Download as PDF, PPTX

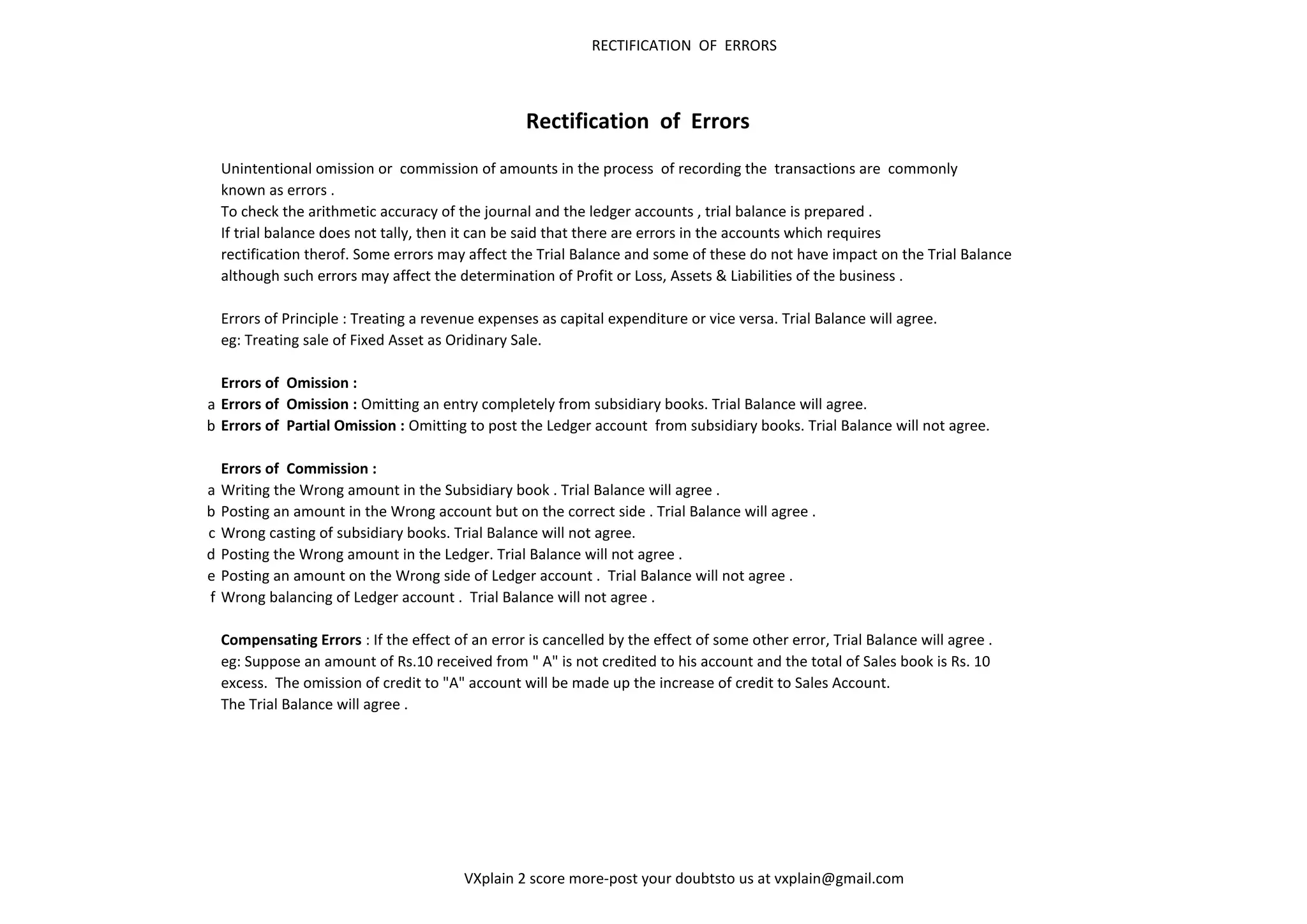

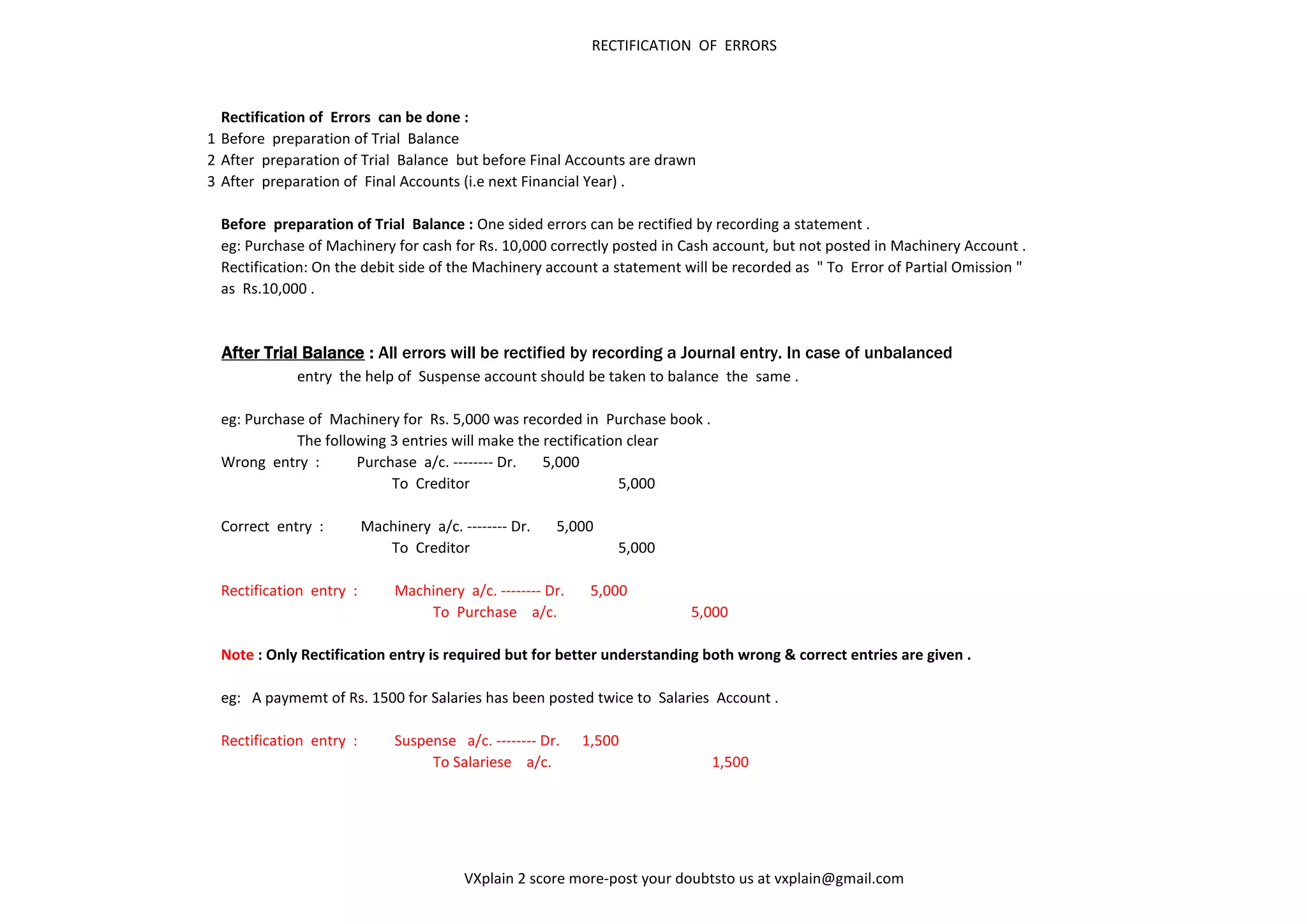

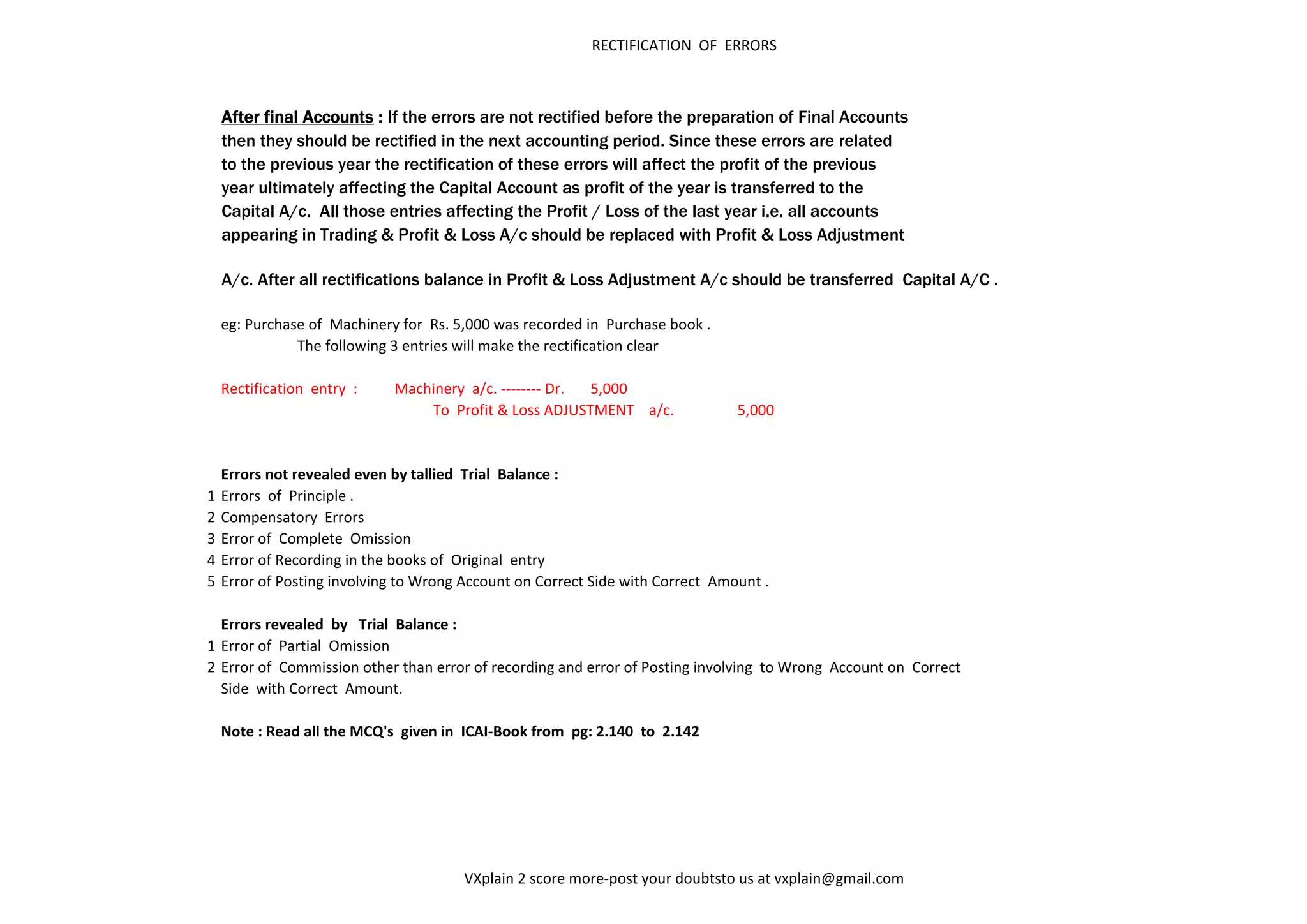

Rectification of errors involves correcting mistakes made in recording accounting transactions. Errors can occur during recording in journals or ledgers. A trial balance is prepared to check for errors, as errors will cause it to be out of balance. There are different types of errors such as errors of principle, omission, commission, and compensating errors. Errors are rectified through journal entries, with a suspense account used if needed to balance entries. Errors found after accounts are finalized still require rectification, which impacts the previous year's profit and capital.