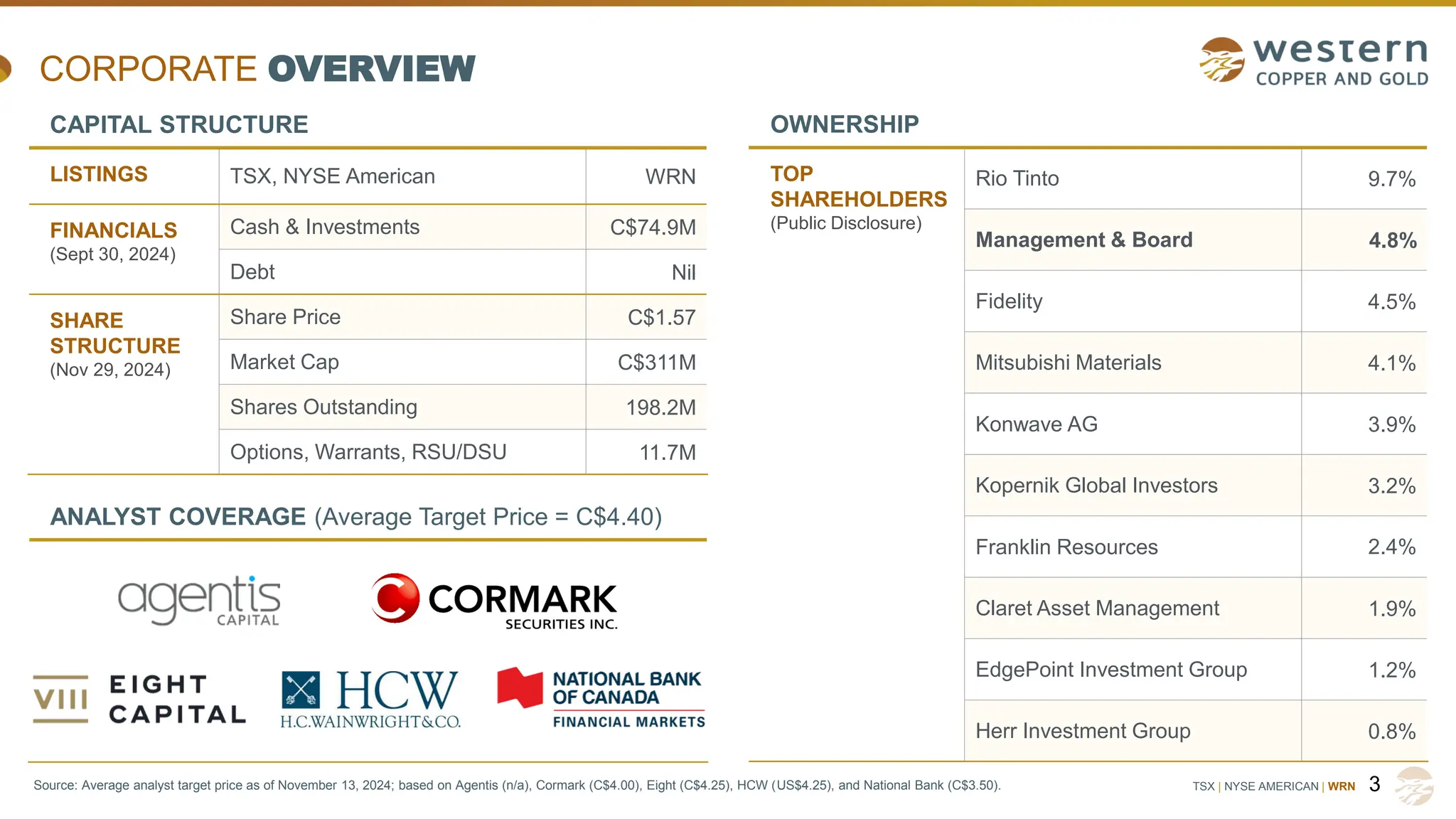

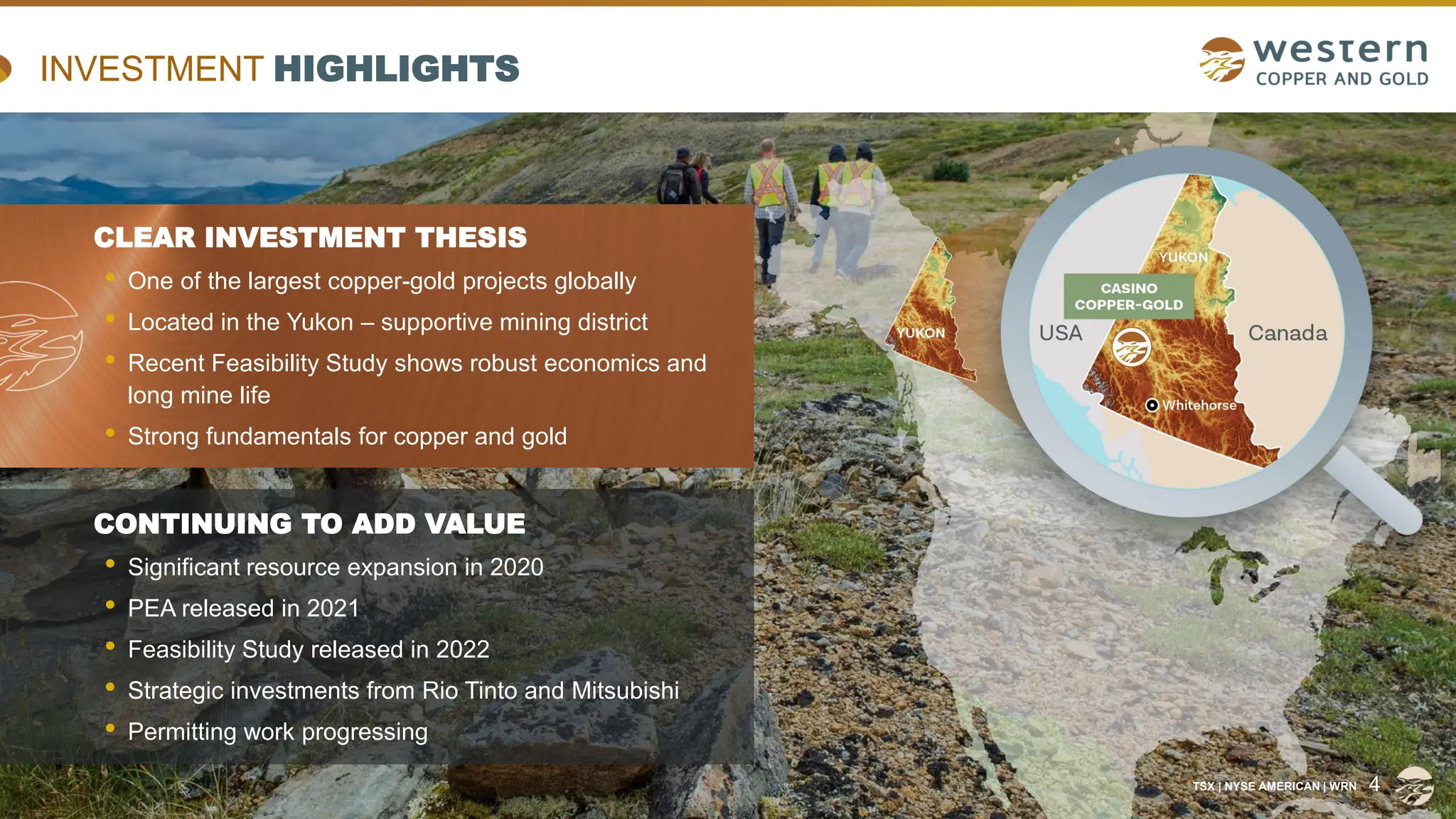

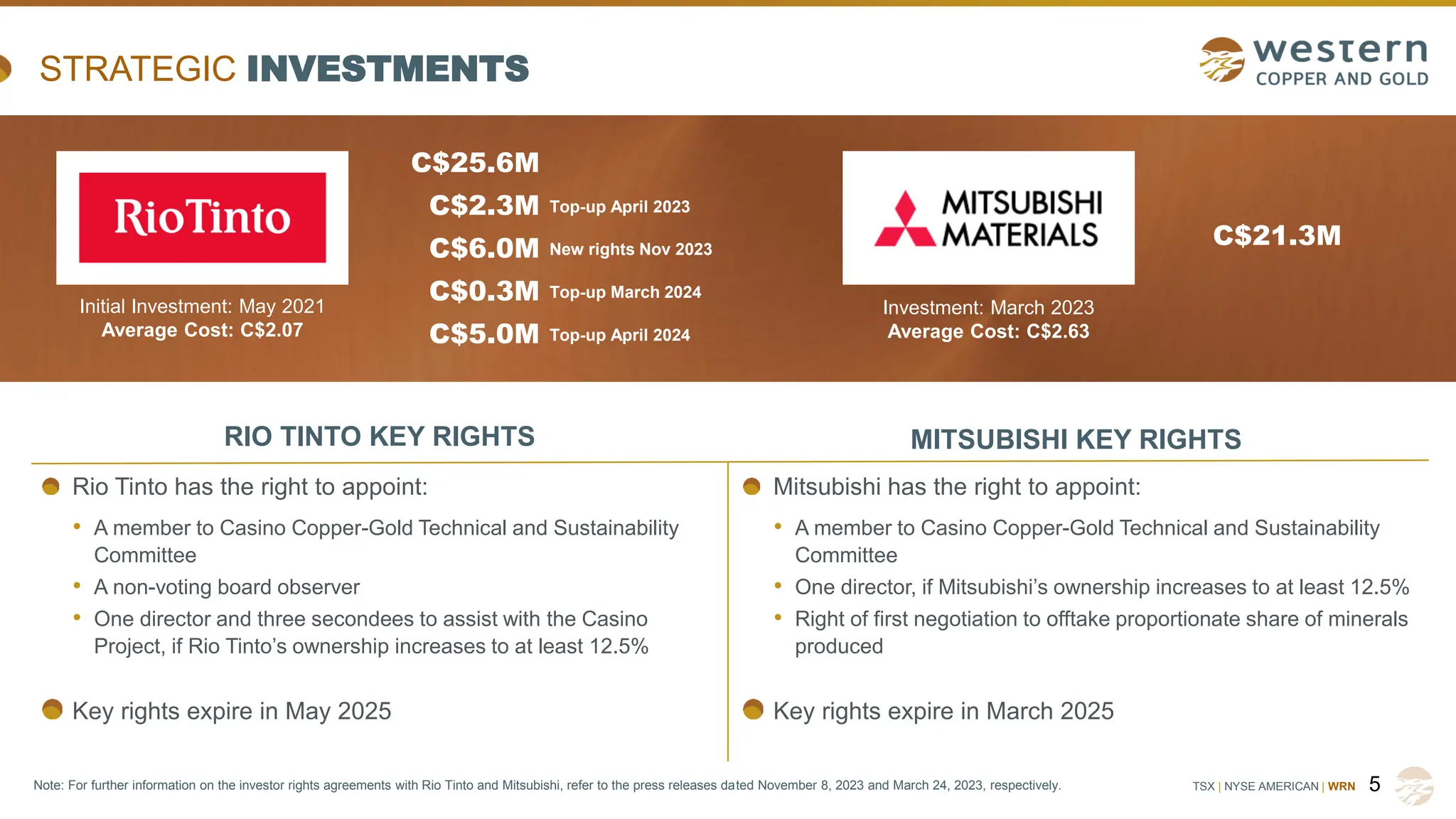

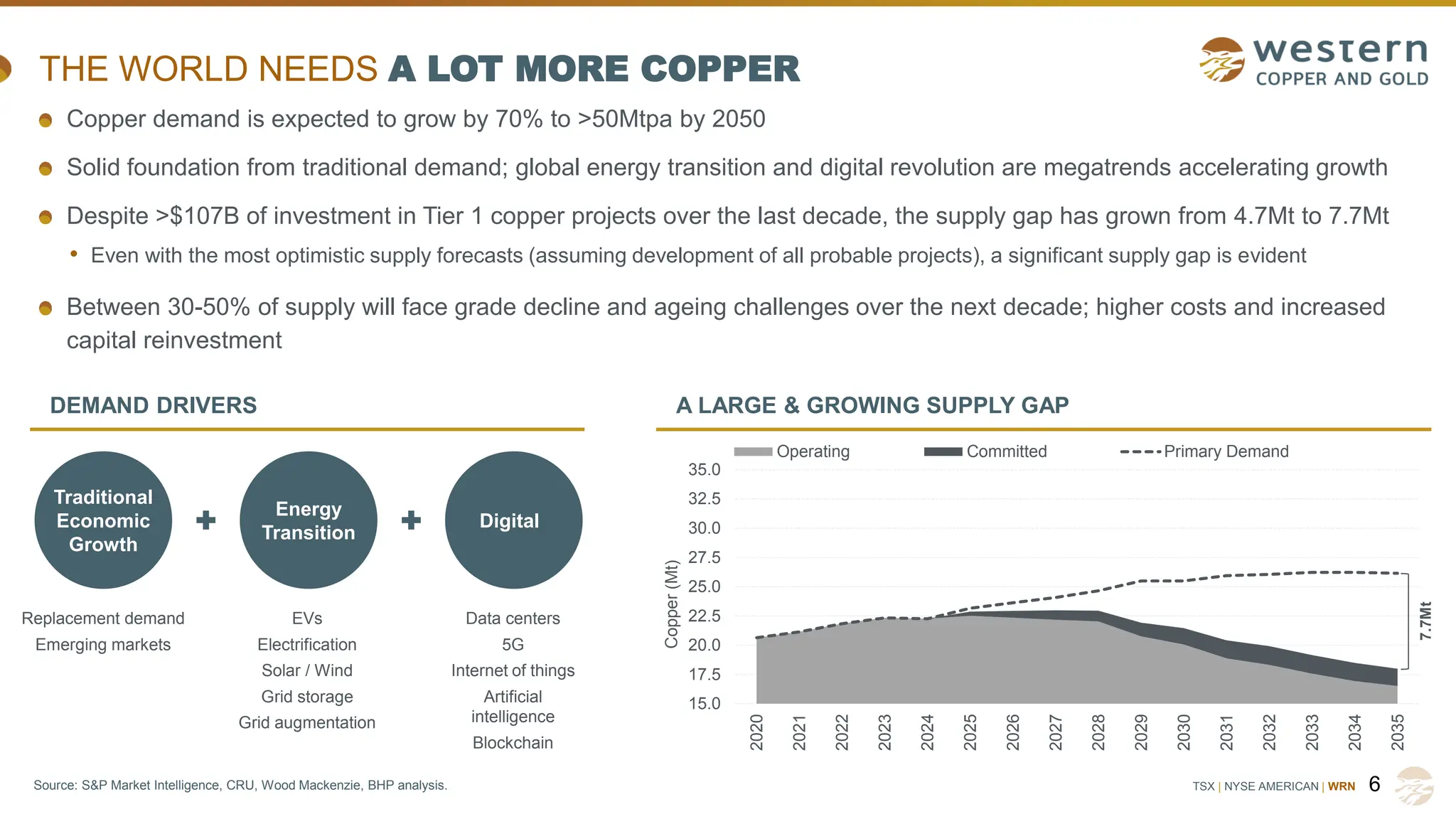

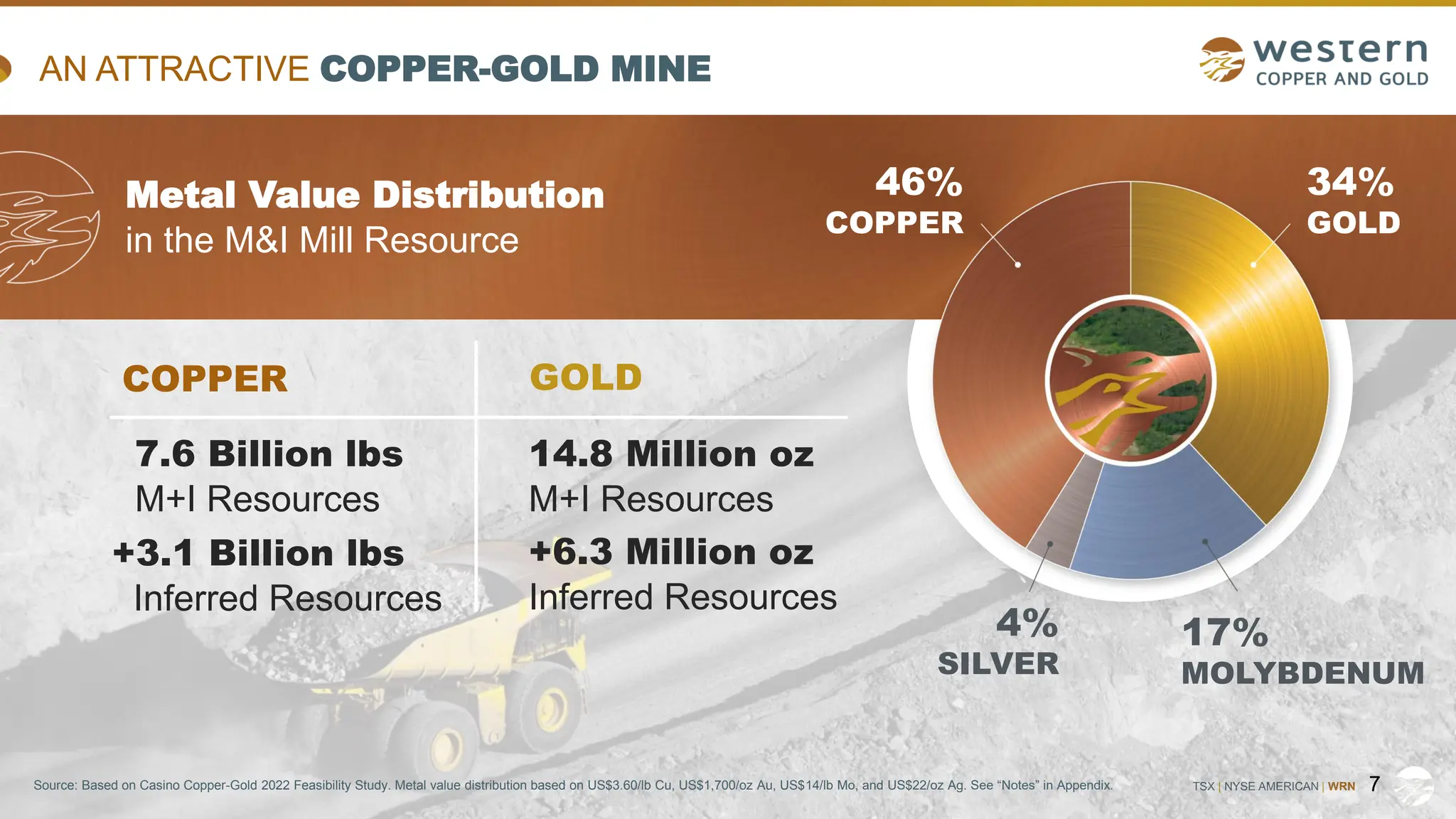

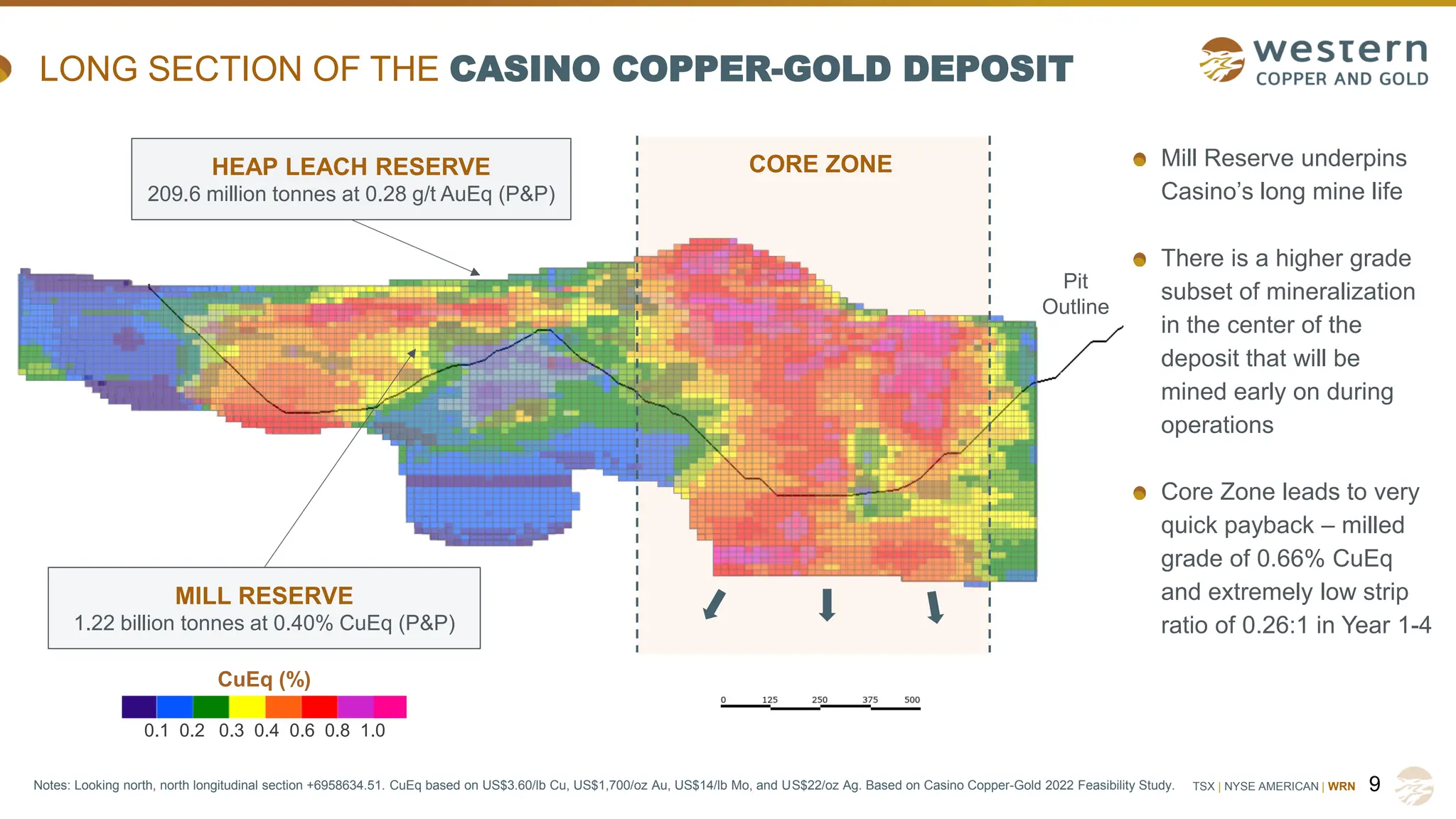

The document presents an overview of Western Copper and Gold Corporation's Casino copper-gold project, emphasizing its position as one of the largest copper-gold projects globally with strong fundamentals and potential for future growth. It outlines the company's financial structure, strategic investments from major players like Rio Tinto and Mitsubishi, and provides details on mineral reserves and resources as well as associated risks. The presentation also discusses the projected increase in copper demand due to global trends, highlighting the project's attractiveness in addressing the supply gap.