0% found this document useful (0 votes)

12 views5 pagesExample Example Analysis Variations

The document presents an analysis of variations between the budget and the actual sales for the month of April for 13 models. It is observed that total sales were lower than budgeted, mainly due to reductions in price and sales volume of several models. Some models exceeded planned sales thanks to higher selling prices or greater quantities sold.

Uploaded by

ScribdTranslationsCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

12 views5 pagesExample Example Analysis Variations

The document presents an analysis of variations between the budget and the actual sales for the month of April for 13 models. It is observed that total sales were lower than budgeted, mainly due to reductions in price and sales volume of several models. Some models exceeded planned sales thanks to higher selling prices or greater quantities sold.

Uploaded by

ScribdTranslationsCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as PDF, TXT or read online on Scribd

/ 5

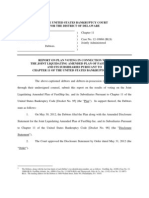

Example: Analysis of Variations. Price vs Volume.

Budget for the month of April

Price Cost Margin Vol. Vol.

Model Quantity Margin

Unitary Unitary Gross Sales Cost

XPG-01 120 $30 $15 50% $3,600 $ 1,800 1,800

XPG-02 130 $ 35 $ 16 54% $ 4,550 2,080 2,470

XPG-03 190 $25 $ 14 44% $ 4,750 $2,660 $ 2,090

XPG-04 140 $ 28 $ 16 43% $3,920 $2,240 $ 1,680

XPG-05 150 $ 33 $ 18 45% $ 4,950 $2,700 2,250

XPG-06 90 $ 40 $ 22 45% $3,600 $1,980 1,620 dollars

XPG-07 80 $ 45 $ 29 36% $3,600 $2,320 1,280

XPG-08 110 $ 15 $ 10 33% $1,650 $1,100 $ 550

XPG-09 150 18 dollars $10 44% $ 2,700 $ 1,500 $1,200

XPG-10 100 $ 12 $7 42% $1,200 $ 700 $500

XPG-11 115 $ 33 $ 19 42% $3,795 $2,185 $1,610

XPG-12 115 $39 $ 22 44% $ 4,485 $ 2,530 $1,955

XPG-13 130 $ 43 $23 47% $5,590 $2,990 $ 2,600

TOTAL 1,620 TOTAL $ 48,390 $ 26,785 $21,605

Real Sales of April

Price Cost Margin Vol. Vol.

Model Qty Margin

Unitary Unitary Gross Sales Cost

XPG-01 91 $ 25 $15 40% $ 2,275 $1,365 $ 910

XPG-02 141 $ 30 $ 16 47% $4,230 $2,256 $ 1,974

XPG-03 178 $ 29 14 dollars 52% $ 5,162 $2,492 $ 2,670

XPG-04 160 $28 $ 16 43% $4,480 $2,560 1,920

XPG-05 162 $ 33 $ 18 45% $ 5,346 $ 2,916 $ 2,430

XPG-06 100 $ 40 $ 22 45% $ 4,000 $ 2,200 $ 1,800

XPG-07 50 $ 46 $29 37% 2,300 $1,450 $850

XPG-08 115 $ 18 $10 44% $2,070 $ 1,150 $920

XPG-09 170 $ 22 $10 55% $3,740 $1,700 $2,040

XPG-10 84 $ 12 $7 42% 1,008 $588 $ 420

XPG-11 150 $ 31 $ 19 39% $ 4,650 $ 2,850 $1,800

XPG-12 112 $ 38 $ 22 42% $4,256 $ 2,464 $ 1,792

XPG-13 160 $ 35 $ 23 34% $ 5,600 $3,680 $1,920

1,673 TOTAL $ 49,117 $ 27,671 $ 21,446

GLOSSARY Diff $ 727 $ 886 -$ 159

Variation in Selling Price

(Actual Selling Price – Budgeted Selling Price) x Actual Units Sold

Variation in sales volume (number of physical units)

(Actual Units Sold - Budgeted Units) x Budgeted Unit Profit

Margin

Gross%

50%

54%

44%

43%

45%

45%

36%

33%

44%

42%

42%

44%

47%

45%

Margin Var. Effect

Var. Vol Comment

Gross % Price Total

40% -$ 455 -$ 435 -$890 The decline in sales is due to a combined effect of reduction

47% -$705 $ 209 -$496 The decline in sales is mainly due to a decline in the

52% $712 -$132 $580 The decline in sales is mainly due to a fall in the

43% $0 $ 240 $ 240 The decline is due to a reduction in the units sold.

45% $0 $ 180 $ 180 The decline is due to a reduction in the units sold.

45% $0 $180 $180 The drop is due to a reduction in the units sold.

37% $ 50 -$ 480 -$430 Although it was sold a little more expensive than budgeted, the

44% $ 345 $ 25 $ 370 The increase in sales was mainly due to a higher

55% $ 680 $ 160 $ 840 The increase in sales was mainly due to a greater

42% $0 -$80 -$80 Although it was sold without discount, the units fell re

39% -$ 300 $ 490 $ 190 Despite a lower selling price, the discount boosted the

42% -$ 112 -$51 -$ 163 Both the drop in price and a slight reduction in units

34% -$ 1,280 $ 600 -$680 The decrease is due to a reduction in the selling price.

44%

-$ 1,065 $906 -$ 159

o

Volume and price action.

the price.

the price.

The units fell compared to the budget, dragging sales down.

or selling price.

or selling price.

affecting the budget by dragging sales down.

physical sales exceeded the budgeted amount, which generated a higher level of income.

Aged produced the drop in income.